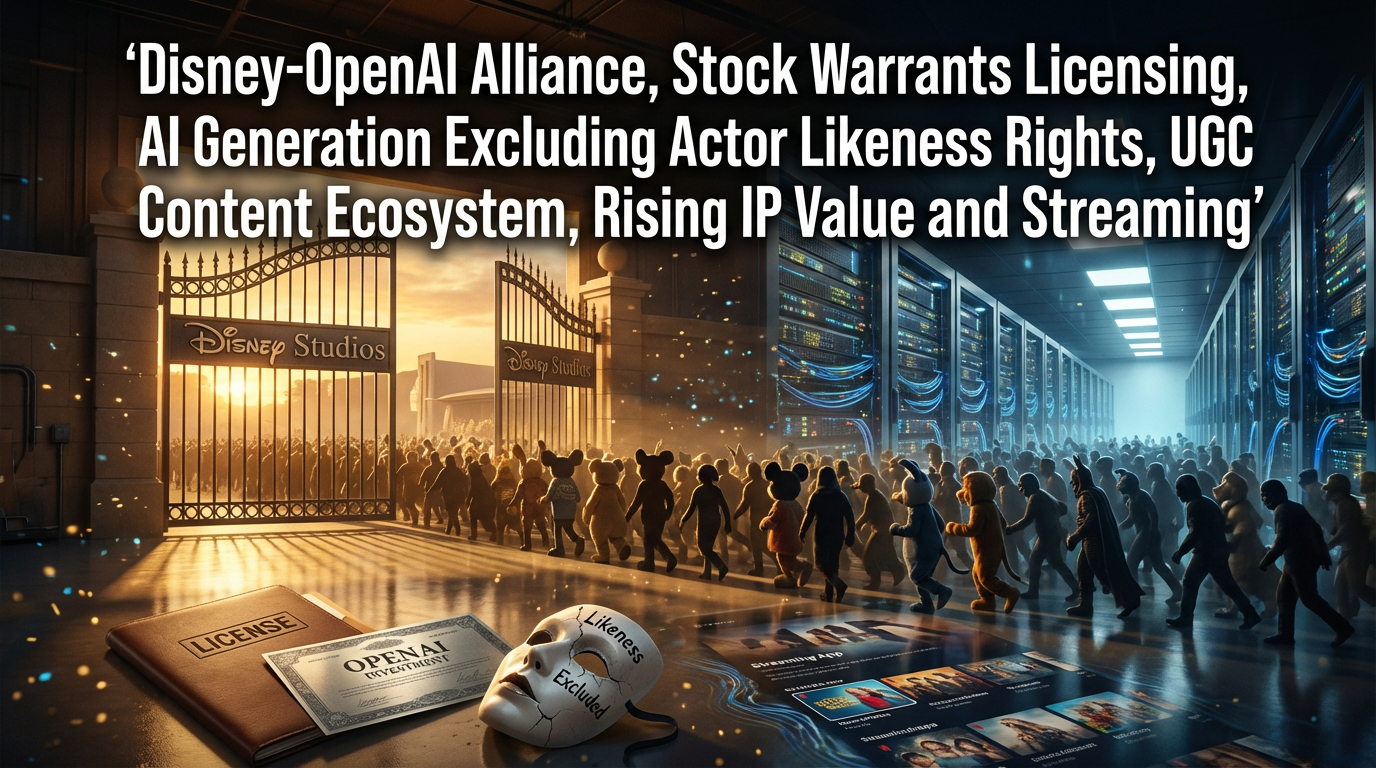

● Disney-Unleashed-AI-OpenAI-Billion-Dollar-Deal-200-Iconic-Characters-Exclusive-2026-Content-War-Shift

Why Disney Officially Declared “Use My Characters Freely with AI”: OpenAI’s $1 Billion Investment + 200 Character Licenses That Will Rewrite the Rules of the “Content War”

This article firmly includes exactly three things.

1) Why the Disney–OpenAI deal structure uses “stock purchase options instead of cash” (this is where the outcome is decided).

2) What will be possible/impossible starting in 2026 (excluding actors’ likeness rights carries major implications).

3) From a global economy perspective, how this deal reshapes markets (streaming, advertising, creators, IP value).

Plus, I’ll separately summarize the “truly important point” that other news coverage tends to overlook (Disney didn’t put down the sword; it changed the scabbard).

1) One-line breaking news: Disney–OpenAI, the first official alliance between Hollywood and generative AI

On December 11, 2025 (based on the original source), Disney announced a partnership with OpenAI.

The key takeaway is that it allows 200+ character assets from Disney/Pixar/Marvel/Star Wars to be officially generated in ChatGPT and Sora 2.

Why this is huge is that it’s close to the first case of resolving a long-running standoff between the AI industry and the media industry—previously defined by “unauthorized training/unauthorized generation”—through a contract.

2) Deal core point summary (for fact-checking): What becomes possible, and what is blocked

What becomes possible (starting in 2026)

Using Disney characters and related elements (costumes, props, vehicles, backgrounds, etc.) to generate and share images and short-form videos of about 30 seconds.

Includes major franchises such as Mickey Mouse, The Little Mermaid, Cinderella, The Lion King, Zootopia, Beauty and the Beast, and more.

Also includes Marvel (Iron Man/Thor/Captain America) and Star Wars (Darth Vader/Yoda, etc.).

What is not possible (the rights defense line)

Live-action actors’ likeness rights/voice rights are excluded.

Example: Iron Man is allowed in the comics version or helmeted version, but generation that inserts Robert Downey Jr.’s face is not allowed.

It’s a structure where Disney opens “character IP” while tightly locking down “human actor rights.”

Term and exclusivity

The licensing agreement is for 3 years.

From 2026, OpenAI receives exclusivity for 1 year (after that, similar agreements with other AI companies become possible).

This one-year exclusivity is a highly aggressive “growth booster” for OpenAI from a market-share perspective.

3) The money flow is unusual: licensing fees paid via “stock purchase options instead of cash”

Typically, IP licensing is cash-based, but this deal broke the rule.

OpenAI agreed to pay Disney’s licensing fees in the form of stock purchase options (stock options/the right to purchase shares in the future).

In other words, OpenAI minimized immediate cash outflow while securing Disney-level super IP,

and Disney chose to capture “OpenAI’s future value” together rather than “cash right now.”

Separately, Disney decided to make a $1 billion (about 1.5 trillion KRW) equity investment in OpenAI.

This is interpreted as a record-level investment by a Hollywood major into an AI model developer.

This structure is not just an entertainment collaboration; it is effectively “a content company bringing an AI infrastructure company into its strategic asset portfolio.”

When U.S. interest rates are in a high range, cash-flow management becomes even more important,

and OpenAI crafted a deal that preserves cash while pulling growth (users/content/brand) forward.

4) Why Disney suddenly became this “open”: the answer is “engagement”

The keyword Disney CEO Bob Iger repeated was engagement.

These days, the content success formula is “spreads like a meme on social media → fans create derivative works → algorithms amplify it,”

but Disney’s strong IP protection arguably blocked that viral loop.

This agreement is a decision to “let fans officially play with the characters,”

and it even mentions a direction of selectively sharing some results on Disney+.

This can also be read as a move to transform streaming from a simple viewing service into a “fan creation platform.”

Ultimately, Disney’s goal is not simple promotion,

but more time spent inside the streaming platform + attracting younger audiences + supplying UGC (user-generated content).

If this works, Disney+ can play a different game from Netflix: a fandom-based creation ecosystem.

5) The real purpose of “allowing”: creating a “baseline” to reduce unauthorized use

This is why the timing was described as exquisite in the original source.

Right before the announcement (12/10), Disney sent Google a warning to stop unauthorized use,

and earlier it even filed a lawsuit against Midjourney.

In other words, Disney didn’t “embrace AI”; it’s closer to “embracing only AI that can be controlled.”

The point is this.

If people are going to make similar things anyway, bring them into an official license and draw a clear “legal line.”

Once that line is drawn, it becomes easier to pressure anything created outside it as “unauthorized generation/unauthorized distribution.”

This is a classic strategy in the IP business.

When complete blocking becomes impossible, “designating a standard platform” becomes the strongest defense.

6) What OpenAI gains: not “technology,” but a “distribution network + super IP”

It’s significant that OpenAI secured Disney as an enterprise customer,

but the bigger win is that it creates a powerful legal space where AI videos featuring Disney characters can be made.

As generative AI capabilities become commoditized, differentiation shifts from “model performance” to “content/data/rights.”

And Disney IP is a massive moat asset that competitors can’t easily touch.

With the one-year exclusivity starting in 2026, the user-growth momentum (especially for video generation) could be quite strong.

This is a signal flare that platform competition in the AI market is shifting from “technology competition” to “IP alliance competition.”

7) The message to the media/content industry: in the AI era, IP value rises rather than falls

If AI drives production costs toward zero, supply (content) explodes.

Then, paradoxically, what becomes scarce is “originality and worldbuilding,” and that is IP.

So this agreement is not simply “Disney opened its characters,”

but a reference case showing how IP owners can monetize, control, and expand in the AI era.

Economically,

IP is essentially a “brand asset” that tends to retain pricing power even in inflationary times,

and AI can become a replication engine that multiplies that IP faster.

Ultimately, Disney chose “don’t treat the replication engine as an enemy—make it my engine.”

8) (Important) A point other news mentions less: Disney isn’t “opening up,” it’s building an “operating system (OS)”

From here is the real core point.

On the surface it looks like “fans can freely create derivative works,” but Disney’s design is a bigger picture.

Point A. Disney wants to pull UGC into the “production process,” not just “distribution”

Saying it will share some content on Disney+ implies that,

in the long run, Disney can build a pipeline to edit/review/recommend/revenue-share UGC.

If that happens, Disney becomes not a streaming service but the operator of an “IP-based creator economy.”

Point B. “Excluding actors’ likeness rights” foreshadows the standard for future “digital human contracts”

Excluding actors this time isn’t mere consideration; it’s compartmentalization for the next stage (three-party contracts among actors/studios/AI platforms).

Later, when actors participate, an entirely different market opens with separate royalties/usage scope/term/territory.

Point C. Paying via stock purchase options is not about “cash flow” but a “lock mechanism for the alliance”

Cash payments can make parties strangers again when the contract ends,

but equity/options structures bind each side’s incentives for longer.

This is less a partnership and more a method of creating cohesion that is close to a “strategic merger.”

Point D. This deal is a sample case of “licensed data/licensed generation” that reduces AI regulatory risk

As governments around the world tighten generative AI regulation,

“rights-cleared generation (licensed generation)” is increasingly likely to become a baseline requirement in the enterprise market.

OpenAI can use the Disney case to expand more easily to other studios/publishers/game companies.

9) Market outlook (global economy + AI trend perspective): where the money could be

1) Streaming (Disney+) retention competition intensifies

If Netflix competed with “recommendation algorithms,”

Disney is more likely to create retention through “worldbuilding participation.”

2) Restructuring of the creator economy

If derivative creation on YouTube/TikTok moves from a “gray zone” to “license-based,”

platform revenue-sharing structures could also change.

3) Expansion of the advertising/brand collaboration market

If legal generation with official characters becomes possible,

a format where brands have “fans create short-form videos for my campaign” becomes real.

4) IP price re-rating

The more content overflows, the more expensive IP becomes.

This flow, separate from manufacturing-side issues like global supply chains, creates a structure where digital assets receive a “scarce-asset premium.”

5) Acceleration of enterprise AI adoption

Disney’s mention of API usage and enterprise adoption means that,

AI is moving beyond a “production tool” into a “company-wide operations tool.”

In this process, AI investment (capex/opex) will also increase, and generative AI budgets may rise to a core IT line item.

10) Checkpoints: what to watch over the next 6–12 months

During OpenAI’s 1-year exclusivity

How much actual user growth occurs (centered on video generation).

Whether a UGC channel/tab appears inside Disney+

Whether “selective sharing” ends as a test or becomes a fully developed platform feature.

Follow-on deals by other studios

What terms (cash vs equity/options, exclusivity period, whether actors are included) majors like Warner/Universal/Sony follow with.

Regulatory and litigation trends

The contract model isn’t a “get-out-of-jail-free card.”

How standards evolve for training data/style imitation/similarity judgments remains a continuing variable.

< Summary >

Disney invested $1 billion in OpenAI and allowed official generation of 200+ characters in ChatGPT and Sora 2 starting in 2026.

OpenAI paid the licensing fees not in cash but via stock purchase options, reducing cash outflow while securing super IP.

Disney may appear to be “opening up,” but in reality it designated a legal platform and created a baseline to pressure unauthorized generation.

This deal is likely to be a turning point where the conflict between generative AI and the media industry shifts from “exclusion” to “contracts and revenue sharing.”

Going forward, streaming retention, the creator economy, IP value re-rating, and enterprise AI adoption are expected to be reshaped together.

[Related posts…]

Analysis of Disney’s IP strategy shift and its impact on the content market

OpenAI’s platform competitiveness: the battleground in the generative AI era

*Source: [ 티타임즈TV ]

– 디즈니, 픽사, 마블 캐릭터로 AI생성 맘껏 하라는 디즈니, 왜?

● China Open Source AI Shocks Closed Giants, GLM 4 7 Agent Stability Surge, Manus Design View Editable Slides Disrupt Workflow

China-origin open-source AI is genuinely shaking up the “limits of closed models”: GLM 4.7 agent stability + Manus Design View’s ‘editable’ workflow revolution

This article contains exactly two key takeaways.

First, Zhipu’s GLM 4.7 breaks the fixed idea that “open source is only for demos,” showing that it has realistically caught up with measurable results in coding agents, tool use, and long-horizon execution.

Second, Manus’s Design View shifts AI images/slides from “generate once and done” to precise partial edits, text editing, and slide element-level editing, with a strong chance of changing real-world production workflows end-to-end.

And at the end, I’ll separately summarize the most important point (the point that actually makes money in real work) that other YouTube/news coverage usually doesn’t highlight.

1) Today’s core point news briefing (one line each)

[Model] Zhipu released GLM 4.7.

[Positioning] Designed not as “a model that looks smart in short chats,” but as coding-first + agent-friendly.

[Benchmarks] Noticeable gains in coding/agent categories, including SWEBench Verified 73.8% and Live CodeBench v6 84.9%.

[Key improvements] Focused on reducing common long-run failures: drift (context wobble), instruction-chain collapse, and tool-calling mistakes.

[Distribution] Broader access via Z.AI API + OpenRouter → easier for global dev teams to “plug in” immediately.

[Product] Manus updated Design View.

[Problem solved] Attempts to solve the infamous AI image issue where “regenerating changes everything” through local editing (partial edits).

[Slides] Converts AI slides that become frozen as images into assets editable at the element level (also emphasizes bulk edits support).

2) GLM 4.7: Why people say “open source has caught up”

2-1. The point is “agent stability,” more than “raw performance”

In real work, the pattern of how coding agents break usually looks like this.

It starts with a decent plan → tool/terminal/file changes accumulate midstream → at some point it forgets or contradicts earlier decisions → attempts to fix it make it even more tangled.

GLM 4.7 emphasizes a performance jump exactly in this zone: long-running execution + tool integration + accumulated decision-making.

This matters because when companies talk about “AI adoption” now, they’re measuring KPIs not on simple chatbots but on work automation (agents).

2-2. Coding benchmarks: the difficulty of “reading and fixing a codebase”

SWEBench Verified 73.8%

This metric matters because the model isn’t just cranking out a single function; it has to do:

understand an unfamiliar project structure → locate the bug → patch it according to conventions → pass tests.

Live CodeBench v6 84.9%

This track is often seen as closer to “real-world developer sense” because it demands constraints and edge-case handling like actual development.

SWEBench Multilingual 66.7%

They also emphasized a jump in multilingual code/issue-document environments, which is a fairly practical point for organizations with lots of global collaboration (issues/PRs/docs).

2-3. Terminal workflows: where an agent’s “mental resilience” shows

Terminal Bench 2.0 41% (mentioned as a big increase vs. before)

Terminal work is all about sequence, state, and output interpretation, so it’s essentially an “agent durability test.”

Improvement here can be read as:

instruction chains break less often, recovery plans after failure are better, and output-parsing mistakes decrease.

2-4. Tool use (browsing/context management): evaluated as a “system,” not a standalone model

Humanity’s Last Exam (tools enabled) 42.8%

Messaging that the jump is large when tools are enabled is quite candid.

It means it’s optimized under the assumption of external tools (browsing/context/execution), rather than “the model alone solves everything.”

On BrowseComp, they mention the default setting is in the 50s, rising to 67.5 with context management applied.

The hint here is simple.

This model’s value grows not from “just write better prompts,” but from an agent architecture with a context-management layer.

Tao² Bench 87.4 (interactive tool use)

Highlighted as a metric demonstrating strength in tool calls and interaction.

3) GLM 4.7’s real technical core point: Why three Thinking modes matter

GLM 4.7 packages reasoning control as an “agent feature.”

① Interleaved thinking

A structure that inserts reasoning before each response/tool call.

→ Reduces impulsive answers and improves the consistency of next actions.

② Preserved thinking

Designed to preserve the reasoning state even when turns change.

→ Mitigates drift (the phenomenon where decisions slowly wobble and the outcome collapses) in long tasks.

→ Fewer repeated re-reasoning passes may also reduce inference cost.

③ Turn-level thinking control

Adjusts “thinking intensity” based on difficulty.

→ Fast for easy tasks, deep for hard tasks.

In practice, this connects directly to cost/latency optimization.

4) From a developer’s perspective: 3 more realistic signals than “benchmarks”

4-1. The deployment path is production-friendly (Z.AI API + OpenRouter)

Even if a model is good, teams won’t use it if access is poor.

GLM 4.7 emphasized that it offers an API via Z.AI and can be called directly via OpenRouter.

This means it’s easy to swap into existing stacks, accelerating adoption.

4-2. It explicitly claims “coding-agent compatibility”

The tone suggests it was designed assuming it will be plugged into “think → act → tool → verify” loops, like Claude Code-style setups and other multi-step code-agent configurations.

Companies are increasingly trying to extract productivity from agents, and this ties directly into digital transformation investment.

4-3. It targets “messy real-world details” like UI/slide generation as improvement points

Details like accurate 16:9 slide layout aren’t flashy, but

they directly cut the cost of “humans fixing generated outputs,” which hits real efficiency head-on.

5) You also need to see GLM 4.7’s limits (reality check)

① For ultra-hard instant answers (zero-shot perfection), top closed models may still have an edge.

② Local deployment is heavy: full precision requires high-end hardware, and even quantized versions aren’t trivial.

③ In the end, enterprises buy “controllable + cost-predictable,” not “absolute strongest”

Open-weight or quasi-open approaches have major advantages in compliance, customization, and long-term cost control,

so in an environment burdened by interest rates, when CFOs start watching “AI operating costs,” they gain even more leverage.

6) Manus Design View: AI visuals/slides move from “generative” to “editable”

6-1. The problem definition is accurate: from prompt roulette to an editing workflow

The chronic disease of AI images is this.

It’s almost right → you want to change just one part (color/logo/furniture/text) → regenerate → everything changes → meltdown.

Manus Design View pushes, instead of “regenerate,” this flow:

select an area on the canvas (mark tool) → locally edit only that part → preserve the rest of the characteristics.

6-2. Photoreal editing: “consistency preservation” is the real difficulty

Manus highlighted photoreal work such as interiors using Google’s Nano Banana Pro, and

the key question is how well it prevents the “lighting/reflection/texture collapse” problem when partially editing.

In other words, editing is harder than generation, and Manus set value on the harder side.

6-3. Don’t leave text to image models; “editable overlay” is the practical answer

Broken text in AI images is basically a meme at this point.

Manus addresses this not by “making the model draw letters perfectly,” but by using

an editable text overlay on the canvas.

This is extremely rational in real work.

Branding/copy keeps changing until the very end, and handling that via regeneration each time destroys productivity.

6-4. Slides: directly fixes the fatal weakness of “image slides”

If AI generates slides as “images,” they look decent, but

the moment you need to fix one typo or one spacing issue and have to regenerate everything, they are instantly disqualified in real work.

Manus makes slides editable at the element level, and emphasizes

Before/After comparison and multi-select bulk edits.

Anyone who builds presentations in teams will immediately feel how big this is.

6-5. It’s not a speed improvement; it’s an “iteration speed” improvement

Generation taking 10–30 seconds is normal, but if partial edits reduce the number of regenerations, the total project lead time drops.

This is operational efficiency, and it becomes a measurable point in enterprise digital transformation outcomes.

6-6. Clear commercial-use/ownership terms are mandatory for B2B adoption

Manus explicitly stating ownership/commercial use is a classic “market expansion signal” intended to lower legal/compliance hurdles for enterprise adoption.

7) The “most important content” that other YouTube/news rarely says

7-1. GLM 4.7’s real weapon isn’t “scores,” but “open weights + agent operating cost”

Most content only talks about things like SWEBench scores.

But what actually triggers enterprise movement is this.

Token cost + failure rate + controllability when running agents all day

If open approaches become strong here via pricing/quotas/customization/vendor lock-in avoidance,

this shifts from simple model competition to a restructuring of the AI supply chain (cloud, semiconductors, platforms).

In today’s U.S.–China tech competition landscape, more “open models usable in real operations” shake up the market even faster.

7-2. Manus redefines ROI not as “generative AI,” but as “editable production assets”

The ROI of AI design is not determined by “generation speed,” but by

edit cost (labor) and communication cost (versioning/feedback loops).

Design View is designed to reduce those costs.

This is a structure that makes enterprises use AI more deeply in producing design/marketing/sales materials.

7-3. The next battlefield isn’t “model vs. model,” but “agent operating systems (context/tools/editing)”

GLM 4.7 emphasizing jumps from context management, and

Manus changing workflows with an editable canvas are the same trend.

Now the competition shifts from “who gives the smartest answer” to

who can finish work longer, more stably, more editably, and more cheaply.

When a winner emerges here, related companies’ global supply chains and enterprise IT spend flows move with it.

8) Practical adoption checklist (a viewpoint you can use immediately)

8-1. Teams that should consider GLM 4.7

Teams running coding agents/DevOps automation/test-fix loops where costs are becoming burdensome.

Teams running long tasks based on tool calls (browsing/terminal/context management).

Teams that dislike vendor lock-in and have compliance/customization needs.

8-2. Teams that should consider Manus Design View

Teams losing the most time due to “partial edits” of generated images (marketing/commerce/interiors/branding).

Teams that couldn’t use AI slides because, even if they looked great, they were “not editable.”

Organizations with lots of versioning/feedback loops (bulk edit features are especially important).

< Summary >

GLM 4.7 is a signal that open-source (open-family) models are catching up into real-use territory in coding agents, tool use, and long-horizon stability.

Manus Design View turns AI visuals/slides into not “generated outputs,” but editable production assets, changing the ROI of real-world workflows.

The real battlefield is shifting from model performance bragging to an “agent operating system” that includes context management, tool orchestration, and editable workflows.

[Related posts…]

Latest AI market trends: why enterprise adoption is accelerating and the next battleground

Open-source AI model war: changes in cost structures and vendor lock-in strategy

*Source: [ AI Revolution ]

– China’s New Open AI Shocks OpenAI: DESTROYS Closed Model Limits (Better Than DeepSeek & Kimi)