● Trump, Iran, Oil Shock, Global Fallout

Why Trump Pushed Toward a War with Iran: Breakdown in Nuclear Talks, U.S. Conservative Calculus, and the True Cost of a Middle East Conflict

This issue is not adequately explained by a simple “Trump is hawkish, so he escalated the war” narrative. Key points include: why both the U.S. and Iran prefer a rapid end yet face strong incentives to prolong; how a failed nuclear negotiation pivoted into military action; how entrenched anti-Iran sentiment within U.S. conservatives shaped policy choices; and how the conflict transmits into oil prices, inflation, global growth, and South Korea’s security and export strategy. Under-covered factors include U.S. interceptor and air-defense capacity constraints, spillovers into the Taiwan Strait and Ukraine, and the internal legitimacy effects of an ascendant Mojtaba framed through Shiite political tragedy narratives.

1. What is this Middle East war in one line?

The U.S. and Iran have limited reasons to sustain a long war, but their conditions for ending it are fundamentally incompatible.

From the U.S. and Trump-aligned perspective, returning to negotiations is not meaningful unless Iran’s military leverage and nuclear-related capabilities are reduced beyond a threshold.

From Iran’s perspective, backing down after conceding deterrence capacity and regime symbols risks undermining domestic legitimacy and internal cohesion.

Both sides prefer a fast conclusion, but each requires the other to concede first. Even if conceived as a short campaign, the structure increases long-war risk.

2. News-style core summary: Why did Trump push toward war with Iran?

2-1. First driver: The breakdown of nuclear talks was decisive

A central trigger was the collapse of nuclear negotiations. While publicly framed as “pressure to resolve the nuclear issue,” a more credible interpretation is that trust failed late in the process, catalyzing a shift to military coercion.

The key dispute was the handling of enriched uranium. Iran indicated a willingness to dilute higher-enriched material to lower levels, but reportedly signaled it would retain the diluted stock domestically.

For the U.S., this is highly sensitive: “dilution” can be technically reversible, whereas “export/removal” is materially harder to reverse.

Trump-aligned decision-makers may have assessed Iran as pursuing delay tactics—approaching a deal while avoiding substantive concessions—prompting a move from diplomatic sequencing to battlefield leverage.

2-2. Second driver: Anti-Iran sentiment in the U.S. conservative camp

Focusing only on the Netanyahu factor is incomplete. Long-standing anti-Iran sentiment and threat perceptions within U.S. conservatism are a deeper structural driver.

For U.S. conservatives, Iran is not merely a regional adversary. The 1979 U.S. embassy hostage crisis—444 days of national humiliation—and the perceived weakness of the Carter administration remain politically salient.

This experience reinforced the view that “Iran is not a trustworthy counterpart,” paralleling hardline attitudes toward North Korea.

Accordingly, the decision reflects not only tactical judgment but accumulated historical memory, emotion, and ideological hostility.

2-3. Third driver: Decapitation-strike expectations and excessive optimism

Israeli intelligence inputs and U.S. hardline judgments likely reinforced expectations that Iran’s core command structure could be neutralized quickly.

The decapitation concept—simultaneous strikes against top leadership and command nodes—assumes rapid regime destabilization.

Past operational successes may have biased expectations. However, state systems rarely collapse from removing a small number of individuals, particularly regimes sustained by religious legitimacy, revolutionary narratives, IRGC networks, and regional militia linkages.

Early optimism may have been high, but the operational reality is more consistent with “damage is feasible; regime collapse is unlikely.”

2-4. Fourth driver: “Netanyahu prolongation” alone is insufficient

Some interpret the war primarily as an attempt to extend Netanyahu’s political survival. Israeli domestic politics may have mattered, but attributing U.S. action entirely to Netanyahu reduces explanatory power.

The U.S. had independent decision logic, and the Trump camp likely pursued its own political and strategic payoffs.

A more realistic synthesis is that Israeli objectives, U.S. hardline strategy, nuclear-talk collapse, decapitation optimism, and U.S. political timing jointly increased pressure for war.

3. Why Trump did not want a long war

3-1. The dominant political constraint: midterm elections

Trump may have had incentives to initiate force, but limited incentives to sustain a prolonged campaign due to U.S. domestic politics.

A longer war raises oil prices; higher energy prices re-accelerate consumer inflation, weaken expectations of rate cuts, and pressure equity and asset markets. This elevates recession risk and voter fatigue, conflicting with midterm strategy.

In practical terms: “short, forceful pressure” can generate political signaling value; “expensive, prolonged, uncertain war” is an electoral liability.

3-2. Economic costs also disincentivize duration

Prolongation is not only higher military spending. It increases oil risk premiums, maritime logistics disruption, insurance costs, supply-chain instability, USD strength pressures, and risk-asset volatility.

If the Strait of Hormuz is destabilized, markets can price a sharp risk premium even without a full physical supply cutoff.

If U.S. consumer sentiment weakens, recession risk returns. Trump may have sought symbolic political leverage, but likely preferred to avoid war-driven macro deterioration.

4. Why the war does not end easily

4-1. End-state conditions are incompatible

The U.S. seeks a “successful termination” after reducing Iran’s military threat and nuclear potential. Iran seeks a “non-capitulation termination” with regime prestige and deterrence intact.

One side’s win condition is close to the other side’s loss condition, complicating negotiation.

4-2. War is not governed by rationality alone

International politics involves calculation; war also involves emotion, face-saving, misperception, domestic politics, and leadership traits.

Even when both sides recognize that ending quickly is economically rational, decisions can still move in the opposite direction.

5. The key military reality: the U.S. cannot fight indefinitely

5-1. U.S. interceptors and air-defense assets are finite

Many assume U.S. military power implies unlimited endurance. In practice, the U.S. does not fight only in the Middle East.

It must also support Ukraine, plan for Guam defense, and posture for the Taiwan Strait and broader Indo-Pacific contingencies.

Air-defense systems, interceptors, THAAD-class assets, and fleet air-defense resources are globally allocated constraints. Extended Middle East commitments can weaken deterrence in other theaters.

5-2. Why U.S. military leadership is structurally negative on a long war

Senior military leadership prioritizes global strategic balance, not only a single theater’s outcomes.

If Middle East air-defense resources are depleted quickly, China may reassess U.S. capacity around the Taiwan Strait; Russia may factor in reduced Western support to Ukraine.

This supports a view that the U.S. can sustain only a limited-duration high-intensity posture in the Middle East. The conflict is therefore also a test of the cost structure of global primacy.

6. Iran domestic variable: why Mojtaba’s rise matters

6-1. Not just a succession story

Interpreting Mojtaba’s rise solely as dynastic succession misses key domestic political mechanisms. Shiite political culture embeds tragedy and repression narratives as legitimacy resources.

Themes such as oppressed orthodoxy, sacrificed leaders, martyrdom, and endurance—rooted in Karbala, Husayn’s martyrdom, and Ashura memory—function as political legitimacy templates, not only religious rituals.

6-2. Tragedy narratives can strengthen leadership legitimacy

Mojtaba was not universally viewed as the most likely supreme leader; formal credentials were limited, and hereditary transfer is ideologically costly for a revolutionary system.

However, war dynamics, repression, family sacrifice, and oppression narratives can alter perceptions. Within this political culture, tragedy framing can increase legitimacy.

External pressure can therefore produce a counter-effect: strengthening internal cohesion and symbolic politics rather than weakening the system. Mojtaba’s rise is a representative case.

7. The most hazardous lens: assuming “authoritarian regimes collapse easily”

Iran’s authoritarianism does not imply it is strategically dismissible.

Deterrence through strength differs from strategic contempt; the latter increases failure risk.

Iran’s clerical governance structure, IRGC apparatus, religious networks, and survival strategies are more resilient than many assume. Ignoring system mechanics undermines forecasting and policy design.

The most costly error in geopolitics is not criticizing an adversary, but underestimating it.

8. Global macro impact: oil, inflation, rates, equities

8-1. Upward pressure on crude prices

The longer the conflict persists, the faster crude markets respond. Hormuz risk can raise prices via risk premiums even absent direct supply disruption.

Higher energy prices can re-ignite global inflation pressures.

8-2. Inflation vs. rate-cut expectations

Markets have been highly sensitive to disinflation and prospective rate cuts. Oil spikes are a primary variable that can disrupt this trajectory.

Beyond the level of inflation, the direction of inflation matters. Energy-driven increases force central banks to reassess easing timelines.

Middle East risk therefore transmits into rates, USD, yields, and equity valuation directly.

8-3. Global growth and asset-market effects

Prolonged war tends to raise safe-haven demand and equity volatility. In high-valuation regimes, geopolitical shocks often provide a catalyst for repricing.

Defense, energy, and selected commodities may see relative support, but the dominant macro feature is higher uncertainty.

9. What South Korea should monitor: security, diplomacy, exports, energy

9-1. The most direct economic variable: energy prices

South Korea’s high import dependence makes it sensitive to crude prices and maritime transport risk. Higher crude and gas costs, marine insurance, and freight raise corporate costs and consumer inflation.

This can pressure export margins, domestic demand, and FX stability through second-round effects.

9-2. Alliance dynamics and potential deployment pressure

If conditions worsen, South Korea may face increased pressure for naval deployments or diplomatic participation.

Policy must balance Middle East security cooperation, U.S. alliance management, China relations, and energy security simultaneously. This conflict is therefore a test of Korean diplomatic and strategic calibration.

10. Key points under-emphasized in mainstream coverage

10-1. The core dynamic: neither side wants a long war

Hawkish rhetoric is prominent, but both sides face high costs of duration. The binding constraint is incompatible end conditions.

10-2. U.S. power has global-allocation limits

The U.S. is strong but not unlimited. Sustained Middle East commitments can weaken posture toward Ukraine, Guam, and the Taiwan Strait.

10-3. External pressure can harden Iran internally

Many analyses assume stronger strikes weaken the regime. Shiite political culture and tragedy narratives imply the opposite can occur: greater legitimacy and cohesion. Mojtaba’s rise is emblematic.

10-4. Underestimating Iran invalidates analysis

Treating Iran as irrational and easily collapsible risks errors in strategy, market expectations, and diplomatic response.

11. Outlook: short-term de-escalation is possible; structural risk remains

Over the next several weeks, the intensity of operations may be adjusted downward, given the high costs of expansion for both sides.

However, this would be closer to temporary containment than resolution. Trust in nuclear negotiations has deteriorated; anti-Iran sentiment within U.S. conservatism persists; and direct Israel-Iran confrontation risk is not fully removed.

Markets may stage intermittent relief moves, but a Middle East geopolitical risk premium may remain, continuing to influence crude prices, inflation, rate expectations, and broader global macro conditions.

12. Conclusion

Trump’s pressure toward war with Iran is best explained as a multi-factor outcome: nuclear-talk breakdown, entrenched anti-Iran sentiment within U.S. conservatives, overconfidence in decapitation-strike effects, Israel-linked alignment of interests, and domestic political timing.

The conflict is increasingly less about who is stronger and more about who cannot afford to endure. Monitoring should prioritize end-state conditions, depletion of defensive assets, crude-price dynamics, and changes in Iran’s internal cohesion.

< Summary >

Trump’s push toward war with Iran reflects a combination of nuclear negotiation failure, long-standing anti-Iran sentiment in the U.S. conservative camp, decapitation-strike expectations, and domestic political calculations, rather than a single Netanyahu-driven explanation.

Both the U.S. and Iran have limited tolerance for a prolonged war, but incompatible conditions for termination make a quick end difficult.

Key points: U.S. interceptor and air-defense resources are finite; external pressure can strengthen Iran’s internal cohesion and Mojtaba’s legitimacy; and underestimating Iran leads to analytical and policy failure.

Macro transmission runs through crude prices, inflation, rate-cut expectations, and equity volatility. South Korea should monitor energy costs, export impacts, alliance dynamics, and Middle East diplomatic strategy.

[Related Articles…]

- Trump risk and a core summary of the 2026 global asset-market outlook: https://NextGenInsight.net?s=Trump

- How a crude-price spike impacts South Korea’s economy and inflation: https://NextGenInsight.net?s=oil

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 트럼프는 왜 이란전을 밀어붙였나. 핵협상 파행, 미국 보수의 계산, 중동전쟁을 보는 법 | 경읽남과 토론합시다 | 백승훈 교수_4편

● Jeonse Loan Crunch, Housing Slump Trigger

Why a Reduction in Jeonse Loans Can Become the True Trigger for Housing Price Declines: The Essential Points to Monitor in the Current Real Estate Market

This is not a simple question of whether home prices will fall.

To assess current conditions, it is necessary to connect: (i) why jeonse listings appear to be shrinking, (ii) why that may be temporary, (iii) why tighter jeonse lending can pressure transaction prices, and (iv) how government supply and presale pricing policy can reshape market sentiment.

This report focuses on two under-emphasized mechanisms: (1) the chain “jeonse loan contraction → expectations of weaker jeonse pricing → reduced purchase demand → price adjustment,” and (2) the point that the method of announcing presale prices can move sentiment more than headline supply volumes.

It also summarizes how multi-home owners are currently positioning, whether a shift toward monthly rent necessarily implies sustained rent inflation, and what indicators renters and prospective buyers should monitor.

1. Key Development: Why Jeonse Loan Contraction Translates Into Downward Pressure on Home Prices

If jeonse loans contract, the impact is not limited to tenant affordability. The effective ceiling on jeonse deposits declines, and the transaction price supported by those deposits faces pressure.

In the domestic market, jeonse levels often function as a psychological and financial downside support for transaction prices.

Because jeonse is tightly linked to transactions, abundant jeonse financing historically enabled higher deposits, which in turn supported leveraged purchases (gap investment) and helped defend transaction prices.

Even a policy signal of gradual, long-term jeonse loan reduction changes expectations:

“Jeonse deposits may no longer rise as they did.”

“Transaction prices may be harder to sustain at current levels.”

Once this expectation forms, both end-users and investors tend to delay purchases, reducing demand, weakening volumes, and increasing adjustment pressure.

This is an expectations-channel shift in an asset market, comparable in relevance to interest rates, liquidity, and supply policy.

2. Why Jeonse Listings Appear Scarce: Potentially a Structural Optical Illusion Rather Than True Supply Shortage

Market participants increasingly report “jeonse listings have dried up.” This may be temporary when viewed alongside the flow of listings from multi-home owners.

2-1. Why listings look tighter

Previously, listings were more balanced between jeonse and sale. Recently, in the metropolitan area, sale listings appear to dominate to a much greater degree.

Interpretation: units that would have been offered as jeonse are being offered for sale first.

Implication: the apparent jeonse scarcity may reflect owner behavior (attempted liquidation), not a shortage of housing stock.

2-2. What happens if units do not sell

If transactions fail to clear, owners may need to restore liquidity.

Owners who vacated a unit to sell may revert to leasing it out to secure cash flow.

Therefore, jeonse supply could re-enter the market after a lag, and using near-term jeonse tightness to infer imminent price appreciation may be unreliable.

3. The Shift Toward Monthly Rent: Does It Necessarily Lead to Sustained Rent Inflation?

A common claim is that weaker jeonse financing mechanically increases monthly-rent demand and drives rent inflation. A counter-view is that rents may also converge toward equilibrium over time.

3-1. Jeonse vs. monthly rent is an opportunity-cost decision

Tenants compare: (i) locking up a large deposit with minimal monthly payments versus (ii) paying monthly rent while deploying capital elsewhere.

The preferred option depends on interest rates, expected returns on financial assets, and housing price expectations.

When price appreciation expectations are muted and alternative returns are available, higher-income cohorts may rationally choose renting over buying.

3-2. High-priced housing can enter a “renting is more efficient than buying” zone

Illustration: instead of purchasing a KRW 3.0 billion apartment, a household rents it with KRW 100 million deposit and KRW 4.0 million monthly rent (annual rent ~ KRW 50 million).

If foregone purchase capital can earn competitive financial returns, renting can dominate in periods of low expected home price appreciation.

Monthly-rent demand can rise, but prices are constrained by substitution between jeonse and monthly rent; excessive increases tend to shift demand back toward alternatives.

3-3. Conclusion

Monthly-rent pressure may emerge in the short term. Over time, as jeonse supply normalizes, transaction prices adjust, and opportunity-cost calculations reset, rents may stabilize rather than rise without bound.

4. What Multi-Home Owners Are Considering: Monetization Over Holding

Field signals suggest a shift from acquisition-oriented questions to timing and pricing of sales.

4-1. Asset-holder sentiment is changing

When owners focus on exit execution rather than additional purchases, sentiment can weaken before prices.

If a new administration signals reduced tolerance for rapid price increases, perceived policy risk rises, encouraging de-risking behavior among multi-home owners.

4-2. Higher risk for villa and multiplex owners

Highly leveraged gap-investment structures depended on abundant jeonse financing: tenants funded high deposits, enabling repeat acquisitions and refurbishments.

If jeonse loans contract, deposits may not clear at prior levels, forcing owners to bridge gaps with their own capital. With multiple units, liquidity stress can compound.

Potential outcomes include distress sales, auctions, and increased leasing supply.

5. The Real Center of Supply Policy: The Presale Price Signal Matters More Than Headline Volumes

Market impact often hinges less on “how many units” and more on “at what price” the new supply is offered.

5-1. Historically, price suppression was associated with near “half-price” supply

Past episodes of large-scale supply that materially undercut prevailing prices changed buyer behavior:

“There is no need to buy at today’s price.”

“Waiting may allow purchase at a lower price.”

This expectation diverts demand toward waiting and weakens the price-supporting bid.

5-2. Why recent supply measures felt less effective

Even with price controls, presale prices were not perceived as sufficiently discounted. As pricing became partially anchored to surrounding market levels, buyers viewed presales as still expensive.

Result: supply headlines increased, but the incentive to wait remained limited.

5-3. If a prime-area presale price is meaningfully lower than expected

If large-scale supply in a prime location is priced materially below market expectations, the spillover can be substantial:

- Purchase demand shifts toward subscription/pre-sale queues.

- Owners of high-priced units consider profit-taking.

- Even core districts can see reduced upside expectations.

- Lower volumes can be followed by ask-price adjustments.

This is the primary channel through which policy shifts sentiment.

6. What First-Time Buyers Should Monitor: Market Lows Often Emerge From Policy and Liquidity Signals Before Price Prints

The key issue is not whether prices have declined, but whether the underlying regime has shifted.

6-1. In corrections, assess distance from fundamental “normalization”

Housing prices cannot remain disconnected from inflation, income growth, interest rates, supply, and demographics indefinitely. Overshoots are typically followed by normalization.

Valuation conditions can differ materially by region: core areas may remain expensive while some peripheral markets may have already deflated more meaningfully.

6-2. Priority variables to track

- Pace and scope of jeonse loan contraction

- Actual presale prices for public land and third-phase new town supply

- Post-election local government cooperation on supply execution

- Intensity of multi-home owner listing flow

- Volume trends and evidence of lower transaction prints

- Interest rate direction and household credit regulation stance

Market bottoms typically form through the interaction of policy, sentiment, and liquidity rather than a single price level.

7. Long-Term Outlook: Demographic Effects May Become a Primary Variable Around 2033–2034

Beyond near-term pricing, demographic structure may become a more direct driver of housing demand.

7-1. Why 2033–2034 may matter

Fewer marriages translate into fewer new households, reducing core end-user demand across both rental and transaction markets.

While low birth rates are already known, their direct translation into housing-market metrics may become more visible over time, shifting market narratives toward structurally weaker demand.

7-2. Why “Japan-style” arguments may re-emerge

This does not imply uniform outcomes across regions. However, if population decline, widening regional demand dispersion, high-basis purchases, and policy-driven supply expansion coincide, some areas could face prolonged stagnation or structural decline debates.

In investment-driven segments, when capital-gain expectations weaken, liquidity can freeze before large price moves occur.

8. Four Under-Covered Points in Mainstream Coverage

8-1. Jeonse loans functioned as a price-support mechanism

While framed as tenant support, jeonse loans also propped up jeonse deposits and, indirectly, transaction prices. Reducing this support can alter price formation.

8-2. Falling jeonse listings may reflect sale-first behavior, not shortage

Interpreting near-term jeonse scarcity as a renewed upcycle is risky if unsold inventory later returns to the lease market.

8-3. Supply policy impact is driven by the presale price signal

Markets react more to price than to unit counts. A clearly discounted presale price in a prime area can have outsized sentiment effects.

8-4. Over the long term, the recognition point matters more than the demographic fact

Population decline is known, but asset markets move when the consensus begins to price it in. The 2033–2034 window may be a period when that recognition accelerates.

9. Positioning Framework by Participant Type

9-1. First-home end-users

Prioritize policy direction over momentum chasing. Monitor public-supply presale prices, jeonse lending rules, and transaction volume contraction. “Buy now or be priced out forever” narratives appear less dominant than in prior cycles.

9-2. One-home upgraders

Upgrade demand persists in prime locations, but leverage expansion at elevated valuations increases execution risk. Evaluate saleability of the current home and the valuation of the target asset.

9-3. Multi-home investors

Tax policy, credit constraints, rental-market shifts, and supply policy can tighten simultaneously. Jeonse-based leverage strategies are materially riskier; cash-flow and maturity profiles should be stress-tested for liquidity shocks.

10. Integrated View: The Market Should Be Analyzed Through Three Axes—Jeonse, Policy, and Sentiment

The market is not explained by supply shortage alone. Jeonse loan contraction can pressure both lease and transaction pricing; the current decline in jeonse listings may be temporary; and materially discounted presale pricing in core areas could cool sentiment faster than expected.

Combined with changing multi-home owner behavior and longer-term demographic constraints, residential property may be less suitable to model as a one-directional appreciating asset.

The environment is neither a deterministic surge nor an immediate crash. The dispersion between participants who understand transmission mechanisms and those who react to surface-level headlines is likely to widen.

< Summary >

Jeonse loan contraction can create expectations of weaker jeonse pricing, reduce purchase demand, and increase downside pressure on transaction prices.

The recent decline in jeonse listings may reflect multi-home owners shifting units to for-sale inventory; if sales do not clear, lease supply may return.

A shift toward monthly rent may occur near term, but substitution and opportunity-cost dynamics can limit sustained rent inflation.

The most market-moving supply variable is not unit count but the presale price signal, particularly in prime locations.

Longer term, demographic structure around 2033–2034 may become more directly priced, supporting a more conservative posture toward property investment and broader asset allocation.

[Related Articles…]

- Comprehensive Summary: How Shifts in Interest-Rate Direction Affect Korean Asset Markets

- After the AI Revolution: Where Capital Is Likely to Flow Across Real Estate and Equities

*Source: [ Jun’s economy lab ]

– 전세대출 때문에 집값 꺾입니다. 조심하세요(ft.한문도 교수 2부)

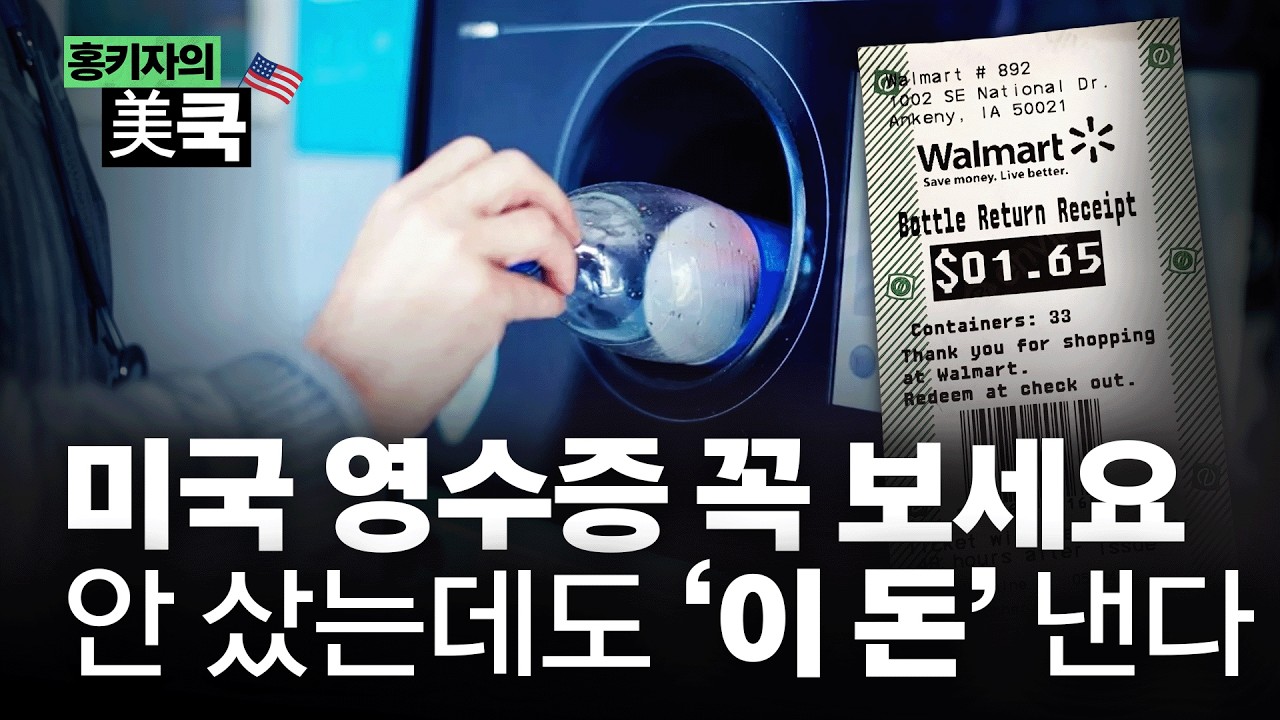

● Hidden Fees, Bottle Deposit Black Market, Costco Receipt Crackdown

Hidden Costs on US Grocery Receipts, the Bottle-Deposit “Micro Cash Economy,” and Costco Receipt Checks — A Unified View

US consumer prices often feel higher than shelf labels suggest, receipts frequently include unexpected add-ons, and some retailers verify purchases again at the exit. Viewed together, these practices illustrate core features of the US consumer system: incentive-driven policy design, informal cash-flow mechanisms, retail loss prevention, and contract-based compliance.

This report focuses on (i) why bottle deposits function as a city-level micro cash economy, (ii) why large-format US retailers prioritize verification over presumed trust, and (iii) how these structures connect to inflation perception, consumer psychology, retail strategy, and the emerging automation/AI stack in retail.

1. Why a $1.99 shelf price becomes higher at checkout

In the US, purchases of bottled water, soda, and juice can total more than the shelf label at checkout.

Beyond sales tax, receipts may include a separate line item: a bottle deposit (also listed as a bottle/container deposit). This is not product price; it is a refundable deposit returned when the empty container is redeemed.

2. Core logic: recycling is designed through financial incentives

Recycling participation in the US varies widely by region. Some states prioritize economic incentives over moral appeals:

- Pay a deposit at purchase

- Return empty bottles/cans after consumption

- A redemption machine reads the barcode and prints a refund receipt

- The receipt is redeemed as cash-equivalent at the retailer/redemption point

This is an incentive-based public-policy mechanism rather than a purely environmental program.

3. In large cities, empty containers become an informal “cost-of-living” cash flow

In major metros (e.g., New York), individuals collecting bags of cans/bottles often treat them as monetizable assets.

This can be a practical income source for:

- Unhoused individuals

- Low-income households

- Recently arrived immigrant workers

- Workers with unstable or irregular earnings

Small per-unit values (e.g., $0.05–$0.10) can aggregate into daily food, transit, and essential expenses. As implemented, bottle deposits can function as a distributed, informal micro cash economy not fully captured by headline economic statistics.

4. Why cross-border “deposit arbitrage” emerges: state-by-state policy differences

Bottle-deposit rules differ by state. This creates arbitrage incentives:

- Collect large volumes of empty containers in non-deposit states

- Transport them into deposit states (e.g., New York, California)

- Redeem them for cash via machines/centers

At scale, this can become economically material and has led to organized transport and systematic exploitation attempts.

5. Common abuse patterns

Where cash-equivalent refunds exist, exploit attempts follow. Common methods include:

- Importing containers from non-deposit states

- Applying counterfeit barcode stickers to trigger refunds

- Taking redeemable containers from residential recycling bins

- Exploiting redemption machine/process weaknesses for repeated refunds

California has seen recurring reports of organized schemes involving interstate container inflows and large refund claims.

6. Structural takeaway: systems are designed around incentives and controls

The primary function is behavior shaping through mechanism design: converting targeted actions into financially rational choices.

This logic parallels modern platform economics, where behavior is influenced via rewards, rankings, fees, and algorithmic incentives rather than normative messaging.

7. Why Costco checks receipts after payment: operational logic

Large-format retailers—especially membership clubs such as Costco or Sam’s Club—commonly verify receipts at the exit.

This is not solely a security ritual; it reflects an operating model that treats transaction completion as including final verification.

8. The US concept of trust in retail: trust as verifiable state

The baseline assumption is that errors and omissions occur and intentional non-payment is possible. Exit staff typically verify:

- Item count on receipt vs. items in cart

- Missing high-value items

- Undercharges/overcharges and duplicates

- Oversized items on lower racks or cart bases

This functions as a final control for operational accuracy and loss minimization.

9. Why membership clubs are stricter

Membership models embed receipt checks in member terms. Entry and purchase imply contractual consent to verification processes.

This highlights a broader US market norm: contracts and terms frequently take precedence over informal expectations.

10. Primary objective: shrink management

A critical retail metric is “shrink” (inventory loss), driven by:

- Theft

- Employee error

- Self-checkout non-scans

- Internal fraud

- Inventory-record inaccuracies

At industry scale, shrink totals are reported in the tens of billions of dollars annually, affecting profitability and, indirectly, pricing and perceived inflation.

Exit checks operate as a low-cost final control layer.

11. Consumer-side benefit: error detection

Receipt verification can also protect customers by catching:

- Double scans

- Missed discounts

- Incorrect quantities

When detected, customers can be directed to service desks for correction.

12. Economic implications for investors

These mechanisms provide several investable and policy-relevant signals.

12-1. Perceived inflation is amplified by the gap between posted and paid prices

US consumers frequently face:

- Pre-tax shelf pricing

- Local tax variability

- Deposits

- Fees and service charges

- Tipping norms

This widens the difference between displayed prices and actual outlays, increasing perceived cost pressure even when nominal shelf prices appear stable.

12-2. Deposit systems can function as a supplemental cash-flow channel

While designed for recycling, deposit refunds can provide small but meaningful cash income for economically vulnerable populations, partially substituting for formal safety nets in practice.

12-3. US retail is shifting from experience optimization toward loss control

With pressures from theft, wage costs, logistics costs, higher interest rates, and demand uncertainty, retailers increasingly prioritize loss reduction over frictionless customer experience.

Related measures include:

- Receipt checks

- Tighter self-checkout oversight

- Locked displays for high-value goods

- Increased access control and surveillance

12-4. From an AI trend perspective, “verification automation” is likely to expand

Retail is a high-probability deployment environment for:

- Computer vision and video analytics

- Smart carts and real-time basket validation

- RFID and automated inventory reconciliation

- Integrated payment-and-verification systems

This supports continued growth in retail technology and automation tooling, with measured adoption tied to shrink economics and labor substitution.

13. News-style key points

1) US receipts may include add-ons beyond tax, including refundable bottle deposits.

2) Deposits are an environmental incentive mechanism that can also operate as an urban micro cash economy.

3) State-level policy differences enable gray-market arbitrage and fraud (interstate transport, counterfeit barcodes, theft from recycling streams).

4) Costco receipt checks reflect shrink management and contract-based operating culture, not purely consumer distrust.

5) Both systems demonstrate a US preference for incentives, verification, and formal mechanisms over reliance on goodwill.

14. Core linkage often missed in mainstream coverage

Bottle deposits and receipt checks appear unrelated but share the same design principle:

- Incentivize targeted behavior via economic mechanisms

- Enforce outcomes through verification and process controls

Comparable patterns exist in insurance, subscriptions, platform labor, ad-recommendation systems, credit scoring, and AI-enabled surveillance/monitoring.

15. Application for investor and expatriate audiences

This topic supports multi-angle analysis:

- Drivers of US perceived inflation at the point of sale

- Consumer behavior and retail operating strategy

- Informal cash flows and micro-economies in urban settings

- Corporate loss-control priorities under inflation and margin pressure

- Expansion pathways for AI-enabled retail automation

< Summary >

Bottle deposits on US receipts are refundable incentive instruments designed to increase recycling participation. In major cities, deposit redemption can operate as a micro cash economy for vulnerable groups, while state-level differences create opportunities for arbitrage and fraud.

Costco-style receipt checks are primarily a shrink-control and accuracy mechanism embedded in contract-based membership operations.

Both cases highlight a broader US system design preference: incentives over moral persuasion, verification over assumed trust, and formal mechanisms over informal norms. These dynamics align with continued deployment of AI-driven verification and retail automation.

[Related Posts…]

- https://NextGenInsight.net?s=USA

- https://NextGenInsight.net?s=AI

*Source: [ Maeil Business Newspaper ]

– “빈 병 밀수해 돈 번다” 미국 영수증이 만든 지하 경제 | 홍키자의 美쿡 | 홍성용 특파원