● Tariff Chaos Sparks Market Shock Tesla Quietly Unleashes Steering Wheel-Free Robotaxi Unboxed Mass Production Pivot

Amid a Tariff-Driven “Market Shock,” Tesla Quietly Changed the Game: “Hundreds” of Cybercabs (Robotaxis) + Indications of Full-Scale Adoption of the Unboxed Manufacturing Process

This report focuses on three points:

1) Why uncertainty around US tariff policy has escalated into a broad risk-asset sell-off, and how this can create opportunity for investors

2) The significance of a “decisive change” observed in Palo Alto Cybercab sightings (removal of steering wheel and side mirrors) as a signal for regulation and commercialization

3) The implications of testimony suggesting “hundreds of units” inside Giga Texas and full implementation of the Unboxed process for cost, throughput, and margin structure

1) Today’s Market Headline: Volatility Shock Driven by “Tariff Policy Uncertainty”

Key news flow

- After the US Supreme Court constrained Trump’s broad authority over reciprocal tariffs, investors interpreted the move as a break in policy continuity.

- Trump subsequently referenced a “universal 10% tariff on all imports,” then signaled it could rise to 15%, amplifying market instability.

- Europe indicated possible countermeasures (e.g., suspending trade agreement baselines), increasing concern over retaliation cycles.

Nature of the market shock

- The primary risk is not the tariff level itself, but uncertainty: the perception that rules can change abruptly.

- For corporates, the lack of stable assumptions undermines supply-chain planning, cost management, and pricing pass-through strategies, encouraging more conservative investment, hiring, and inventory decisions.

- Growth and technology equities, with valuations more dependent on distant cash flows, tend to reprice first in such regimes.

Investor takeaways

- In high-volatility periods, high-quality companies can decline alongside the broader market.

- For long-duration assets with validated competitive positioning, valuation compression can improve entry points.

- The key analytical question is whether the drawdown reflects fundamental impairment or a macro-driven risk-off repricing.

2) Cybercab Sighting: Why “No Steering Wheel + No Side Mirrors” Is Material

Observed changes (per source description)

- The steering wheel is not visible in the cabin.

- Occupant behavior suggests no active driving involvement (e.g., handling paperwork).

- Side mirrors appear fully removed.

- Wheel covers appear larger with a more conspicuous gold-toned finish.

Why these changes matter

- Removing the steering wheel is typically among the last symbolic and practical steps in moving toward unsupervised autonomy or an operating design closely aligned with it.

- Eliminating side mirrors signals confidence in a camera-based vision system and may indicate a move toward design freeze for a production-intent configuration.

Regulatory and business-model implications

- The core value proposition of robotaxis is not incremental unit sales, but maximizing revenue-generating utilization per vehicle.

- If robotaxis scale commercially, Tesla’s narrative shifts from an automaker toward a platform and mobility-network operator.

- For market recognition of this shift, regulatory approvals and operational metrics (miles, incident rates, intervention rates) must converge.

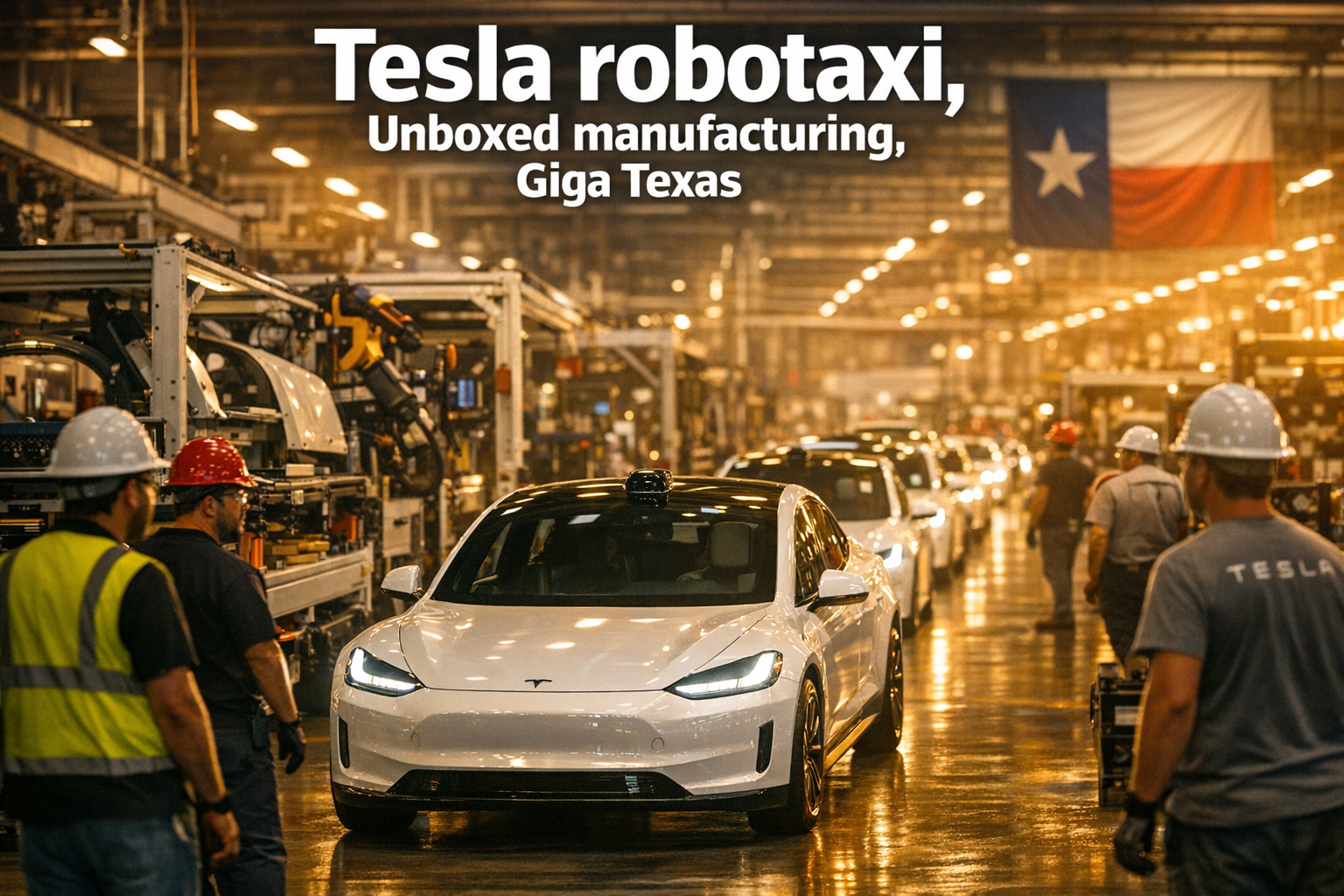

3) Robotaxi Tracker: The Signal in the Gap Between “31 Sighted” and “Hundreds Inside the Plant”

Visible count

- A robotaxi tracker cites approximately 31 officially sighted vehicles.

The higher-information data point may be inside the factory

- Drone operator Joe Teggmaier states there are “hundreds” of units inside Giga Texas.

- The discrepancy between external sightings and internal inventory suggests the phase may be shifting from public demonstrations to ramping production capacity.

Investor checkpoints

- If production at scale is occurring, the next question is when, where, and under what constraints operations begin.

- The critical path is the regulatory sequence from technology demonstration to limited operations to commercial operations.

- Equity markets typically respond more to operating authorization and revenue recognition than to production claims alone.

4) Indications of Full Unboxed Process Adoption: A Pivot Point for Cost and Throughput

Unboxed process as described

- The Cybercab is divided into five primary modules produced in parallel and then joined.

- Modules: front section; central section with structural battery pack; rear section; left and right carbon-tube structures (2), totaling five components.

Why this can be structurally significant

- Traditional automotive production is optimized around long, sequential assembly lines.

- A parallelized approach can reduce bottlenecks and shorten takt time, supporting higher throughput.

- Potential outcomes include lower unit cost, higher capacity, and more efficient factory layouts.

Practical considerations

- The magnitude of cost and productivity impact depends on whether Unboxed is partially or fully implemented.

- Joint quality (precision, durability) and serviceability (repair complexity) become key variables in commercialization.

- Even with faster assembly, constraints may shift to supply chain (batteries, cameras, compute) and regulatory approval timelines.

5) Musk’s Message: “Time Allocation Is Primarily Engineering and Production”

Stated message

- Musk indicated on X that most of his time is focused on product engineering and manufacturing processes.

Market signal

- In periods of elevated noise and controversy, markets demand evidence of execution.

- Emphasizing engineering and production focus can be interpreted as intent to meet near-term production targets referenced in the same context.

6) Key Points Often Underweighted in Coverage

Point A: Manufacturing scale may monetize earlier than unsupervised autonomy

- Attention is concentrated on unsupervised FSD performance; however, equity value is often more directly affected by unit economics and output.

- If Unboxed is effectively deployed at scale, Tesla could reshape margin structure through cost leadership and manufacturing leverage even before robotaxi commercialization.

Point B: Rising tariff uncertainty increases the premium on localized manufacturing

- In tariff and trade-friction environments, local production becomes a stronger hedge than global supply-chain optimization.

- Evidence of rapid ramp at Giga Texas should be evaluated as both a product milestone and a geopolitical risk mitigant.

Point C: “31 sightings” may signal operating-system buildout rather than low volume

- Small fleets running repeated routes often reflect operational maturation (maintenance, charging, dispatch, insurance/liability, customer experience), not only algorithmic testing.

- Competitive advantage may be determined by city-scale operations capability in addition to autonomy software.

7) AI-Era Investment Lens: The Question Matters as Much as the Answer

- A core observation is that decision-makers may not yet know which questions are most important.

- Applied to investing, the relevant question is less about daily price moves and more about whether the company can sustain pricing power and production advantage over a 2–3 year horizon.

8) Forward Checklist: What to Confirm in Upcoming News Flow

- (Regulation) Scope and geography of on-road permissions for vehicles without steering wheels

- (Operations) Formal disclosures on dispatch/control centers, insurance, and liability frameworks

- (Manufacturing) Official evidence of Unboxed deployment (process footage, line design, productivity metrics)

- (Financials) Timing of production expansion translating into recognized revenue and margins

- (Macro) Whether tariff policy re-ignites inflation pressure and alters the Fed rate path

US tariff policy volatility increased market instability and pressured risk assets.

Separately, Palo Alto sightings of a Tesla Cybercab without a steering wheel or side mirrors suggest progression toward a commercialization-ready configuration.

More consequential than the tracker’s 31 sightings are claims of “hundreds” of units inside Giga Texas and indications of full Unboxed adoption, which could affect unit cost, production speed, and margin structure.

The relevant framework is to evaluate autonomy performance together with manufacturing scale, operating readiness, and the regulatory sequence.

[Related Posts…]

- Tariff volatility: consolidated view of impacts on global equities and FX

- Robotaxi commercialization: regulatory, insurance, and operating-model hurdles in one view

*Source: [ 허니잼의 테슬라와 일론 ]

– [테슬라 독점 속보] 기가텍사스 내부 공개! 테슬라 ‘언박스드’ 공정 활용 사이버캡 ‘수백 대’ 생산 중!● Altcoin Bloodbath, US Bitcoin War-Chest 2026

Altcoins: “99% Extinction”? How the 2026 “Bitcoin as a Strategic Asset” Theme Could Evolve (Clarity Act, Lummis Bill, SBR, Stablecoins, and Asset Tokenization)

This report covers:1) Why “99% of altcoins will disappear” is increasingly a structural outcome driven by regulation, fundamentals, and liquidity

2) The capital roadmap: 2024 ETFs → 2025 corporates (DAT) → 2026 SBR (Strategic Bitcoin Reserve)

3) A key market blind spot: the U.S. can accumulate Bitcoin through channels that do not require tax-funded purchases

4) Why stablecoins and asset tokenization are the infrastructure that determines altcoin survivability

5) The “surviving 1%” criteria individual investors should prioritize now

1) Key discussion headlines (single-line summaries)

Headline A. “99% of altcoins go to zero” is less a fear narrative and more a rational consolidation in a regime where regulation, fundamentals, and liquidity are simultaneously required.

Headline B. U.S. Bitcoin strategic-asset positioning is driven less by declarations and more by system design (Clarity) and accumulation pathways (seizure/purchase/mining).

Headline C. 2026 could be the year the SBR (Strategic Bitcoin Reserve) narrative resets the market’s upside expectations (pricing may respond faster to reactivation signals than to formal passage).

2) A structural interpretation of “99% of altcoins will disappear”

2-1. Altcoins function more like blockchain-native startups

Altcoins typically must prove “technology + network + utility.” In risk-on cycles, issuance proliferates; when cycles reverse, most fail. As with post–dot-com consolidation, exchange listings do not ensure survival.

2-2. The surviving 1% must meet all three: regulatory fit + real usage + liquidity

Regulatory fit: Without compliance viability, trading, listings, and institutional inflows face structural constraints.

Real usage (demand): Without persistent demand, narratives fade and maintenance costs dominate.

Liquidity (reasons for capital to remain): Without durable liquidity, assets may spike in uptrends but structurally decay in downtrends.

2-3. Why the “prime apartment” analogy is misleading, and a more appropriate framing

Real estate tends to be a market where most assets persist; altcoins are a market where most projects fail. A closer analogy is gold (Bitcoin) vs. silver (altcoins): silver can outperform in rallies but typically underperforms in drawdowns. Altcoins are structurally high-volatility, making selection risk decisive.

3) The core of Bitcoin “strategic-asset” positioning: SBR, the Lummis bill, and the Clarity Act

3-1. Roadmap: 2024 ETFs → 2025 corporates (DAT) → 2026 SBR

The proposed framework:

- 2024: Spot ETFs expanded institutional access

- 2025: Corporates integrate digital assets into holdings, payments, and treasury strategy (DAT: “digital-asset treasury” phase)

- 2026: Federal or state-level SBR narratives could raise the market’s perceived ceiling

This progression links directly to liquidity migration.

3-2. Lummis bill (accumulating 1,000,000 BTC over 5 years): the “reactivation signal” may matter more than passage

Markets often price expectations before outcomes. Even without enactment, renewed signals from political leadership, the Treasury, or Congress could expand volatility and re-rate expectations.

3-3. If “tax-funded purchases” are constrained, three accumulation pathways remain

1) Seizure (criminal/illicit proceeds)

2) Mining (direct federal mining is unlikely; policy can still shape a favorable domestic mining ecosystem)

3) Purchase (if direct tax funding is restricted, indirect accumulation via reserve-asset rebalancing logic, e.g., gold, may be debated)

The key point: viewing “purchase” as the only mechanism can understate the feasibility of strategic accumulation, as seizure/forfeiture channels can remain continuously active.

4) Under-discussed but material considerations

4-1. U.S. accumulation may already be progressing through enforcement capacity rather than legislation

A relevant interpretation is that the U.S. may have superior capabilities to secure access/control in complex legal contexts, even when adjudication timelines are long. Strategic reserves can be built not only by budgeted buying, but also by enforcement leverage and asset recovery.

4-2. Criminal-supply liquidation could create episodic sell pressure

In private-key-based assets, internal compromise and coercion risks can increase incentives to liquidate holdings rapidly. For investors, a useful framing is that short-term price weakness can reflect supply-structure changes rather than purely demand deterioration.

4-3. The Clarity Act’s practical role: laying the rails for SBR feasibility

State action requires clear legal classification, accounting treatment, auditability, and transaction infrastructure. The Clarity Act functions as institutional “rail-building,” and SBR narratives should be monitored in conjunction with such framework development.

5) Why stablecoins and asset tokenization determine altcoin survivability

5-1. Stablecoins create measurable demand in payments/settlement/remittances

Many altcoins fail due to insufficient real-world use. Stablecoins have clear utility and can reshape market-wide liquidity and trading plumbing.

5-2. Asset tokenization makes infrastructure competition tangible

This underpins platform competition (e.g., Ethereum vs. Solana):

- Solana: throughput/fees/user experience advantages

- Ethereum: trust, standards, and ecosystem depth

The market may be in an early “infrastructure build-out” phase where direction of completion and adoption matters more than past price performance.

6) Individual investor checklist: screening for “surviving 1%” altcoins

If fewer than 4 of the 6 are met, long-term survival probability declines materially:

1) Regulatory risk trending lower (security-status controversy, issuance structure, governance)

2) Connected to real demand: stablecoins, asset tokenization, payments

3) Developer/user metrics rising persistently (not one-off pumps)

4) Institutional-grade custody, transparency, and auditability

5) Network effects (if easily substitutable, price competition tends to erode value)

6) Appreciation driven by more than narrative: at least minimal usage, fees, or cash-flow-like fundamentals

7) One-sentence macro framing

In a transition from safe assets to risk assets, regulatory clarification tends to elevate Bitcoin’s “digital gold” positioning first, then infrastructure assets (e.g., Ethereum/platforms), and finally broader altcoins; understanding this liquidity sequence reduces timing pressure and refocuses attention on survivability.

< Summary >Altcoin “99% extinction” is consistent with a market structure that increasingly requires regulatory fit, real usage, and liquidity simultaneously.

Bitcoin strategic-asset positioning depends not only on the Lummis bill but also on framework legislation (e.g., the Clarity Act) and ongoing accumulation channels such as seizures, potential purchases, and mining ecosystem policy.

The 2024 ETF → 2025 corporate (DAT) → 2026 SBR narrative sequence provides a practical lens for liquidity rotation and for prioritizing “surviving 1%” assets.

[Related…]

- https://NextGenInsight.net?s=Stablecoin

- https://NextGenInsight.net?s=Bitcoin

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 알트코인 99% 사라진다 ‘비트코인 전략자산’ 움직인다 | 경읽남과 토론합시다 | 3인토론(김광석×표상록×김동환) 6편

● Samsung and SK Hynix smash records on AI inference HBM frenzy, KOSPI supercycle hype amid rate and CAPEX shock risks

Samsung Electronics touches KRW 200,000; SK Hynix surpasses KRW 1,000,000: 5 evidence-based drivers beyond “sentiment”

This note consolidates the following in one place.

1) Why inference, rather than training, is driving disproportionate growth in memory (HBM) demand

2) Why NVIDIA remains resilient and the structural reasons behind the rise of Broadcom and TPU/ASIC approaches

3) What a ~30% HBM ASP increase in six months implies, and where the true bottleneck sits

4) Blind spots and key checkpoints in PER-based valuation narratives for SK Hynix and Samsung Electronics

5) The mechanisms that make KOSPI 6,000–8,000 scenarios more plausible, and the primary risk triggers

1) Market snapshot (one-line summary)

- Samsung Electronics reversed from early weakness to strength, briefly touching KRW 200,000.

- SK Hynix extended gains more aggressively, surpassing KRW 1,000,000.

- Large-cap semiconductors lifted the index, with the KOSPI returning to prior high levels.

The core market question is whether further upside is supported by fundamentals or whether the move is late-cycle.

2) Key driver #1: The AI cycle is shifting from training to inference

2-1. Training: why “GPU-led” performance dominated

Training prioritizes compute throughput to build large models. As a result, GPU performance was the primary constraint, supporting a GPU-centric rally over recent years.

2-2. Inference: why “memory bandwidth-led” performance becomes decisive

Inference runs trained models as real-time services. The constraint shifts from compute alone to timely data delivery (parameters, cache, context), making memory bandwidth a first-order determinant of user-perceived performance. This increases the strategic value of HBM (High Bandwidth Memory).

2-3. Why the shift is material: inference operates under highly variable real-world loads

Unlike training workloads, inference demand is driven by live service usage with highly variable concurrency. As deployment expands across autonomous systems, robotics, and agentic applications, the need to fetch and stage model data quickly scales structurally, increasing the importance of memory capacity and bandwidth.

3) Key driver #2: HBM bottlenecks are lifting ASPs, which in turn supports earnings

3-1. What HBM ASP changes signal

Reported dynamics point to an approximate 30% increase in expected next-generation HBM pricing over six months (with HBM3 referenced versus prior periods). This is consistent with supply lagging demand rather than purely narrative-driven strength.

3-2. Inference increases duration and intensity of HBM utilization

Training demand can be more episodic and capex-bunched. Inference scales with service penetration and tends to require ongoing capacity additions, reinforcing the market view of HBM demand as structural rather than transient.

3-3. Interpreting “faster delivery” requests from NVIDIA

The implication is not only accelerator shortages, but that accelerators cannot be fully utilized without adequate HBM bandwidth. HBM functions as a performance unlock, not an optional add-on.

4) Key driver #3: Why NVIDIA and memory-related names remain comparatively resilient even as broader mega-cap tech softens

AI infrastructure components (accelerators, networking, HBM) have shown relative resilience versus broader mega-cap volatility.

4-1. Why Broadcom and TPU/ASIC approaches are increasingly referenced

As inference scales, workload specialization and data-center-level optimization become more valuable. This expands the opportunity set from a GPU-only framework to include TPU/ASIC and networking-centric architectures.

4-2. Implication: AI exposure broadens into a data-center value-chain trade

This enlarges the earnings leverage for memory suppliers such as Samsung Electronics and SK Hynix.

5) Key driver #4: Where PER frameworks work, and where they can mislead

5-1. Why PER can appear low: earnings catching up to price

If prices rise while PER remains contained, it can reflect earnings growing faster than price. In this context, the two dominant preferences for foreign capital tend to be:

- Earnings visibility

- Perceived undervaluation

5-2. A critical caveat: cyclical distortion risk in PER

Semiconductors remain structurally cyclical. Even if HBM demand is structural, near-term earnings estimates may be sensitive to concurrent dynamics such as peak pricing, capacity additions, and competitive catch-up. A low PER can reflect either genuine undervaluation or peak-earnings distortion.

5-3. Investor checklist: four metrics to monitor

1) HBM contract structure: shifts in long-term contract mix versus spot exposure

2) Customer capex: whether AI data-center spend is deferred versus canceled

3) Competitor yields and ramp: pace of catch-up during HBM4 transition

4) FX: persistence of export-supportive exchange-rate conditions

6) Why KOSPI 6,000–8,000 scenarios are being discussed (mechanism)

6-1. Index levels are a function of earnings and multiples

KOSPI re-rating requires higher earnings (E), higher multiples (PER), or both.

6-2. The current market focus is on earnings expansion

If HBM-led profit growth materially lifts aggregate index earnings, the index level can adjust higher without requiring broad multiple expansion. In this framing, higher index targets reflect earnings composition changes driven by large-cap semiconductors more than a generalized market re-rating.

7) Under-discussed point: the bottleneck is broader than HBM alone

7-1. The deeper constraint: memory hierarchy optimization

Inference optimization requires coordinated advances across cache, interconnect, packaging, power delivery, and cooling. The competitive field is shifting toward simultaneous optimization of compute, memory, and power.

7-2. Potential winners: firms that lock supply chains and execute ramps

Advantage may accrue not only to HBM manufacturers, but to companies that secure long-term volumes and stabilize packaging, qualification, and production transitions. This helps explain market sensitivity to supply and contracting disclosures rather than technical headlines alone.

8) Risk framework: three key triggers to monitor

1) US rate path: renewed inflation and higher long-end yields can pressure growth-equity multiples

2) AI capex moderation: formal guidance indicating slower investment cadence can reprice the value chain

3) HBM supply normalization: faster-than-expected supply relief can compress ASP expectations

9) Conclusion: KRW 200,000 and KRW 1,000,000 levels may reflect an early phase of the “inference economy,” not necessarily a terminal move

The move appears linked to structural change as AI expands from training-centric development into inference-centric services, where HBM becomes a high-cost, high-impact bottleneck. However, PER-based comfort should be tempered by cycle distortion risk, with contract structure, capex trajectory, competitive ramp, and FX conditions as primary monitoring variables.

The core thesis behind the sharp moves in Samsung Electronics and SK Hynix is the shift from training to inference, elevating HBM as a performance bottleneck. Rising HBM ASPs indicate supply tightness and can support earnings growth, which may keep PER optics favorable. Higher KOSPI ceiling scenarios are largely an earnings-driven framework, while rates, AI capex pacing, and supply normalization remain the principal risks.

[Related links…]

- https://NextGenInsight.net?s=HBM

- https://NextGenInsight.net?s=KOSPI

*Source: [ Jun’s economy lab ]

– 삼성전자 20만원, SK하이닉스 100만원 돌파한 이유