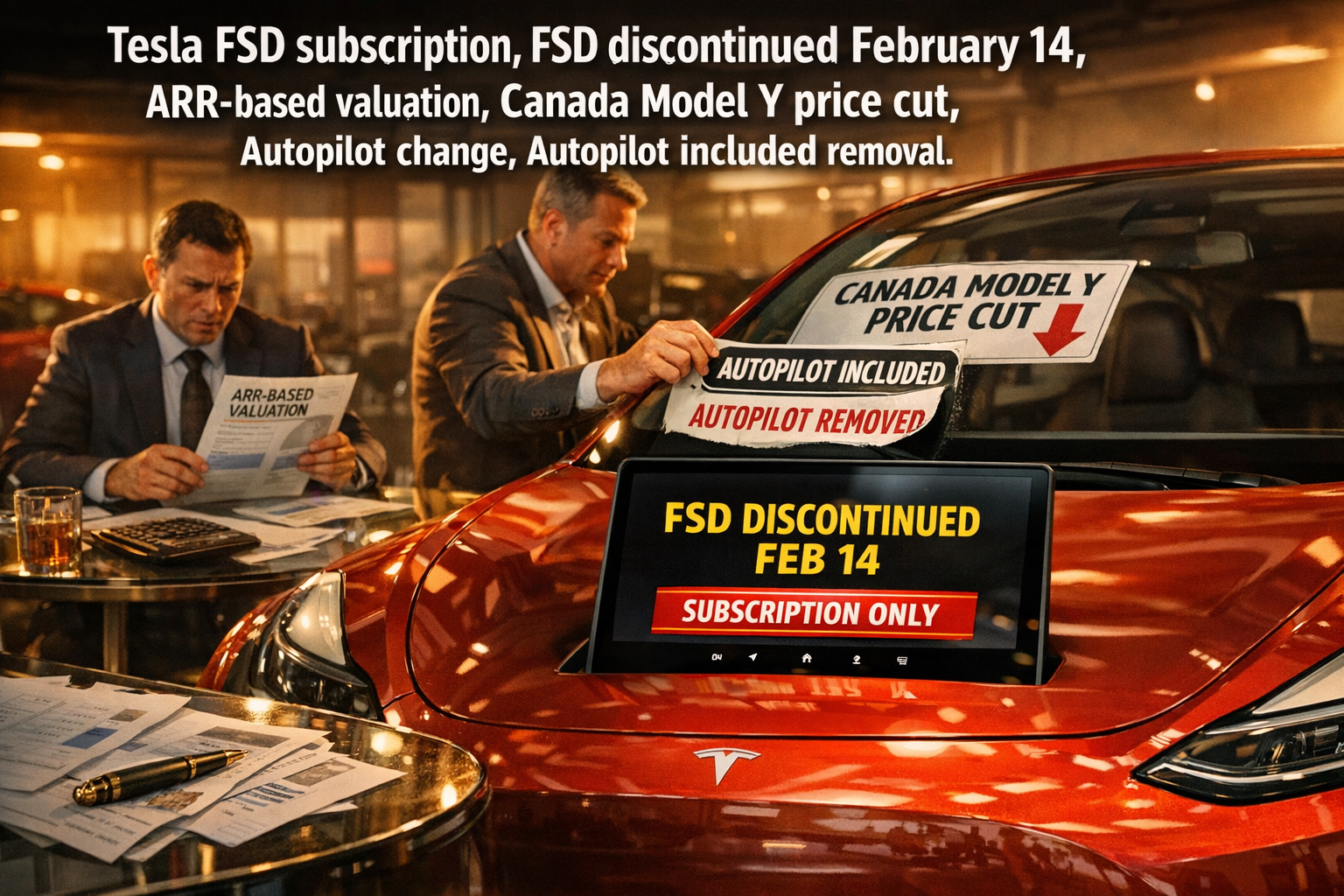

● Tesla Kills FSD Buyout, Subscription Only After Feb 14 – Platform Pivot, Cash Grab, Console Style Monetization

Imminent Suspension of FSD One-Time Purchases: Tesla’s Next Move Toward “Subscription-Only” After February 14

This report focuses on three points:1) The underlying objective behind Tesla making FSD unavailable as an outright purchase (beyond surface-level pricing policy).

2) How the change reshapes Tesla’s earnings, cash flow, and equity valuation framework through a subscription-economy lens.

3) A key signal often overlooked: how “low-cost trim expansion + removal of Autopilot wording” indicates a shift toward a console-style business model.

1) Key Development: “FSD One-Time Purchase to Be Discontinued After February 14”

What is happening

Tesla is signaling that after February 14, 2026, Full Self-Driving (FSD) will effectively no longer be offered as a one-time purchase and will be provided primarily via a monthly subscription.

Surface interpretation

A shift from an $8,000 upfront option to a $99/month subscription.

Core implication

This is less a pricing adjustment and more a strategic step toward positioning Tesla as a software/platform business rather than a pure automaker. The market is likely to emphasize subscription-based cash flows (ARR) over traditional auto-sector multiples.

2) Symbolic Timing: Washington, DC Autonomous-Driving Hearing and Musk’s “Discontinue Sales” Signal

Why timing matters

The messaging coincided with a US House hearing addressing autonomous-driving regulation (deployment limits, liability frameworks).

Interpretation

Tesla appears to be reinforcing a monetization roadmap centered on subscriptions/platform economics as regulatory frameworks evolve. Regulation tends to move slowly; market narratives and monetization models can shift more quickly.

3) Tesla News Briefs (3 Items)

3-1) Euro NCAP 2025 Results: Model 3 and Model Y Ranked #1 in Their Classes

- Model 3: #1 in the Large Family Car category.

- Model Y: #1 in the Small SUV category.

- Euro NCAP described Model Y as the “gold standard” for small SUV safety.

Why it matters

Safety performance supports brand credibility and can influence insurance outcomes, regulatory perceptions, and consumer trust. Euro NCAP increasingly reflects driver-assistance system improvements, including OTA-driven enhancements, implying that software updates are being recognized as a core safety component.

3-2) Firebaugh, California: Major Charging Hub Expansion (304 Stalls + 16 Megachargers)

- Expansion from 72 to 304 chargers (adding 232).

- Addition of 16 Megachargers for Semi trucks.

Why it matters

This is a logistics and freight infrastructure play rather than a consumer convenience story. Along the I-5 corridor, a dedicated heavy-duty charging network can become a defensible moat as Semi volumes scale, supported by operational data and service infrastructure.

3-3) US EV Sales Data: Gap Between “Tesla Share Loss” Narrative and Observed Drivers

- Model 3: 192,000 units in the US (+1.3% YoY).

- Model Y: 357,000 units in the US (-4% YoY), with factory downtime and product transition effects (Juniper) cited as major drivers.

Key framing

In a slowing or stagnant EV market, the relevant comparison is often relative resilience rather than absolute share headlines. Maintaining scale through a downcycle can increase leverage when rates decline, demand recovers, and new products launch.

4) Why Now: Cash-Flow Support During a Seasonally Weaker Q1

Practical driver

Q1 is typically seasonal weakness for autos, following year-end discounting and deliveries.

Mechanism

A firm deadline (February 14) can trigger pre-deadline demand and encourage some buyers to choose the $8,000 one-time purchase.

Financial impact

Even if portions are deferred as revenue, cash collection occurs immediately, supporting near-term liquidity and financial flexibility in a higher-rate environment.

5) Primary Strategic Objective: Reframe Valuation Around ARR

Why subscriptions matter

Investors typically assign higher multiples to predictable, recurring revenue than to one-off feature sales.

Tesla application

- From: vehicle sales-driven model (manufacturing multiple).

- To: installed base monetization via recurring software payments (platform/service multiple).

Broader implication

A higher share of recurring revenue can reduce sensitivity to macro variables (rates, inflation, supply-chain volatility, FX), potentially shifting perception from cyclical exposure toward cash-flow durability.

6) Underappreciated Signal: Canada Low-Cost Model Y + Removal of “Autopilot Included” Wording

Canada development

A Model Y Standard Range RWD launch at an aggressive price point, consistent with supply/production optimization.

Cost-down configuration

Elements aligned with an entry-level strategy (e.g., simplified trims and component standardization).

Critical signal

Early website wording indicating “Autopilot included” was reportedly removed.

Why it matters

If baseline driver-assistance access is reduced on lower-cost hardware while higher functionality is unlocked via subscription, Tesla moves further toward:

low-margin hardware distribution + high-margin software monetization.

Business-model interpretation

This resembles a console-style model: hardware adoption expands the installed base; software/services drive lifetime monetization.

7) What the Incentives Suggest: FSD Subscribers as a Strategic KPI (10 Million Target)

A key point is the linkage between performance incentives and targets consistent with large-scale FSD subscriber adoption.

Why subscriptions scale better than upfront purchases

An $8,000 price point limits mass-market penetration; $99/month lowers the entry barrier and supports trial-to-retention conversion.

Illustrative scale

- 10 million subscribers × $99/month = $990 million/month

- Annualized: approximately $12 billion

Primary lever

The central impact is margin structure: software revenue typically scales with limited incremental cost, supporting operating leverage and cash-flow expansion.

8) Why Tesla Can Shift to Subscription: Confidence in FSD Performance and Next Releases (14.3/14.4)

Subscription risk

If product performance is insufficient, churn increases quickly.

Implied stance

The shift indicates confidence that FSD is moving toward a level of reliability that can sustain recurring payments, supported by positive reception to recent builds and expectations for further improvements.

Market messaging

A subscription-only strategy is consistent with positioning FSD as a mature, monetizable product rather than an experimental add-on.

9) Consumer-Level Tradeoffs: Existing Purchasers vs New Entrants

9-1) Existing one-time purchasers

A one-time purchase may become a scarcer attribute, potentially influencing used-vehicle pricing for buyers who prefer avoiding recurring fees.

9-2) Transferability across vehicles

To reinforce subscription economics, entitlement is more likely to remain tied to the vehicle or contract rather than freely transferable.

9-3) New buyer impact

A subscription model enables structured trials (e.g., limited-duration access, promotional periods), which can accelerate adoption and conversion.

10) If FSD Approaches Full Autonomy, Pricing Context Shifts

Time value

If driving time becomes productive or discretionary time, subscription cost can be framed as time purchase rather than feature purchase.

Household vehicle count

Autonomous pickup/drop-off functionality could reduce the need for secondary vehicles in some households.

Asset monetizationIf vehicles can generate revenue during idle time (robotaxi model), the vehicle shifts from consumption to income-generating asset, making FSD a cash-flow enablement layer rather than an optional feature.

11) Conclusion: February 14 as a Business-Model Repositioning Event

The discontinuation of one-time FSD purchases aligns with:

- A short-term objective: Q1 cash-flow support via pre-deadline uptake

- A long-term objective: reframing Tesla toward ARR-based platform valuation

The Canada entry-trim strategy and changes to Autopilot positioning reinforce a potential shift toward an installed-base monetization model: aggressive hardware adoption paired with recurring software revenue.

Most Material Takeaways

1) The core issue is not FSD pricing; it is Tesla’s effort to shift its peer group and valuation framework toward subscription software economics.

2) The Canada low-cost Model Y and the removal of “Autopilot included” wording may indicate testing of a console-style model: low-margin hardware expansion paired with software monetization.

3) Subscription-only conversion increases execution risk due to churn sensitivity, implying internal confidence in product performance improvements.

< Summary >

Tesla is strongly signaling a shift away from one-time FSD purchases toward a subscription-first model after February 14.

The change supports seasonal cash-flow management while advancing an ARR-driven valuation narrative.

The Canada entry-level Model Y strategy and Autopilot messaging changes may indicate a broader move toward hardware-led adoption with recurring software monetization.

Overall, February 14 functions less as a pricing update and more as a platform-transition milestone.

[Related Articles…]

- Impact of autonomous-driving regulatory shifts on the robotaxi market: https://NextGenInsight.net?s=autonomous-driving

- How subscription economics reshape valuation frameworks (ARR-based): https://NextGenInsight.net?s=subscriptions

*Source: [ 오늘의 테슬라 뉴스 ]

– FSD 판매 전격 중단! “이제 돈 주고 못 산다” 2월 14일 마지막 기회, 일론의 진짜 의도는?

● Rate-Hold Shock, Won Whiplash, FX Band-Aid Fails

Why the KRW Rebounded After the Bank of Korea’s “Five Consecutive Holds”: The Core Link Between Rates, FX, and Intervention, and the Worst Trap Korea Could Face in 2026 (Entrenched Low Growth)

Key points:

① Why the Bank of Korea had limited room to move despite FX instability.

② Why FX intervention can act as a short-term band-aid but rarely addresses structural drivers.

③ Why the KRW/USD is being driven less by sentiment and more by capital-flow structure and the policy mix.

④ What policy package is required to target both FX stability and growth support, including sequencing.

⑤ From an AI-trend perspective, how FX volatility affects investment across Korea’s AI value chain and inbound global capital.

1) News Briefing: Bank of Korea’s First 2026 Rate Decision — “Fifth Consecutive Hold”

Key facts

The Bank of Korea’s Monetary Policy Board kept the policy rate unchanged at 2.50%.

This extends the sequence to five consecutive meetings without a rate change.

Market backdrop

The KRW/USD moved up to the 1,470 range (as cited), making a near-term rate cut more difficult.

The Korea–U.S. policy-rate differential was cited at approximately 1.25%p; wider differentials can increase capital outflow pressure and weaken the KRW.

Keywords

Monetary policy, policy rate, KRW/USD, foreign exchange reserves, inflation.

2) Immediate Interpretation: Why Not Raise Rates Despite FX Stress? The Policy Transmission Mechanism

(1) The Bank of Korea cannot react to FX alone

The policy rate is a multi-objective tool covering inflation, growth, and financial stability, not only FX stability.

While FX considerations may imply tighter policy, higher rates transmit quickly to growth and financing conditions, including household and corporate debt-service burdens.

(2) Inflation conditions provide limited justification for hikes

With inflation referenced in the low-to-mid 2% range and the central bank’s outlook around the low 2% range, the incremental case for tightening appears limited based on inflation alone.

(3) Growth conditions raise the cost of tightening

Weak growth (referenced in the 1% range for 2025) increases the risk that additional tightening would further depress consumption, investment, and employment, reinforcing an entrenched low-growth regime.

(4) Conclusion: FX constrained cuts; it did not justify hikes

The hold reflects FX sensitivity that limits easing, while the growth trade-off makes tightening less feasible.

3) Why the FX Rate “Re-Spiked”: Structural Limits of Intervention (Band-Aid Effect)

(1) Intervention can work in the short term

Selling USD and buying KRW can cap the near-term upside in KRW/USD, particularly around year-end pricing dynamics.

(2) If underlying drivers do not change, renewed depreciation is a predictable outcome

Without changes to structural supply-demand and capital-flow dynamics, spot stabilization tends to fade and the exchange rate reverts toward underlying pressures.

(3) Repeated intervention can weaken perceived defense capacity

As intervention continues, reserve drawdowns become more salient and markets may discount future defense capacity into prices, potentially amplifying upside risk in KRW/USD.

4) The Core Issue: FX Framed Too Narrowly as Flow-Only

The key critique is that treating FX instability primarily as a near-term flow imbalance leads to policy responses focused on flow management (intervention, restrictions, guidance) rather than structural adjustment.

(1) Over-attributing FX moves to outbound equity investment can distort policy

Retail overseas equity buying and corporate outbound FDI are outcomes of portfolio choice and corporate strategy; suppressing them risks undermining capital-market credibility and creating broader distortions.

(2) If liquidity and relative money growth are not addressed, the currency can weaken structurally

If domestic money supply expands faster than that of the U.S., relative currency value can deteriorate over time. The policy implication is not a mechanical rate hike, but tighter management of the overall policy mix (fiscal, monetary, and stabilization tools) and the pace differential versus the U.S.

(3) Prolonged FX instability is more damaging for SMEs and mid-caps in manufacturing

Large exporters can hedge and pass through costs; smaller suppliers often face contract constraints that compress margins. This can translate into lower investment, weaker hiring, regional slowdown, and declining potential growth—conditions consistent with low-growth entrenchment.

5) Structural Policy Package: FX Stabilization First, Then Space for Rate Cuts

(1) Manage the pace of monetary and fiscal settings

The objective is not abrupt tightening, but controlling relative liquidity expansion so it does not outpace U.S. conditions. The key variable is the relative pace versus the U.S.

(2) Elevate inbound FDI as an FX policy lever

FX is materially driven by the capital account. If outbound investment cannot be eliminated, the policy focus shifts to increasing structurally durable inbound investment to rebalance flows.

(3) In 2026, the AI value chain can be a high-impact lever for FDI inflows

Relevant segments include HBM, GPUs, data-center power and cooling, semiconductor supply chains, and AI services. Bundling these into a national investment-attraction package can strengthen the rationale for larger and stickier USD inflows than traditional manufacturing-only strategies.

(4) Reframe regulation, labor, and taxation on a global competitiveness basis

The benchmark should be peer-country competitiveness rather than domestic historical comparisons, to improve the business environment required for sustained capital inflows that support FX stability.

(5) Reposition intervention as a secondary tool

Intervention remains useful for volatility smoothing, but should not be the primary line of defense given reserve costs and signaling effects that can heighten market stress.

6) AI Trend View: Three Channels Through Which FX Instability Impacts the AI Investment Cycle

(1) AI infrastructure capex is USD-linked

Prolonged KRW weakness raises the effective cost of servers, GPUs, and network equipment, potentially delaying or reducing domestic AI capex.

(2) A weaker KRW can create inbound strategic FDI opportunities

Currency weakness can make local assets and operating costs more attractive to global firms. Realizing this requires readiness in permitting speed, incentives, and institutional execution.

(3) Persistent FX stress can constrain monetary policy and slow counter-cyclical support

When FX stability dominates the policy constraint set, the central bank may have reduced room to ease even as growth weakens. Since AI ecosystems depend on financing conditions and risk appetite, simultaneous rate and FX instability can compress investment activity.

7) Key Takeaways Commonly Missed in Mainstream Coverage

① If “FX defense = intervention” becomes the default, markets will price its limits early

Repeated intervention elevates concerns about reserve depletion and policy capacity, which can widen the upside tail for KRW/USD.

② Current FX dynamics are increasingly structural rather than purely sentiment-driven

Attributing moves primarily to outbound equity buying encourages restrictive policies, whereas durable solutions require building offsetting inflow capacity.

③ FX stabilization must precede sustainable rate cuts for growth support

If sequencing reverses, the cycle can become: FX instability → constrained easing → weaker growth.

④ The AI value chain is an industrial policy lever and a high-leverage FX policy instrument

Positioning AI as a capital-attraction package can support USD inflows and improve the preconditions for FX stabilization.

< Summary >

The Bank of Korea held the policy rate at 2.50% for a fifth consecutive meeting, balancing FX instability against weakening growth and inflation near target.

FX intervention can dampen short-term volatility, but absent structural change, depreciation pressures tend to re-emerge.

Framing FX as a narrow flow issue risks over-reliance on temporary measures and limits the ability to prevent prolonged KRW weakness.

A structural package centers on pace management of monetary/fiscal settings, expanded inbound FDI, globally competitive regulation and business conditions, and an AI value-chain capital-attraction strategy, with intervention used primarily for volatility smoothing.

FX stabilization is a prerequisite for creating room for rate cuts and credible growth support.

[Related links…]

- KRW/USD Surge: Key Drivers and a Consolidated 2026 Response Framework

- Post-Hold Asset-Market Scenarios: Equities, Real Estate, and Bonds — Key Checkpoints

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [속보] 한국은행 ‘5연속’ 금리동결 : 환율 ‘재폭등’, 외환당국이 실패한 문제인식 [즉시분석]

● Bessent Bombshell, Korea-Won Warning, FX Whiplash, Minerals Alliance Play

Why the USD/KRW Reversed After Treasury Secretary Bessent Mentioned the Won: Not Mere Verbal Intervention, but a U.S. “Minerals–Alliances–FX” Package Signal

This report consolidates four points:1) Why the U.S. Treasury Secretary explicitly referenced the Korean won

2) Structural reasons markets reacted as if it were verbal intervention

3) Key checkpoints for renewed USD/KRW volatility (policy tools, flows, technical dynamics)

4) Core issue often missed: the FX narrative is increasingly linked to the strategic critical-minerals agenda

1) Event Summary: “USD/KRW Falls Sharply After the Open… Triggered by Interpretation of Bessent’s Remarks”

USD/KRW dropped rapidly at a specific point, prompting market interpretation that the move reflected U.S. verbal intervention. The decline resembled a policy-driven move rather than ordinary intraday volatility. A partial rebound later fueled debate over whether the move was temporary or a signal of a broader shift.

2) Key Line and Market Meaning: “The Won’s Weakness Is Excessive Versus Korea’s Fundamentals”

The phrase that drove the reaction was effectively:“Recent depreciation in the won is not consistent with Korea’s solid economic fundamentals.”

This was interpreted less as praise and more as signaling:“Current won weakness is difficult to justify → pricing may be distorted → the U.S. does not view these levels favorably.”

Given the role of expectations in FX, any indication of U.S. discomfort can destabilize short-term positioning. USD/KRW is also sensitive to rapid shifts in global risk flows, amplifying the impact of official rhetoric.

3) Why Korea Was Singled Out: FX as Surface, Critical-Minerals Alliance as Substance

The broader context of Bessent’s engagements emphasized critical minerals. The key interpretation is:

FX is not a stand-alone agenda item; it is increasingly bundled with supply-chain, minerals, and industrial-alliance negotiations as a pricing variable.

For the U.S., critical minerals are strategic inputs spanning semiconductors, batteries, and defense. As China-related risks rise, the U.S. is pushing to reconfigure “resource–refining–materials–components” chains within allied blocs. Korea is central to battery and semiconductor value chains, making the “fundamentals” reference relevant to alliance leverage rather than generic commentary.

4) Why Verbal Effects Are Powerful but Often Not Durable

Verbal intervention can create a large short-term shock by shifting expectations. Sustained impact typically requires:

(1) Concrete policy/action tools

Examples: liquidity measures, market-operation steps, repeated escalation in messaging

(2) A change in flows

FX levels generally reset only when persistent dollar buyers pause or reverse.

Tools such as currency swap lines are typically reserved for systemic stress episodes, limiting the probability of rapid deployment. Absent follow-through, volatility is likely to re-emerge.

5) Technical Dynamics: Why a Near-Term Downside Path Remains Plausible

The referenced AI-based market read is best treated as a sentiment proxy rather than a deterministic forecast. The prevailing setup can be framed as:

Sharp decline → rebound attempt → if capped at resistance, renewed downside risk remains.

In this structure, market participants may treat rebounds as potential selling opportunities, sustaining elevated volatility.

6) Forward Watchpoints: USD/KRW Is Increasingly Driven by U.S. Intent and Global Policy

The episode underscores that near-term USD/KRW direction is less likely to be explained by Korea-only fundamentals (e.g., exports or sector cycles) and more by U.S. policy signaling and global macro conditions.

6-1) U.S. Policy / Global Macro Checklist

U.S. rates: a “higher for longer” trajectory supports dollar strength.

Inflation: renewed upside risk can shift positioning toward the dollar.

Federal Reserve stance: incremental hawkish repricing can pressure the won.

6-2) Korea Market (Flows/Policy) Checklist

Foreign flows: equity and bond inflows/outflows transmit directly into USD/KRW.

Official smoothing operations: persistence versus one-off actions matters for volatility.

6-3) Industry/Geopolitics (Critical Minerals) Checklist

FX monitoring increasingly requires parallel tracking of “minerals/materials supply-chain” developments. As U.S. requirements for allied participation (supply-chain alignment, investment, regulatory conditions) expand, currency and financial conditions may be treated as part of an integrated package.

7) Most Material Point Often Underemphasized

The key weight of the remarks is less about near-term FX defense and more about embedding FX stability into a broader effort to consolidate an allied critical-minerals and industrial bloc.

If won weakness becomes disorderly, it can raise USD funding costs, disrupt investment plans, and increase import-price pressure, potentially affecting supply-chain execution. Treating the episode as a single-comment FX story risks missing subsequent spillovers from the minerals/industry/security package.

8) Investor Positioning: Prioritize Scenario Management Over Directional Certainty

The current regime is not well-suited to single-path positioning. Verbal intervention can drive abrupt declines, but durable trend changes generally require follow-through.

A practical approach is:

- Stress-test portfolio exposure to renewed USD strength (overseas assets, USD allocation, import costs).

- Separate beneficiaries and laggards under additional USD/KRW downside (exporters vs. domestic demand vs. commodity-linked sectors) and manage exposure by scenario.

< Summary >

- Bessent’s remarks were interpreted as verbal intervention via the framing that won weakness is excessive relative to Korea’s fundamentals.

- Verbal intervention has limited persistence; without policy follow-through or flow reversal, FX volatility is likely to return.

- The core context is not FX in isolation, but linkage to the U.S.-led critical-minerals supply-chain realignment and alliance package.

- Key drivers to monitor: U.S. rates/inflation/Fed stance, foreign flows, and critical-minerals/supply-chain developments.

[Related…]

- https://NextGenInsight.net?s=exchange%20rate

- https://NextGenInsight.net?s=semiconductor

*Source: [ Jun’s economy lab ]

– 베센트 재무장관이 환율 구두개입을 한 이유