● Tesla-Optimus Shock, Robot Ban, Musk Power Grab

Tesla Optimus Gen 3 Spotted in the Wild; Proposed US Robotics Restrictions Emerge: Why Elon Musk’s “Robot Dominance” Scenario Is Becoming Plausible

This development extends beyond a standard product update. It combines (i) early physical indicators of a Gen 3 Optimus unit, (ii) the likely rationale for adopting a fabric-like exterior, (iii) the strategic relevance of a proposed US “robotics equivalent of a TikTok ban,” (iv) the potential for Tesla to be re-rated as a strategic technology platform rather than an EV manufacturer, and (v) the impact of rates, inflation, and labor data on Tesla and broader AI risk sentiment.

Key differentiators often underweighted in mainstream coverage include data sovereignty, the true barriers to entry in physical AI, and the structural linkages across Tesla, SpaceX, and xAI, which help explain why markets increasingly view Optimus as prospective infrastructure rather than a standalone robot product.

1. Key Developments (At a Glance)

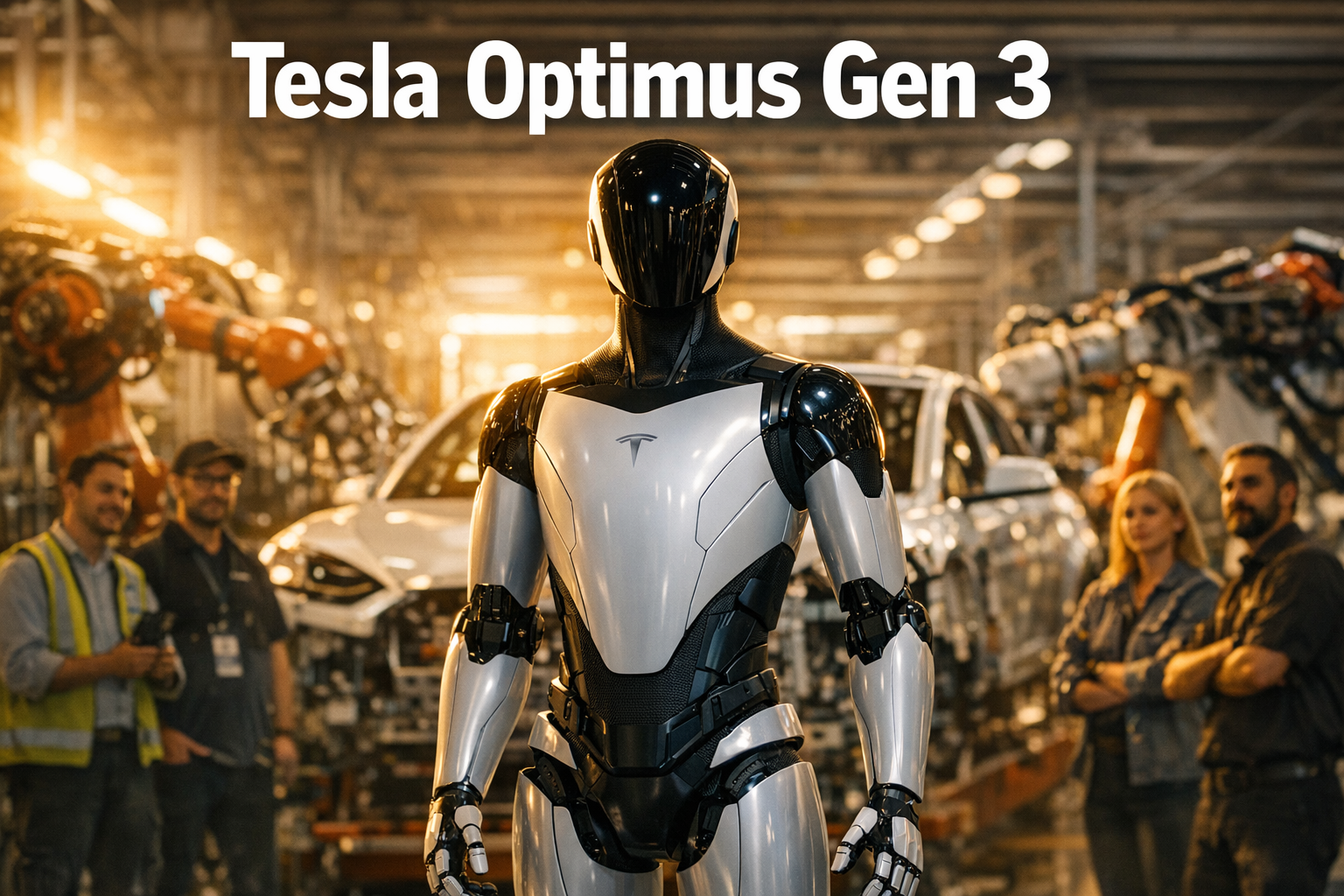

- A team photo from Tesla’s Optimus organization appears to show a next-generation humanoid consistent with a more productized, manufacturing-ready design language.

- US policymakers introduced a bill intended to restrict federal procurement and operation of robots produced in “adversary” countries.

- Markets frame this as a “robotics version of a TikTok ban,” implying potential share gains for US-aligned incumbents in domestic robotics deployments.

- Concurrent macro catalysts (Fed policy signals, energy prices, and labor releases) may affect global risk assets and technology-sector positioning.

2. Gen 3 Optimus Physical Sighting: What Appears to Have Changed

2-1. The Core Signal from a Single Photo

- The image was shared by Konstantinos Laskaris, Tesla’s electric motor technology director and the lead for Optimus actuator design.

- The central robot appears less like an exposed prototype rig and more like a consumer/industrial product candidate.

- The implication is a transition from R&D demonstrator to manufacturable SKU trajectory.

2-2. Why a “Suit” Instead of Exposed Metal Panels

The fabric or mesh-like exterior is likely functional rather than aesthetic:

1) Human-robot interaction (HRI)

- A softer, less mechanical appearance may reduce user resistance in homes and offices, supporting trust and adoption.

2) Manufacturing and cost

- Replacing complex exterior paneling with flexible materials can simplify assembly and improve throughput.

- Given Tesla’s stated target price point near ~$20,000, exterior simplification is consistent with cost-down and scale objectives.

2-3. Why Humanoid Form Factor Matters

- Most industrial and household infrastructure is built to human dimensions (stairs, door handles, tools, shelving, kitchen layouts, and aisle geometry).

- A humanoid platform can reduce retrofitting costs and accelerate deployment by leveraging existing environments.

3. The Primary Moat Is “Physical AI,” Not Industrial Design

3-1. The Core Requirement: Stability and Robustness, Not Aesthetics

- Several Chinese vendors have accelerated humanoid announcements, but visual similarity does not imply parity.

- The hard problem is real-time balance, perception, and control under uncertainty (surface variation, friction, center-of-mass shifts, obstacle avoidance, collision handling, and rapid response).

3-2. Why Tesla’s 8.9B+ Miles of Real-World Data Matters

- Tesla’s advantage is not limited to robotics-specific datasets; it has accumulated extensive real-world perception and navigation data via its vehicle fleet.

- While cars and humanoids differ materially, both require reliable real-world scene understanding and decision-making.

- Tesla is positioned to extend a unified stack (vision-first learning, onboard compute, custom AI chips, update pipeline) from vehicles to humanoids.

3-3. What the Chest/Internal Packaging May Indicate

- Commentary suggests the torso cavity resembles vehicle-grade computing packaging.

- If accurate, Tesla may be standardizing compute modules across vehicles and robots, enabling:1) Faster development cycles2) Lower unit costs via shared components3) Higher software update efficiency and fleet management consistency

This aligns with a platform expansion strategy rather than a standalone product approach.

4. Proposed US “Robot TikTok Ban”: Why It Could Benefit Tesla

4-1. Bill Objective (High Level)

- The proposal would limit US federal agencies from purchasing or operating robots manufactured in “adversary” countries.

- The stated rationale is national security, with emphasis on data exfiltration risk.

4-2. Why Robots Are More Sensitive Than Smartphones

- Robots combine cameras, microphones, depth/ranging sensors, and autonomous mobility within private and operational spaces.

- Potentially collectible data includes room layouts, access patterns, behavioral routines, asset locations, and workplace configurations.

- As a result, robotics increasingly intersects with data sovereignty and security policy.

4-3. Regulation as an Industry Structure Catalyst

- If public-sector procurement shifts away from Chinese-origin robots, domestically aligned full-stack providers gain advantage.

- Tesla is a leading candidate given its US-aligned hardware/software integration and AI compute strategy.

- The robotics market may move toward a geopolitically shaped structure where supply chain alignment and compliance become competitive levers.

5. Why Tesla May Be Hard to Displace Even if China Scales Quickly

5-1. Cosmetic Imitation vs. Operational Performance

- Similar shells, materials, or colorways do not determine deployment readiness.

- Key metrics are stability, task repeatability, safety, and reliability under real-world variability.

5-2. The Market Signal from “Falls” in Public Demos

- High-visibility instability events highlight that humanoids cannot be assessed via staged clips alone.

- Without robust autonomy and control, adoption in factories, logistics, and households remains constrained.

- Tesla’s limited disclosure combined with confidence signals suggests emphasis on control software and real-environment neural networks as primary moats.

6. Tesla’s Potential Re-Rating as a Strategic Technology Platform

6-1. Optimus as a Shift in Corporate Identity

- Mass production of Optimus would integrate vehicles, AI silicon, autonomy, energy systems, robotics, and data platforms under one operating model.

- This reduces the relevance of EV unit sales as the sole valuation anchor.

6-2. Robots as a Productivity and Labor Market Asset

- Broad humanoid deployment could alter cost structures in manufacturing, logistics, services, care, and hazardous work.

- Over time, it may partially offset labor shortages and demographic aging pressures, supporting productivity-linked narratives.

7. Near-Term Macro Variables: Rates, Oil, and Labor Data

7-1. Policy Expectations as a Risk Factor

- Markets appear to be pricing a high probability of a Fed hold.

- Risk increases if messaging turns more hawkish than expected or if rate-cut expectations are pushed out.

- Growth equities, including Tesla, remain rate-sensitive.

7-2. Higher Oil as an Inflation Re-Acceleration Vector

- Rising energy costs can feed into transport and input costs, influencing inflation expectations.

- This can delay policy easing and pressure long-duration AI/growth valuations.

7-3. Labor Data and Pre-Holiday Volatility

- Claims and other employment indicators can move markets if they diverge materially from expectations.

- Ahead of market holidays, de-risking behavior can amplify volatility.

8. SpaceX, xAI, and Tesla: The Musk Ecosystem Linkage

8-1. Potential Effects of a SpaceX IPO Narrative

- IPO speculation could reshape retail flows and investor overlap across Musk-affiliated assets.

- Overlap may influence future strategic optionality, governance dynamics, or capital allocation perceptions.

8-2. The Emphasis on ~25% Voting Control

- Repeated focus on ~25% voting power appears tied to maintaining strategic continuity for long-horizon initiatives (AGI-adjacent work, autonomy, humanoids).

- This reduces vulnerability to short-term governance pressures that could constrain long-duration R&D programs.

8-3. Convergence Toward a Unified AI Infrastructure Stack

- Tesla: real-world data, autonomy, robotics deployment endpoints

- SpaceX: communications and space-based infrastructure

- xAI: model training and inference capabilities

If these elements become more interoperable, Optimus can be viewed as a physical endpoint for a broader AI infrastructure ecosystem.

9. Investor/Industry Takeaways (News-Style)

9-1. Industry

- Tesla appears to be shifting from EV manufacturer to AI/robotics platform company.

- US policy momentum could simultaneously constrain Chinese suppliers and catalyze domestic robotics adoption.

- Competitive advantage in humanoids is likely to concentrate around data, control software, supply chain resilience, and security compliance.

9-2. Investment

- Near-term: rates, oil, and labor data are key drivers of Tesla and broader tech risk appetite.

- Medium/long-term: Optimus commercialization cadence and US regulatory direction may influence valuation frameworks.

- Capital flows and governance developments involving SpaceX and xAI may become incremental variables for shareholder outcomes.

10. Underemphasized but Material Point

Optimus’ competitive positioning likely extends beyond the robot itself. Key elements include:

- Data sovereignty

- Real-world physical AI training capability

- Standardized compute architecture

- Potential policy tailwinds in the US

- Ecosystem linkages across Musk-affiliated platforms

Humanoid robotics is increasingly a composite sector spanning semiconductors, cloud/compute, national security frameworks, and AI software.

11. Key Watch Items and Timeline Catalysts

1) Official Gen 3 Optimus reveal and the quality of live demonstrations2) Legislative progress and scope expansion of US robotics restrictions3) Fed trajectory and inflation trend impact on growth-equity premia4) Tesla’s cost-down progress and credible mass-production roadmap disclosure5) Financial and structural linkages across Tesla, SpaceX, and xAI

12. Conclusion

The Gen 3 Optimus sighting is best interpreted as a signal of productization and scaling intent rather than a routine hardware update. If US regulatory and procurement trends increasingly prioritize security and domestic alignment, Tesla could benefit structurally. Market evaluation may shift from EV delivery metrics toward real-world data control, physical AI commercialization speed, and policy positioning.

< Summary >

- Gen 3 Optimus indicators suggest a manufacturable design direction and possible compute standardization.

- Proposed US “robot TikTok ban” dynamics could reduce Chinese participation in public-sector robotics and create policy advantages for Tesla.

- Tesla’s moat is likely centered on real-world data-driven physical AI and data sovereignty rather than exterior design.

- Rates, inflation, and labor prints may drive near-term volatility; Optimus commercialization and regulatory direction are larger medium/long-term variables.

- Tesla may be increasingly framed as a strategic technology platform spanning AI, robotics, security, and productivity.

[Related Posts…]

- https://NextGenInsight.net?s=Optimus

- https://NextGenInsight.net?s=Interest%20Rates

*Source: [ 오늘의 테슬라 뉴스 ]

– 테슬라 3세대 옵티머스 실물 포착! 미국 ‘로봇판 틱톡 금지법’ 발의… 일론 머스크 독점 시대 열리나?

● Red Sea Crisis, Oil Shock, Market Panic

Middle East Risk Not Priced In by Trump: Why Red Sea Closure Fears Are Increasing Volatility in US Equities and the Global Economy

This is not a routine geopolitical headline.

The market is currently focused on three variables:

First, the probability of US ground-force involvement is being interpreted not as rhetoric but as a tangible signal of mobilization.

Second, a scenario in which shipping is disrupted not only at the Strait of Hormuz but also in the Red Sea is being incorporated into pricing for the first time.

Third, the shock is transmitting simultaneously across crude oil, US Treasury yields, the Nasdaq drawdown, inflation expectations, and global supply chains.

This report moves beyond the simplified view of “war equals equities down” and outlines: why the setup resembles 2022; why US energy and LNG-linked equities are outperforming; why investors should prioritize oil and rates over mega-cap narratives; and how to frame risk controls and staged entry approaches. A key focus is that the primary threat from a Red Sea disruption may be logistics and consumer inflation rather than energy alone.

1. One-line summary: the first thing to watch

US equities are moving from a standard pullback to a phase that reflects both prolonged conflict risk and maritime logistics disruption.

The Nasdaq has declined more than 10% from its peak, consistent with a formal correction, and the S&P 500 is following a similar path.

Earnings and idiosyncratic stock factors are secondary; crude oil and the US 10-year Treasury yield are currently exerting the strongest influence on direction.

2. Situation update: why the conflict is shifting into a new phase

2-1. Why ground-force risk is re-tightening markets

Recent developments are increasingly interpreted as preparations that extend beyond airstrikes and deterrence, including potential ground-force options.

Reports and market chatter around Marine deployments and reserve-related official communications have weakened risk sentiment.

From a market perspective, this matters because air campaigns can end quickly, while ground involvement typically extends the time horizon.

Markets generally price prolonged uncertainty more negatively than the initial shock.

In 2022, the most damaging phase was not the initial drop but the extended cycle of failed rebounds and renewed declines. Current positioning reflects similar concerns.

2-2. Why Trump’s “pause” messaging is losing market impact

Markets appear less responsive to alternating escalation and delay signals than in prior cycles.

Repeated shifts in deadlines (e.g., 48 hours, 5 days, 10 days) increasingly read as prolongation rather than negotiation leverage.

Markets are prioritizing observable signals—troop movements, route risk, and oil pricing—over political messaging.

The regime is shifting from rhetoric-driven headlines to pricing of operational readiness and energy-flow disruption risk.

3. Core issue: why the Strait of Hormuz is no longer the only focus

3-1. Why the Red Sea is the most critical variable this week

Middle East risk is often framed around the Strait of Hormuz.

The differentiator in this episode is the rising probability of disruption in the Red Sea and the Bab el-Mandeb Strait.

Hormuz is primarily an energy chokepoint; the Red Sea is a key corridor for both energy and containerized trade.

One channel shocks oil and gas prices; the other transmits into freight rates, delivery delays, consumer prices, and corporate margins.

If both routes are impaired, markets begin to price a combined “energy inflation + logistics inflation” shock.

3-2. Why the risk increases if the Saudi bypass scenario weakens

A stabilizing assumption has been that even if Hormuz risk rises, Saudi Arabia could redirect volumes via pipelines and Red Sea export routes, partially offsetting supply shocks.

This expectation helped cap crude volatility.

If Red Sea security deteriorates, the bypass itself becomes less reliable.

Market perception shifts from “temporary disruption” to “no safe alternative route,” which can matter more than the initial price spike because it removes an expected stabilizer.

3-3. Why the Ever Given episode is being referenced again

The strategic importance of the Red Sea–Suez corridor is illustrated by the Ever Given blockage: a short disruption triggered global logistics dislocations and higher freight costs.

That episode was accidental; current risk is military.

Operational accidents are resolved; military risk is open-ended, prompting more conservative market pricing.

4. The transmission mechanism into US equities: why mega-cap tech is more exposed

4-1. Why the Nasdaq and growth equities are sensitive to higher oil

Higher crude and higher yields typically pressure growth equities first.

Growth valuations rely on discounting future cash flows; higher rates reduce present value more materially.

Energy-driven cost pressures can compress margins and weaken demand, accelerating de-rating in tech-heavy indices.

In this regime, macro variables dominate company-specific headlines.

4-2. Why semiconductors, platforms, and software weaken together

Recent pressure across mega-cap platforms and semiconductors reflects a broader decline in risk appetite.

In risk-on markets, idiosyncratic negatives are often absorbed; in risk-off markets, small negatives are amplified.

Current conditions resemble the latter.

5. Relative strength: why US energy and LNG remain bid

5-1. Why US energy is positioned as a beneficiary

Rising Middle East risk tends to increase relative demand for US energy producers.

US crude, natural gas, and LNG export capacity is perceived as an alternative supply base that does not rely on Middle East chokepoints.

If global demand holds while competing supply is exposed to disruption, pricing power shifts toward alternative suppliers.

This supports relative performance in integrated majors and LNG-export-linked equities.

5-2. Implications of higher Asian demand for US energy

Official references to increased US energy procurement by Asian economies should be interpreted as signals of accelerated diversification under energy-security constraints.

This aligns with structural shifts: supply-chain reconfiguration in energy, higher US LNG share, and changes in procurement strategy across Asia.

The theme may function as a short-term oil shock trade, but it also links to a broader shift toward US-centered energy leverage.

6. Investor checklist: what to monitor now

6-1. Two indicators that matter more than ten headlines

The primary checklist is:

First, whether crude oil stabilizes.

Second, whether the US 10-year yield rolls over.

Stabilization in both increases the probability of sustained relief in the Nasdaq, semiconductors, AI-linked equities, and smaller-cap growth.

If both continue rising, equity rebounds may occur but tend to lack durability.

6-2. Why energy is acting as portfolio defense

In regimes where war risk and inflation rise together, energy exposure can function as a hedge-like sleeve.

This does not imply energy equities are risk-free, but negative correlation versus tech can reduce overall portfolio volatility.

This pattern was also evident in 2022.

6-3. Staged buying is viable, with conditions

Staged entry can be appropriate in correction phases, but execution should be rule-based.

Rather than buying solely on perceived cheapness, entries should be conditioned on trend changes in oil and yields.

For long-horizon investors, staged exposure via broad US equity ETFs, high-quality mega-cap franchises, and core AI infrastructure names can be structured by drawdown thresholds.

This is a regime for managing cash levels and predefined entry bands rather than concentrated timing bets.

7. Macro implications: why this episode is more threatening to global growth

7-1. Inflation risk may re-accelerate

Higher oil and gas prices transmit beyond energy into transportation, manufacturing costs, food pricing, and services over time.

If Red Sea logistics disruptions persist, the result can be broad consumer inflation rather than a narrow commodity shock.

This can delay expectations for Fed easing.

The core market concern is not the conflict headline itself, but the potential for renewed inflation pressure and a longer period of restrictive financial conditions.

7-2. Potential spillover into food and fertilizer

Prolonged conflict and logistics disruptions can spill into food and fertilizer pricing.

In 2022, these categories became a major secondary inflation channel.

Food inflation tends to compress consumer sentiment more quickly and can impose simultaneous FX and inflation stress on emerging markets.

If grains, fertilizer, and shipping-linked assets move together, it should be read as a broader growth headwind rather than a standalone thematic rally.

8. The Trump variable: what markets are implicitly pricing

8-1. Markets are pricing resolution capacity, not initial toughness

The relevant variable is not the intensity of opening statements but the ability to shorten the timeline, stabilize oil, and reduce rate pressure.

A rapid de-escalation around April could limit the duration of the correction.

An extended pressure campaign without a negotiated path increases the probability of a 2022-style prolonged range-bound drawdown.

8-2. Why April is treated as a pivot window

Political timelines, legal authority constraints, and diplomatic calendars contribute to April being treated as a decision window.

If risk resolves within that window, expectations for the second half can recover.

If the window passes with escalating signals, markets may shift to a more defensive regime.

9. Key points (news format)

- Indicators of US ground-force mobilization and reserve-related issues are reinforcing expectations of a longer conflict horizon.

- Red Sea closure risk, in addition to Hormuz risk, is increasing concern over global supply-chain disruption.

- The Nasdaq has entered correction territory; mega-cap tech and growth equities are broadly weaker.

- US energy, LNG, and refining-linked equities are outperforming on alternative supply expectations.

- The two primary market checkpoints are crude oil and the US 10-year yield.

- Rapid de-escalation could enable a technical rebound; prolonged escalation raises the risk of an extended 2022-like adjustment.

10. The most important point often omitted: why Red Sea closure is more dangerous than “oil up”

Most coverage stops at “Middle East instability equals higher oil.”

The more material risk is that Red Sea disruption can transmit more strongly into logistics costs and consumer inflation.

Hormuz primarily affects crude and gas flows; the Red Sea affects containers, intermediate goods, consumer products, food, freight rates, and delivery times.

Accordingly, this is not only an energy-sector catalyst; it is a potential repricing of the global cost structure.

Sectors with high sensitivity to component lead times and logistics—AI infrastructure, semiconductors, EV supply chains, and industrials—can face not only multiple compression but also earnings pressure if disruptions persist.

The underlying issue is not the war headline; it is the risk of accelerated supply-chain reconfiguration.

11. Practical response framework for investors

First, avoid emotionally timing bottoms; confirm the direction of oil and yields.

Second, distinguish between tactical bounces and trend reversals; pace exposure accordingly.

Third, consider partial defensive sleeves such as energy, cash-equivalents, and ultra-short-duration Treasury ETFs.

Fourth, long-term investors can prepare staged entries in broad index ETFs and high-quality equities using drawdown-based rules.

Fifth, the AI theme is not structurally broken; it is currently constrained by macro risk. Use the correction to monitor drawdown magnitude in core AI and semiconductor exposures.

12. How to frame this from an AI trend perspective

A near-term decline in AI-linked equities does not, by itself, invalidate the structural growth thesis.

This phase is likely to increase differentiation within the AI complex.

Power, data centers, semiconductors, and cloud infrastructure require heavy capex and are directly exposed to rates and input-cost pressure.

Software-centric AI services are less capex-intensive but can face multiple compression if enterprise IT budgets tighten.

AI investing is shifting from “growth at any price” to a framework that integrates energy costs, supply-chain reliability, cost of capital, and monetization durability.

13. Conclusion

Markets are pricing a joint shock: potential conflict prolongation, supply-chain disruption, and renewed inflation pressure.

In the near term, crude oil and yield stability are more decision-relevant than company-specific narratives.

A short, decisive resolution could normalize conditions faster; a prolonged path increases the probability of a 2022-like grind.

The priority is risk management. Effective positioning requires separating headline fear from the concrete channels through which geopolitical risk transmits into macro conditions, US equities, and AI-linked exposures.

< Summary >

- Signals of US ground-force mobilization are increasing expectations of a longer conflict timeline.

- Red Sea closure risk, in addition to Hormuz risk, is expanding supply-chain disruption concerns.

- The Nasdaq and mega-cap tech are under pressure from higher oil and rate sensitivity.

- US energy and LNG-linked equities are outperforming on alternative supply expectations.

- The key indicators are crude oil and the US 10-year Treasury yield.

- The primary Red Sea risk is logistics and consumer inflation, not energy alone.

- The structural AI growth thesis remains intact, but near-term performance is constrained by macro risk.

[Related Articles…]

Nasdaq correction signals and conditions for a US equity rebound

AI infrastructure investment and the next opportunity in semiconductors

*Source: [ 소수몽키 ]

– 트럼프도 예상 못했다? 홍해 봉쇄 우려, 미 증시에 더 큰 혼란 줄까

● Middle East Shock, Oil Spike, Korea Hit

Escalation of the Middle East War: Is a Fourth Oil Shock Becoming Plausible? Core Scenarios That Could Simultaneously Disrupt Korea’s Economy, Semiconductors, and Inflation

The key market question is whether the Middle East conflict remains a contained geopolitical risk or develops into a potential fourth oil shock.This is not limited to higher crude prices; it can transmit to Korea via import prices, inflation, semiconductors, petrochemicals, construction, and consumption through cascading supply-chain effects.

This report organizes the issue in a news-style framework:why the Strait of Hormuz is the critical choke point;why an oil-price surge may represent a supply shock rather than a price-only event;why naphtha, LNG, and helium are strategic inputs for Korea’s industrial base;and why Korea may face amplified sensitivity versus peers.

It also highlights under-covered risks:a naphtha shock;the impact of helium shortages on semiconductor processes;and structural constraints whereby damaged energy facilities may require 2–3 years to normalize.

1. Why this is not just war-related news but a potential macro risk signal

As the conflict persists, markets typically focus on three concurrent risks:

- Crude oil price spikes

- LNG supply disruptions

- Maritime logistics bottlenecks and broader raw-material supply instability

The key risk is a shift from “higher prices but available supply” to “insufficient volumes regardless of price.”This is the defining mechanism of an oil-shock environment.

In industrial supply chains, physical constraints often matter more than spot-price moves.If essential inputs such as crude oil, LNG, naphtha, and helium become constrained, downstream manufacturing, exports, logistics, and consumer-goods production can be disrupted.

2. The Strait of Hormuz is the primary focal point

The Strait of Hormuz is a critical conduit for global energy flows.Any blockade, restriction, or sustained degradation in transit can destabilize the global energy supply chain.

A significant share of global crude oil and LNG shipments pass through this route, making the risk systemic rather than country-specific.

If vessel counts and carried volumes decline materially, markets may reprice risk as an actual supply reduction, raising the probability of not only a short-lived spike but also a prolonged high-price regime.

3. Why a fourth oil shock could be more disruptive than prior episodes

Relative to prior oil shocks, the modern economy is more deeply dependent on energy and petrochemical inputs.

Industrial structures are more complex than in the 1970s.Smartphones, data centers, semiconductors, electric vehicles, advanced manufacturing, e-commerce logistics, and packaging systems rely on energy and petrochemical feedstocks.

Accordingly, the primary risk is not only cost inflation but also operational disruption driven by supply unavailability.

Another structural factor is recovery time.If regional refining or production assets are damaged, supply does not normalize immediately upon de-escalation.From procurement and contracting to construction and commissioning, normalization can take 2–3 years or longer, turning the event from a short-term headline into a medium-term macro variable.

4. Why Korea is structurally more vulnerable

- Low energy self-sufficiency

- High dependence on Middle Eastern crude

- Large share of export-oriented manufacturing

- Exchange-rate pass-through that amplifies import-price inflation

Korea imports energy, converts it into manufactured exports, and is therefore exposed to simultaneous shocks in input costs and external demand.If oil prices rise while the currency weakens, import unit costs increase, production costs rise, and exports can soften alongside global growth deceleration.

This configuration increases stagflation pressure: inflation rises while growth slows.

5. Macro transmission: inflation up, growth down

- Higher crude prices → higher import prices

- Higher energy costs → higher corporate cost bases

- Higher living costs → weaker consumption

- Lower profitability → weaker investment

- Lower growth → deeper cyclical slowdown

This is a dual deterioration in inflation and growth.For central banks, easing becomes constrained if inflation re-accelerates, potentially increasing financial-market volatility.

6. Sector impact (1): Naphtha shock as an underappreciated core risk

Public discussion often centers on gasoline and heating bills; however, naphtha is the more critical industrial risk.

Naphtha is a key petrochemical feedstock.Cracking produces base inputs such as ethylene and propylene, which underpin plastics, packaging, synthetic fibers, synthetic rubber, consumer containers, and industrial materials.

- Plastic bags

- Pay-as-you-throw waste bags

- Food packaging materials

- Instant noodle packaging

- Bottled-water containers and other packaging

- Synthetic fibers for apparel

- Synthetic rubber for tires

- Plastic construction materials

If naphtha supply is disrupted, the impact extends beyond petrochemicals to retail distribution, food, consumer staples, construction, and autos.This is not only price pressure; packaging and materials shortages can interrupt production and shipment.

7. If a naphtha shock materializes: likely sequence of effects

An early signal would be reduced operating rates at petrochemical complexes.This can weaken corporate earnings and transmit to employment and local economies in industrial hubs.

Next is consumer inflation and distribution disruption.Food and household products depend heavily on petrochemical-based packaging; shortages can prevent shipment even when finished goods exist.

Construction is also exposed.Costs and lead times for windows, insulation, coatings, piping, and interior materials can rise, increasing pressure on project costs and housing prices and weighing on construction activity.

8. Sector impact (2): LNG shock affecting power, city gas, and industrial fuel

The risk is not limited to crude oil.LNG disruptions are material, particularly given the role of major exporters such as Qatar.Operational disruptions or export curbs are therefore highly market-sensitive.

If exporters prioritize domestic supply, delivery can tighten even under long-term contracts.For Korea, this increases pressure on power and city-gas costs.

- Higher generation costs

- Increased pressure to raise electricity tariffs

- Higher household city-gas burdens

- Margin compression for energy-intensive industries

Steel, chemicals, and manufacturing broadly face immediate margin impacts from higher energy input costs, with potential second-order effects on investment and employment.

9. Sector impact (3): Semiconductor risk driven by helium supply constraints

A key operational risk is helium.While market narratives often emphasize memory pricing or AI-driven demand, process-level constraints from specialty gases can become binding.

- Cooling of wafers and equipment

- Leak detection

- Purge processes for impurity removal

Helium shortages can reduce throughput efficiency and weaken quality control, potentially causing production disruptions.If Korea is materially dependent on Qatari helium, the Middle East risk can translate directly into bottlenecks for AI infrastructure, memory, and advanced manufacturing.

10. Implications for Korea’s export complex

Semiconductors are not a single export item but a core pillar of the export and industrial ecosystem.Electronics, displays, smartphones, PCs, autos and parts, appliances, batteries, and machinery are linked to semiconductor availability.

- Direct decline in semiconductor exports

- Production constraints across related industries

- Delays in capital expenditure

- Compounding risk if global IT demand also weakens

Heightened geopolitical risk can also delay global data-center and IT hardware investment, creating a scenario where supply constraints and demand hesitation occur simultaneously.

11. Expected market transmission to Korean equities and financial conditions

- Higher crude prices

- Renewed inflation concerns

- Reduced expectations for policy-rate cuts

- Currency depreciation pressure

- Higher equity-market volatility

Korean equities have high exposure to semiconductors, autos, chemicals, and transportation, which are sensitive to energy inputs and global demand.A prolonged risk premium can pressure valuations.

A higher USD/KRW can support 일부 exporters in isolation, but in an energy-import shock, the macro effect is typically negative due to rising import costs.

12. Key points (news-style summary)

(1) Energy markets

- Strait of Hormuz risk increases uncertainty in crude oil and LNG supply

- Higher probability of a sustained high-price regime rather than a brief spike

- If physical disruptions occur, fourth-oil-shock narratives may strengthen

(2) Korea macro

- High import dependence increases pass-through of the shock

- Greater stagflation pressure via higher import prices and weaker growth

- Currency weakness can amplify the burden

(3) Sector channels

- Naphtha shock can propagate from petrochemicals into packaging, construction, autos, and consumer goods

- LNG shock pressures electricity tariffs, city-gas costs, generation economics, and industrial fuel costs

- Helium constraints create direct operational risk for semiconductors and advanced manufacturing

(4) Investment and markets

- Rising global growth concerns can weaken risk appetite

- Policy easing expectations may decline

- Korean equities may see higher volatility led by semiconductors and export cyclicals

13. Under-covered but high-importance points

- (1) The primary industrial risk may be naphtha rather than crude prices.

Naphtha shortages can disrupt packaging and intermediate inputs, with spillovers to consumer goods, construction materials, and auto components. - (2) De-escalation does not equal supply normalization.

If infrastructure is damaged, recovery may require 2–3 years, creating a structural supply constraint. - (3) Semiconductor risk may be driven first by specialty gases such as helium.

Process inputs can become binding constraints even if end-demand remains strong. - (4) Korea is exposed to supply-chain bottlenecks, not only higher oil prices.

Low energy self-sufficiency, high manufacturing intensity, and export dependence compound sensitivity. - (5) This is an industrial-system risk, not only an inflation headline.

The key risk is synchronized disruption across factories, logistics, distribution, and exports due to input shortages.

14. Key indicators to monitor

- Status of Strait of Hormuz transit conditions

- Escalation of LNG supply disruptions including Qatar

- Whether oil moves are transient spikes or become entrenched

- Further depreciation in USD/KRW

- Availability of semiconductor-grade helium and other specialty gases

- Operating rates at petrochemical complexes and naphtha inventory trends

- Government use of strategic reserves and progress on alternative sourcing

15. Policy and corporate response priorities

Near-term actions

- Audit and optimize strategic energy inventories

- Secure alternative procurement for LNG, helium, and naphtha

- Support import diversification and expedite emergency customs clearance

- Targeted financial support for vulnerable sectors and price-stabilization measures

Medium-to-long-term actions

- Diversify the energy import mix

- Build domestic resilience in strategic raw-material supply chains

- Strengthen stockpiling strategies for key inputs in petrochemicals and semiconductors

- Enhance energy security via renewables, nuclear, and storage infrastructure

The central question is not whether oil prices rise, but whether Korea’s industrial supply chain has sufficient resilience to withstand physical constraints and bottlenecks.

< Summary >

Escalation risk in the Middle East is a real-economy and supply-chain shock risk, not merely a geopolitical headline.

The core variable is the Strait of Hormuz.Disruption can constrain crude oil and LNG flows, raise import prices, and intensify the overlap of inflation pressure with growth deceleration.

Korea’s high energy import dependence and manufacturing intensity increase sensitivity.

Key industrial transmission channels are naphtha, LNG, and helium-linked semiconductor risks; physical availability is the dominant concern versus price alone.

Because infrastructure repair can require 2–3 years, the risk should be framed as a structural variable rather than a short-lived event.

[Related]

- Fourth Oil Shock and Key Transmission Channels for Korea

- Semiconductor Supply-Chain Reconfiguration and Export Strategy in the AI Era

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 중동전쟁 확전, 4차 오일쇼크 오는가? 반도체 산업도 흔들리나? 한국경제에 어떤 충격을 줄까? [경읽남 238화]