● Record Long Rate Gap, FX Shock Risk, Liquidity Data Switch Alarm

FX Pressure Driven by the “Largest and Longest” Korea–U.S. Rate Differential, and the Underappreciated Risk of Monetary Aggregate Redefinition

This report focuses on three points:1) The structural mechanism by which the “maximum and prolonged” Korea–U.S. rate differential tends to weaken the KRW.

2) Why the Bank of Korea’s discussion of “monetary aggregate changes” can distort policy assessment (optical effects) and create justification for broader liquidity expansion.

3) A clear allocation of “who is responsible for FX stability” under Korea’s framework, and why markets currently perceive limited policy authority.

1) News Briefing: Three Core Issues

1-1. Korea–U.S. rate differential: record high (2%p) + record duration = persistent KRW discount

The repeated message is straightforward: if the U.S. maintains higher rates for longer while Korea does not match, capital reallocates toward higher-yielding assets. Over time, FX markets price a higher probability of structural KRW weakness.

The critical factor is not a short-lived spread but its prolonged duration. As the period extends, markets interpret it as policy regime rather than a temporary event, increasing the likelihood of a higher equilibrium FX level.

1-2. Monetary aggregates (e.g., M2) redefinition: the issue is not the number, but the policy rationale

The Bank of Korea indicated that current aggregates may not reflect effective liquidity. The concern is that redefining the aggregate could mechanically lower reported money growth (e.g., to around 5%), which may be interpreted as a signal that additional easing is acceptable.

A central dispute is how ETFs and other beneficiary certificates should be treated. One view argues these instruments are not readily cash-convertible and their inclusion distorts liquidity measures. The opposing view is that they can still be converted into liquidity and excluding them could be more misleading.

1-3. Responsibility for FX stability: separation between accountability and execution

Under Korea’s framework, the Ministry of Economy and Finance determines FX market stabilization actions (smoothing operations), while the Bank of Korea executes them (USD/KRW transactions).

Market discomfort increases when officials attribute KRW weakness to retail overseas investing, because investors and corporates optimize returns rather than targeting FX stability. USD demand is an observed outcome; stabilizing expectations is the policy function.

2) How the Rate Differential Transmits into FX Depreciation (Structural Mechanism)

2-1. Rate differential → capital flow → expectations → higher FX level persistence

A widening Korea–U.S. spread typically unfolds in stages:

1) Yield gap widens: increased preference for USD assets (U.S. Treasuries, MMFs, USD deposits, U.S. equities).

2) Capital outflows / higher USD demand: retail investors, institutions (including pension funds), and corporates increase USD purchases.

3) Expectations form: markets pre-price “continued KRW weakness.”

4) Level persistence: corporates and investors delay selling USD, and the FX rate becomes less responsive downward.

The fourth step is critical: FX is shaped not only by flow but also by expectations. Policy credibility is required to reset expectations; the current concern is that markets do not perceive sufficient authority.

2-2. Trade-off between domestic support and external balance: key vulnerability for a small open economy

As a small open economy, Korea cannot ignore external balance (capital flows and FX stability). A stronger tilt toward domestic stimulus can delay rate responses, widen the rate differential, and increase FX volatility.

This raises questions about the degree of monetary policy independence and whether the practical U.S. benchmark constraint is being reflected in decision-making.

3) Why Redefining Monetary Aggregates Can Create “Policy Optical Effects” (Primary Risk)

3-1. Redefinition is a policy-communication issue, not a technical issue

Monetary aggregates are not merely statistics; they are a shared language between policymakers and markets. If the definition changes, policymakers can argue “money growth is low, easing is possible,” while markets may interpret it as “liquidity expansion is coming.”

In a period of heightened FX sensitivity, any perceived easing signal can reinforce KRW depreciation expectations. The key point is the linkage between aggregate redefinition and FX expectations.

3-2. Should ETFs/beneficiary certificates be treated as money? Focus on cash convertibility and behavioral change

A notable claim was that ETFs previously exited quickly like cash-equivalents, but recent redemption/exit behavior has been limited. If correct, including ETFs in M2 could overstate effective liquidity and make policy appear tighter than it is.

The counterargument is that these assets remain convertible into liquidity, and excluding them could create a different distortion. The primary risk is not inclusion/exclusion per se, but whether the change is interpreted as expanding room for easing.

4) Who Owns FX Stability: Signals of Weakened MOEF Authority

4-1. Smoothing operations: perceived willingness matters more than nominal capacity

Based on cited figures (FX reserves approximately USD 430bn; spot market turnover roughly USD 13–14bn per day), Korea is viewed as having operational capacity to stabilize markets.

Despite this, FX instability persists because markets do not observe credible authority signals. Historically, strong verbal intervention alone has deterred speculative positioning; current signaling is viewed as weaker.

4-2. Risks of the “retail overseas investors are to blame” narrative

Overseas allocation by households, corporates, and pension funds can be a response rather than a root cause. When macro uncertainty and depreciation expectations rise, shifting toward perceived safer assets is rational.

If authorities emphasize this narrative, markets may infer that policymakers are dispersing accountability rather than managing expectations. This can add a “policy risk premium” to the FX rate.

5) Key Items to Monitor for Korea Monetary Policy and FX in 2026

1) The speed and rationale of Korea–U.S. rate differential narrowing.

2) Whether monetary aggregate redefinition is announced, and how it is communicated to markets.

3) If domestic stimulus strengthens, whether safeguards exist to prevent liquidity expansion from amplifying depreciation expectations.

4) Whether MOEF verbal and actual intervention appears rule-based and consistent (predictability supports credibility).

5) Whether an AI-driven cycle (semiconductor upcycle) creates growth “optics” that evolve into easing justification.

6) The Single Most Important Point

The central issue is not directional FX forecasting. The primary risk is that monetary aggregate redefinition is interpreted as justification for additional liquidity, which can lock FX expectations at a higher level.

Rate differentials are numeric; monetary aggregates are the policy language. When the language changes, markets may infer a change in direction, and FX markets often move first on expectations.

< Summary >

If the Korea–U.S. rate differential remains at record highs for an extended period, capital flows and expectations tend to entrench KRW weakness.

Redefining monetary aggregates is not merely a statistical adjustment; it may be read as an easing rationale and can amplify depreciation expectations.

In Korea, MOEF holds decision authority for FX stabilization while the Bank of Korea executes operations; markets currently focus on perceived weakening of policy authority.

Attributing FX pressure to retail investors or corporates describes the symptom; expectation management and credible signaling remain the key policy variables.

[Related Articles…]

- https://NextGenInsight.net?s=FX

- https://NextGenInsight.net?s=interest%20rate

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 환율 책임은 누가 지는가? 한미 금리차 사상 최대·최장 기록… 환율이 무너질 수밖에 없는 이유 | 심층토론 – 김대호, 노영우 3편

● Korea FX Defense Crackdown, Dollar Outflows Targeted, Retail Investors Hit

FX Defense Has Effectively Begun: Comprehensive Policy Scenarios Targeting Retail Overseas Investors, Corporate USD Holdings, and Pension Flows

This report covers:

First, why Korea’s FX-defense approach is likely to follow a “gradual tightening → large step after a threshold is breached” pattern.

Second, how policy may tighten “USD outflow channels” rather than banning overseas equity investing itself.

Third, how to interpret the “investor protection” framing and the signals it sends to markets.

Fourth, three core drivers often overlooked in media coverage (credibility, sentiment, sequencing of regulation).

1) Key News Briefing (News-Style Summary)

① Bank of Korea messaging: “FX depreciation drivers = overseas investment and USD hoarding, not domestic liquidity”

The key point is the attribution of KRW weakness to “USD demand leaving the country (overseas investment) + corporate USD retention,” rather than to excess domestic liquidity.

This functions as an official rationale for defining future policy targets.

② Discussion of reducing disclosure on the National Pension Service’s overseas investments: limiting follow-on flows

A proposal to make the National Pension Service’s overseas investment details less transparent can be interpreted as an early-stage effort to shape public acceptance.

The implied linkage is: “NPS invests abroad → retail investors follow → USD demand rises → FX pressure increases.”

The signal is intent to weaken this transmission channel.

③ Financial authorities: pressure on brokerages to curb marketing of overseas investing

Publicly framed as investor protection, the practical message is to reduce activity that stimulates USD outflows at elevated FX levels.

Rather than direct bans, initial measures are more likely to focus on marketing, product distribution, and advertising channels.

④ Tighter regulation of overseas derivatives (mandatory pre-education and simulated trading)

Overseas derivatives have historically faced less stringent requirements than domestic products; mandatory education and simulated trading are being introduced.

While justified as protection for high-risk investors, markets may interpret this as restricting high-beta USD-outflow channels (options, leveraged ETFs).

⑤ Indications of FX smoothing: perceived intervention during evening/overnight sessions

Reports of abrupt, time-specific moves are consistent with “smoothing” intervention aimed at preventing a rapid upside acceleration.

A near-term objective may be to slow the pace of depreciation rather than force an immediate reversal.

2) Reframing the Policy Path Using a Real-Estate-Regulation Analogy

Core pattern: light restrictions → assess market response → progressively tighter measures → a decisive step at a critical threshold

Authorities often escalate in stages to manage side effects and public acceptance, implying a similar trajectory for FX-related measures.

In FX policy, rule-setting authority remains with the government

Households and corporates adapt to rules rather than set them.

In this environment, anticipating policy direction becomes a key component of risk management.

3) Two Potential Policy Targets: Retail Overseas Investors vs. Corporate USD Holdings

Target A) Retail overseas investors

Likely tools are indirect rather than outright prohibitions: marketing limitations, restricted access to higher-risk products, tighter derivatives rules, and stricter advertising standards.

These measures are operationally fast and supported by a strong “investor protection” rationale.

Target B) Corporates holding USD offshore/on balance sheet (cash-like USD deposits)

When corporates retain USD, market USD supply tightens and depreciation pressure can persist.

Authorities may therefore pursue incentives or pressure to increase USD conversion/supply, starting with softer tools such as voluntary agreements, strengthened guidance on FX-related prudential practices, or enhanced reporting requirements.

4) How to Interpret the “Investor Protection” Frame

1) Assess whether the primary objective is investor protection or FX-defense communication

Tightening rules on high-risk derivatives marketing can be justified on risk grounds.

However, broader restraints on overseas-investment marketing may be interpreted primarily as FX defense.

2) Timing risk: regulation introduced during FX instability can amplify fear rather than confidence

Even necessary investor-suitability measures may be perceived as control when announced during FX stress.

Such perceptions can reduce willingness to supply USD liquidity and reinforce defensive USD hoarding.

3) FX is primarily a credibility and confidence variable

Increasing USD supply requires confidence that stabilization is credible.

Fear-driven narratives can incentivize further USD retention, reinforcing a negative feedback loop that policymakers seek to avoid.

5) Three High-Importance Points Often Underemphasized in Media Coverage

Key point 1) The core is not banning overseas investing, but managing USD-demand channels

The likely objective is to stabilize FX supply-demand by addressing USD demand sources across households, corporates, and institutions.

This is better characterized as external-balance management than asset-market control.

Key point 2) The goal of intervention may be to break upside expectations, not to push spot materially lower

Once a higher FX level becomes the perceived “new normal,” pricing anchors change across households and corporates, structurally raising USD demand and policy costs.

Near-term focus may therefore be on preventing normalization of higher levels.

Key point 3) In the macro “triple set” (rates, inflation, USD strength), FX becomes the most policy-sensitive variable

In an externally exposed economy, FX depreciation transmits quickly into import prices and corporate cost structures.

FX is therefore not merely a market quote but a macro variable influencing both inflation and growth, with implications for USD-settled sectors such as semiconductors and technology.

6) Investor Checklist (Practical Considerations in the Current Regime)

① Separate policy risk from asset risk

Equity return prospects are distinct from potential changes in the operating environment for overseas investing (marketing rules, access conditions, derivatives constraints, remittance convenience).

② During FX volatility, execution mechanics can dominate portfolio decisions

FX movements are often felt before portfolio performance.

Staggered conversions, staged entries, and liquidity management of USD cash-like allocations may become more important.

③ AI and mega-cap exposure is structurally linked to USD demand

AI-related themes (semiconductors, cloud, mega-cap technology) can reinforce preference for USD assets.

Authorities may interpret AI-driven retail demand as incremental USD demand, increasing the likelihood that leverage-linked and aggressively marketed products face earlier scrutiny.

7) Monitoring Indicators (Phrases to Track in Upcoming Headlines)

1) Whether “investor protection 강화” expands from advertising limits to distribution or sales restrictions

2) Whether “cooperation requests” on corporate USD holdings evolve into guidelines or binding requirements

3) Whether disclosure of institutional overseas investment activity is materially reduced

4) Whether intervention shifts from “pace control” to explicit “level defense”

5) Whether global USD-strength drivers (US rates, inflation, growth expectations) conflict with domestic policy messaging

< Summary >

Authorities have increasingly framed KRW weakness as driven by overseas investment demand and USD retention, narrowing perceived policy targets to retail overseas investors and corporate USD holdings.

Measures such as guidance to curb overseas-investment marketing and tighter requirements for overseas derivatives are framed as investor protection but also function as FX-defense tools.

The likely emphasis is on managing USD-demand channels rather than prohibiting overseas equities, with stabilization dependent on credibility and sentiment as much as flow mechanics.

[Related Articles…]

During FX Surges: Key Checkpoints for USD Assets and Hedging Strategy

Rebalancing AI and Mega-Cap Exposure During Elevated Nasdaq Volatility

*Source: [ Jun’s economy lab ]

– 투자자보호를 위해 미국주식을 막아라(ft.환율대책)

● Trump Shock Plan Tariffs Energy Rate Cuts

Trump-Style “America Recovery” Remarks: Key Investor Takeaways

1) USD 18T investment framing

2) Tariffs to force reshoring

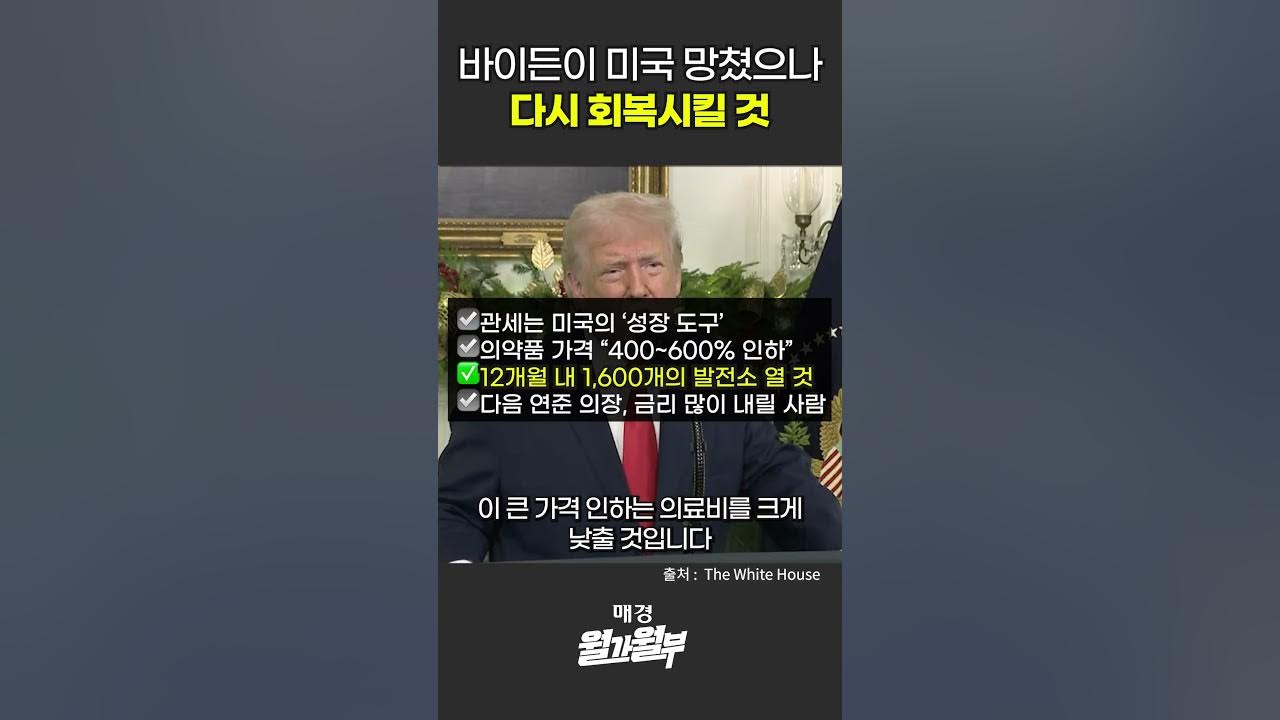

3) “400–600% drug price cuts” claim: verification points

4) Energy emergency + 1,600 power plants

5) Pressure for rate cuts via Fed chair replacement

…plus a “hidden variable” likely to move markets more materially

1) News Briefing: Reconstructing the Remarks as a Policy Package

1-1. “USD 18 trillion in investment inflows” framing

- Core message: attract record-scale capital into the U.S. to support jobs, wages, factory utilization, growth, and national security.

- Investor interpretation: the headline figure is less important than the reshoring and capital-repatriation narrative.

- Market implications:

- If implemented through combined domestic capex incentives and import barriers (tariffs), near-term demand may rise for construction, industrials, and power infrastructure.

- Stronger tariffs can raise import prices and reintroduce inflationary pressure.

1-2. “No tariffs if you build factories in the U.S.” (tariffs as reshoring leverage)

- Core message: tariff relief conditional on domestic production.

- Investor interpretation: tariffs positioned as a negotiation tool and industrial policy mechanism, not solely punitive.

- Market implications:

- Accelerated supply-chain restructuring; nearshoring (e.g., Mexico/Canada) may benefit as firms reconfigure North American production footprints.

- Export-oriented industries may face increased pressure to raise U.S. local production content, particularly autos, batteries, and semiconductors.

1-3. “400–600% drug price cuts” claim + tariffs shifting burden abroad

- Core message: large drug-price reductions via direct negotiation and/or coercive leverage.

- Verification points (investor lens):

- The “400–600%” phrasing is likely rhetorical and mathematically inconsistent as a literal price reduction; treat as political messaging until substantiated by policy text and pricing data.

- The substantive policy signal is intent to force lower U.S. prescription drug prices through stronger negotiation and regulation.

- Market implications:

- Potential margin and cash-flow pressure across U.S. healthcare stakeholders (notably large pharma and intermediaries) depending on policy design.

- Lower out-of-pocket costs could support real disposable income, but regulatory uncertainty can increase sector volatility.

1-4. “Energy emergency on Day 1” + gasoline at USD 2.50 + 1,600 power plants

- Core message: use energy policy to suppress inflation and reduce household cost burdens; rapid expansion of generation capacity.

- Investor interpretation: energy price control as an inflation lever; the feasibility of “1,600 plants” requires scrutiny given permitting, siting, transmission constraints, and financing.

- Market implications:

- Lower energy prices would mechanically soften headline inflation and strengthen expectations for rate cuts.

- Build-out efforts could trigger bottlenecks in copper, transformers, grid equipment, and turbines, raising selective input and industrial prices.

1-5. “Naming (replacing) the Fed chair” + “much lower rates”

- Core message: signal commitment to materially lower rates through leadership selection.

- Investor interpretation: challenges perceived central-bank independence; markets may reprice policy credibility and term premium.

- Market implications:

- Near-term equity support via lower discount-rate expectations.

- If political influence appears to dominate monetary policy, long-end Treasury yields and USD volatility may rise as investors demand higher risk premia.

1-6. “Aggressive housing reform” preview

- Core message: housing policy beyond rate policy, combining supply, regulation, and financing.

- Market implications:

- Housing materially affects U.S. household balance sheets and consumption via wealth effects; specifics could shift growth expectations.

- Rate cuts alone can reignite prices by stimulating demand; supply expansion is necessary for sustained affordability.

2) Three Macro Scenarios Implied by the Package

2-1. Scenario A: “Energy decline + gradual rate cuts” (benign disinflation)

- Energy stabilization → inflation deceleration → Fed obtains room to cut → easing cycle begins

- Potential tailwinds for growth equities, housing activity, and consumption; higher odds of a soft-landing configuration

2-2. Scenario B: “Tariff escalation → higher import prices → inflation re-acceleration”

- Reshoring may progress, but near-term costs rise

- Inflation persistence delays easing; higher volatility across rates and risk assets

2-3. Scenario C: “Fed pressure controversy → higher bond and FX volatility”

- “Rate cuts” rhetoric supports equities

- Perceived erosion of Fed independence can feed into higher term premium and unstable long-end yields

3) AI Trend Implications

3-1. Generation and grid build-out as the binding constraint for AI data centers

- Competitive advantage in generative AI increasingly depends on power availability, transmission, cooling, transformers, and turbines.

- Power and grid expansion signals can be interpreted as enabling conditions for data-center scaling.

3-2. Tariffs/reshoring and AI hardware supply-chain restructuring

- Tariff pressure can alter procurement of GPU servers, networking equipment, and component supply chains.

- AI is software-driven but is increasingly sensitive to manufacturing, logistics, and energy policy.

3-3. Rate-cut expectations as a direct driver of AI/tech valuation

- Lower rates increase the present value of long-duration cash flows, supporting growth and platform businesses.

- Fed leadership signaling can transmit quickly into AI-sector multiples.

4) Under-Discussed Points with High Investor Relevance

4-1. Tariffs generally raise prices rather than reduce them

- Messaging that “foreigners pay” conflicts with typical pass-through dynamics; tariff costs often transmit to domestic prices.

- Achieving reshoring and simultaneous price stability is operationally challenging.

4-2. Lower rates may help equities but can destabilize the USD and long-end Treasuries

- Greater political proximity to monetary policy can raise required risk premia.

- Short-rate expectations can fall while long-end yields remain sticky or rise.

4-3. Drug-price cuts support households but may weigh on innovation investment

- Lower medical costs can lift consumer purchasing power.

- Reduced pharma cash flow can pressure R&D intensity and pipeline valuation.

4-4. The primary battleground is power: AI, manufacturing, and EVs compete for electricity

- The critical issue is execution bottlenecks: transmission, transformers, permitting, and local opposition.

- Failure to resolve these constraints limits both AI scaling and industrial expansion.

4-5. Housing reform can alter the business cycle

- Housing policy materially affects consumption and credit conditions.

- Investors should evaluate reform as a combined package: supply expansion, regulatory changes, and financing rules.

5) Practical Monitoring Checklist

- Whether tariff escalation becomes actionable through formal proposals or executive actions

- Whether energy policy prioritizes price stabilization versus production expansion

- Whether Fed-chair commentary measurably weakens perceived independence and credibility

- Whether drug-price policy is implemented via negotiation tactics versus statutory/regulatory change

- Whether housing reform is demand-stimulative or supply-expansive (a key determinant of price direction)

< Summary >

- The remarks bundle a policy package: reshoring via tariffs, inflation via energy, cost-of-living via drug prices, and rates via Fed leadership.

- The central investor issue is not the growth narrative, but the potential conflict among inflation dynamics, supply-chain restructuring, and rate-cut expectations.

- From an AI perspective, power and grid capacity are critical for data-center expansion, while rate sensitivity directly influences tech valuation.

[Related Links…]

- NextGenInsight.net?s=interest%20rates

- NextGenInsight.net?s=inflation

*Source: [ Maeil Business Newspaper ]

– 바이든이 미국 망쳤으나, 다시 회복시킬 것 #shorts