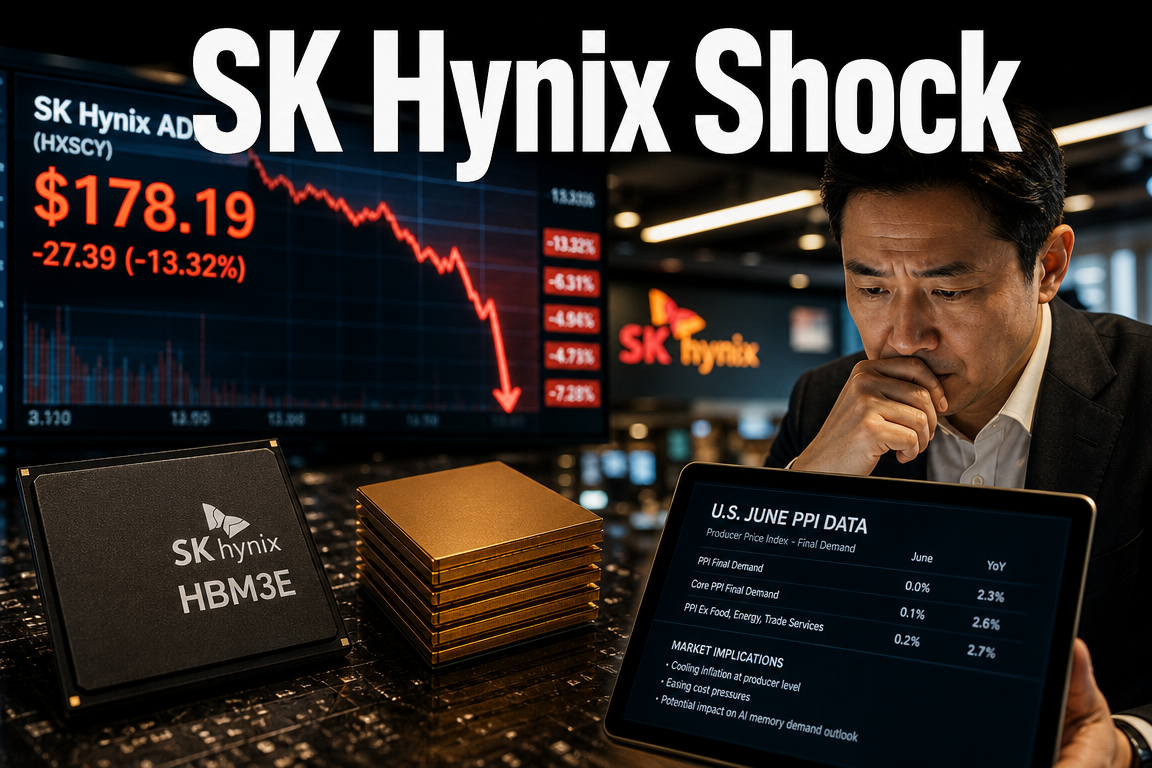

● SK Hynix ADR Plunge, AI Chip Shock, Kospi Hit

Summary of the Sharp Decline in SK hynix ADR: What Drove the Volatility in Semiconductors and the Impact on the KOSPI

The recent decline in the SK hynix ADR should not be viewed as a simple one-day selloff.

The key issues are threefold.

First, capital is rotating out of memory semiconductor names and into large-cap technology stocks that had rallied less aggressively earlier in the year.

Second, the premium that had built up between the SK hynix ADR and the domestic Korean listing may be starting to normalize.

Third, crowded positioning in AI semiconductors and HBM-related names is creating near-term pressure on the KOSPI outlook.

The main question is not whether SK hynix fundamentals have suddenly deteriorated, but rather how aggressively capital is being unwound from a heavily re-rated stock.

1. Event Summary: Why Did the SK hynix ADR Fall So Sharply?

According to the source, the SK hynix ADR fell as much as 11% intraday.

An ADR is a depositary receipt that allows U.S. investors to trade shares of a foreign company without directly accessing the local market.

In other words, the ADR is linked to the Korean-listed stock, but it can move more sharply depending on U.S. market liquidity and sentiment.

-

Reason 1: Capital shifted from memory semiconductors to large-cap technology stocks.

-

Reason 2: The premium between the SK hynix ADR and the domestic share price was viewed as excessive.

-

Reason 3: Sentiment among semiconductor investors weakened quickly, accelerating selling pressure.

-

Reason 4: A steep decline in KOSPI night futures increased concerns about broader weakness in Korean equities.

This move appears to reflect valuation concerns, profit-taking, and crowded positioning more than a change in underlying industry conditions.

2. First Factor: Rotation from Memory Semiconductors to Large-Cap Tech

One of the strongest global equity themes this year has been AI semiconductors.

Within that theme, SK hynix has rallied strongly on expectations tied to HBM, or high-bandwidth memory.

Rising expectations for HBM supply into Nvidia GPUs have led the market to re-rate SK hynix as a core AI infrastructure company rather than a conventional memory manufacturer.

However, markets discount expectations in advance.

Even high-quality companies can face profit-taking after a rapid run-up.

Global investors may rotate from stocks that have already risen significantly into large technology names that still offer relative upside.

-

SK hynix and other memory semiconductor stocks posted strong gains on AI expectations earlier this year.

-

By contrast, some large-cap technology stocks had shown comparatively lower upside during parts of the rally.

-

For institutional investors, reducing exposure to names with large unrealized gains and reallocating to less extended tech leaders is a standard strategy.

-

In that process, ADRs traded in the U.S. can be the first to move sharply.

The issue is not that SK hynix has weakened operationally, but that the stock had become expensive after a strong advance.

3. Second Factor: Pressure from the SK hynix ADR Premium

The most important issue in this move is the ADR premium.

Although the ADR represents the same underlying company as the Korean listing, its market price can diverge based on U.S. demand and supply.

When U.S. investor demand is strong, the ADR can trade at a significant premium to the domestic share price.

According to the source, the premium between the SK hynix ADR and the domestic listing at one point reached as much as 50%.

This means the U.S.-traded ADR was valued far above the Korean share price on a converted basis.

The premium can be understood in three parts.

-

ADR implied price: The ADR price converted into KRW and adjusted for the ADR ratio.

-

Domestic share price: The actual SK hynix price traded in the Korean market.

-

Premium: The gap between the ADR implied price and the domestic share price.

When the premium becomes too large, the market tends to expect normalization.

That normalization can happen in two ways.

-

The domestic share price rises to close the gap.

-

The ADR falls to close the gap.

In this case, the second mechanism appears to be at work.

Rather than the Korean listing catching up, the ADR moved lower toward the domestic price.

This point is material because price dislocations can unwind more sharply than fundamental changes.

4. Third Factor: Investor Positioning and Sentiment Deteriorated

In equity markets, the most unstable conditions arise not when bad news appears, but when crowded positions begin to reverse.

Expectations for AI semiconductors, HBM, and a recovery in memory pricing had been strong throughout the year.

As a result, many investors were concentrated in SK hynix and related semiconductor names.

In that setting, even a modest sell signal can trigger broader downside.

-

Short-term valuation pressure had already increased.

-

Concerns over the ADR premium added to the pressure.

-

Selling in U.S. trading may have prompted algorithmic and short-term traders to add to the decline.

-

As U.S. and Korean investors moved in the same direction, volatility increased further.

The reference to the spread of Korean trading behavior into the U.S. market highlights the shift in sentiment.

It suggests that the concentrated, momentum-driven trading patterns commonly seen in Korea also emerged in the ADR market.

5. What the KOSPI Night Futures Decline Signaled

The source noted that KOSPI night futures fell by about 6.58%.

That figure does not necessarily translate directly into the next regular session.

However, it clearly indicates that the market was pricing in a meaningful shock.

SK hynix is one of the largest companies in the KOSPI by market capitalization.

Along with Samsung Electronics, it is a key driver of Korean equity direction.

As a result, a sharp decline in the SK hynix ADR can create immediate pressure on the KOSPI outlook.

-

Foreign investors may reduce exposure to Korean semiconductors.

-

Sentiment may spill over into the broader AI semiconductor supply chain, including Samsung Electronics, Hanmi Semiconductor, and Isu Petasys.

-

The KOSPI index may come under pressure from large-cap semiconductor weakness.

-

Currency and U.S. rate movements may amplify foreign investor sensitivity.

That said, a large decline in night futures does not always lead to an equivalent drop in the cash market the next day.

The extent of the move will depend on late-session recovery in the U.S. market, won won stability, and bargain buying.

6. The Market Concern Is Not a Breakdown in SK hynix Earnings

When interpreting this move, it is important not to conclude too quickly that SK hynix earnings expectations have collapsed.

The market’s immediate concern is valuation rather than profitability.

More precisely, the issue is the price level, the ADR premium, and crowded positioning.

HBM demand has not disappeared.

The AI server investment cycle has not ended overnight.

Expectations for a memory sector recovery remain in place.

However, stocks do not continue rising simply because the underlying story remains favorable.

Once positive news is largely reflected in price, the market begins to ask new questions.

-

How much additional earnings growth from HBM can still justify the current valuation?

-

Can the memory pricing cycle remain stronger than expected?

-

Is there a risk of slower AI investment from Nvidia-centric demand?

-

Can the SK hynix ADR premium widen again?

In other words, the key issue is no longer whether the company is strong, but whether the current price still offers sufficient upside.

7. A Key Point Often Missed in Other Coverage

The most important aspect of this event is that the narrowing of the ADR premium is not merely a pricing detail.

It signals that global investors’ valuation framework for SK hynix is being reassessed.

The Korean listing is influenced by domestic investors, foreign flows, the KOSPI, and the won.

By contrast, the ADR is more directly affected by U.S. investors, dollar liquidity, Nasdaq sentiment, and global hedge fund positioning.

Because the investor base is different, price gaps can emerge.

When the premium becomes too large, arbitrage logic tends to favor selling the expensive instrument and buying the cheaper one.

The challenge for individual investors is that this arbitrage is not always easy to execute.

-

There are exchange rate differences between the ADR and the domestic share.

-

Trading hours are different.

-

Access differs between institutions and retail investors.

-

Constraints may exist in short selling, hedging, and conversion structures.

As a result, a premium can remain elevated for some time and then unwind abruptly.

The recent SK hynix ADR decline appears consistent with that pattern.

Another important point is that this selloff does not necessarily indicate the end of the AI semiconductor cycle.

Rather, it reflects the fact that the market had priced in a very strong version of that cycle.

The stronger the theme, the more crowded the positioning becomes, and the narrower the exit becomes when sentiment reverses.

8. Key Indicators Investors Should Monitor

In a volatile market, emotional reactions are common.

However, the relevant indicators are clear.

-

ADR premium changes: Track how much the gap between the SK hynix ADR and the domestic listing has narrowed.

-

U.S. large-cap tech flows: Monitor whether capital is rotating from memory semiconductors into Apple, Microsoft, Alphabet, Amazon, and Meta.

-

Nvidia share price: Nvidia remains the center of AI semiconductor sentiment.

-

Exchange rate: A sharper move in the KRW can make foreign flows more sensitive.

-

Foreign buying in the KOSPI: Watch whether foreign investors continue to sell semiconductors or return as buyers.

-

HBM supply agreement updates: SK hynix’s medium-term value still depends on HBM competitiveness and customer demand.

Near term, price action will be driven by positioning and sentiment.

Longer term, earnings, memory pricing, AI server investment, and HBM market share will remain decisive.

9. A Practical View on SK hynix Shares

SK hynix remains a core global memory semiconductor company.

In HBM, it is viewed as a critical supplier within the AI semiconductor supply chain.

For that reason, the company’s long-term growth thesis remains intact.

However, long-term strength does not eliminate short-term correction risk.

The market is not rejecting the company’s future prospects; it is reassessing expectations that were reflected too quickly in the share price.

Investors should therefore separate two issues.

-

Business value: HBM competitiveness, AI server demand, and memory market recovery remain key drivers.

-

Share price positioning: The recent rally, ADR premium, and global capital rotation create short-term correction risk.

High-quality companies can still fall when valuations are stretched.

Even without negative news, heavily re-rated stocks can decline.

The SK hynix ADR move is a clear example of that dynamic.

10. Conclusion: This Was Primarily a Repricing Event, Not a Fundamental Breakdown

The recent SK hynix ADR decline is better understood as a repricing event than as evidence of a sudden deterioration in fundamentals.

AI-related expectations drove strong gains in SK hynix and other memory semiconductor names, while the ADR premium also expanded materially.

Subsequently, investors rotated toward large-cap technology stocks, and pressure to normalize the premium intensified, contributing to the sharp decline.

The move is a short-term negative for the KOSPI.

Because SK hynix and Samsung Electronics have large index weights, weaker semiconductor sentiment can affect the broader Korean market.

However, the decline does not by itself signal the end of the AI semiconductor cycle.

What matters now is monitoring the ADR premium, foreign flows, the exchange rate, Nvidia’s share price, and HBM earnings expectations.

Markets routinely move between excess optimism and fear.

This decline should be viewed as a strong correction within that cycle.

< Summary >

The SK hynix ADR declined primarily because capital rotated from memory semiconductors into large-cap technology stocks.

The premium between the ADR and the Korean listing had become excessive, and the decline reflects a normalization of that gap through ADR weakness.

AI semiconductor and HBM demand remain relevant, but much of that optimism had already been priced in.

The KOSPI may face near-term pressure from large-cap semiconductor weakness, although night futures declines do not always translate directly into the next cash-market session.

The main indicators to monitor are the ADR premium, foreign flows, the exchange rate, Nvidia’s share price, and HBM earnings prospects.

[Related Articles…]

- AI Semiconductor Cycle and Global Memory Stock Trends

- KOSPI Outlook and Foreign Flow Monitoring Points

*Source: [ 내일은 투자왕 – 김단테 ]

– 하이닉스 ADR 개박살난 이유 #하이닉스 #ADR #개박살

● PPI Shock, Inflation Cooldown, Fed Hold Odds Surge

[Breaking Analysis] U.S. June PPI Drops Sharply: The Real Reasons Behind the Inflation Cooling Signal and the Outlook for the July FOMC Rate Decision

The key takeaway from the June U.S. PPI release is not simply that prices declined.

Producer prices came in well below market expectations, easing concerns about a renewed acceleration in U.S. inflation and materially reducing the likelihood of another rate hike at the July FOMC meeting.

There is, however, a more important layer to this development.

The inflation slowdown likely reflects not only weaker demand, but also the combined effects of increased imports of Chinese household goods and IT components following the U.S.-China summit, as well as lower global oil prices.

In other words, U.S. inflation should be assessed not only through CPI and PPI, but also by monitoring China’s exports to the U.S., global oil prices, Middle East tensions, U.S. Treasury yields, and the dollar index.

1. Key Takeaways from the June U.S. PPI Release

According to the U.S. Bureau of Labor Statistics, the June Producer Price Index, or PPI, slowed sharply on a year-over-year basis.

In the source material, June PPI growth was cited in the 5.4% to 5.5% range, down clearly from 6.5% in the prior month.

Given that market expectations were around 6.2%, the release came in well below consensus.

Core PPI also showed further moderation.

The source material cited core PPI in the 4.7% to 5.1% range, which is significant because the market had been concerned about renewed upward pressure in core inflation.

Core PPI excludes volatile items such as food and energy and is therefore a key input in the Federal Reserve’s assessment of the inflation trend.

Overall, the release sent a clear message that inflation is cooling more than expected.

As a result, U.S. technology stocks, growth stocks, Korean equities, and risk assets more broadly are likely to interpret the data as a supportive short-term factor.

2. Why PPI Matters: A Leading Signal for CPI

PPI measures producer prices.

In practical terms, it captures changes in the costs firms face before goods and services reach consumers.

While CPI reflects the prices consumers actually pay, PPI captures wholesale prices, input costs, and upstream pricing pressure.

When PPI declines, CPI tends to follow with a lag of roughly two to three months.

Conversely, if PPI rises again, companies may pass higher costs through to consumers, putting upward pressure on CPI.

The June PPI slowdown is particularly meaningful because it followed a softer June CPI report.

U.S. CPI for June rose 3.5% year over year.

When both CPI and PPI moderate at the same time, the market naturally begins to question whether the Federal Reserve needs to raise rates further.

3. First Driver of the Inflation Slowdown: Surge in Chinese Imports After the U.S.-China Summit

One of the most important factors to monitor is the sharp increase in Chinese exports to the U.S. following the U.S.-China summit.

The source material states that exports of Chinese household goods, IT products, computer components, and semiconductors-related parts to the U.S. increased materially around the May summit.

China’s exports to the U.S. had been weak in January, February, and March, but rose 11.3% year over year in April, 35.3% in May, and 13.9% in June.

June exports to the U.S. were cited at approximately $43.5 billion, the highest level of the year.

This is more than a simple recovery in trade flows.

It likely reflects front-loading behavior, as U.S. companies accelerated shipments before tariff conditions changed.

In practical terms, this resembles preemptive inventory accumulation and tariff-avoidance shipping.

For the U.S., a larger inflow of Chinese household goods and low-cost consumer products can ease consumer price pressure.

For companies, lower prices on components, appliances, computers, and IT equipment can reduce producer price pressure.

This is likely one of the main reasons behind the June PPI slowdown.

4. A Key Point Often Overlooked: This Inflation Cooling May Reflect Supply Recovery Rather Than Weak Demand

Many reports simply describe a lower PPI as “inflation easing.”

However, the current situation requires a more nuanced interpretation.

The decline in prices may reflect a renewed inflow of low-cost Chinese goods and IT components rather than a sharp drop in U.S. consumption.

That distinction matters.

If prices decline because demand collapses, recession risk rises.

If prices decline because supply conditions improve, the impact on equities is much more constructive.

Corporate margins are better supported, consumer purchasing power is preserved, and pressure on the Federal Reserve to tighten policy is reduced.

This is also relevant from the perspective of AI infrastructure investment.

U.S. major technology firms continue to invest heavily in AI servers, data centers, semiconductor equipment, power infrastructure, and networking equipment.

If higher imports of Chinese computer and IT components reduce cost pressure, that would support the AI investment cycle.

Accordingly, the June PPI decline is not only a macro inflation story but also a factor relevant to U.S. technology stocks and the AI supply chain.

5. Second Driver: Lower Global Oil Prices Contributed to the June Inflation Cooling

Lower global oil prices also played a clear role in the June PPI and CPI moderation.

The source material indicates that stable oil and commodity prices through June helped ease inflationary pressure.

At the same time, it is important to note that oil prices did not return to pre-conflict levels.

Even if prices declined month over month, they may still remain elevated on a year-over-year basis.

Because CPI and PPI are measured year over year, a modest recent decline in oil does not mean inflationary pressure has fully disappeared.

Crude oil affects not only energy prices.

It also influences transportation costs, plastics, chemicals, fertilizers, agricultural prices, airline fares, logistics, manufacturing input costs, and a wide range of services.

In other words, oil is a fundamental input across the modern economy.

If global oil prices rise again, the inflation improvement seen this month could reverse.

6. Why Middle East Tensions Remain a Critical Risk Factor

Although the latest inflation data were favorable, the situation is not yet fully stable.

The most important variable remains the Middle East.

The source material refers to the risk of a possible Strait of Hormuz disruption, pressure on Gulf producers to invest in the U.S., and the political use of regional tensions.

The Strait of Hormuz is one of the most important global oil transit routes.

Rising tensions in the region can quickly move global oil prices.

If oil prices rise sharply again, firms’ energy costs will increase.

Over time, those costs may be passed through to consumers.

If that process intensifies, PPI would likely rise first, followed by CPI and PCE inflation.

An important point from the source material is the lag effect from inventories.

Even if oil prices spike, companies may continue using inventory purchased at lower prices, delaying the inflation impact.

Once those inventories are depleted two to three months later, firms may need to buy higher-priced oil, creating delayed inflation pressure.

A similar pattern was observed during the Russia-Ukraine war, when the energy shock reached inflation with a time lag.

7. Current Assessment of U.S. Inflation Conditions

On the surface, U.S. inflation is moving into a more stable range.

CPI has declined from its peak, and core CPI has moderated rather than reaccelerated sharply.

This latest PPI report also reduced concern about renewed inflation acceleration.

However, it is still too early to conclude that inflation is fully under control.

Energy costs remain a factor, Middle East risks have not been resolved, and the boost from higher Chinese imports may prove temporary.

If the increase in Chinese imports reflects front-loading, the inflation relief seen in May and June may fade later.

That is why July and August data will be important in determining whether this is a genuine trend.

8. Market Impact: Potential Decline in U.S. Treasury Yields and the Dollar Index

The market’s first reaction to the PPI release is likely to be in U.S. Treasury yields.

When inflation comes in below expectations, the probability of further Federal Reserve tightening declines.

As a result, the 10-year U.S. Treasury yield may face downward pressure.

The source material also notes that Treasury yields had already declined after the CPI release, with some pre-PPI rebound driven by caution, followed by renewed downward momentum after the weaker PPI print.

The dollar index could move in a similar direction.

As the likelihood of further rate hikes falls, the upward pressure on the dollar weakens.

A softer dollar would be supportive for emerging markets, the Korean won, commodities, and risk assets.

Technology stocks would also benefit.

When yields fall or rate-hike expectations diminish, the present value of future earnings rises, which tends to support growth stocks and AI-related equities.

9. CME FedWatch: Higher Probability of a July FOMC Hold

According to the source material, before the PPI release, CME FedWatch already showed a high probability of a policy hold.

After the PPI report, the probability of holding rates steady rose to around 90%.

This means the market sees a July rate hike as highly unlikely.

Of course, the Federal Reserve considers not only CPI and PPI, but also employment, wages, consumption, PCE inflation, and financial conditions.

Still, with both CPI and PPI moderating, additional tightening would be difficult to justify.

The U.S. policy rate is already at a relatively high level.

In that sense, the Fed can maintain a restrictive stance even without another hike.

This is one reason the policy backdrop differs from Korea’s.

10. Difference Between U.S. and Korean Monetary Policy

The U.S. has kept rates high without cutting aggressively.

As a result, even with CPI in the mid-3% range, the Federal Reserve may still judge policy to be sufficiently restrictive.

The situation is different in Korea if policy rates have already been lowered materially.

If inflation in Korea returns to the mid-3% range, the Bank of Korea may face pressure to hold rates steady or reconsider tightening.

This difference should be viewed through the lens of real interest rates.

The real policy rate is the nominal rate minus inflation.

If real rates remain sufficiently positive, a central bank may not need to tighten further.

But if real rates are low or near zero, stronger policy action may be required to contain inflation.

11. Upcoming Key Dates: July FOMC and Bank of Korea Policy Meeting

According to the source material, the FOMC meeting is scheduled for 3:00 a.m. Korea time on July 30.

The consensus view is that the Fed will likely hold rates steady.

More important than the rate decision itself will be the Fed’s messaging.

If the Fed says that inflation is clearly moderating, markets may begin to price in a future rate cut.

If it emphasizes the need to monitor energy prices and Middle East tensions, expectations may be adjusted again.

The Bank of Korea’s monetary policy meeting is also important.

The Bank of Korea must consider U.S. policy, the won-dollar exchange rate, domestic inflation, household debt, and the property market simultaneously.

Even if the Fed holds steady, the Bank of Korea may not be in a position to ease quickly.

12. Key Data to Watch Next: PCE, Oil, China Exports, and U.S. Employment

Following the PPI release, the market’s attention will shift to the next set of inflation indicators.

The Federal Reserve’s preferred inflation gauge is the PCE price index.

Core PCE is especially important for assessing the rate outlook.

Four key data points should be monitored going forward.

First, July and August PCE inflation.

The key question is whether the moderation in CPI and PPI is reflected in personal consumption expenditures data.

Second, global oil prices.

If Middle East tensions escalate and oil prices rise again, the inflation cooling scenario could weaken.

Third, China’s export flow to the U.S.

It remains to be seen whether the increase in low-cost Chinese goods and IT component imports continues or fades after front-loading ends.

Fourth, U.S. employment and wage growth.

Even if inflation cools, persistent wage growth could keep services inflation sticky.

13. Market Implications for Investors

The June PPI slowdown is short-term positive for risk assets.

If U.S. Treasury yields fall and the dollar weakens, the Nasdaq and S&P 500 are likely to benefit.

Korean equities may also see improved sentiment, particularly in semiconductors, batteries, AI infrastructure, and growth stocks.

That said, investors should avoid excessive optimism.

If the recent inflation relief depends heavily on supply-side factors such as higher Chinese imports and lower oil prices, market sentiment could reverse quickly if those variables change.

In particular, a renewed spike in oil prices could bring stagflation risk back into focus.

Stagflation refers to a combination of slowing growth and rising prices.

In that environment, central banks find it difficult to cut rates, and corporate earnings expectations deteriorate, making it one of the most difficult settings for equities.

14. Conclusion: Inflation Has Eased, but the Trend Is Not Yet Fully Settled

The June U.S. PPI clearly provided relief to the market.

Following the softer CPI print, the lower-than-expected PPI reading significantly reduced concerns about a renewed inflation surge.

The probability of a July FOMC rate hold also increased materially.

However, the underlying drivers of the inflation slowdown should be examined carefully.

The decline likely reflects not only softer U.S. demand, but also increased Chinese imports, tariff expectations, front-loading, and lower oil prices.

Going forward, the key issues are whether China’s exports to the U.S. remain elevated, whether oil prices avoid another sharp increase, and what signal the Federal Reserve sends at the July FOMC meeting.

The market has valid reasons to react positively.

At the same time, investors should continue monitoring oil prices, Middle East tensions, PCE inflation, and U.S. Treasury yields.

< Summary >

The June U.S. PPI came in well below both the prior reading and market expectations, signaling a clear cooling in inflation.

Following softer CPI data, the June PPI release materially increased the likelihood that the Federal Reserve will hold rates steady at the July FOMC meeting.

The inflation slowdown appears to reflect not only weaker demand, but also a surge in Chinese imports of household goods and IT components, along with lower global oil prices.

However, if Middle East tensions intensify and oil prices rise again, PPI and CPI could reaccelerate.

Going forward, investors should monitor PCE inflation, China’s exports to the U.S., U.S. Treasury yields, the dollar index, and global oil prices.

[Related Articles…]

U.S. Inflation Cooling and the Fed Rate Outlook

Oil Prices and the Risk of Reaccelerating Inflation

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [속보] 미국 6월 PPI 물가 크게 하락… 아직 물가 안정적인 이유 [즉시분석]