● Tesla 30K Model Y Shock Resets EV War

Tesla’s New Model Y Standard: Real-World Capture and the $30K Price Shock That Created a New Order in the Electric Vehicle War

This article organizes the leaked actual price and specifications, the effective price shaped by the subsidy and interest rate environment, the cost structure and battery strategy, the AI/FSD-based software revenue model, and even the global economic variables all at once.

While other channels only skim through the specs, here the focus is on why now is not a time for a “price cut” but rather a “business model transformation,” how the removal of hardware is offset by software revenue, and how global economic variables like interest rates, inflation, and a strong dollar affect demand elasticity.

In short, the $30K Model Y Standard is not simply a low-cost model, but rather a harbinger of Tesla’s “game changer” that has redesigned its supply chain, manufacturing methods, and software billing strategies.

1) Timeline Overview Before 2025: Caught in Austin → Web Code Price Leak → Signal of Imminent Unveiling

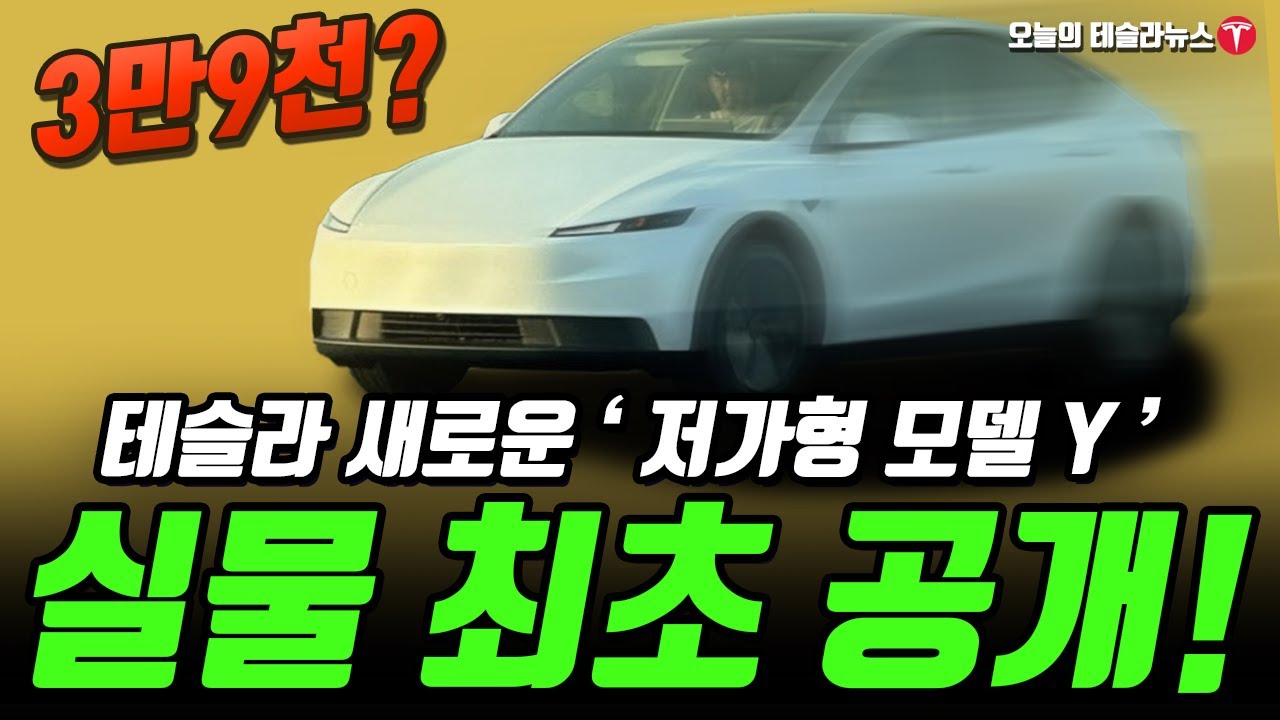

In the vicinity of Giga Texas, several test vehicles suspected to be the new Model Y Standard without camouflage were spotted on the roads.

At the same time, keywords related to the “Model Y Standard,” a price of $39,990, and specifications were found in Tesla’s website code, pushing the rumors beyond the speculation stage to an imminent unveiling phase.

The gathering of Tesla influencers in Austin further signals that this is not merely a test but a countdown to launch.

2) The True Take-Home Price of $39,990: Influenced by Subsidies, Interest Rates, and Residual Value

The sticker price appears to be $39,990.

However, the effective cost varies dramatically depending on subsidies, financing conditions, residual values, insurance premiums, and state-specific incentives.

In terms of subsidies, there have been cases where specific regulations and order cutoffs are utilized, with the application of tax credits differing greatly by region and timing.

Higher interest rates sharply increase the monthly payment, so when interest rates peak or step down, the effective price drops immediately.

With high residual values, Tesla can lower monthly payments through lease and residual value guarantee programs, greatly increasing demand elasticity according to global economic trends in interest rates and inflation.

In summary, the decision-making is centered on the “total cost of ownership (TCO)” rather than just the sticker price, with interest rates, a strong dollar, and the reduction or extension of subsidies acting as key variables.

3) Cost-Reduction Points Observed in the Real Vehicle: The Art of Deletion and Manufacturing Simplification

Observations include a Highland-style single headlight, a conventional roof (eliminating the panoramic option), new 18-inch wheels, fabric trim, manual steering adjustment, removal of the rear seat screen, simplified climate control, and the exclusion of the HEPA filter.

This combination is interpreted as a “deletion-based simplification” strategy that reduces the BOM (bill of materials) and assembly process while maintaining external design completeness.

Eliminating the glass roof reduces parts, assembly, and leak risks and is advantageous for managing body torsion strength, which in turn can contribute to improved production yield.

Coupled with Tesla’s expertise in large castings, supplier cost renegotiation, and process step reductions, the manufacturing economics of the $30K price point gradually start to align.

4) The Key to Battery Strategy: 4680 vs. LFP, and Structural Battery Packs

The 4680 line at Giga Texas is a core element for cost reduction and the application of structural battery packs.

However, for the entry-level model, there is also a high possibility of adopting LFP (lithium iron phosphate).

LFP offers advantages regarding raw material price volatility and thermal stability, and its strengths of “charging convenience and longevity” make it suitable for urban and commuter demand.

The combination of 4680 produced locally in the U.S. and the flexible supply of LFP can disperse supply chain risks, allowing for a “modular strategy” that adjusts the battery pack configuration to meet regional regulations and subsidy requirements.

In short, rather than going all-in on a single chemistry, a flexible hybrid operation that mixes options to optimize costs, subsidies, and logistics is highly likely.

5) The Essence of this Car is a ‘Hardware-Software Bundle’: Recovering Revenue Through FSD and Robo-Taxi

The entry-level Model Y is closer to a typical platform strategy aimed at recovering revenue through software and services (such as FSD subscription, robo-taxi, connectivity, and usage-based insurance) rather than preserving hardware margins at all costs.

By increasing the number of vehicles at the low entry price, it is expected that free FSD trials, transitions to subscriptions, and bundled options will boost ARPU.

In this structure, even though there are concerns of declining automotive margins, the ultra-high margins of the software can defend the overall profit margin.

In other words, Tesla is already changing the rules of the game from “selling cars cheaply and selling data expensively” to “deploying cars widely and generating long-term cash flow through AI capabilities and networks.”

6) The Reshaping of the Global Price War: Dynamics with BYD, Hyundai-Kia, and Traditional OEMs

In China, BYD is explosively increasing volumes with EVs and PHEVs in the $20K-$30K range.

In Europe, due to subsidy reductions, high interest rates, and inflation, high-priced EV demand is dwindling, with demand shifting towards mid-priced and entry-level models.

In the U.S., Tesla’s brand power is enhanced by the convenience of the NACS supercharger network, making the charging experience a “decisive differentiator” at the same price point.

Hyundai and Kia are pushing back by improving the quality of mid-range models through the switch to E-GMP 2.0 and the adoption of LFP.

The introduction of the entry-level Model Y by Tesla is not a defensive move but an attempt to reclaim leadership, with the combination of the charging network and software rewriting the rules of the price war.

7) Checking Macroeconomic Variables: Interest Rates, Inflation, and a Strong Dollar Divide Demand and Margins

Passing the peak in interest rates and the easing of inflation can improve monthly payments and consumer sentiment, thereby expanding demand.

A strong dollar has mixed effects on domestic costs, imported components, and export prices in the U.S., leading to frequent fine-tuning of regional pricing.

On the supply chain side, battery materials and semiconductor supply stabilization are underway, but certain mineral regulations and geopolitical risks occasionally create cost volatility.

If the global economic cycle experiences a smooth soft landing, fixed-cost leveraged companies like Tesla stand to benefit significantly from volume expansion and margin recovery.

8) Regional Impact in Europe, China, and the U.S.: The Same Car, Completely Different Outcomes

In the U.S., the advantages of charging infrastructure, brand strength, and residual values mean that entering the market at around $30K directly translates into “monthly payment competitiveness.”

In Europe, where price sensitivity is high due to subsidy reductions, the introduction of the entry-level Model Y could swiftly stimulate demand elasticity.

In China, although local brands aggressively push ultra-low prices, there is still a willingness to pay a premium for Tesla’s software and charging experience.

The key lies in a nimble combination of “region-specific specs, pricing, and finance packages” tailored to each area’s regulations, subsidies, and interest rate fluctuations.

9) Margins and Valuation: Short-Term Dilution vs. Long-Term Software Leverage

In the immediate aftermath of the entry-level launch, overall automotive margins may decline.

However, as the vehicle lineup expands, FSD subscription conversion rises, the data network expands, and even robo-taxi, insurance, and energy solutions come into play in a virtuous cycle, the blended margins could improve.

From an investor’s perspective, the key is not the “short-term automotive margin” but the “long-term ARR (subscription revenue) growth rate” and the “asset value of AI/autonomous driving data.”

10) 7 Points the Market Has Yet to Notice

– The adoption of a conventional roof not only cuts costs but also reduces the risks associated with body rigidity, noise, and quality control, thereby potentially increasing production yield.

– Standardizing 18-inch tires optimizes the balance among tire cost, durability, and efficiency to lower the TCO.

– The structural battery pack reduces the number of parts, shortening assembly time, and the simplified crash structure design may lower repair costs.

– The core of the low-cost model is not merely being “ultra-cheap” but rather designing a funnel that leads from FSD trials to subscription conversion.

– With the opening of NACS, as more non-Tesla EVs join, Tesla will gain additional new revenues based on traffic and payment data from its charging network.

– Increasing the number of vehicles improves the precision of UBI (usage-based insurance) by better analyzing driving habits, thereby reducing loss ratios and boosting insurance profit contributions.

– In a strong dollar environment, increasing the share of local production rather than exports is more advantageous for margin protection, aligning with the logic behind expanding Gigafactories.

11) Short-Term Roadmap Checklist: What to Watch Over the Next 90 Days

Monitor the timing of EPA certification and the update of the driving range label.

Once the VIN decoder and option codes are released, clues about battery chemistry and country of origin will emerge.

When the configurator opens, initial lead times and trim configurations can indicate potential production constraints.

If there is an Austin delivery event or a limited regional launch, the production ramp-up curve should be conservatively estimated.

Frequent fine-tuning of prices and incentives can be interpreted as a test of demand elasticity.

12) Risks and Responses

Delays in production ramp-up and bottlenecks in specific components could increase variability in initial delivery times.

FSD regulatory and accident issues may directly affect subscription conversion rates and the brand’s reputation.

Aggressive price cuts in China and Europe could further pressure margins.

To counteract potential dilution of brand positioning, strategies such as upselling higher trims and bundling software options are needed to defend the average selling price (ASP).

13) Conclusion: Transitioning from a ‘Cheap Tesla’ to a ‘Platform Tesla’

The Model Y Standard is not aimed at a mere price cut but is the start of a platform strategy intended to maximize software and service revenue through an expanded installed base.

Even amidst the complex environment of global economic factors such as interest rates, inflation, a strong dollar, and supply chain challenges, Tesla’s economics—bolstered by its charging network and AI capabilities—remain robust.

If the unveiling materializes by late this year or early next year, the battle in the electric vehicle war is highly likely to shift from a “specs race” to a “network and data race.”

< Summary >

The $39,990 Model Y Standard begins a platform strategy that lowers costs through deletion and simplification while recovering revenue through FSD, insurance, charging, and other software-based services.

Global economic variables such as interest rates, inflation, and a strong dollar affect the effective price, and regional subsidies along with a flexible supply chain are crucial in determining success.

Although there may be short-term margin dilution, in the mid-to-long term, subscription revenue and data networks will be the keys to revaluing the company.

Keywords: Global economy, interest rates, inflation, supply chain, strong dollar

[Related Articles…]

The Reality of Tesla’s Price War and the 2025 Demand Scenarios

Robo-Taxi Economics: How FSD Subscriptions Are Changing the Automotive P&L

*Source: [ 오늘의 테슬라 뉴스 ]

– 테슬라 신형 Model Y 스탠다드 실물 공개! 3만 달러대 가격 충격… 전기차 전쟁의 판도가 바뀐다?

● Tesla Bombshell, Budget EV, Robotaxi, China Q4 Surge, Goldman Crash Warning

Tesla “Embargo Circumstances” Analysis: Budget Model · Robotaxi Signals, Q4 China Demand Explosion Trigger, and Goldman’s Crash Warning All Covered in One Strategic Roadmap

Before reading, let’s highlight only the key points.

- It structurally outlines the actual release candidates and website update signals indicated by the Austin “embargo circumstances.”

- It models the integrated effect of tax changes to explain why Q4 deliveries in China are likely to surge further.

- It summarizes the “revenue recognition” and “fleet operations” aspects in the robotaxi timeline that the market is overlooking.

- It reinterprets Goldman’s CEO crash warning along the axes of “interest rates, liquidity, and AI CapEx” to distinguish risks and opportunities for tech stocks.

- From a long-term investor perspective, it provides a ready-to-use checklist to stay undeterred.

1) Timeline: Austin-Originated “Embargo Circumstances” and Release Candidates

In early October, many Tesla influencers gathered in Austin and consistently chose to remain silent about the reason.

Tesla’s official account’s playful replies and the mention of “site refresh (F5)” are interpreted as imminent website update signals.

The key point is that a similar pattern of “quiet gathering + minor website tweaks” has repeatedly preceded major Tesla updates in the past.

This time, the agenda candidates fall into two main categories.

- Budget lineup (especially a variant or new trim of the Model Y)

- Robotaxi/FSD major update (version transition or operator change)

They can occur concurrently rather than being mutually exclusive.

This is because it is a dual-track strategy: securing volume through price range expansion while supplementing profitability with autonomous driving software.

2) Budget Model Circumstances: Design, Cost, and Pricing Strategy

Based on recently captured physical photos and community reports, a simplified design without the front light bar seen on the “Juniper” is being discussed.

This aligns with a typical cost engineering approach that reduces assembly complexity and parts cost by simplifying options.

The powertrain is likely to feature LFP batteries, and reducing the casting scope along with interior specifications could offset the initial ASP decrease.

Price positioning hinges on the “psychological threshold.”

- Global demand elasticity for affordable electric vehicles reacts sharply at specific price ranges (e.g., around $30,000–$35,000).

- If Tesla utilizes lease subsidies and financing costs (interest rate adjustments) to lower monthly payments, the effective price perceived by consumers will drop even further.

Here is a point that other media often overlook. - Changes in the page code often coincide with the timing of updates to the financial partner API, lease, and insurance rates.

- In other words, one should check not only the product price but also whether the “monthly payment calculator and terms updates” are released simultaneously.

- If they are, a far stronger demand stimulus is triggered immediately than a simple price reduction.

3) FSD · Robotaxi: Revenue Recognition and the Role of the Fleet, More Crucial Than the Technology Roadmap

The major FSD v14 update is not merely about performance improvements.

If limits on the functional regions and conditions expand within regulatory bounds, Tesla may have the opportunity to recognize a portion of its deferred FSD revenue.

This “accounting revenue recognition” can dramatically impact quarterly margins and profitability, serving as a catalyst for stock volatility.

Additionally, changes in the entity managing the fleet serve as a signal.

- Hiring and pilot projects related to “safety driver reduction” or “fleet operator” indicate that commercialization is on the threshold.

- The core of robotaxi lies not in the number of sensors but in the operational algorithm, securing available operating hours, insurance/liability structure, and fare settlement system.

- If Tesla integrates in-app call, payment, and dispatch logic, it can unlock software and service margins that exceed hardware margins.

Another aspect overlooked by other news outlets is the indirect connection between the “Supercharger/NACS expansion” and robotaxi. - The integration and openness of the charging infrastructure actually yield operational efficiencies through “optimized charging costs + maximized turnover.”

- Since robotaxi profitability is highly sensitive to charging time and costs, infrastructure dominance directly translates into a TCO advantage.

4) Q4 China Deliveries: Policy Bracket Shifts and “Full-Forward” Demand

In China, from 2023 to 2025, NEVs (new energy vehicles) are fully exempt from acquisition tax (with a cap), and from 2026 to 2027, the tax is reduced by 50%.

In other words, from 2026 the purchase cost perceived by consumers could increase by up to around 15,000 yuan (depending on the model and cap).

This structure is a classic trigger for “full-forward” demand (pulling forward purchases) in Q4 of 2025.

Furthermore, if seasonality (increased Q4 deliveries) and new specifications (e.g., China-specific LWB/Long Range options) coincide, quarterly deliveries are likely to surpass estimates.

If U.S. demand was pulled forward in Q3 due to tax credit changes, a similar effect could reoccur in Q4 in China from an even broader base.

Despite intensifying competition, if Tesla’s price elasticity, brand credibility, and supply chain reliability (Shanghai shipping slots, securing capacity on trailers) combine, a “final surge” is possible.

However, it is risky for media to draw conclusions based on just one number.

- The key factors are the Shanghai factory’s day and night operational rates, minimizing roll-over, local financial product interest rates, and approval speed.

- Especially since shifts in interest rates are immediately reflected in consumer sentiment via monthly payments, the link between “interest rates and demand” must be monitored in real time.

5) Q4 China Scenario in Numbers (Range-Based)

Conservative Scenario: If there is a delay in recognizing the policy effects in Q4, accompanied by intensified competitor promotions and logistics bottlenecks, growth could be in the high single-digit range compared to the same period last year.

Baseline Scenario: If tax transition awareness combines with seasonality and new specification effects, growth could be in the low to mid double digits compared to the same period last year.

Aggressive Scenario: If favorable financial costs (interest rates), an influx of fleet demand in major cities, and simultaneous website/lease promotions occur, growth could be in the high double digits.

The core factors are the effective price based on monthly payments and the shortening of delivery lead times.

If both conditions are met, even among tech stocks, electric vehicle volume stocks will experience significant leverage effects.

6) Turning Goldman’s CEO “Crash Warning” into an Investment Blueprint

The context in which the Goldman CEO mentioned a potential crash within 1–2 years while evoking the dot-com bubble ultimately serves as a warning about the risks of “excess liquidity, high real interest rates, and overinvestment in AI CapEx.”

- If real interest rates remain high, it puts downward pressure on valuations, particularly for tech stocks.

- If AI capital expenditures outpace productivity improvements, a combination of fixed cost burdens and declining profitability could emerge in the later stages of the cycle.

- As the likelihood of inflation reigniting increases, central banks will slow down their interest rate cuts.

The differentiating factor here is “cash flow and embedded software revenue.” - While hardware-centric tech stocks are vulnerable to cyclical fluctuations, platforms that combine software and services possess stronger margin defense even during downturns.

- As Tesla expands FSD revenue recognition, charging network earnings, and insurance/lease revenue, its defensive capabilities in volatile phases are enhanced.

7) Checklist for Long-Term Investors: Filtering the Noise, Focusing on the Signals

Product Signals: Whether the “monthly payment calculator/financial terms” are updated simultaneously with the website pricing.

Supply Signals: Shipping/distribution slots in Shanghai and Austin, roll-over rates, and lead times.

Demand Signals: Weekly trends in registered units in major Chinese cities, lease approval speeds, and inventory days.

Software Signals: Expansion in the functional scope in FSD release notes, regional activation maps, and the decrease in deferred revenue.

Margin Signals: Changes in option mix, increased LFP proportion, and a rising share of revenue from insurance/energy/charging.

Macroeconomic Signals: Updates on the global economic outlook, the direction of real interest rates, the potential for inflation to reheat, and the synchronization of a strong dollar with commodity prices.

8) Conclusion: What the Market is Overlooking

The Austin “embargo circumstances” imply more than just a new vehicle announcement.

For a significant volume boost, price (or monthly payment), website functionality, lease/insurance, and shipping slots must move simultaneously.

Q4 in China is notable as “full-forward” demand—driven by an impending tax transition—overlapping with seasonality, and it is worth targeting performance above the baseline scenario.

In robotaxi, it is not the performance demos but “revenue recognition and fleet operations” that change the numbers.

Goldman’s warning is not meant to scare, but to serve as a filtering hint.

In an environment of interest rates and liquidity, the survival of tech stocks versus electric vehicles comes down to “cash flow + software margins.”

Long-term investors need only focus on these five aspects.

- Monthly payment trends.

- China delivery lead times.

- FSD functional scope and reduction in deferred revenue.

- The revenue mix from charging/insurance/energy.

- The direction of real interest rates.

If these remain stable, short-term volatility will eventually prove to be an ally.

[Related Articles…]

Is Tesla’s Budget Model About to Launch? 5 Signals Investors Should Watch First

Robotaxi Commercialization Checklist: The Numbers That Revenue Recognition and Fleet Operations Will Change

*Source: [ 허니잼의 테슬라와 일론 ]

– 테슬라 신규 이벤트 준비 정황! ‘중국 4분기’ 수요 증가 추가 정황! 하지만 대폭락 경고하는 골드만?

● Korea vs Chaos – Free Trade Collapse – Energy Wars Shadow Finance AI Pivot

[2025-2027] South Korea’s Survival Strategy after the Collapse of Free Trade: A Roadmap for the Transformation of Energy, Finance, and AI Supply Chains

The following text includes three core frameworks that are rarely discussed in other YouTube channels or news outlets.

First, as the power demand of AI data centers transforms into the next generation of “crude oil,” it unveils the invisible mechanism by which energy and power grids reshape the global economy and geopolitics.

Second, instead of the slogan “replace the dollar,” it quantifies the real impact on Korean exports, exchange rates, and interest rates created by “sanction-evading payment networks” and “prepayment secured by gold and raw materials.”

Third, it provides an actionable checklist showing what Korean companies and policymakers must change within a 0–36 month timeline to avoid the “all-die-in-alliance trap” and overcome the global cycle of inflation and recession.

1) Developments 2022–2024: The Economics of ‘Disorder’ Created by an Energy War

The Russia-Ukraine war was won not only by gunfire but also by supply lines through pipelines, shipping insurance, and long-term LNG contracts.

Europe, having lost inexpensive Russian gas, entered a state of structural deindustrialization due to soaring electricity prices and declining industrial competitiveness.

The Western price cap on crude oil bolstered the arbitrage channels for India and China’s re-refining, thus propping up Russian finances.

While the U.S. kept interest rates “relatively high” for a prolonged period to curb inflation, its net interest expenses grew to levels matching or even exceeding defense spending, thereby constraining fiscal capacity.

The WTO’s dispute resolution mechanism is virtually paralyzed, and the “normless policies” of tariffs, subsidies, and export controls in the 232/301 format have become the new norm.

Payment networks have shifted from dollar hegemony to “safeguard diversification.”

By accumulating traffic in circumvention networks like China’s CIPS, India’s UPI/Rupee Vostro, and Russia’s MIR, gold purchases have emerged as a crucial hedge for emerging market foreign exchange reserves.

2) Policy Environment in 2025: ‘The Time of Policy’ and the Leverage Game

The United States has a strong incentive to maintain and even intensify bipartisan public and global subsidies as well as retaliatory tariffs.

Reevaluations of subsidies, redesigns of tax credits, and the risk of retroactive application of regulations may become realities.

“Merely nominal FTAs” are becoming common, while substance transitions into deals combining trade and security.

Even among allies, leveraging positions to push through, and then rewriting the rules once the other side perseveres, becomes the “rules of the game.”

South Korea must increase its hidden leverage positions rather than relying solely on explicit agreements to gain negotiating power.

3) Scenarios for 2025–2027: Base, Bear, Bull

-

Base Scenario

Tariff barriers remain in the 15–25% range, with alternating periods of a strong and weak dollar, leading to increased exchange rate volatility.

Europe, despite improvements in the spread between natural gas JKM/TTF, fails to reshore manufacturing due to delays in investing in its power grid.

The power demand of AI data centers encroaches upon non-IT power, continuing to put upward pressure on electricity prices. -

Bear Scenario

Disruptions in Middle Eastern shipping and insurance or delays in gas pipelines cause a surge in spot LNG prices.

A rebound in U.S. interest rates and a sharp strengthening of the dollar lead to a liquidity crunch in emerging market foreign currencies.

A recurrence of a global recession simultaneously shocks Korean exports and exchange rates. -

Bull Scenario

The U.S., China, and India expand individual deals on current issues to ease some tariffs and subsidies.

Europe accelerates investments in its power grid and restarts nuclear power plants, stabilizing wholesale electricity prices.

The introduction of AI efficiency technologies (compression, low precision, optical interconnects) greatly improves performance per watt.

4) South Korea’s Chronological Roadmap: 0–36 Month Implementation

-

0–6 Months: Strengthening Liquidity and Basic Energy Infrastructure

Adjust overseas debt durations to a barbell structure centered on 2–3 years, and increase the proportion of T-bills/cash-equivalent dollars.

Secure additional long-term LNG off-take options for KOGAS and large-scale power plants for periods beyond 2030, and pre-allocate FSRU (Floating Storage Regasification Unit) charter rights.

Initiate pilot projects for payment currency diversification.

Test partial RMB trade settlements via CIPS and conduct tests for trade settlements linked to crude oil/refined products using India’s INR Vostro.

Break down U.S. CAPEX into “US +1,” and hedge risks by parallel investments in locations within Mexico/Canada/Europe that offer good access to low-carbon power. -

6–18 Months: Simultaneous Design of Industry, AI, and Power

Expand HBM and advanced packaging (2.5D/CoWoS/FO-PLP) capacity through a one-stop system that approves power, water, and cooling in tandem.

Major domestic data centers will pilot dual PPAs by bundling renewable energy PPAs with nuclear power contracts.

For AI training, establish joint centers in overseas “low-cost power” bases (e.g., Nordic, Canada, UAE), while domestic operations in Korea focus on inference and workloads with sensitive personal data.

Increase investments in “export-control evasion-type” open stack ecosystems—such as RISC-V, HBM-PIM, and optical link NIC—to ease supply chain constraints.

Launch a flexible refinery slate project to address Venezuela/Mexico heavy crude in the oil refining and petrochemical sectors. -

18–36 Months: Shifting the Center of Gravity in Institutions and Diplomacy

Expand KEXIM and non-guaranteed local currency loans and guarantees to regularly facilitate non-dollar trade finance in currencies such as the Rupee, Yuan, and Dirham.

Slightly increase the weight of gold in reserves and partially introduce prepayment structures secured by raw material collateral to preemptively secure resource access.

Simultaneously enter projects in the Middle East and Southeast Asia with consortia for smart nuclear power plants, SMRs, and high-level waste processing technologies.

Deploy an AI compliance engine that monitors sanctions and secondary risks in real time to export companies.

5) Key Points: The “Invisible Levers” Most Overlook

AI power demand is altering the trajectory of prices and interest rates.

Due to bottlenecks in expanding power grids, data centers are driving up industrial electricity prices, thereby creating underlying inflationary pressures.

If Korea does not integrate power and water permits with semiconductor/AI investment reviews, it will lose leadership in the global economic transformation.

“Shadow settlements” reduce not dollar usage, but the “velocity of the dollar.”

Gold purchases, raw material collateral prepayments, and bilateral currency settlements are not about switching reserve currencies but about reducing the turnover of dollars, thereby weakening the transmission channels of interest rates and exchange rates.

The Korean exchange rate is more likely to couple with the “non-dollar settlement share” rather than simply following the dollar DXY.

Shipping insurance and reinsurance act as invisible choke points.

If P&I clubs and reinsurance regulations tighten, the physical transport of crude oil and LNG will be hampered, causing prices to spike irrespective of policy, and premiums for sanction-evading vessels will rise.

Diversifying import sources and increasing FSRU and inventory days are the lowest-cost options to offset insurance risks.

The microstructure of the U.S. Treasury market is the real indicator of fluctuations in Korean interest rates and exchange rates.

If clearing mandates, buybacks, and basis trade regulations occur simultaneously, liquidity will thin out, leading to frequent interest rate jumps.

Domestic bond duration management must be adjusted automatically based on a rule-based system linked to U.S. Treasury liquidity indicators.

6) Practical Design of a Korean-Style ‘Diversification’: Alliances That Don’t Fail Together

Maintain alliances, but reduce dependency.

Continue investments and supply in the U.S. while presenting numerical evidence of Korea’s indispensability in energy, power, and data to create leverage at the negotiating table.

Data on job creation and tax revenues in the U.S., as well as Korea’s power resilience and HBM market share, will boost negotiating power for tariff and regulatory exemptions.

At the same time, in India, the Middle East, and ASEAN, secure a position as an indispensable supplier through localization rates, technology transfers, and workforce development packages.

7) Monitoring Checklist: Numbers That Change Behavior

-

Energy

EU gas storage rates, 3-month averages of JKM/TTF spreads, German base-load power futures. -

Finance/Exchange Rates

Trends in U.S. net interest expenses, U.S. Treasury auction coverage/primary dealer indicators, shifts in the holding countries in TIC data, dollar DXY/won implied volatility. -

Payments/Raw Materials

Overseas transaction volumes for CIPS/UPI, gold purchases by the PBoC/RBI, India’s imports of Russian crude and the operational rates of its refineries. -

AI/Industry

Domestic data center PPA contracted capacity, HBM shipment and post-processing capacities, lead times for approval of server power capacity expansions.

8) Risks and Hedges

-

Risks

Disruptions in shipping in the Middle East/Black Sea, a resurgence in U.S. interest rates, European power grid failures, and expanded export controls on semiconductors. -

Hedges

Spot LNG call options, increased holdings of gold/cash equivalents, distributed data centers in the U.S./Nordic/UAE regions, and diversification into commodity currencies such as CAD and NOK.

9) The Intersection of AI Trends and the Economy: Investment and Policy Prioritization

The bottleneck in AI is no longer the “number of GPUs” but the “watts, wires, and water.”

Companies that secure water, transmission lines, and substation capacities first will have an edge in AI competitiveness.

On the modeling side, low-precision (8/4/2-bit), knowledge distillation, serverless inference, and on-device edge models drive higher performance per watt.

Korea has the opportunity to lead global standards in “memory-centric AI” by leveraging its technological edge in HBM and packaging.

The state must create an investment framework that, through a “power-adjacent location permit system” bundled with data centers, grids, and industrial complexes and standardized long-term PPAs, provides robust investment structures resilient to shocks in interest rates and exchange rates.

10) Conclusion: A Korean-Style Survival Formula after the Collapse of Free Trade

The essence is simple.

Dollar hegemony is losing momentum, energy is reclaiming price-setting power, and AI is driving electricity demand.

In such an environment, Korea must maintain alliances while reducing dependency, and re-engineer its settlement currencies, energy, power, and data as an integrated bundle.

Only diversification with a timeline can transform an “all-die-in-alliance” into an alliance where everyone wins.

In the process, monitoring indicators of global inflation, interest rates, the dollar, exchange rates, and recession signals numerically—and realigning the sequence of investments and diplomacy—will be the decisive move.

< Summary >

- The energy war undermines Europe’s manufacturing competitiveness, and AI’s power demand creates a new ceiling for inflation.

- It is not about replacing the dollar but about the diversification of settlements, with an increase in gold- and raw material-collateralized transactions.

- The United States institutionalizes tariffs, subsidies, and export controls, making leverage-based diversification essential for Korea.

- A 0–36 month roadmap simultaneously designs investments in liquidity, LNG, payment settlements, AI power, HBM, and localization.

- Monitoring indicators and hedging against shocks in interest rates and exchange rates turn “disorder” into an opportunity.

[Related Articles…]

- The Cracks in Dollar Hegemony and the Future of Raw Material Settlements

- The Clash between AI Semiconductors and Energy Security

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [풀버전] “세계 강국 미국도 무너진다”… 자유무역 붕괴 속 한국의 대응 전략은? | 경읽남과 토론합시다 | 진재일 교수