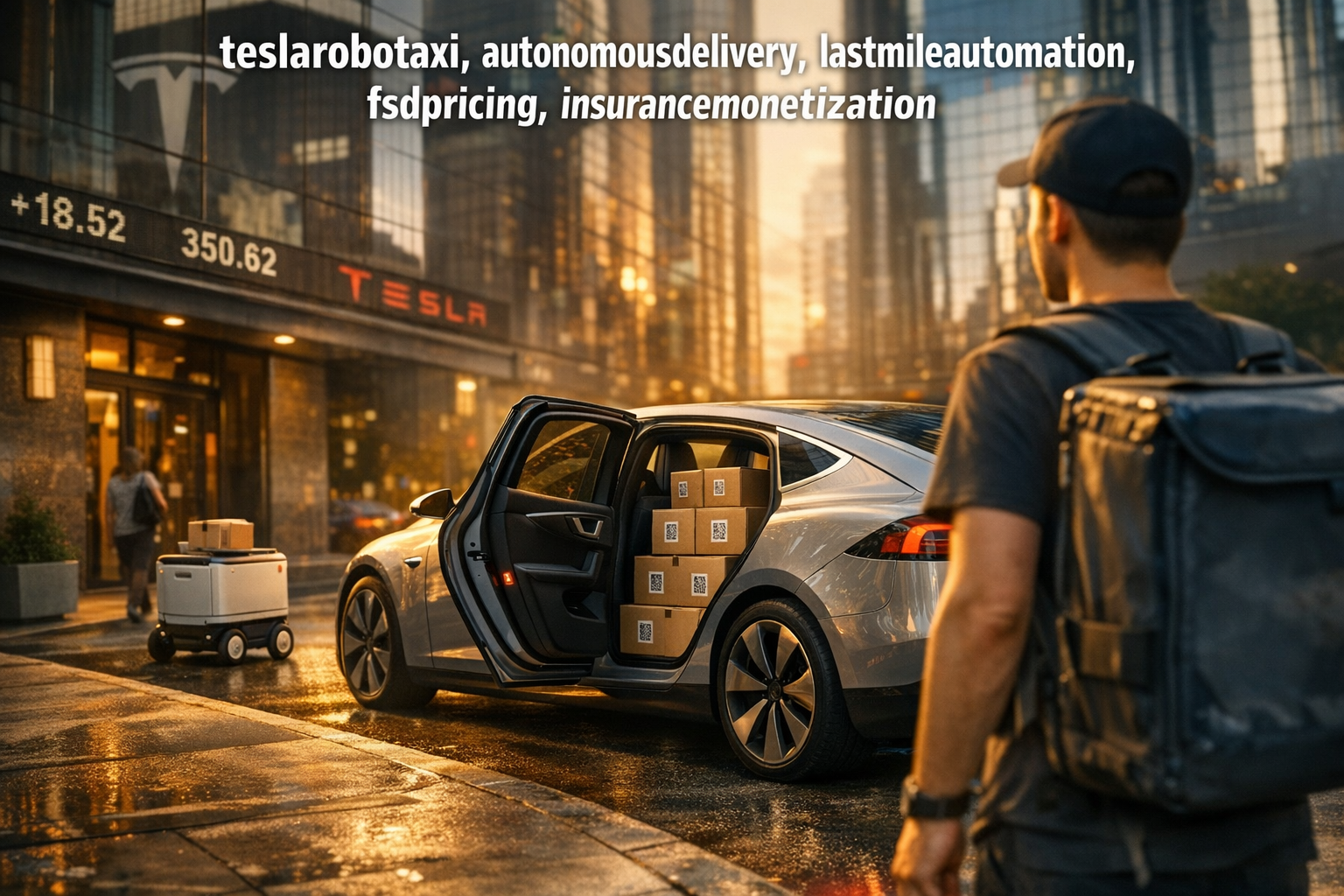

● 500-Dollar-Delivery-Tesla-Robotaxi-Logistics-Disruption

Will a KRW 500 Delivery Fee Era Actually Arrive? A Scenario in Which Tesla’s Robotaxi “Next Round” Disrupts a KRW 660 Trillion Logistics Market

This report focuses on:

1) Why Tesla’s unsupervised robotaxi is likely to expand from “Uber replacement” into logistics and delivery

2) The delivery market’s primary bottleneck (beyond platform fees): the demographic cliff, and why the cost structure is structurally vulnerable

3) The strategic implications of vertical integration: Semi (mid-mile) → Cybercab (last-mile vehicle) → Optimus (doorstep/last-meter)

4) Defensive strategies of incumbent platforms (Baemin, Coupang Eats, Uber Eats) and key investment risks/variables

5) A separate summary of the most decision-relevant point often omitted in mainstream coverage

1) News Brief: One-line takeaway

As Tesla formalizes unsupervised autonomy (robotaxi) as a service, the same network may extend from ride-hailing into last-mile delivery, creating potential for structural change in logistics costs beyond near-term impacts on ride-share valuations.

2) Why Robotaxi Commercialization Connects Directly to Logistics

2-1. Implication of “If you can carry people, carrying goods is easier”

Passenger transport imposes the strictest constraints: safety, comfort, and controlled acceleration/deceleration. If unsupervised autonomy begins to clear that threshold, applying the same driving stack to logistics/delivery generally reduces incremental complexity. The vehicle becomes a mobility platform; passengers, food, and parcels differ primarily by payload.

2-2. Product and app design already indicate delivery use cases

Despite being a two-seat Cybercab, design emphasis on expanded cargo capacity and a hatchback-style opening suggests delivery-first considerations. App UI examples such as “your coffee is arriving” imply that mixed passenger + logistics workflows are embedded in the product concept.

3) The Delivery Market Today: Cost Structure per Order

3-1. The economics of the “fee war”: consumer delivery fee vs. merchant-borne costs

Total intermediation and fulfillment costs per order can approach KRW 6,000 on average. Beyond consumer-visible delivery fees (e.g., KRW 3,000), merchants absorb platform commissions, delivery agency fees, payment processing fees, and VAT, creating a structurally low-satisfaction equilibrium and a direct link to regulatory and “shared growth” policy debates.

3-2. Larger structural risk: rider supply contraction from demographic decline

Independent of fee levels, human-labor-dependent last-mile models are exposed to demographic trends. As younger labor supply shrinks, rider availability declines and labor costs rise structurally. This is a long-duration trend rather than a cyclical fluctuation, implying persistent margin pressure. Last-mile automation may function less as optional efficiency and more as a supply continuity mechanism.

4) Tesla’s Cost Logic: Why “KRW 5,000 vs. KRW 500” Could Be a Regime Shift

4-1. Unit economics as the decisive factor

Using external estimates (e.g., ARK), Cybercab operating cost is modeled at ~USD 0.25 per mile (approximately KRW 300). If Optimus handles the last-meter handoff, per-drop costs could fall further. Human-based delivery faces a hard floor driven by minimum wages, insurance, and vehicle operating costs; autonomous/robotic delivery is dominated by electricity, depreciation, and maintenance, enabling stronger scale effects.

4-2. Price-setting power can rebase the market

If a KRW 500 delivery fee remains economically viable, the outcome is not incremental undercutting but a reset of reference pricing. In that scenario, incumbent defenses via fee cuts and promotions may be insufficient.

5) The Strategic Endgame: A Fully Unmanned Logistics Chain (Vertical Integration)

5-1. Port → hub → urban delivery → doorstep automation

Proposed chain:

1) Tesla Semi transports containers from ports

2) Cybercab performs last-mile delivery from hubs to end locations

3) Optimus completes last-meter tasks (stairs, doorways, elevators)

If integrated, this stack materially reduces human dependence in the most expensive segments: last-mile and last-meter.

5-2. Macro relevance: logistics costs as embedded inflation

Logistics costs are embedded across most goods and services. Lower last-mile costs can alter retail margin structures and influence consumer-facing prices, implying potential long-run disinflationary pressure from autonomous logistics. The topic spans corporate earnings and macro variables (prices and labor markets).

6) Market Size: KRW 660 Trillion (Why it matters, and where it can mislead)

6-1. Requirements for “10% share = KRW 66 trillion” to be credible

With global food delivery + last-mile estimated near USD 500 billion (~KRW 660 trillion), a 10% share implies ~KRW 66 trillion in revenue. This requires multiple conditions: jurisdiction-specific approvals for unmanned operation, workable insurance/liability frameworks, consumer adoption, and aligned CAPEX and maintenance systems. Deployment speed is likely to vary materially by region.

6-2. Structural advantage vs. platforms: reducing labor share of cost

Incumbent platforms retain significant labor-linked costs even after taking commissions. If unmanned operations scale, labor share could decline sharply and operating margins could structurally expand. The investment relevance is not only revenue growth but margin model redefinition.

7) FSD Pricing and Subscription Signals: Autonomy as SaaS

Signals suggest a shift from lifetime licenses toward subscription monetization. This is consistent with positioning autonomy as recurring software revenue, potentially improving cash flow stability and influencing valuation frameworks applied to growth equities.

8) Five Under-discussed Variables That Determine Outcomes

8-1. Regulation is constrained less by “permission” than by liability allocation

In unmanned incidents, the binding issue is liability assignment among manufacturer, operator, software provider, vehicle owner, and insurers. Even with permission to operate, an expensive liability structure can undermine unit economics.

8-2. The key competitor is not only Uber Eats but convenience retail and quick commerce

Beyond restaurant delivery, competition expands to near-inventory models: dark stores, convenience-store logistics, and large retailers’ in-house delivery networks.

8-3. Operations (Ops) can be harder than driving

Scaling requires robust dispatching, charging, cleaning, maintenance, incident response, and customer support. High autonomy performance does not compensate for weak operational execution.

8-4. A KRW 500 fee is a market reset mechanism

Lower pricing can increase order volume and concentrate traffic. If a data flywheel emerges (more driving data → model improvement → higher safety/efficiency → more orders), competitive gaps can widen.

8-5. Employment displacement can become political risk

Job impacts on drivers and riders can trigger social safety net debates and slow regulatory timelines. Outcomes depend on policy and public sentiment, not solely technology.

9) Korea-Specific Checkpoints: Implications for Baemin and Coupang Eats

Korea’s density and mature delivery culture support rapid experimentation, while pedestrian complexity, narrow streets, and parking constraints increase operational difficulty. A likely rollout path is: limited-zone deployment (new towns/campuses/business districts) → expansion to nights/off-peak → integration with logistics hubs. Over time, this can marginally influence services inflation dynamics monitored by the central bank.

10) Conclusion: Robotaxi is a Logistics Cost Reset, Not Only a Taxi Industry Shift

The core implication extends beyond equity-market headlines. When autonomy scales from passenger mobility into last-mile logistics, it intersects with platform-fee disputes, structural labor cost inflation, demographic contraction, and services inflation. The theme links to supply-chain reconfiguration, inflation and rates sensitivity, and growth-equity valuation.

< Summary >

Tesla’s unsupervised robotaxi is positioned to expand from ride-hailing into delivery and logistics.

The delivery market’s structural bottleneck is demographic-driven labor scarcity and rising labor costs, not only platform fees.

If the Semi → Cybercab → Optimus unmanned chain matures, last-mile costs could fall sharply and reset market pricing.

Regulation, liability, operational capability, and political risk are key determinants of speed and feasibility.

This is a macro-relevant technology shift intersecting inflation, employment, and strategic control of logistics infrastructure.

[Related Articles…]

- How Autonomous Driving Regulatory Shifts Affect Global Equity Markets

- Logistics Automation and Robotics: 2026 Investment Checklist

*Source: [ 오늘의 테슬라 뉴스 ]

– “배달비 500원 시대” 테슬라가 660조 물류 시장을 삼키면 벌어지는 일 ?

● Tesla Robotaxi Boom – Austin Fleet Surges, Costs Crush Rivals, FSD Price Spike Payday

Why Tesla Robotaxi’s “KRW 4,500 Trillion Market” Is Structurally Disruptive: Austin Deployment Velocity, Unit-Cost Advantages, and the FSD Pricing Rationale

This report focuses on three items:

1) The pace at which Tesla robotaxis in Austin appear to be moving from testing into early operational deployment.

2) Why ARK Invest’s USD 34 trillion market thesis is rooted in cost structure rather than narrative.

3) Why potential FSD subscription price increases should be evaluated through an insurance + monetization framework, not as a standalone consumer cost increase.

1) Field Update: Austin Robotaxi Fleet Growth Appears to Be Accelerating

Observed signals

- The robotaxi fleet count in Austin has increased rapidly since the 21st.

- Tracking charts suggest an expansion rate of approximately ~10 vehicles per day.

- New CyberCab additions have been observed at roughly ~1 vehicle per day.

- Footage captured multiple CyberCabs (approximately 6–8) traveling from Giga Texas toward Austin.

Why it matters

- Autonomous ride-hailing deployments typically scale slowly in pilot geographies due to regulatory, safety, and operational constraints.

- A daily increase pattern implies a potential transition from a technology demonstration phase toward an operational scaling phase.

2) Extreme-Environment Validation: Why Alaska Testing Matters

Key disclosure

- Tesla’s official robotaxi account posted content referencing CyberCab testing in extreme cold conditions in Alaska.

Operational implication

- Autonomous driving performance must sustain reliability across seasons, severe weather, camera contamination, and sensor uncertainty.

- Demonstrating extreme-condition readiness supports an “extreme reliability” positioning.

Economic relevance

- Higher reliability reduces downtime.

- Reduced downtime increases utilization per vehicle, directly affecting revenue per asset and margin structure.

- This is a prerequisite for robotaxi services to function as cash-flow businesses rather than demonstrations.

3) Hardware Detail: Camera Cleaning Nozzles as an Enabler of Unsupervised Operations

Observed hardware changes

- A robotaxi-configured Model Y appears to include a cleaning nozzle for side cameras.

- CyberCab is also believed to include cleaning nozzles on all cameras.

Why it is critical for unsupervised operations

- A major failure mode in real-world autonomy is camera occlusion/contamination (rain, snow, dust, insects, de-icing chemicals).

- In unsupervised fleets, human intervention is both a direct operating cost and a scalability constraint.

Conclusion

- Camera cleaning hardware is a cost-structure feature designed to reduce field-support dispatches and manual interventions.

4) Narrative Shift Signal: Traditionally Critical Media Turning More Positive on FSD

Reported development

- A previously critical outlet published a notably favorable assessment of FSD capability.

Interpretation

- The material point is narrative transition, not a single article.

- Regulatory posture and consumer acceptance are sensitive to public framing and perceived responsibility allocation.

- A shift in tone may reduce future adoption and regulatory friction costs.

5) FSD Subscription Price Increases: From “Higher Cost” to “Value Capture via Insurance + Monetization”

Key point

- In the context of Autopilot-related discussion, Elon Musk indicated supervised FSD subscription pricing could increase.

- Higher capability may justify higher monthly pricing; unsupervised capability could create a step-change in pricing.

Investment-relevant reframing

- FSD pricing may shift from feature pricing to allocation of economic value across:

1) accident risk reduction and potential insurance premium compression,

2) time savings and reduced driving burden,

3) cash-flow opportunities via robotaxi network participation.

Illustrative logic

- Even at USD 300/month for unsupervised FSD, adoption could increase if robotaxi participation generates approximately USD 1,000/month in net income to the owner/operator.

Investor takeaway

- FSD can evolve from subscription revenue to a platform take-rate model once robotaxi monetization scales.

6) ARK Invest Thesis: Unit Economics, Not Headline TAM, Drives the Core Argument

1) Market share dynamics (San Francisco)

- Human-driven Uber/Lyft share declining.

- Waymo robotaxi share rising.

Implication

- The debate is shifting from feasibility to deployment timing by geography.

2) Data advantage

- Tesla is claimed to have cumulative autonomy-related driving data exceeding peers by 100x+.

Economic mechanism

- Data scale translates into lower intervention requirements to reach comparable safety, reducing operating costs and improving margins.

3) Cost comparison: operating cost as the decisive lever

- ARK estimates Model Y-based robotaxi operating cost per mile is ~35% lower than Waymo.

- If safety drivers/operational staff are removed, the gap could widen to 60%+.

- Under 2030 assumptions, Waymo costs may remain ~2x higher than CyberCab.

Conclusion

- Robotaxi competition is structurally a unit economics contest.

- Sustained cost advantage enables lower pricing while preserving profitability, pressuring higher-cost competitors.

7) Price Compression: USD 2.8/mile to USD 0.25/mile and Demand Expansion

Referenced benchmarks

- US taxi: USD 2.8 per mile.

- Personal driving cost: approximately USD 0.8 per mile.

- China taxi: approximately USD 0.5 per mile.

- Robotaxi future scenario: USD 0.25 per mile.

Mechanism for market expansion

- Lower prices expand demand beyond existing taxi substitution by:

1) displacing portions of public transit,

2) increasing short-trip frequency,

3) reducing private vehicle ownership.

Macro linkage

- This dynamic can affect household spending composition and service inflation, with potential implications for interest-rate sensitivity and broader economic outlook.

8) The Headline Figure: USD 34 Trillion Robotaxi Market

Claim

- ARK Invest sizes robotaxi as a USD 34 trillion, enterprise-value-scale market.

Interpretation

- The core is labor displacement (human driving) and the reallocation of transportation spend.

- Value capture may accrue more to network operators than to vehicle sellers.

Tesla’s cited structural advantages

- Data scale.

- Potential to reduce or eliminate operational staffing requirements (safety drivers, remote intervention intensity).

- Manufacturing scale to produce vehicles rapidly via gigafactory-driven capacity expansion.

9) “USD 100 Trillion Market Cap” Commentary: The Key Variable Is Speed

Referenced statement

- Musk suggested the largest company could reach USD 100 trillion market cap; the author speculated SpaceX as a candidate.

Investment framing

- The central point is not the absolute number, but the increasing velocity of value creation enabled by AI and autonomy.

- Recent expansion in the upper bound of mega-cap valuations supports this framing.

Market context

- Equity-market outlook cannot be modeled solely through cyclical frameworks; structural technology-driven growth may dominate in periods of rapid adoption.

10) Five Under-Discussed Points in Mainstream Coverage

1) The primary competitive edge is not autonomy performance alone, but the cost of on-the-ground interventions.

- Remote assistance, dispatch, and safety staffing function as hidden labor costs.

- Hardware such as camera cleaning nozzles signals efforts to structurally eliminate these costs.

2) FSD pricing increases may indicate the start of insurance-linked bundling and monetization.

- Decision-making shifts from monthly cost to ROI: insurance savings + monetization potential.

3) Unit-economics lock-in matters more than the USD 34 trillion headline figure.

- Per-mile cost gaps (35%–60%; potentially ~2x long-term) imply the lower-cost operator can price aggressively while sustaining profit.

4) Austin deployment velocity is a signal of operational maturity.

- Daily fleet increases suggest the presence of functioning loops for dispatch, charging, cleaning, maintenance, and customer support.

5) This trend links directly to semiconductors and AI infrastructure.

- Larger robotaxi fleets increase training and inference demand.

- AI chip demand, data centers, and power infrastructure may rise as second-order effects, impacting global supply chains and industrial structure.

11) Monitoring Checklist (Execution and Risk Indicators)

- Expansion of the Austin unsupervised operating domain.

- Post-safety-driver incident response protocols and transparency.

- Actual FSD subscription policy changes (pricing, regional differentiation, bundling, insurance integration).

- CyberCab mass-production timing and unit-cost signals.

- Competitors’ ability to reduce dependence on remote intervention (failure to do so implies persistent cost disadvantage).

< Summary >

Robotaxi fleet counts in Austin appear to be increasing on a daily cadence, consistent with movement from testing toward early operational deployment.

Extreme-cold testing and camera cleaning hardware align with a strategy to reduce field intervention costs, a prerequisite for scalable unsupervised operations.

ARK Invest’s USD 34 trillion thesis is primarily grounded in per-mile operating cost advantages, not headline market sizing.

Potential FSD price increases should be evaluated through an ROI lens incorporating insurance savings and robotaxi monetization pathways.

These dynamics connect to macro variables (inflation, rates, consumption patterns) and to AI infrastructure demand, including semiconductors and data centers.

[Related Posts…]

-

Tesla Robotaxi Era: Five Signals Korean Investors Should Track First

https://NextGenInsight.net?s=Tesla -

Autonomous Driving Industry Reset: Waymo vs. Tesla, the Decisive Battle Is Cost

https://NextGenInsight.net?s=Autonomous%20Driving

*Source: [ 허니잼의 테슬라와 일론 ]

– [테슬라] 4.5경 원 시장 열렸다! 아크 인베스트 보고서가 폭로한 테슬라 로보택시의 압도적 수익 구조 / 일론의 시총 ‘100조 달러’ 예상

● Seoul-Bubble Freeze, Provinces-Rent Surge Rebound, Last-Buy Window 2027

Seoul: “Overvalued + Transaction Freeze”; Regional Markets: “Undervalued + Supply/Demand Rebound” — Why a “Final Below-the-Knee Window” Through 1H 2027 Can Be Argued Using Data

This report covers:

1) Why policy changes after the 10/15 measures produced a “transaction cliff,” not a “price cliff” (market energy perspective)

2) Why high-end Seoul apartments held up (or formed a bubble): preferential loans + eased gifting rules + wealthy capital inflows

3) The key leading signal for regional markets: jeonse rental supply/demand (rent-driven transmission to sales prices)

4) Why Ulsan and Busan rebounded first, explained via “demand/supply indicators + forward supply”

5) The rationale for viewing 1H 2027 as a “final buying window” (30% construction-cost increase creating downside rigidity)

6) Why PF and completed-but-unsold inventory (“bad” unsold units) may be riskier than headlines imply

1) One-line market summary

Seoul: Tighter regulation leaves only selective demand and liquidity; transactions freeze while prices remain sticky.

Regional markets: After prolonged correction, prices are depressed; improving jeonse rental supply/demand is emerging as an early-stage recovery signal pushing sales.

2) Why transactions collapsed before prices after the 10/15 measures

Observed pattern

- Pre-measures: last-minute demand (including maximum-leverage buying) surged.

- Post-measures: daily reported transactions fell sharply, often below 100, creating a transaction “ice age.”

Data interpretation (sentiment / market energy)

- Similar to equities: peak volume often marks the end of ownership turnover and a decline in market energy.

- In real estate, “buyers have already bought” phases frequently lead to shrinking volume before meaningful price declines.

Policy transmission (demand constraint)

- Layered regulation (adjustment zones, overheated zones, land transaction permits) materially reduces borrowing capacity, especially for higher-priced assets.

- Occupancy requirements reduce both investor demand and upgrade demand, limiting listings and suppressing transaction flow.

3) Evidence that Seoul is in an “overvalued” zone: HAI, PIR, and rental yield

1) Housing Affordability Index (HAI)

- Exceeds the 2021 peak level, implying historically high purchase burden.

2) Price-to-Income Ratio (PIR)

- Near prior peak levels, indicating price levels not supported by income growth.

3) Seoul apartment monthly-rent yield vs deposit rate

- Seoul apartment rent yield: ~1.7% vs bank interest: ~2.6%

- When rental cash flow underperforms deposits, prices are more dependent on “asset preservation” motives than income generation.

Core implication

- Both end-user and investor affordability is constrained; further upside likely requires incremental support from broader capital markets (e.g., sustained strength in U.S. equities and crypto), rather than domestic fundamentals alone.

4) Why high-end Seoul held up (or inflated): policy + capital markets + intergenerational funding

1) Two-year accumulation of preferential lending (large-scale liquidity)

- Policy lending in 2023–2024 supported the market floor and reinforced leverage expectations, including the high-end segment.

2) Expanded gift-tax exemptions tied to marriage/childbirth

- Higher tax-free gifting limits increased purchasing power when combined with policy finance, shifting demand from pure leverage to family capital + policy credit.

3) “Young wealthy” capital inflows into Seoul as an asset store

- Gains from U.S. equities, crypto, and startups have rotated into Seoul, particularly high-end assets.

- This cohort is less sensitive to conventional credit tightening.

4) Tight supply + occupancy requirements driving “listing lock-in”

- If upgrading is constrained, fewer owners sell, increasing price rigidity.

5) The leading regional rebound signal is rentals, not sales

Mechanism

- Improving jeonse supply/demand → jeonse prices rise → sales prices are pulled higher.

Indicator interpretation

- Jeonse supply/demand above 100 indicates demand dominance.

- Levels around 140–150 can be interpreted as demand exceeding supply by 40–50%.

Why rentals transmit to sales

- Rising jeonse costs push households toward purchase decisions.

- A narrowing gap between jeonse and sales reduces the effective barrier to buying.

- Rentals function as a faster leading indicator in regional markets.

6) Why Ulsan and Busan moved first (per indicator logic)

Ulsan

- Jeonse supply/demand is among the highest nationwide.

- Limited forward supply combined with strong rental demand increases the probability of continued jeonse inflation, which can stimulate sales.

- Sales market indicators show strengthening buyer dominance and weakening seller dominance.

Busan

- Jeonse supply/demand rose above 150, with jeonse prices reacting first.

- Both sales and rental transactions resumed simultaneously after a prolonged lull, consistent with an early ignition phase.

Summary

- Regional rebounds are being captured first in a sequence of “rental tightness → transaction recovery,” rather than via sentiment or headline-driven catalysts.

7) Why the “final buying window through 1H 2027” is argued: downside rigidity from construction costs

Construction costs increased by 30%+ over the past five years

- Higher replacement costs raise the effective price floor, limiting downside even under weak demand.

Regional prices are already well below the 2021 peak

- With a higher cost base and already-depressed prices, the risk/reward profile can improve in select areas.

Implication of the “below-the-knee” framing

- When sentiment is negative, pricing and terms can become more favorable for buyers; historically, such conditions can coincide with data-driven opportunity zones.

8) Regional markets will not rise uniformly: risk checklist

1) Avoid maximum-leverage buying

- If rates rise, leveraged buyers absorb losses first.

2) Risk of renewed rate increases + reactivation of PF stress

- Higher long-term yields and lending rates can re-tighten financing conditions for developers and contractors.

3) Rising completed-but-unsold inventory (“bad” unsold units)

- Completed units that do not sell indicate blocked cash recovery.

- Accumulation can spill over into local growth, employment, and financial-sector asset quality.

4) Refinancing and maturity-wall pressure on households

- Loans originated around five years ago may reset or mature, increasing payment burdens and potentially triggering distressed sales or auctions.

9) Key points often underemphasized in mainstream coverage

Point A: Seoul regulation tends to freeze market mobility before it drives price declines

- The result can be stepwise, segmented repricing rather than rapid drawdowns.

Point B: The regional trigger is “rental tightness + forward supply,” not local news flow

- Jeonse indicators and the move-in pipeline lead sentiment-based narratives.

Point C: The 30% construction-cost increase is structural, not psychological

- It changes the cost-based floor and reinforces downside rigidity.

Point D: The core PF risk is not PF volume but cash-flow blockage from completed-but-unsold units

- Even if PF exposure appears to decline, unsold completed inventory can materially weaken builders and lenders.

Point E: 2026–2027 housing outcomes cannot be assessed using domestic policy alone

- Domestic housing is increasingly linked to global liquidity and risk-asset cycles (U.S. equities and crypto), making cross-asset conditions relevant.

10) Six indicators to monitor

1) Seoul vs regional transaction volume (daily reported counts): often leads prices

2) Jeonse supply/demand index: key regional leading indicator

3) Move-in volume (forward supply): central to the rental-to-sales transmission

4) HAI and PIR: valuation and affordability filters

5) Rent yield vs deposit rate: floor check for investment attractiveness

6) Completed-but-unsold inventory: primary regional risk alarm

< Summary >

Seoul shows overvaluation signals (HAI, PIR), low rental yields, and tighter regulation, reinforcing a structure where transactions freeze before prices adjust materially. Regional markets show early recovery signals driven by improving jeonse supply/demand; in select areas such as Ulsan and Busan, a “rent → sales” sequence is visible through transactions and supply/demand indicators. A 30%+ rise in construction costs is a structural driver of downside rigidity, supporting the argument that the period through 1H 2027 may represent a late-stage accumulation window in select undervalued regions. Key risks include renewed rate increases, PF-related stress, completed-but-unsold inventory, and refinancing pressure; leverage discipline and data-based regional selection remain critical.

[Related Links…]

-

Real estate market: latest summary of Seoul vs regional trends and investment checkpoints

https://NextGenInsight.net?s=real-estate -

Rate outlook and linkages across asset markets (equities and real estate)

https://NextGenInsight.net?s=interest-rates

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [풀버전] 서울은 고평가, 지방은 저평가. 27년 전까지 마지막 매수 기회가 온다 | 경읽남과 토론합시다 | 김기원 대표