● Tokyo-Driven Matchmaking Shock

A Seoul National University graduate founder launched a Korea-Japan matchmaking event in Japan, but the model was not simply a dating business; it was built on connecting a market imbalance

The key point in this case goes far beyond the superficial idea of “wanting to meet Japanese women.”

The Korea-Japan matchmaking event reflects demographic shifts, individual mobility in the global economy, early customer acquisition for startups, the limitations of dating apps, service automation in the AI era, and even investor psychology in the stock market.

On the surface, it may look like a questionable matchmaking business, but a closer look suggests it resembles a form of “relationship market arbitrage” that connects structural imbalances in the Korean and Japanese dating markets.

One element often overlooked in other videos or reports is that this business is not simple matching, but a cross-border community business that builds trust through content and converts it into offline events.

1. Core development: why a Seoul National University graduate investor started a Korea-Japan matchmaking business in Japan

The founder in the original story is a Seoul National University graduate who had been involved in investing and stock study since college.

He initially focused on the stock market and trading, but moved to Japan in 2022 after the pandemic period.

His original reason for going to Japan was personal.

In his own words, he went to find a woman to marry, or more generally, to look for love.

He first enrolled in an MBA program at Waseda University and tried to meet a future spouse through the school, but after one semester concluded that it was not the right environment and changed direction quickly.

He later prepared for Japan’s Business Manager visa and started a company there.

The Business Manager visa is a category for foreigners who intend to operate a business in Japan, and it requires a legal entity and a concrete business plan.

He said this process took about one year.

2. Business model: maximize the number of introductions per trip to Japan

The core product is an offline exchange event where Korean men and Japanese women can meet naturally.

The original explanation makes clear that this is not an international marriage brokerage service, but an event designed for natural cross-cultural exchange and meetings between Korean and Japanese participants.

It is also important that the service does not promise marriage or act as a marriage intermediary.

The current format is closer to a rotation-style matchmaking event.

For example, when Korean men visit Japan on a weekend, the event is structured so they can speak briefly with multiple Japanese women on both Saturday and Sunday.

Participants have 10-minute one-on-one conversations with each other, then rank their preferences from first to third choice.

Matches are announced when both sides select each other.

In one event mentioned in the original story, the format was 8 men and 8 women, resulting in 6 matched couples.

Given that 3 to 4 couples is the usual average for an 8-on-8 event, this was a relatively high match rate.

The founder said this result reflected a well-balanced participant composition.

3. Operating regions and scalability: not only Tokyo, but also Fukuoka and Nagoya

One notable point is that this is not a small gathering of acquaintances.

The original explanation states that events are held in other parts of Tokyo and also simultaneously in Fukuoka and Nagoya.

In other words, Korea-Japan matchmaking events are operated in parallel across multiple Japanese cities every weekend.

This is closer to a real startup operating model than a casual social meetup.

That is because the process requires event operations, participant recruitment, gender balance management, on-site facilitation, match result tracking, and post-event communication.

The founder also mentioned plans to launch a landing page and web service in addition to the existing Naver Cafe channel.

He further plans to add one-on-one introductions alongside the rotation-style event format.

4. Founder’s market thesis: imbalance in the Korean and Japanese dating markets

The most important economic interpretation of this business is supply-demand imbalance.

The founder views the Korean dating market as one in which women of the same age group are relatively scarce, increasing competition in dating and marriage.

By contrast, he says Japan has a large number of men over 40 who have little or no dating experience.

Of course, this should not be reduced to a simplistic generalization of either country.

However, the founder appears to believe that connecting a subset of Korean men and Japanese women who are interested in one another can create a viable market.

From an economic perspective, this is similar to arbitrage based on regional price differences.

Some people in Korea may still struggle to match despite being competitive in the dating market, while in Japan there are women interested in Korean men but lacking accessible channels to meet them.

By connecting these two groups, both sides gain new options.

This case illustrates how globalization and mobility are increasingly transforming dating and marriage into a cross-border market.

5. Difference from conventional dating apps: focus on getting people to meet

The founder was critical of conventional dating apps.

His view is that many dating apps monetize in-app communication and item purchases rather than actual meetings.

In other words, the company’s revenue model may not be fully aligned with whether users actually meet in person.

He also noted that many dating apps have severely imbalanced gender ratios, often 9:1 or 10:1.

He chose the opposite approach and first secured a female user base.

He reportedly gathered more than 10,000 Japanese female followers.

He then planned to use this base to offer introductions and coordinate meetings for Korean men visiting Japan based on preferences and needs.

This approach is not a standard app business but rather a community-based offline matching service.

6. Content strategy: the founder became his own tester

Another distinctive feature is that the founder became an influencer himself.

Although he said he is naturally private and identifies as introverted, he created content and built followers to promote the service.

He positioned the business as the answer to the question Japanese women might ask: where can I meet Korean men?

In development, using your own product is sometimes called dogfooding.

This case is similar.

The founder first used SNS in Japan to publicly search for his own partner, turning the process into content.

He then expanded the story into a brand narrative: he met someone this way, and many good Korean men around him could also be introduced.

This is not an ad-heavy model, but one that builds trust through the founder’s story.

It is a typical example of an early-stage startup building trust and narrative before capital.

7. Participant experience: language preparation and sincerity affect match outcomes

Participant interviews from the event are also notable.

One Korean attendee said Japanese study was his hobby and that he joined because he thought meeting Japanese women could help him learn the language while building a relationship.

He described Japanese women as gentle.

After the event, participants said the women were attractive and charming, and that they would recommend the experience to friends.

He added that preparing in Japanese would make the experience much better.

The founder also said some participants ask ChatGPT to generate likely questions and memorize Japanese answers in advance.

This is a practical use of AI.

AI is not replacing dating, but reducing the burden of language barriers and conversation preparation.

This trend is likely to grow in international exchange, study abroad, overseas employment, and cross-border dating markets.

8. Cultural differences in Korea-Japan dating: communication means different things

One of the most practical cultural differences mentioned in the original story is communication frequency.

In Korea, communication in a relationship is often seen as part of the relationship itself.

Daily updates, travel notifications, and messages that prevent worry are often considered part of maintaining the relationship.

In Japan, communication is described as being used more functionally.

It may be limited to arranging plans, morning greetings, and evening greetings as a way to confirm well-being.

Instead, there is a stronger emphasis on being fully present during in-person meetings.

This difference has both advantages and drawbacks.

It can support mutual trust and respect for each other’s time, but communication gaps may also feel unsettling.

Anyone considering a Korea-Japan relationship should therefore understand communication style differences before focusing on appearance or image.

9. Main operating risk: fatigue from a people-intensive service business

The founder originally worked in investing and trading, so he had limited service-sector experience.

Stocks are ultimately a contest between the individual and the market, but service businesses require direct interaction with customers.

While most customers are reasonable, some participants may behave rudely or outside normal social boundaries, which creates significant fatigue.

This is a core risk in offline matching services.

Just a few problematic customers can damage the atmosphere of an event and the brand’s credibility.

To scale this business, participant screening, behavioral rules, on-site safety, privacy protection, and dispute resolution are more important than simple recruitment.

Cross-border relationship services in particular require a highly detailed operating manual because language and cultural differences add complexity.

10. Investment perspective: long-term holding of structural winners over trading

The original story also includes the founder’s investment experience.

He said he suffered major losses while trading alone in Japan.

Operating in isolation limited idea exchange, undermined conviction, and led to poor timing.

He said he even lost money in rising stocks, reflecting weakened trading discipline.

He later admitted he was not suited to trading and shifted to a strategy centered on fundamentally strong companies aligned with long-term trends.

In the original story, he is said to have concentrated his investment in SK hynix.

He effectively positioned himself behind a leading semiconductor company benefiting from AI chip demand and HBM market growth.

One interesting point is that being too busy with the business reduced his ability to watch the stock market frequently, which may have helped him endure volatility.

In the market, there is a common joke that “you make money only if you sleep on it for a year.”

In practice, holding strong assets for longer can be more effective than frequent trading.

Of course, there is no single correct approach, and concentrated positions carry significant risk.

Still, this case shows how being busy with a business can reduce overtrading.

11. AI and the future of developers: automation pressure starts with expensive work

The latter part of the discussion also covers artificial intelligence and the future of developer jobs.

The argument is that developers are expensive, which creates strong pressure for AI substitution.

Development work also has a large amount of publicly available code and training data, and many tasks have relatively clear outcomes.

Unlike fields such as art, where it is difficult to judge definitively what is better, code has a more measurable standard of whether it works.

For that reason, development is one of the areas most likely to be penetrated first by AI.

That said, the founder said developers at his company help reduce workload and support new service development.

This is important.

Rather than eliminating developers, AI is more likely first to expand the scope of work one developer can handle and accelerate execution in startups.

In the future, more small teams will likely use AI tools to build web services, automate operations, manage customers, and create matching systems.

12. The deeper point rarely emphasized in other videos or news reports

The core of this case is not simply “connecting Korean men and Japanese women.”

The real significance lies in three points.

-

First, relationship markets are becoming global.

In the past, dating and marriage were shaped by neighborhoods, schools, workplaces, and introductions through acquaintances.

Today, language learning, travel, SNS, content, and AI translation tools are making relationships increasingly cross-border.

-

Second, this is the dating version of content commerce.

The founder builds trust through content, gathers followers, and then converts them into offline events and paid services.

This is a model long used in e-commerce and education businesses, now applied to dating.

-

Third, offline trust is becoming a premium asset in the digital era.

Dating apps are convenient, but often cause fatigue and do not always lead to real meetings.

By contrast, verified people meeting at a fixed time and place can reduce trust costs.

13. Key issues that must be addressed for growth

The growth potential is clear, but several issues remain.

The first is legal positioning.

The company must clearly distinguish itself from international marriage brokerage and avoid language that could be interpreted as promising marriage or acting as a spouse intermediary.

The second is participant quality control.

If demand becomes too concentrated on one gender, service satisfaction will decline.

Participant temperament, language ability, age group, interests, and etiquette must be balanced to sustain match rates.

The third is safety and privacy protection.

Cross-border meeting services involve contact exchange, follow-up meetings, and travel arrangements, so incident response is critical.

The fourth is the balance between scalability and human oversight.

Too much automation weakens trust, while too much manual work exhausts the founder and operations team.

Ultimately, AI-based customer management, participant recommendations, language support, and scheduling systems are likely to become core infrastructure.

14. What this business means from an investor perspective

From an investor perspective, this is a niche-market startup with a clear target segment.

It does not target the entire population, but rather Korean men interested in Japanese women and Japanese women interested in Korean men.

Although the target market appears narrow, the message is clearer as a result.

It also connects naturally to adjacent demand from travel to Japan, Japanese language study, K-content, and Korea-Japan cultural exchange.

If customer acquisition costs remain low, profitability could be acceptable.

However, trust is difficult to restore once broken in a matching service.

Maintaining community quality and brand reputation is more important than short-term revenue.

In that sense, the founder’s strategy of appearing publicly and building a brand story is both an advantage and a risk.

Trust can be built quickly, but any problem may concentrate responsibility on the founder personally.

15. Message for individuals: compete where you have an advantage

The most memorable line in the original story is the idea that people should compete in the market where they are advantaged.

Failing in Korea does not necessarily mean a person lacks appeal or value.

It may simply mean that their strengths work better in a different market.

This applies not only to dating, but also to careers and investing.

For some people, long-term investing is a better fit than trading; for others, startups fit better than large corporations; for others, overseas markets fit better than domestic ones.

The key is not to force oneself into the wrong environment, but to find the one in which one’s strengths are most effective.

The founder’s shift from investor to Japan-based Korea-Japan matchmaking entrepreneur can be seen as the result of that kind of decision.

< Summary >

A Korea-Japan matchmaking event launched in Japan by a Seoul National University graduate investor is not simply a dating business; it is a startup model built on connecting imbalances in the Korean and Japanese relationship markets.

The core product is a rotation-style offline event in which Korean men and Japanese women meet multiple participants over a weekend.

The business operates across Tokyo, Fukuoka, and Nagoya, and one 8-on-8 event reportedly produced 6 matched couples.

Unlike conventional dating apps, it emphasizes real meetings, participant balance, and offline trust.

The founder first built a Japanese female follower base and used content and personal branding to establish trust.

AI is likely to become increasingly important for Japanese conversation preparation, customer management, and service automation.

From an investment perspective, the case also illustrates the value of long-term holding in semiconductor leaders and the risk of overtrading.

The central message is that whether in dating, investing, or careers, individuals should seek the market and environment where they are most effective.

[Related Articles…]

*Source: [ 내일은 투자왕 – 김단테 ]

– 서울대 출신이 만든 수상한 한일 소개팅 사업

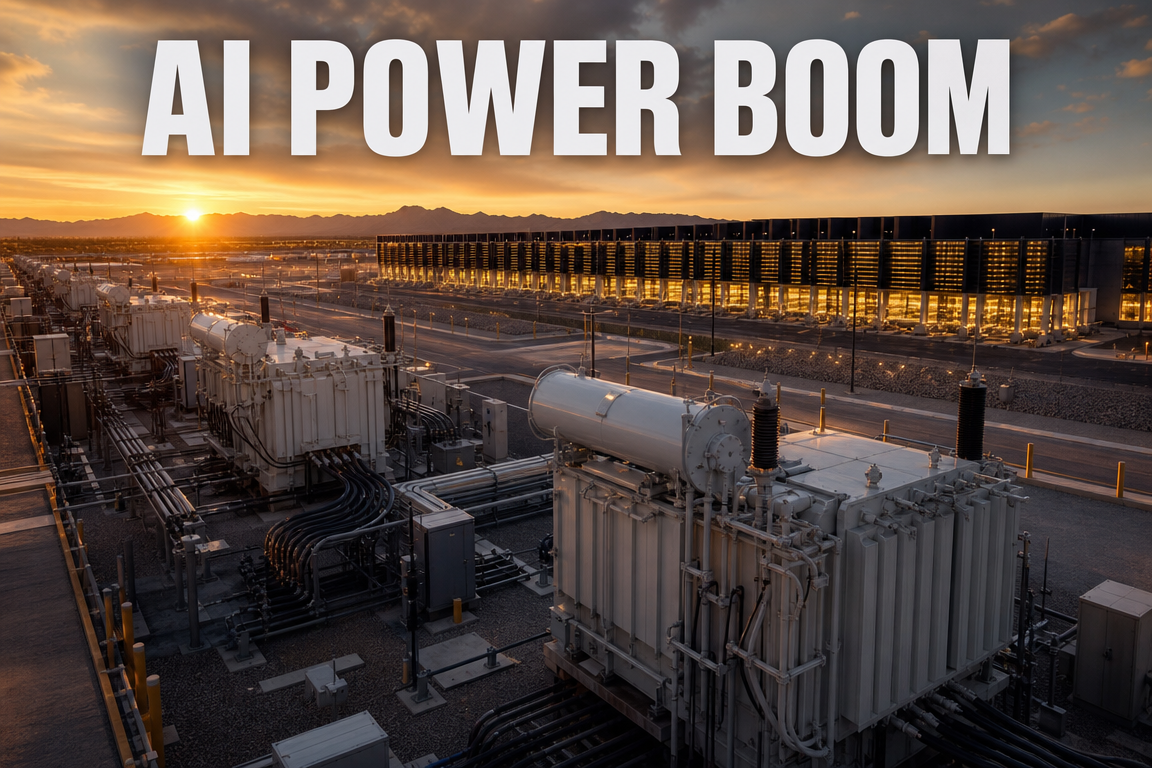

● Power Grid Supercycle, AI Data Centers, Power Bottleneck

The Next Bottleneck After Semiconductors Is Power: Key Takeaways From the AI Data Center Power Infrastructure Supercycle

The key point of this article is clear.

The real bottleneck in AI data center growth is shifting from GPUs and HBM to power infrastructure.

The power equipment cycle has already entered a supercycle since 2023 and should be viewed not as a theme but as a structural shift that may extend through 2030 and, in some cases, to 2035.

In particular, ultra-high-voltage transformers, distribution equipment, ESS, on-site generation, renewable energy, and SMRs are emerging as the next major pillars of the AI investment cycle.

However, because some stocks have already risen significantly, it is important to distinguish between an industrial cycle that is still in an early phase and a stock-price cycle that is already in the mid-stage.

Failing to distinguish between the two can lead to poor timing even when the underlying industry remains strong.

1. The key market trend in 2026: semiconductors still lead, but power infrastructure is catching up

The 2026 stock market can be characterized by strong concentration in technology.

In the first quarter, semiconductors and power equipment moved together.

Within the same AI infrastructure theme, Samsung Electronics, SK hynix, HD Hyundai Electric, Hyosung Heavy Industries, and LS Electric all posted strong performance.

From the second quarter onward, however, the market dynamic changed.

Capital and speculative demand became increasingly concentrated in Samsung Electronics and SK hynix through single-leverage products and stronger fund flows.

In other words, since May, the market has effectively treated semiconductors as a liquidity black hole.

The power equipment sector has not weakened operationally; rather, it has temporarily lost some leadership in the short term.

Semiconductors are likely to remain the near-term market leader in the second half.

That said, over the medium to long term, AI data center expansion will continue to increase the importance of power infrastructure.

2. The power equipment supercycle began in 2023

Many investors believe that the power shortage linked to AI data centers is a recent issue.

In reality, the power equipment cycle entered shortage conditions in 2023.

Initially, the main drivers were not AI data centers but replacement of aging U.S. power grids, reshoring policy, manufacturing relocation, and renewable energy interconnection demand.

Once a power grid replacement cycle begins, it rarely ends quickly.

Even a standard infrastructure replacement cycle can last more than six years.

This time, new AI data center demand has been added on top of that.

That is why the cycle is being described as a power supercycle.

Importantly, order backlogs already extend through 2030.

Looking further out, the cycle may continue through 2035.

This is not a short-term theme but a structural shift driven by AI infrastructure, the energy transition, and manufacturing reshoring simultaneously.

3. The AI bottleneck is moving from GPU to HBM to power infrastructure

Within the AI value chain, bottlenecks have continued to move.

In 2024 and 2025, GPU shortages were the central issue.

Without access to Nvidia GPUs, AI models could not be deployed at scale.

After that, HBM and DRAM constraints became more prominent.

High-bandwidth memory became essential for performance gains in AI semiconductors, drawing investor attention to SK hynix and Samsung Electronics.

By mid-2026, however, another bottleneck is becoming increasingly important.

That bottleneck is power.

Even if a company wants to build an AI data center, it cannot proceed without sufficient power supply and regulatory approval.

Some data centers consume more electricity than the residential demand of a city of one million people.

The issue is no longer simply whether GPUs can be purchased, but whether the data center can be built at all.

At that point, the key constraints become the power grid, transformers, distribution equipment, and generation capacity.

4. Power bottlenecks may partially ease semiconductor bottlenecks

There is an important paradox here.

If power infrastructure is insufficient, AI data center construction slows.

If data center construction slows, demand for GPUs and HBM cannot expand as aggressively in the near term.

In other words, a power infrastructure bottleneck may partially temper pressure on semiconductor supply chains.

This is a key point that is often overlooked in mainstream commentary.

Looking at the AI investment cycle only through the lens of semiconductors can be misleading.

The next leadership sector is often determined by where the binding constraint lies.

The bottleneck first sat with GPUs, then with HBM, and now increasingly with power infrastructure.

For this reason, AI investment analysis should cover not only the semiconductor supercycle but also the power infrastructure constraint.

5. Why power equipment earnings should continue to improve

The earnings strength of power equipment companies is straightforward.

Demand is strong while supply remains limited.

Ultra-high-voltage transformers, circuit breakers, and distribution systems cannot be scaled up as quickly as semiconductors.

In particular, ultra-high-voltage transformers have long lead times and high technical barriers.

Delivery can typically take around two years.

As a result, orders are recognized in revenue only gradually.

This structure allows earnings to be reflected sequentially over several years.

Major companies have already delivered substantial operating profit growth since 2023.

HD Hyundai Electric recorded operating profit growth of more than 100% early in the supercycle.

Hyosung Heavy Industries also posted operating profit growth close to 100% and is expected to maintain high growth.

LS Electric attracted attention later, but operating profit growth has risen significantly this year as well.

In this sense, the power equipment sector is a growth industry supported by earnings.

6. However, investors should watch for deceleration in growth rates

A strong industry does not mean every stock can keep rising at the same pace.

Capital markets do not focus only on absolute earnings.

They focus on the rate of change in earnings.

For example, if operating profit rises 100% one year and 60% the next, the business is still growing very strongly in real terms.

But the equity market may interpret that as a slowdown in growth.

This distinction matters.

Corporate earnings may continue to improve even when share prices pause.

At the same time, capital may rotate toward companies showing faster growth within the same sector.

When analyzing power equipment, the key question is not simply whether the industry is attractive, but which companies can sustain accelerating growth in the next one to two years.

That is also why HD Hyundai Electric, Hyosung Heavy Industries, and LS Electric gained attention at different times.

7. Why ultra-high-voltage transformers matter: only a few companies can produce 765kV units

One of the most important product categories in the power equipment cycle is the ultra-high-voltage transformer.

In particular, demand is rising rapidly in the United States for 765kV-class transformers, which only a very limited number of companies worldwide can produce.

Only four to five global players are considered capable of meaningful production in this segment.

South Korean companies are among them.

HD Hyundai Electric and Hyosung Heavy Industries are commonly cited examples.

This is the core of Korea’s competitiveness in power equipment.

Demand is rising sharply while supply remains concentrated, creating favorable pricing power for suppliers.

In that environment, margins improve.

The earnings upside is driven not only by foreign exchange effects but also by technology strength and supply scarcity.

8. Could a weaker KRW/USD exchange rate be a major risk for power equipment companies?

In 2025 and 2026, a stronger dollar supported export-oriented companies.

Power equipment firms, which have significant U.S. exposure, also benefited from a favorable exchange rate.

Some investors worry that a stabilization in the exchange rate could weaken earnings.

That concern appears overstated.

Pricing power in the power equipment sector is driven more by product competitiveness and supply tightness than by currency movements.

For ultra-high-voltage transformers in particular, where global suppliers are limited, demand-supply imbalance matters more than exchange rates.

In addition, Korean companies are expanding U.S. local production to address tariff risks and supply chain restructuring.

As local production increases, sensitivity to the exchange rate should gradually decline.

Accordingly, while a strong dollar has supported earnings, a weaker dollar does not automatically imply the end of the power equipment supercycle.

9. How the Middle East conflict and rising bond yields affected power infrastructure investment

Following the Middle East conflict, a notable shift occurred in the global economic outlook.

Governments increased defense spending and energy security investment.

This led to higher sovereign issuance and upward pressure on bond yields.

Normally, higher bond yields weigh on equities.

However, some sectors such as semiconductors and power equipment remained strong.

The reason was earnings support.

The conflict increased attention to energy security and strengthened the push to reduce dependence on fossil fuels.

As a result, investment in renewable energy, nuclear power, power grids, transformers, and ESS became even more important.

In the U.S. as well, the political stance against renewables has shown signs of softening.

Power infrastructure investment is therefore becoming not only an AI theme but also a strategic energy and security theme.

10. Data center permitting delays: power shortages are the direct constraint

One of the biggest issues in AI data center construction is permitting.

Even when a company wants to build a data center, approval may be delayed if the local power grid cannot support the load.

In the U.S., reports of delayed data center projects continue to emerge.

The reasons include power shortages, transmission constraints, environmental regulation, local opposition, and concerns over higher electricity prices.

To address these issues, U.S. regulators and grid operators are revising interconnection rules.

There are efforts to speed up permitting and accelerate grid connection.

However, regulatory improvement does not immediately solve equipment shortages.

Ultra-high-voltage transformers and related power equipment still require long production lead times.

This is one of the reasons the power equipment cycle may last longer than typical industrial upcycles.

11. Why on-site generation is gaining traction: building power plants next to data centers

Relying on distant power supply through the grid takes time.

Transmission expansion and permitting are also required.

As a result, on-site generation is increasingly seen as an alternative.

On-site generation refers to installing small power sources near the data center.

Possible solutions include solar, ESS, gas turbines, and fuel cells.

Solar power combined with ESS can help cover part of the data center’s load.

Gas turbines are attracting attention because they can be installed relatively quickly.

However, gas turbines are not strictly renewable energy.

Hydrogen fuel cells and SOFCs are also being discussed as potential power sources for data centers.

The issue is that these generation technologies may also face shortages if demand rises sharply.

In effect, AI data centers may create shortages not only in power equipment but across the generation ecosystem.

12. ESS is becoming important both inside and outside data centers

ESS refers to energy storage systems.

Because they can store electricity and supply it when needed, they help stabilize the grid.

Within AI data centers, where electricity demand is large and load fluctuation matters, ESS adoption is likely to increase.

ESS is not only a complement to renewable energy.

It can also be used within data centers to stabilize power quality.

Recent increases in ESS shipments in the U.S. are consistent with this trend.

As renewable energy, on-site generation, and internal power stabilization converge, ESS is becoming a core product category in the power value chain.

13. Why distribution deserves more attention

Historically, the market has focused on transmission when assessing power equipment companies.

Transmission has higher technical barriers and stronger margins.

Ultra-high-voltage transformers, for example, can command premium valuations because only a few companies can produce them.

However, distribution is now receiving more attention.

The reason is data centers.

Data centers and adjacent facilities require substantial distribution equipment to allocate power efficiently.

As on-site generation expands and power is supplied over shorter distances, demand for distribution equipment should increase.

The distribution market is more competitive than transmission.

Even so, the market itself is expanding.

Companies that can rapidly gain share in distribution may therefore receive greater attention.

This is also why LS Electric is drawing interest across both distribution and transmission.

14. Special transformers and Sanil Electric: why valuation discussions are emerging

The special transformer market has historically received less attention.

There have been relatively few Korean companies with meaningful exposure to this segment.

Sanil Electric is one of the companies attracting attention in special transformers.

Although termed “special,” these transformers are often similar in size to distribution transformers.

Their unit prices are much lower than those of ultra-high-voltage transmission transformers.

Transmission transformers can cost hundreds of billions of won per unit, while special transformers are priced significantly lower.

That is why the market has typically assigned higher multiples to transmission-focused companies.

However, Sanil Electric is reporting strong operating margins.

With operating margins above 30%, the company appears attractive on the numbers alone.

It is also expected to enter the 154kV-class ultra-high-voltage transformer market from 2028.

If that occurs, it may support a re-rating.

That said, the company does not yet have global top-tier share, so it may take time to justify the same multiple as larger peers.

High margins may also be viewed as a challenge rather than a given.

As revenue scales up, sustaining the current margin profile will be the key issue.

15. Can SMRs solve the power shortage?

Nuclear power is a stable source of large-scale electricity.

However, new nuclear projects take too long to complete.

Even if a project is awarded today, permitting, contracting, construction, and testing can take more than 10 years.

As a result, conventional nuclear power has limited usefulness in solving near-term AI data center shortages.

SMRs are being discussed as an alternative.

SMRs, or small modular reactors, could be linked to distributed power networks, on-site generation, and industrial power supply.

If SMRs are commercialized and applied near data centers, they could become a major development.

However, commercialization timing and practical applicability still need to be confirmed.

In short, SMRs are an important long-term option, but they cannot fully resolve the current bottleneck today.

16. Could space-based data centers be a negative for power infrastructure?

SpaceX and Elon Musk’s concept of space-based data centers has drawn market attention.

If data centers can be built in space, demand for terrestrial data centers may decline.

If space-based data centers fully replace ground-based facilities, that would clearly be negative for power infrastructure companies.

Lower demand for terrestrial data centers would reduce demand for transformers, distribution systems, and power grids.

However, current market assessments generally view the concept as difficult to realize in the near term.

Even if technically feasible, economics remain a major challenge.

It is unlikely that space-based data centers can displace terrestrial hyperscale facilities in the short term.

Placing GPUs on satellites may be possible in some form, but the scale and cost efficiency of current ground-based data centers would be difficult to match quickly.

Accordingly, the likelihood that space-based data centers materially reduce power infrastructure demand before 2030 appears low.

That said, such headlines may continue to create sentiment pressure in the stock market.

Investors should distinguish between operational risk and market sentiment risk.

17. The most important point missing from many other discussions

The most important point is that the power infrastructure cycle should be viewed through both an industrial-cycle lens and a stock-price-cycle lens.

From an industry perspective, power infrastructure still has a long runway.

As AI data centers continue to expand, and as physical AI, robotics, autonomous driving, and industrial AI spread, power demand will likely increase further.

Demand for grids, transformers, ESS, distribution equipment, and on-site generation may continue well beyond 2030.

From a stock-market perspective, the picture is different.

Some power equipment stocks have already risen severalfold.

Accordingly, it is not accurate to assume that every name is still at an early stage of the cycle.

The industry may be early or mid-cycle, but certain stocks are already in a later phase of valuation re-rating.

That distinction is central to investment decisions.

Another key point is that the power bottleneck can act as a control mechanism on semiconductor demand.

If data centers cannot be built, the pace of GPU and HBM orders may also slow.

Therefore, AI investors should track not only semiconductor earnings, but also power permitting, transformer lead times, data center construction delays, ESS supply, and on-site generation contracts.

18. Key investment checkpoints

First, backlog matters.

Power equipment companies are highly order-driven.

Investors should track the size of the order backlog and when it will be recognized in revenue.

Second, product mix matters.

Companies with a higher share of high-margin products such as ultra-high-voltage transformers are better positioned.

The ability to produce 765kV-class products is a major competitive advantage.

Third, operating profit growth rates matter.

Profit growth alone is not enough.

Investors should assess whether the growth rate is still accelerating.

Fourth, U.S. local production matters.

With tariff and supply chain risks in play, U.S. manufacturing capacity is increasingly important.

Fifth, data center exposure matters.

Investors should verify exposure to AI-related orders in distribution equipment, ESS, special transformers, and on-site generation.

Sixth, valuation matters.

Even strong companies can face near-term corrections if expectations are already too high.

Conversely, less-followed companies with strong margins and growth potential may still be re-rated.

19. Conclusion: AI infrastructure is built by semiconductors and power together

The core of the AI era is not semiconductors alone.

GPUs and HBM are the core of AI computation, but power infrastructure is what allows AI to operate in practice.

Without electricity, there are no data centers.

Without data centers, there are no AI services.

For that reason, power infrastructure is the most practical bottleneck in the AI economy.

The semiconductor supercycle and the power supercycle may appear separate, but they are ultimately part of the same AI value chain.

Going forward, global investors should monitor AI data centers, power infrastructure, the energy transition, bond yields, and the KRW/USD exchange rate together.

Semiconductors may still lead in the short term.

However, the structural change over the medium to long term is likely to be more pronounced in power infrastructure.

Investors must distinguish between a good industry and a good entry price.

Power infrastructure is clearly a strong industry.

At the same time, stocks that have already rerated sharply require careful analysis of growth rates and valuation.

That distinction is essential for identifying the next opportunity created by the AI data center power bottleneck.

< Summary >

The bottleneck for AI data center growth is shifting from GPUs and HBM to power infrastructure.

The power equipment supercycle began in 2023 and may continue through 2030 to 2035.

Key value chain segments include ultra-high-voltage transformers, distribution equipment, ESS, on-site generation, renewable energy, and SMRs.

Only a small number of companies globally can produce 765kV-class ultra-high-voltage transformers, and Korean companies remain competitive.

The industrial cycle still has room to run, but the stock-price cycle in some names is already in a later phase, making valuation important.

Space-based data centers may pose a long-term risk, but they are unlikely to replace terrestrial data centers and power infrastructure demand in the near term.

AI investors should therefore monitor not only semiconductors but also power permitting, transformer lead times, ESS, and on-site generation orders.

[Related Articles…]

AI Data Center Power Infrastructure Bottlenecks and Investment Implications

Semiconductor Supercycle and HBM Supply Chain Outlook

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [풀버전] 반도체 다음은 전력? AI 데이터센터가 만드는 진짜 병목 | 경읽남과 토론합시다 | 손현정 연구원