● Homebuying Shock, Hidden Gems, Rate Hikes, 3040 Winners

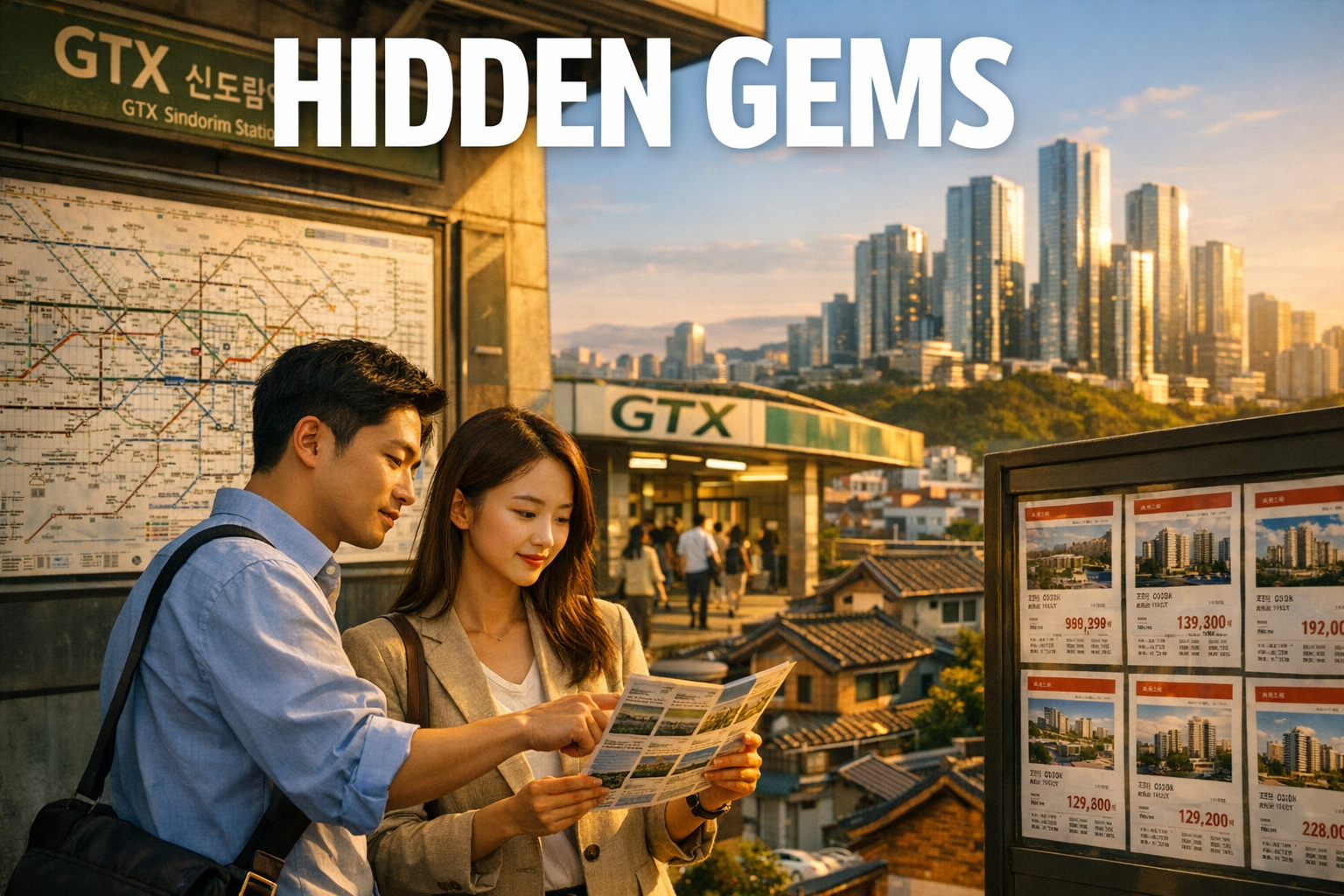

Missing the Real Opportunity by Focusing Only on Prime Districts: Homebuying Strategy for 30–40s Households in Sub-KRW 1 Billion Apartments

This report goes beyond the simple question, “Is it okay to buy a home now?”

It consolidates:

- Why concerns about holding taxes are often overstated

- How to compare the true cost of renting versus owning

- Why some areas can remain resilient despite Middle East risk, inflation, and rate hikes

- How to screen for “hidden gem” areas outside premium districts under KRW 1 billion

A key reframing is emphasized: prioritize areas that are structurally less likely to fall further (downside rigidity) rather than trying to predict which areas will rise next.

By connecting the themes of Seoul apartments, the greater metro market, housing outlook, rate hikes, and inflation, decision-making becomes more practical for first-time buyers in their 30s–40s and newlyweds.

1. Key Takeaway: Most Important Conclusion

In one sentence:

“Focusing only on premium districts can prevent ownership indefinitely; households in their 30s–40s should prioritize feasible purchase ranges and location fundamentals over tax-driven fear.”

- For single-home owners under KRW 2 billion, holding-tax burdens may be smaller than implied by market sentiment

- Delaying purchase can create larger costs via rent payments and foregone asset appreciation

- Geopolitical shocks, oil spikes, inflation, and rate hikes do not affect all apartments uniformly

- Focus on locations with rising demand and new/near-new supply where construction-cost dynamics limit downside

- Shift attention from ultra-high-priced assets to realistically purchasable KRW 0.5–1.0 billion assets

2. Why Non-Owners Worry About Taxes First

A recurring pattern in the market is that even non-owners prioritize tax concerns.

High visibility of policy headlines amplifies perceived burden beyond actual cash impact.

2-1. Holding-Tax Fear May Diverge from Real Burden

The core message is direct:

For homes under KRW 2 billion, using holding tax as the primary reason not to buy is often excessive.

For practical buyers considering KRW 0.5–1.0 billion homes, the more relevant comparison is the opportunity cost of rent and deposit structures versus ownership.

2-2. The Rent Comparison Changes the Decision

- Holding tax is an annual cost

- Rent is a monthly recurring outflow

- Rent does not build equity; ownership preserves the possibility of asset accumulation

As the market shifts from deposit-based leases toward monthly rent, non-owners face higher long-term cash-flow pressure.

Evaluate not only price levels, but also the cumulative rent likely to be paid over time.

3. Why Some Areas May Hold Up Despite Middle East Risk, Inflation, and Rate Hikes

The macro chain is plausible:Middle East geopolitical risk → higher oil prices → inflation → rate-hike pressure.

However, macro shocks do not transmit evenly across all housing assets.

3-1. Tight Credit Conditions Can Reduce Shock Transmission

Strong mortgage restrictions can function as a stabilizer.

When leverage is broadly excessive, rate hikes can force rapid deleveraging and price declines. Under stricter lending conditions, highly leveraged marginal demand may be smaller, reducing the probability of uniform market breakdown.

3-2. The Market Is Increasingly Location-Selective

Not all Seoul submarkets rise, and not all non-Seoul areas fall.

Differentiation is already pronounced within the same region, driven by:

- Transport access

- Employment proximity

- New-build status

- School zones

- Daily-life infrastructure

- Forward supply volume

Areas where these factors concentrate tend to be more resilient.

4. Core Principle: Downside Rigidity Matters More Than Upside Forecasts

Many market narratives focus on “which area will rise.”

For end-users, the more actionable question is:“Which area is less likely to drop materially?”

4-1. Construction Costs Create a Price Floor

The argument centers on build economics.

Even excluding land, construction costs for typical mid-size units are substantial. Adding land costs makes sub-KRW 1 billion pricing structurally difficult for new supply in core Seoul.

This is not purely optimistic framing; elevated replacement cost can limit downside for well-located new or near-new units.

4-2. Prioritize Assets Unlikely to Be Replaced More Cheaply

If comparable new-build products in the same location cannot be delivered at meaningfully lower prices at scale, existing pricing can be more defensible.

This dynamic is increasingly relevant across the greater metro area due to rising build costs and delayed redevelopment cycles.

5. Three Filters for Identifying Sub-KRW 1 Billion “Hidden Gems”

The central concept is demand expansion, driven by three factors.

5-1. Employment Growth

Housing demand ultimately follows jobs.

Drivers include:

- Major business districts

- Industrial clusters

- Tech company concentration

- Public-sector relocation

- Large corporate investment plans

5-2. Transport Links to Core Employment

Transport expands feasible commuting zones and reshapes relative value.

Rail and express transit projects can compress perceived distance to major job centers, pulling in real demand.

5-3. New or New-Scarce Supply

Preference for newer apartments is structural, supported by:

- Higher construction costs

- Redevelopment delays

- Higher presale prices

- Supply constraints

Within the same area, new builds—or locations where new builds are scarce—tend to maintain stronger competitive positioning.

6. Where to Look: Greater Metro Candidate Corridors

The practical target is “commutable-to-Seoul areas with relatively lower price pressure and lighter regulation.”

6-1. GTX-A Beneficiary Areas

GTX-A has visible market impact.

Where Seoul access improves materially, prices can be re-rated as those areas function as substitutes for Seoul housing.

6-2. Sinansan Line Beneficiary Areas

For households tied to Yeouido, the southwest corridor, or central business zones, this line broadens viable residence options. It is frequently cited as a demand-growth corridor with relatively lower entry pricing.

6-3. Dongbuk Line, Line 8 Extension, and Guri–Namyangju Corridor

Improved connectivity to the northeast corridor and Line 8-related access upgrades can support end-user demand. Areas previously considered marginal may be re-evaluated as commuting times change.

6-4. GTX-B and GTX-C Expectation Zones

Select areas such as Uijeongbu, Incheon Seo-gu, Bupyeong-gu, and Yeonsu-gu may see re-rating when transport upgrades align with new-supply competitiveness.

The key variables are access to core employment and scarcity of new apartments, not brand perception.

7. Why Fixating on Premium Districts Can Block Ownership

Premium school zones and ultra-core neighborhoods are high-quality assets.

For most households in their 30s–40s, the issue is that these markets are not a realistic benchmark. Anchoring to them can distort perception of attainable assets and perpetually delay entry.

7-1. Not Lowering Standards, but Making Criteria Realistic

The objective is not to abandon goals, but to secure a viable first entry point that enables future upgrading.

A staged “first station, then transfer” approach can be more feasible than attempting to buy the end destination first.

8. Why End-Use and Investment Considerations Must Be Integrated

For first-time buyers, both dimensions are typically required.

- If living conditions are poor, holding is difficult

- If price defense is weak, upgrading becomes difficult

- If access to jobs is limited, demand depth is weaker

- If new-build competitiveness is low, relative positioning can deteriorate

The first home should be “livable and upgrade-enabling,” rather than an idealized final product.

9. How to Approach Non-Metro Markets: Major City Strategy

Differentiate between major cities and smaller provincial markets.

9-1. Smaller Cities: Assess Industry Concentration Risk

Where a local economy depends heavily on a single industry, housing demand can weaken sharply when the cycle turns. Markets with concentrated exposure require more conservative positioning.

9-2. Major Cities: Focus on Core Tier-A Locations

Major cities have more diversified demand bases.

If a market has already undergone significant correction, core locations with new or near-new inventory can be in a stabilization phase.

Representative Tier-A areas:

- Busan: Haeundae-gu, Suyeong-gu

- Daegu: Suseong-gu

- Gwangju: Seo-gu, Nam-gu

- Daejeon: Seo-gu (Dunsan-dong)

These are local demand magnets rather than uniformly weak “non-metro” markets.

10. Central Message: Housing as a Stability Asset

Housing can be criticized in both rising and falling markets, but it remains a core component of household stability.

The framing is not an argument for multi-home speculation; it is a case for evaluating a primary residence pragmatically as part of cash-flow and stability planning, especially under elevated macro uncertainty.

11. Under-Discussed but High-Impact Points

11-1. Prioritize “Hard to Build Cheaper” Over “Likely to Rise”

Forecasting is uncertain; replacement-cost structure is more observable.

Construction cost, land cost, project feasibility, and presale price structures indicate locations where cheaper future supply is unlikely.

11-2. Rent’s Total Cost Can Exceed Tax Concerns

Policy headlines often amplify sensitivity to taxes, while cumulative rent outflows are underestimated.

From a cash-flow perspective, rent is a clear recurring loss; ownership retains the possibility of balance-sheet accumulation.

11-3. The Key Battlefield Is “Seoul-Accessible Substitutes,” Not Ultra-Core Luxury

The principal theme in the greater metro market may be the speed at which Seoul-accessible substitutes are re-rated, driven by expanding transport networks.

11-4. Credit Tightening Is Both a Headwind and a Crash Dampener

While restrictive credit can suppress demand, it also limits excess leverage and can reduce forced-selling dynamics.

12. Practical Checklist for First-Time Buyers in Their 30s–40s

- Do not anchor to premium districts or ultra-high-price benchmarks

- Calculate holding taxes as annual cash costs, not headline narratives

- Compare long-run rent/deposit costs alongside ownership costs

- Confirm mortgage principal-and-interest affordability first

- Validate the overlap of jobs, transport, and new-build scarcity

- Check whether replacement supply is structurally unlikely to be cheaper

- Evaluate livability and upgrade optionality simultaneously

13. One-Line Conclusion

The key question is not only whether prices rise or fall, but whether a household can secure an affordable asset with limited downside and credible demand support.

Fixation on premium districts can cause viable opportunities to be missed.

< Summary >

- Delaying home purchase solely due to holding-tax fear may be inefficient.

- Evaluate total rent-versus-own costs and foregone asset appreciation opportunities.

- Even under geopolitical risk and rate-hike pressure, locations with jobs, transport, and new-build scarcity can be relatively resilient.

- Prioritize areas where replacement-cost dynamics limit further declines, not only areas expected to rise.

- In the greater metro area, sub-KRW 1 billion new/near-new units in corridors benefiting from major transport upgrades are primary candidates.

- Outside the metro area, focus selectively on Tier-A core districts in major cities, emphasizing new/near-new inventory after meaningful corrections.

- For first-time buyers in their 30s–40s, the first home should enable the next upgrade rather than function as a final “dream home.”

[Related Articles…]

- https://NextGenInsight.net?s=GTX

- https://NextGenInsight.net?s=interest-rate

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 강남만 보면 평생 집 못 삽니다. 10억 이하 숨은 진주 찾는 법 | 경읽남과 토론합시다 | 김학렬 소장_3편

● Iran War Shock, Korea Stocks, Hidden Winners

The Iran War Prolongs: The Real Inflection Points for Korean Equities — Shipbuilding, LNG, Solar, Batteries, and Trading Houses in One View

This issue should not be interpreted solely as an “Iran war” or a Middle East risk event.

As the conflict extends, structural shifts may accelerate simultaneously across Korea’s manufacturing competitiveness, energy supply-chain reconfiguration, renewable energy, and sector leadership within the KOSPI.

This report focuses on:

- How this conflict may transmit to markets differently than the 2022 Russia–Ukraine war

- Why Korea may be a selective beneficiary in specific segments rather than a pure risk victim

- Why solar and nuclear power may regain momentum regardless of political preference in the US

- Which sectors and companies may sit at the center of these dynamics

A key point that is often underemphasized is summarized in Section 12.

1. Key News Briefing: Why This War May Affect Korean Equities Differently

Superficially, Middle East risk implies rising oil prices, logistics disruption, and broader geopolitical uncertainty.

However, current market pricing is not identical to past episodes. Within Korean equities, certain sectors are being reassessed not as direct casualties of war but as potential beneficiaries of supply-chain reconfiguration.

Historically, war-related shocks often caused Korea to trade as a single high-beta risk asset. In the current regime, sector dispersion may be larger, with defense, shipbuilding, LNG, solar, nuclear, batteries, and diversified trading houses gaining attention as “global bottleneck solvers.”

Core framing: not only “risk-off,” but “who becomes the substitute supplier.”

2. Why 2022 and 2026 May Differ: Similar Conflict, Different Market Regime

2-1. In 2022, Demand Shock and Tightening Dominated

During the Russia–Ukraine war, post-pandemic demand normalized while inflation and aggressive rate hikes hit global consumption.

Semiconductors were pressured more by weakening consumer electronics demand (PCs/smartphones) than by data-center resilience. The combined shock—war, high inflation, tightening, and consumption slowdown—depressed most sectors simultaneously.

2-2. Today, Many Large-Cap Korean Firms Are Positioned as Supply-Shortage Solutions

A meaningful portion of Korea’s large-cap complex has manufacturing capabilities that are difficult to replace quickly: defense, shipbuilding, semiconductors, nuclear, solar-related value chains, and batteries.

As wars persist, the key question increasingly becomes “who can produce and deliver,” with Korean corporates included in the plausible substitute set.

3. Sector Focus #1 if the War Extends: Shipbuilding

3-1. Strait of Hormuz Risk Can Increase Vessel Demand

Higher disruption risk in Middle East energy transport can accelerate import diversification.

If Asian buyers raise the share of US LNG, transport distances lengthen. Longer routes increase required ton-miles and, by extension, demand for LNG carriers and other high-value vessels—segments where Korean shipbuilders remain competitive.

3-2. The US May Be Structurally Constrained in Selecting Chinese Shipyards

From an energy-security and strategic-industry perspective, the US is likely to weigh ship origin and supply-chain alignment.

Large-scale ordering from Chinese yards may face political and security constraints, potentially supporting a “trusted supplier” premium for Korean shipbuilders beyond cyclical order growth.

4. Sector Focus #2 if the War Extends: Renewable Energy

4-1. Solar and Wind Are Increasingly Framed as Security, Not Only ESG

Renewables are shifting from an “environmental choice” to an “energy security tool.”

This matters because ESG arguments can be deprioritized in downturns, while security logic often overrides near-term cost concerns.

Imported fossil fuels remain exposed to maritime and geopolitical risks; domestically deployed solar/wind can reduce transport-linked vulnerability.

4-2. Why the US May Need to Re-embrace Solar

US policy motivation is increasingly tied to industrial strategy and national security: reducing reliance on China and lowering Middle East dependence, not only climate objectives.

This reframing can be a stronger and more durable support mechanism for deployment and supply-chain investment.

4-3. Efforts to Exclude China Can Advantage Korea

The US is attempting to reduce China exposure in strategic sectors including solar, nuclear, and batteries.

Near-term full self-sufficiency is limited by installation capacity, labor, value-chain maturity, and time. This creates demand for “non-China” substitute suppliers, where Korean firms may gain relevance.

5. Sector Focus #3 if the War Extends: Nuclear Power

5-1. Nuclear Returns as a Practical Energy-Security Option

Despite political controversy, nuclear remains a practical option for import-dependent economies.

The US seeks nuclear capacity but faces constraints in large-scale construction execution and skilled labor. Korea’s EPC, components, and operating experience can gain value under heightened supply-chain and security pressure.

5-2. The Differentiator Is Execution, Not Only Technology

Nuclear projects are won on delivery: schedule, budget, and safety.

Korea’s execution track record can translate into stronger competitiveness as reliability becomes a premium in an unstable geopolitical environment.

6. Sector Focus #4 if the War Extends: Batteries and EVs

6-1. Solar Expansion Pulls ESS and Batteries Along

Solar deployment increases demand for storage.

ESS is required to shift daytime generation to nighttime load, creating a structural linkage between solar build-out and battery demand. Solar and batteries should be analyzed as a combined theme.

6-2. EV Demand Should Be Assessed Beyond the US

US EV demand has shown volatility, but the global transition remains intact.

In Europe and selected regions, re-acceleration signs exist. Repeated oil shocks and geopolitical risks increase policy and consumer sensitivity to energy cost stability, which can reframe EV adoption beyond pure environmental narratives.

6-3. Europe’s China-Containment Can Become a Tailwind for Korean Battery Suppliers

Europe is increasingly concerned about China’s market penetration in batteries and EVs.

If policy incentives shift toward local or allied production, Korean firms—supported by trade frameworks and overseas manufacturing footprints—may improve access to Europe’s regulated supply-chain “inclusion” criteria, which can matter more than marginal export growth.

7. Sector Focus #5 if the War Extends: Diversified Trading Houses

7-1. Trading Houses Become More Valuable When Supply Chains Break

In wartime conditions, supply disruption, contract instability, and the need for alternative sourcing intensify.

Trading houses function as operational networks that reconnect supply chains, establish alternative procurement routes, and bridge energy, raw materials, and industrial inputs. De-globalization and bloc-based trade can support a structural re-rating of this business model.

7-2. Key Company Angles: POSCO International, Hyundai Corporation, LX International

- POSCO International: relatively high exposure to LNG and gas-related assets; may benefit from LNG import restructuring and upstream positioning.

- Hyundai Corporation: broad product and regional coverage through trading networks.

- LX International: differentiated positioning in resources and commodity-linked assets.

Company selection requires separating sector tailwinds from firm-specific exposures.

8. Why Korea’s Equity Market May Be Stronger Than Before: Structural Drivers Toward a “KOSPI 5000” Narrative

8-1. Korea as a Bottleneck-Relief Manufacturing Base

Korea is increasingly valued not for low-cost production, but for producing “hard-to-replace” industrial outputs.

Defense, shipbuilding, semiconductors, batteries, nuclear, solar-related materials, and industrials position Korea as a high-end manufacturing hub that fills gaps between advanced and emerging economies.

8-2. De-globalization Can Be Selectively Positive for Korea

De-globalization is often viewed as negative for trade-heavy economies.

In the current environment—where the US strategically constrains China—Korea can capture portions of the displaced capacity as an alternative production and technology supplier. This is more aligned with a medium-term 2026 macro/industry outlook than a short-lived theme.

9. Company Spotlight: Why OCI Holdings Is Frequently Discussed

9-1. A Rare Non-China Alternative in the Solar Value Chain

OCI Holdings is highlighted not as a generic solar theme, but as a potential non-China supplier within upstream solar materials, including polysilicon-linked value chains.

As the US tightens restrictions on China-dependent solar supply chains, credible alternatives remain limited, which can attach policy, supply-chain, and energy-security optionality to such names.

9-2. Linking Data-Center Power Demand and Solar

AI-driven data-center growth elevates electricity availability as a strategic constraint.

In this context, solar—alongside generation-asset operations and power delivery models—can be evaluated not only as an ESG segment but also as part of AI infrastructure investment. This angle is often underweighted in mainstream coverage.

10. Why the US May Ultimately Expand Renewables: The Core Rationale

10-1. Not Only Climate; Security and Industrial Hegemony

US renewable momentum can be explained by three overlapping priorities:

- Reducing Middle East dependence

- Reducing China supply-chain dependence

- Securing power infrastructure for the AI era

These drivers imply continued expansion of solar, nuclear, grids, and ESS under a broad range of political outcomes.

10-2. Renewables as a “Must-Do” Industry

Political preference is often overemphasized relative to industrial necessity.

When structural needs dominate, deployment proceeds even with ideological resistance. This shift can affect sector valuation frameworks.

11. Practical Portfolio Guidance for Retirees and Older Investors

11-1. The Key Variable Is Cash Flow, Not Age

Investors over 60 do not automatically need a uniformly conservative allocation.

The determining factor is recurring income (pensions, business income, labor income, rental income). With stable cash flow, a measured allocation to growth assets can be feasible. Without it—if living expenses rely on drawdowns—growth-heavy portfolios can be fragile.

11-2. If Cash Flow Is Limited: Prioritize Monthly Income Structures

Post-retirement, stable monthly inflows can be as important as capital appreciation.

A pragmatic approach may combine monthly dividend ETFs, REIT ETFs, selected covered-call ETFs, and short-duration rate-linked products. A common structure is a majority allocation to income-producing assets with a smaller sleeve for equity growth or index exposure.

11-3. If Single-Name Selection Is Difficult, ETFs May Be More Efficient

Single-stock investing requires continuous monitoring of earnings, industry shifts, valuation, policy risk, and competitive dynamics.

If sector views are constructive but selection is uncertain, using vehicles such as KOSPI 200 ETFs or industry ETFs (e.g., semiconductors, shipbuilding) can be operationally more efficient.

12. The Most Important Undercovered Points

12-1. The Core Benefit Is Not Oil Price Spikes, but Substitute-Supply Premium

Most war playbooks focus on refiners, crude, or gold.

In this regime, a more durable driver may be strategic positioning as a substitute supplier for capacity displaced from the Middle East and China. For Korea, the implication is a shift from “export beta” to “bottleneck relief” status.

12-2. Solar Should Be Evaluated Through the Lens of AI Power Infrastructure

Solar is often framed narrowly as policy-driven decarbonization or power shortages.

Going forward, AI-era electricity demand can re-rate solar, ESS, grids, and generation-asset operators as infrastructure enablers rather than only “green” exposure.

12-3. De-globalization Can Be Selectively Supportive, Not Neutral

Many commentaries treat de-globalization as purely negative for Korea.

In a US-led China-constraining framework, Korea can gain status as a replacement manufacturing base and technology supplier. This represents a potential position upgrade within a restructured industrial order.

13. Investment Checklist: Is It Appropriate to Buy Immediately?

Positive sector narratives do not justify entry at any price.

War-driven themes can exhibit sharp volatility, and policy expectations can be priced in ahead of fundamentals. Key checkpoints:

- Do earnings and cash flows follow through?

- Do policy narratives convert into actual orders and contracts?

- Is the current valuation already discounting excessive optimism?

Themes are secondary to realized performance and cash generation.

14. One-Line Conclusion

Prolonged Iran-war risk can be a macro headwind for Korea overall, but within Korean equities it can increase the strategic value of sectors that function as substitute suppliers—shipbuilding, defense, LNG, solar, nuclear, batteries, and diversified trading houses.

The central question is not fear itself, but who rebuilds supply and industrial order after disruption—and Korea may occupy more critical positions than typically assumed.

< Summary >

Middle East risk can be interpreted not only as a shock but also as an opportunity set tied to Korea’s role in manufacturing and energy supply-chain restructuring.

Shipbuilding, LNG, solar, nuclear, batteries, and diversified trading houses may emerge as structurally advantaged segments.

The key driver is “who becomes the substitute supplier,” not only higher oil prices.

Considering US and Europe’s China containment, intensified energy security, and AI-driven power demand, Korea’s strategic industrial value may rise.

For retirees, portfolio strategy should be determined by cash-flow availability; if single-name selection is challenging, ETF-based implementation can be more practical.

[Related Articles…]

https://NextGenInsight.net?s=solar

https://NextGenInsight.net?s=shipbuilding

*Source: [ Jun’s economy lab ]

– 이란 전쟁 지속되면 이 기업 주목하세요(ft.염승환 이사 2부)

● AI Chip Bottleneck, Packaging Wars, Nvidia-TSMC Power Grab

Advanced Packaging Is the Binding Constraint in AI Semiconductors

The AI semiconductor market is no longer defined solely by GPU design leadership. A key determinant is the ability to connect GPUs and HBM quickly and reliably, and to convert that capability into shipped volume.

This report outlines why advanced packaging has become the primary bottleneck in AI infrastructure, why NVIDIA remains advantaged, why TSMC functions as a gatekeeper, how Intel is positioning a response, and what investors should monitor.

News flow often emphasizes GPUs, HBM, and data center demand. In practice, outcomes are increasingly driven by interconnect and by securing production slots rather than by design announcements.

1. Why advanced packaging has become critical

Packaging has historically been treated as a back-end step focused on protection and external connectivity. In AI systems, packaging has shifted into a performance- and scalability-critical process that enables multiple dies to operate as an integrated system.

For AI accelerators, GPUs must operate tightly coupled with HBM. Even with best-in-class components, inefficient integration materially reduces system-level performance.

Advanced packaging functions as a core enabler of AI chip performance and deliverability.

2. Why the connection can matter more than the GPU

Conceptually:

- GPU: compute engine

- HBM: high-bandwidth data supply

- Advanced packaging: high-speed interconnect fabric

If the GPU–HBM data path is constrained, overall efficiency degrades, with downstream impacts:

- Lower performance per watt

- Reduced data center utilization efficiency

- Higher thermal density and cooling complexity

- Lower effective value proposition for end customers

The constraint is not “can the chip be designed,” but “can it be manufactured into a commercially viable AI module.”

3. The bottleneck: completion capacity, not design capacity

AI chip designs are proliferating as hyperscalers and semiconductor companies expand internal capabilities. However, design availability does not translate directly into shipments.

The limiting step is often advanced packaging capacity, where throughput is finite relative to demand. Common consequences include:

- Completed designs facing delayed shipment schedules

- Demand present but delivery lead times extending

- Competitive opportunities lost despite adequate design capability

- Revenue recognition timing shifting across quarters, affecting equity narratives

Competition is expanding from node leadership to capacity control: who secures scalable advanced packaging and stable supply chains.

4. NVIDIA’s advantage: pre-emptive control of packaging slots

NVIDIA’s position is not explained solely by GPU architecture. A major factor is early reservation of advanced packaging capacity at TSMC.

Technologies such as TSMC’s CoWoS are effectively required for high-end AI GPU + HBM integration. By securing a large portion of capacity, NVIDIA has supported shipment leadership versus competitors.

In AI infrastructure, the ability to supply on schedule often outweighs product announcement cadence. Markets tend to reward execution and conversion speed into revenue.

5. Why TSMC acts as a gatekeeper for AI infrastructure

TSMC is not only a foundry provider; it is a central manufacturing hub for AI accelerators, including advanced packaging. With CoWoS-class capacity constrained, expansion of AI compute can become rate-limited by TSMC’s ramp.

TSMC’s geographic diversification, including Arizona, is aligned with:

- Managing geopolitical concentration risk

- Stabilizing US-oriented supply chains

- Improving responsiveness to large US customers

- Positioning for long-cycle semiconductor capex and policy tailwinds

6. Intel’s differentiated approach: advanced packaging as a strategic counterweight

Intel is leveraging in-house advanced packaging (e.g., Foveros) to create alternative supply options and to support its broader foundry strategy.

Rather than using packaging solely for internal products, Intel is positioning packaging and manufacturing infrastructure to attract external customers. As the number of AI chip designers increases, many will require third-party manufacturing and integration partners.

Facility expansion centered on Arizona supports this repositioning. Market discussion around potential custom AI chip collaboration reflects Intel’s intent to evolve from a CPU-centric vendor toward an AI manufacturing and integration platform.

7. Even with strong HBM, GPUs, and data center demand, packaging is the final constraint

Common AI semiconductor drivers—HBM demand growth, GPU shortages, and data center expansion—convert into shipments only if advanced packaging is available.

Process chain:1) AI services expand, increasing data center demand

2) Data centers require more GPUs and HBM

3) High-performance integration requires advanced packaging

4) Packaging capacity shortages delay shipments

5) Shipment delays slow revenue realization and share gains

The most binding constraint is often late-stage integration capacity.

8. Market shift: key points

(1) Structural change

The industry’s competitive center is shifting from process nodes to advanced packaging capacity control.

(2) Drivers of NVIDIA’s lead

NVIDIA combines design leadership with early, large-scale reservation of TSMC advanced packaging capacity.

(3) Rising strategic importance of TSMC

TSMC is increasingly positioned as core AI infrastructure via manufacturing plus packaging.

(4) Intel’s response

Intel is using proprietary packaging and Arizona-based infrastructure to compete for AI manufacturing demand.

(5) Evolving investment criteria

Assessment is moving from “best design” toward “secured capacity, stable supply, and production execution.”

9. Underemphasized implications

First, advanced packaging is becoming negotiation power.

In a capacity-constrained environment, reserved slots improve delivery reliability and pricing leverage.

Second, potential winners extend beyond chip designers.

Manufacturing infrastructure, equipment, materials, and advanced back-end ecosystems may see more stable long-duration demand.

Third, packaging constraints create revenue timing gaps.

Strong demand does not ensure near-term revenue if completion is delayed, increasing sensitivity to guidance and expectations.

Fourth, geopolitics increases the value of packaging localization.

Taiwan concentration and US capacity build-outs directly affect shipment certainty.

Fifth, even if rate-cut expectations support growth equities, differentiation depends on physical supply.

Where capacity is secured, visibility and valuation support may be stronger than in demand-only narratives.

10. Investor checklist

1) Advanced packaging capacity ramp speed

Focus on time-to-volume, not announcements.

2) Long-term customer agreements

Slot reservation and contracted demand support revenue durability.

3) Yield and thermal management capability

For advanced packaging, quality and reliability can be more constraining than nominal capacity.

4) Exposure to US-led supply chain reconfiguration

Arizona and other US expansions may link to policy and strategic procurement tailwinds.

5) End-to-end linkage across HBM and GPU supply chains

Integration requires synchronized availability; strength in only one segment is insufficient.

11. Outlook: the next phase centers on integration and deliverability

The prior phase emphasized rapid design of high-performance AI chips. The next phase is likely to prioritize the ability to complete, integrate, and ship systems at scale on customer timelines.

Advanced packaging is shifting from a supporting process to a core infrastructure determinant. Investors may need to evaluate not only NVIDIA, TSMC, and Intel, but also back-end equipment, thermal solutions, materials, memory integration architectures, and data center power efficiency.

Core takeaway: the market is moving from “building better chips” to “integrating and delivering better systems at scale.”

Summary

- The primary bottleneck in AI semiconductors is advanced packaging, not GPU design alone.

- GPU–HBM integration speed and reliability drive performance and competitiveness.

- NVIDIA benefits from pre-emptive reservation of TSMC advanced packaging capacity.

- TSMC increasingly functions as a gatekeeper for AI infrastructure expansion.

- Intel is positioning advanced packaging and Arizona-based infrastructure as a competitive lever.

- Investment focus is shifting toward packaging capacity, yields, supply chain resilience, and proven time-to-volume execution.

Related Links

- https://NextGenInsight.net?s=HBM

- https://NextGenInsight.net?s=TSMC

*Source: [ Maeil Business Newspaper ]

– [LIVE] “엔비디아? TSMC?” AI 반도체 숨은 병목 해결사는? | 길금희 특파원