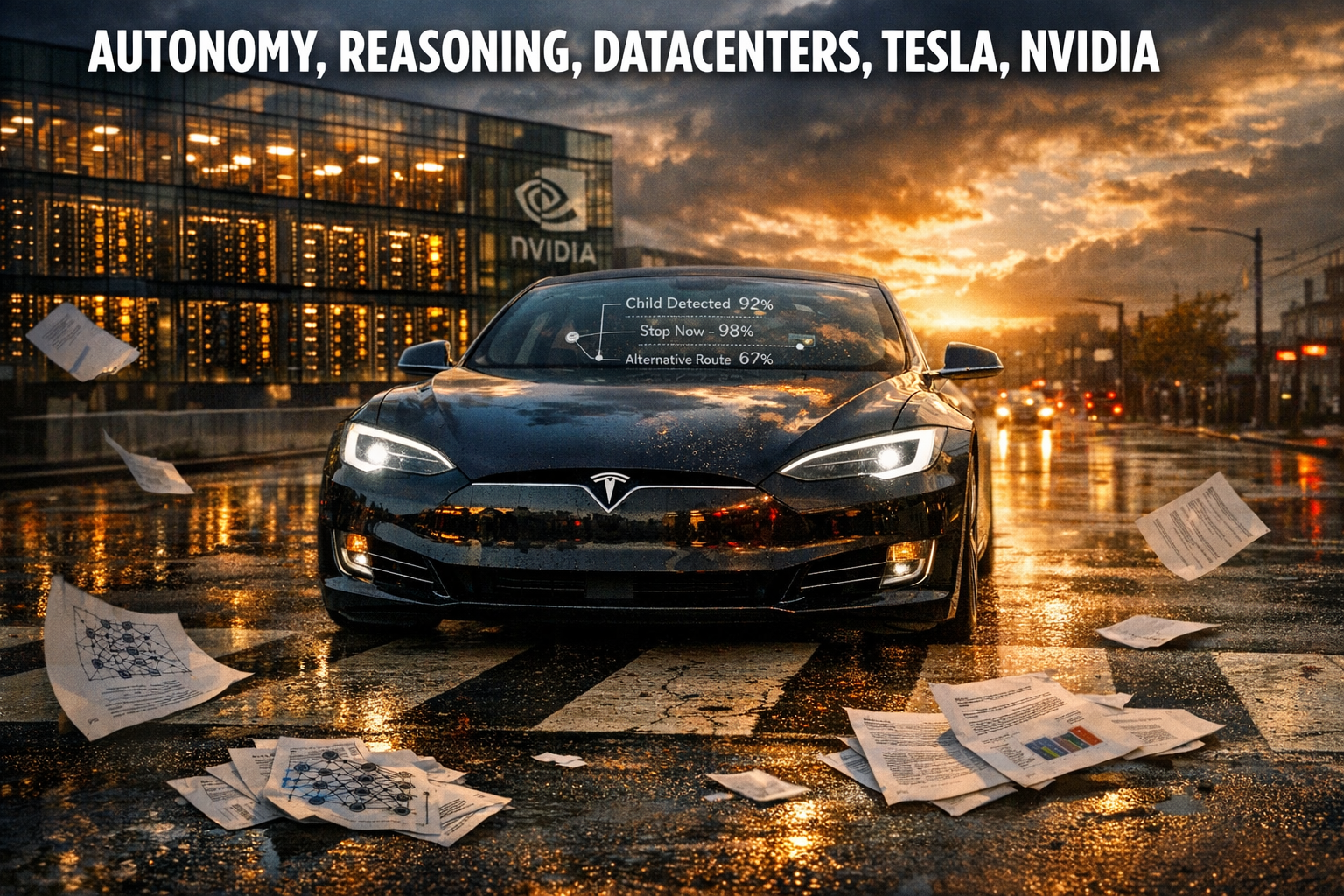

● Nvidias Reasoning Self Driving Bombshell Shakes Tesla Stock

The Actual Reason Tesla Shares Reacted to Nvidia’s “First Reasoning Autonomy”: Same Term, Different Time Axis

This note focuses on four points:1) What Nvidia specifically meant by “reasoning autonomous driving” at CES 2026.

2) Why Tesla’s rebuttal that it is “already deployed” is not semantic maneuvering.

3) Why the competitive locus is shifting from algorithms to power and compute infrastructure (at the ~2 GW scale).

4) An under-covered point: “reasoning” impacts safety, liability, and latency (delay), not only performance.

1) Key News Briefing (Structured Summary)

1-1. xAI announces a USD 20 billion (~USD 20B) AI data center campus in Mississippi

Elon Musk’s xAI is reportedly pursuing a large-scale data center campus in Southaven, Mississippi.

Upon completion, total compute power capacity is described as reaching approximately 2 GW, forming a “compute cluster” with existing Tennessee facilities.

Local government characterized it as the largest single economic development project in state history, emphasizing jobs and infrastructure expansion.

Key implication: AI competition is increasingly defined by infrastructure (data centers and power grids), not solely by model capability.

Given the linkage to interest rates, supply chains, and energy costs, AI capex is increasingly intertwined with macroeconomic dynamics.

1-2. Tesla launches Model Y “Standard Long Range” in Europe (demand testing via price/efficiency)

A new variant marketed as the “most efficient Model Y” in Europe based on range and energy consumption (kWh per 100 km) metrics.

Pricing positioning is a key variable; some outlets frame it as cheaper versus competing models, indicating a renewed attempt to set a low reference price to stimulate demand.

Canada pricing context is also relevant, as the launch price may appear meaningfully lower than in the U.S. on a perceived-value basis.

Tesla continues to apply region-specific, demand-driven pricing rather than uniform global pricing.

This aligns with typical macro-driven responses in an EV market shaped by demand normalization, subsidies, and interest rates.

1-3. The Netherlands: Tesla Model 3 ranks #1 in used EV transactions in 2025

Data indicates the Model 3 led the used EV market, with a sizable gap versus the #2 model.

Used market leadership can be interpreted as an aggregate signal of ownership experience (residual value, satisfaction, operating costs, charging convenience).

This suggests Tesla’s user experience positioning remains relatively favorable in parts of Europe.

2) Nvidia’s “First Reasoning Autonomous Driving” vs. Tesla’s “Already Deployed”: Why Both Can Be Correct

2-1. Market interpretation of “reasoning” = a vehicle that “thinks” more during driving

“Reasoning” is commonly understood as real-time deliberation, such as:

- Is the current speed appropriate?

- Is this the right moment to change lanes?

- Can the system jointly evaluate vehicles, pedestrians, bicycles, and merges to make a safer decision?

As a result, Nvidia’s CES framing of a “first” in reasoning-based autonomy can be interpreted as a breakthrough Tesla had not achieved, contributing to short-term equity volatility.

2-2. Tesla’s “reasoning already deployed” = decisions compressed during training, not debated during execution

In response to Bloomberg questioning, Tesla’s AI lead (Ashok Elluswamy) reportedly stated that reasoning is already deployed in FSD.

In Tesla’s framing, reasoning is less about in-drive deliberation and more about embedding judgment during training using large-scale real-world driving data (including accidents, near-misses, and long-tail events).

The operational objective is to deliver a policy that executes with minimal hesitation in real time, while “reasoning” is reflected in training depth and prior constraint formation.

2-3. Conclusion: same term, different time axis

- Nvidia emphasizes reasoning “inside the vehicle, in the moment,” selecting among alternatives during driving.

- Tesla emphasizes resolving judgment “before driving,” compressing decisions into a fast-executing policy for deployment.

Both can be accurately labeled “reasoning,” but the mismatch in time axis created confusion when the market treated the term as a single definition.

3) Why Nvidia Must Emphasize “Reasoning”: Differences in the Starting Line for Real-World Data

3-1. Nvidia constraint: lack of a directly operated fleet and multi-billion-kilometer real-road dataset

Nvidia is a leading supplier of autonomy platforms, chips, and software stacks, but it does not operate a Tesla-scale fleet that continuously generates real-world data.

This increases dependence on simulation-centric approaches and motivates positioning “in-drive reasoning” as a method to address simulation’s limitations in capturing long-tail real-world conditions.

3-2. Tesla advantage: a data flywheel that functions as a competitive moat

Tesla’s real-road dataset captures rare edge cases, human responses, and pre-incident patterns.

At scale, this can favor an approach where safe choices are learned and compressed during training rather than “debated” at runtime.

Accordingly, Tesla’s statement that reasoning is already deployed is logically consistent within its deployment philosophy.

4) The Most Material Point: Reasoning Is Primarily a Latency, Liability, and Safety Question

4-1. Reasoning competition is not only performance; it is latency (delay), responsibility, and safety

Nvidia-style “runtime deliberation” may improve plausibility in complex scenarios, but driving is continuous and time-critical at sub-second intervals.

In contested moments, who commits to a final decision and how quickly it executes directly affects safety outcomes.

More reasoning can increase not only perceived intelligence but also decision latency risk.

4-2. “Trolley problem” is product engineering, not philosophy

In extreme scenarios, the system cannot request additional time. Practical product design questions include:

- Does the system optimize for collision avoidance or loss minimization?

- Does it default to conservative deceleration/stop policies?

- What is the default behavior under uncertainty?

These choices feed directly into regulation, insurance, consumer trust, and commercialization timelines.

4-3. A single CES phrase moved the stock because autonomy is priced via narrative

Given limited standardized evaluation metrics for fully autonomous driving, investors respond to demos, keywords, partnerships, and declarative claims.

Nvidia’s “first” framing is easily transmitted and can create immediate narrative impact, while Tesla’s “already deployed” explanation is structurally more complex and slower to propagate.

This asymmetry increases short-term volatility.

4-4. The real battleground is power, chips, and data centers: AI infrastructure becomes a macro variable

xAI’s reference to ~2 GW-scale compute is not merely “a large data center.”

It implicates power infrastructure, substations/transmission, regional economic development, energy pricing, and corporate capex simultaneously.

This trend connects to U.S. macro conditions, inflation and rate paths, and global supply chain demand for power equipment, cooling, and semiconductors.

AI is increasingly an economy-wide industrial reconfiguration, not only a technology-sector issue.

5) Investor/Operator Checklist (What to Watch Next)

- Nvidia: degree of productization of “in-drive reasoning” (deployment scope, safety cases, latency design).

- Tesla: what “more reasoning” after FSD v14.2 concretely means (prediction, planning, verification modules).

- xAI: execution variables for the ~2 GW project (power purchase agreements, grid expansion, cooling architecture, commissioning timeline, regulatory and cost constraints).

- Europe/Canada pricing: how Tesla uses price elasticity as demand weakens (margin versus share trade-offs).

- Used-vehicle data: which regions maintain residual value (signal of brand trust and demand quality).

< Summary >

Nvidia’s “first reasoning autonomous driving” and Tesla’s “already deployed” describe different time axes (runtime deliberation vs. training-time compression), creating definitional confusion.

Nvidia’s positioning reflects a strategy shaped by comparatively weaker access to real-road fleet data, emphasizing simulation and runtime reasoning.

Tesla’s approach leverages large-scale real-world data to compress judgment into fast execution and reduce hesitation during driving.

The core evaluation dimension is not “reasoning performance” alone, but latency, default safety policies, and liability structure; AI competition is expanding into power and data center infrastructure.

[Related links…]

- Reasoning and autonomy: safety and liability structure as the key variable

- https://NextGenInsight.net?s=autonomous%20driving

- The 2 GW data center era: how AI infrastructure influences rates and inflation

- https://NextGenInsight.net?s=data%20center

*Source: [ 오늘의 테슬라 뉴스 ]

– 엔비디아의 ‘최초’ 발표, 정말 새로운 걸까? 테슬라는 이미 배포 중이라는 말의 의미는 ?

● Steady Unemployment, Hot Wages, Rate Cuts Delayed

US Employment Data: “Headline Stability, Underlying Friction” — Why Markets Remain Cautious Despite a 4.4% Unemployment Rate (Including FOMC and Rate-Cut Scenarios)

This report covers:1) Why a 4.4% unemployment rate is reassuring, yet also potentially cautionary

2) How weaker payroll growth and a rebound in wage growth create interpretive tension

3) How this release reduced expectations for FOMC rate cuts (and what probability shifts signal)

4) The variables markets are prioritizing over employment data

5) A commonly missed point: the nature of labor-market cooling and the AI investment cycle can alter the rate path

1) Flash Summary: Three Key Figures From This US Jobs Report

1) Unemployment Rate: 4.4%

- Below consensus (4.5%), reducing near-term concerns about an unemployment “shock.”

- The 4.5% level is widely treated as a psychological threshold; remaining below it supported sentiment.

2) Nonfarm Payrolls: Below expectations (implied ~50k range)

- Payrolls increased, but not at the pace markets associate with a clearly resilient labor market.

- The miss reinforces signals of labor-market deceleration.

3) Wage Growth: 3.8% (vs. 3.6% expected)

- The rebound complicates the narrative.

- If employment softens, wage growth is typically expected to cool as well, supporting disinflation and easing. A wage rebound reduces confidence that inflation pressures are fully contained.

2) Standard Market Read: “No Employment Shock, but Rate Cuts Move Further Out”

[Interpretation A: Unemployment at 4.4% indicates the labor market is still holding]

- A lower unemployment rate reduces the probability of a rapid growth downturn.

- This also reduces the Fed’s urgency to adjust policy.

[Interpretation B: Payrolls below expectations indicate cooling is underway]

- Weaker hiring suggests firms are becoming more cautious.

- The signal points to slower growth, not necessarily recession.

[Interpretation C: Wage growth rebound to 3.8% raises upside inflation risk]

- This is a key concern for the Fed.

- Wages can transmit into services inflation (especially ex-shelter services), potentially reintroducing persistent inflation dynamics.

Net implication:

- “No labor-market breakdown” plus “firmer wages” weakens the case for near-term easing.

- The market’s preferred scenario of “soft landing with rapid rate cuts” becomes less clear.

3) FOMC and Rate Cuts: Why Probabilities Matter

- The implied probability of a rate cut at the January FOMC moved from 13.8% to 11.6%.

- The significance is not the magnitude alone, but the reinforcement of a baseline view: holding rates is increasingly treated as the default.

Two common conditions for the Fed to cut:

1) A clear deterioration in employment, or

2) Convincing disinflation (CPI/PCE reaching a comfort zone)

This report did not materially strengthen (1), and the wage rebound may complicate (2). The result is a modest pushout of easing expectations.

Market linkage:

- Shifts in rate-cut expectations typically transmit to the USD, FX, and US Treasury yields.

- A modest rise in Treasury yields is consistent with reduced near-term easing expectations.

4) Why Market Reaction Was Muted: Larger Variables Dominated

- The release was not extreme in either direction, and other event risks (legal or policy-related) drew more attention.

- Mixed signals—stable unemployment (supportive), firmer wages (hawkish), softer payrolls (growth-caution)—tend to reduce directional conviction.

5) Key Points Often Underemphasized

Point 1) The “type” of labor-market cooling matters: cyclical recession vs. policy/structural drivers

- Potential contributors cited include tariff-related policy, shutdown risk, immigration policy, and public-sector efficiency measures (workforce reductions).

- If employment softens due to non-demand drivers, it may not produce the same policy response as a demand-led downturn.

Point 2) Wage reacceleration increases the risk of persistent services inflation

- Markets often focus on headline CPI, while the Fed is particularly sensitive to sticky services inflation.

- Wage growth at 3.8% can delay confidence that inflation is durably contained, potentially deferring easing by one or more meetings.

Point 3) The composition of US growth is shifting: the AI investment cycle can distort labor and inflation paths

- AI-linked private fixed investment may support growth.

- Over the medium term, productivity gains could be disinflationary; however, in the near term, data centers, power demand, semiconductors, and cloud capacity can intensify capex and create localized wage pressures.

- This can support growth while reducing urgency for rapid rate cuts.

6) Investor Checklist: What to Monitor Next

1) CPI and PCE (especially core and services components)

- Even without labor-market deterioration, sufficiently improved inflation prints can allow “insurance” easing.

2) Fed communication and leadership dynamics (guidance risk)

- Market pricing can react more to messaging than to incremental data changes.

3) US Treasury yields (10-year) and the USD

- A retreat in rate-cut expectations can support yields and the dollar; mixed macro inputs can blur short-term signals.

4) Global slowdown vs. continued US outperformance (“US exceptionalism”)

- Persistence of this divergence can increase FX volatility and influence emerging-market flows.

7) One-Line Conclusion

- Unemployment stability reduced immediate labor-shock risk; firmer wage growth reduced confidence in rapid disinflation; softer payrolls signaled cooling without confirming recession. Near-term market sensitivity is likely to remain centered on CPI/PCE and Fed communication.

< Summary >

- Unemployment at 4.4% eased labor-shock concerns.

- Nonfarm payrolls missed expectations, leaving a cooling signal.

- Wage growth rebounded to 3.8%, reviving inflation concerns and modestly pushing back rate-cut expectations.

- The release primarily reduced the rationale for near-term Fed action; key catalysts shift to CPI/PCE and policy communication.

[Related Articles…]

- https://NextGenInsight.net?s=unemployment-rate

- https://NextGenInsight.net?s=interest-rates

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [LIVE] 미국 고용지표 심층분석 : 실업률 쇼크 올까? [즉시분석]

● Expedia Surges 70, Travel Bears Crushed, Wall Street Eyes 2026 Re-Rating

Expedia (EXPE) Rebounds 60–70%: Three Shifts That Reversed the “Travel Is Over” Narrative, Plus 2026 Wall Street Scenarios

This note consolidates four items:

① Why travel demand has remained resilient despite high rates and elevated inflation,

② The core earnings/structural drivers behind Expedia’s 60–70% rebound over six months,

③ Why some sell-side firms are again positioning the name as a potential 2026 top pick (by institution),

④ A set of under-discussed, structurally important factors (beyond headline risks).

1) Key takeaway: “Travel may be moderating, but ‘travel platforms’ are strengthening”

The central point is not anecdotal crowding; it is that travel demand is shifting in form rather than disappearing, and that this shift disproportionately benefits OTAs (online travel platforms).

Expedia’s model spans flights, lodging, car rentals, and activities—capturing search, comparison, and booking across the end-to-end travel journey.

2) Direct catalysts for the 60–70% rebound: improved results and a more favorable profitability structure

2-1. More important than revenue growth: a phase where profit growth outpaces revenue growth

Recent quarters exceeded consensus on revenue and earnings, with post-earnings price action accelerating the rebound.

However, the primary focus has been operating leverage driven by:

cost discipline + platform efficiency + brand rationalization.

2-2. Early improvement in three legacy weaknesses

① Marketing expense intensity → increased efficiency and tighter controls

② Complex brand architecture → consolidation and simplification

③ Lower profitability vs. peers → improving conversion and operating efficiency

3) Why travel holds up amid high rates and inflation: consumption is shifting from “cutting” to “optimizing”

Travel spending is moving away from premium hotels and packaged tours toward:

value-oriented lodging, self-built itineraries, and more time spent on price comparison.

This shift is structurally favorable for OTAs.

As choice sets and trip combinations become more complex, the value of platform-based comparison, recommendations, and bundling increases.

Even if overall travel demand softens, “comparison and optimization” behavior can intensify, supporting platform engagement and monetization.

4) Wall Street scenarios through 2026: broadly neutral consensus with a subset of high-conviction bulls

4-1. Consensus view: broadly neutral (valuation and “prove it” posture)

Average price targets clustering near—or in some cases below—the current price reflect:

valuation concerns and a view that the next leg requires continued execution and results.

4-2. Bull case: “re-rating is not complete”

Evercore ISI (Mark Mahaney) has cited Expedia as a 2026 top-pick candidate with a $350 target.

Key pillars cited include:

① structural normalization in travel demand

② room-night growth

③ potential share gains versus competitors

4-3. Cautious stance: higher targets, but Hold/Neutral maintained

Firms including Goldman Sachs, Argus, and Oppenheimer have raised targets while keeping Hold/Neutral-type ratings.

The core rationale: fundamentals are improving, but the market has priced in a meaningful portion of the improvement.

5) AI angle: the AWS partnership is less about cost and more about “industrializing conversion”

The AWS relationship is framed as infrastructure modernization enabling improved search and recommendation systems, which can raise booking efficiency.

Market interpretation emphasizes this as a signal of evolution from a “travel booking site” to a data-driven technology platform, via:

personalized recommendations

more accurate demand forecasting

higher conversion rates

→ potential for structural margin expansion

In AI monetization, value often accrues to businesses that raise conversion across the full customer journey rather than to “models” alone.

OTAs are well-positioned given dense data across search, comparison, checkout, and repeat usage.

6) Risk considerations (investor framing)

6-1. Cyclicality: travel remains macro-sensitive

U.S. consumption slowing or rising global uncertainty typically increases volatility in travel equities.

Equity sensitivity to earnings and rates can amplify near-term drawdowns.

6-2. Valuation: improved fundamentals can still screen expensive

After a large rebound, expectations rise and quarterly execution is scrutinized more tightly.

The key question becomes:

whether the move reflects short-term momentum or durable profitability improvement.

7) Under-discussed structural points

7-1. The key shift is not “more travel,” but a change in how travel spending decisions are executed

The decision process has become longer and more complex due to optimization behavior.

Longer decision cycles can increase platform data capture and conversion opportunities.

7-2. Expedia’s core product is not “travel inventory,” but the decision interface

While travel is experiential, the final payment step is highly rational and comparison-driven.

The winner is the platform used at the “last comparison” stage; Expedia is positioned to compete for that moment.

7-3. The AWS impact is not “cloud migration,” but a repeatable conversion engine

AI-driven improvements can translate into:

better advertising efficiency (ROAS) → higher repeat rates → membership expansion → cross-sell (air/lodging/activities)

This linkage can influence valuation more meaningfully in 2026 scenarios than near-term headline results.

< Summary >

Expedia has rebounded 60–70% since the second half of 2025, supported by profitability-structure improvement rather than revenue growth alone.

In a high-rate, high-inflation environment, travel spending has shifted from “cutting” to “optimizing,” which structurally favors OTA platforms.

Wall Street consensus is broadly neutral, while select firms argue that re-rating potential remains into 2026.

AWS-enabled modernization is viewed less as cost reduction and more as a pathway to personalization, forecasting, and conversion gains that could reshape longer-term margin structure.

[Related Links…]

Interest-Rate Inflection Signals: Three Early Shifts Observed in Asset Markets

*Source: [ Maeil Business Newspaper ]

– [어바웃 뉴욕] “주가 상승률에 웃음만” 60% 반등의 주인공 ‘익스피디아’ | 길금희 특파원