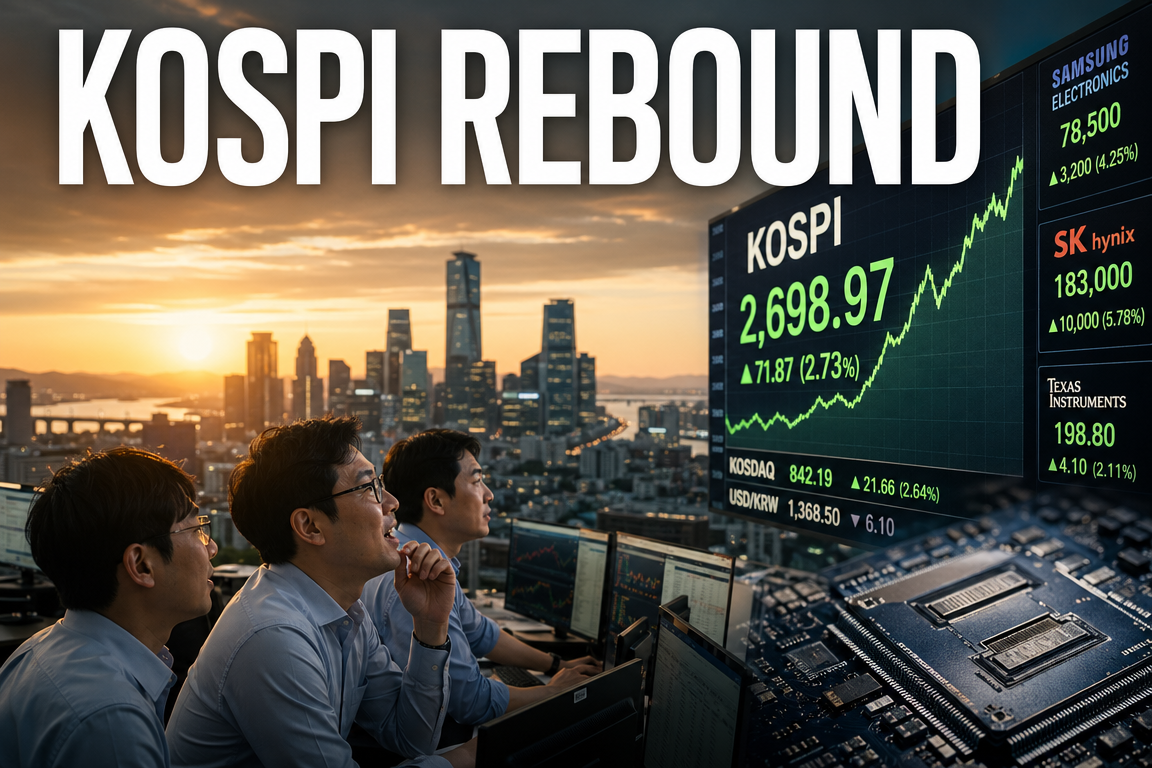

● Middle East War Ends, Korea Stocks Surge, Real Shock Is Oil, Inflation, Rates

Will Korean Equities Rally Sharply After a Middle East War Ends? The Key Variables Are Beyond the War Itself

This development is not well explained by the Middle East war alone. The primary drivers for Korean equities are the war’s second-order effects on inflation, rates, and supply chains.

Key coverage:1) Why Korean equities are not moving identically to the 2022 Russia-Ukraine episode

2) The transmission link between crude oil, inflation, and US long-term yields (news-style framing)

3) Scenario analysis for the KOSPI under early resolution vs. prolonged conflict

4) Underappreciated risk factors: private credit, SaaS deterioration, and redemption gates

5) Post-war themes: reconstruction demand, AI infrastructure, data centers, semiconductors, and energy modernization

Core point: The market impact depends less on whether the war ends and more on how FX (USD/KRW), crude oil, and the US 10-year yield respond.

1. Executive News Summary

The war has contributed to volatility in Korean equities, but the medium-term direction is more likely to be driven by inflation, interest rates, and supply-chain disruptions arising from the conflict.

Priority indicators:

- International crude oil prices

- US 10-year Treasury yield

- CPI and inflation trajectory

The key question for investors:

- Not “how severe is the war,” but “how much does it re-accelerate inflation, and does it alter central-bank policy paths?”

The 2022 drawdown was driven less by the war headline and more by surging inflation and rapid Federal Reserve tightening.

2. Why Korean Equities Were More Sensitive

Korea (and Japan) reacted more sharply due to structural exposure:

- Energy-intensive manufacturing economies

- High dependence on Middle East crude

Korea’s manufacturing-heavy structure amplifies the transmission from higher oil prices to production costs, logistics, import prices, and margins. If combined with a weaker KRW and higher shipping rates, the cost shock becomes multi-layered.

Mechanism:

- Higher crude oil → higher corporate input costs

- Weaker KRW → higher import prices and energy costs

- Higher ocean freight → higher supply-chain costs

3. Why This Is Not a Repeat of 2022

3-1. In 2022, inflation was already near a breakout

The Russia-Ukraine war compounded pre-existing inflation pressure from 2020–2021 liquidity expansion and demand normalization. Oil spiked, inflation surged, and the Fed responded with aggressive tightening.

Core 2022 mix:

- War shock + elevated inflation baseline + delayed and then abrupt tightening

3-2. The current regime is disinflation

Inflation has been trending down from its peak. While price levels remain high, markets focus more on the direction of inflation than its absolute level. This reduces the likelihood of a rapid return to extreme inflation prints, absent a sustained oil shock.

3-3. Lower probability of a repeat policy error

Compared with 2022, central banks are more attuned to separating supply-driven from demand-driven inflation. Even with higher oil, a reflexive return to aggressive hikes is less likely, though not impossible.

4. The Three Primary Market Variables

4-1. International crude oil

If the conflict persists, oil is typically the first major variable to react. Any escalation tied to the Strait of Hormuz increases supply-risk premia, feeding into inflation and corporate costs. For Korea, oil is a top-level equity driver rather than a peripheral commodity input.

4-2. Inflation

The direct shock from war headlines can fade, but sustained supply-chain disruption and higher energy prices can re-ignite inflation. Inflation affects both policy rates and equity valuation simultaneously.

4-3. US 10-year Treasury yield

The US 10-year yield functions as a composite market signal, rapidly reflecting oil, inflation expectations, and policy pricing. The absence of a sharp long-end spike (vs. 2022) is one reason risk assets have avoided a deeper disorderly selloff. Investors should monitor the 10-year yield more than headlines.

5. Scenario Analysis: Korea Equity Pathways

5-1. Early resolution

A meaningful relief rally is plausible as risk aversion eases and the market refocuses on:

- Semiconductor cycle improvement

- Continued AI capex

- Korea’s value-up agenda

Potential breadth expansion:

- Mega-cap semiconductors (e.g., Samsung Electronics, SK Hynix)

- Low PBR re-rating candidates

- Dividend and buyback/buyback-cancellation beneficiaries

Interpretation: with reduced geopolitical risk premia, the market tends to revert to its prior fundamental narrative.

5-2. Conflict extends into April/May and beyond

Prolongation increases the probability that financial stress translates into real-economy drag:

- Higher commodities

- Higher freight

- Persistent supply friction

For Korea’s manufacturing base, this can pressure earnings and widen the valuation headwind from rates, potentially deepening the equity adjustment via lower profit estimates and higher discount rates.

5-3. Adverse prolonged scenario

If oil remains elevated for an extended period, supply disruption intensifies, and inflation re-accelerates toward the 3–5% range:

- Fed and Bank of Korea easing could be delayed

- Tightening risk could re-enter pricing

Under this regime, the KOSPI’s upward path could be interrupted.

6. Supply-Chain Shock: Potentially More Material Than Price Levels

The primary risk in a prolonged conflict is not only “higher prices,” but “unavailable inputs.”

Vulnerable categories can include:

- Semiconductors and semiconductor materials

- Autos and precision chemicals

- Industrial gases (including helium) and other region-concentrated inputs

If shipping lanes are disrupted, air routes constrained, or chokepoints closed, production continuity becomes the binding constraint. Firms may raise inventories, structurally increasing working capital needs and reducing efficiency. This can represent a longer-duration rise in global cost structures.

7. Why Private Credit, SaaS Stress, and Redemption Gates Matter

An additional axis is US private credit, which may be underweighted due to geopolitical focus but remains relevant as an internal financial-system stressor.

7-1. Why private credit expanded

After 2008, regulated banks reduced risk lending. Lower-rated or private firms increasingly relied on private credit and private-fund lending structures. This has supported funding for growth companies and mid-sized corporates.

7-2. The problem: opacity and redemption constraints

Unlike public credit markets, disclosures are limited and exposures are difficult to map. If redemption requests rise, funds may face liquidity mismatches and can impose redemption gates, which can amplify investor concern.

7-3. Why SaaS/software is highlighted

With AI agent adoption and valuation resets, parts of the software universe face sharper repricing. Because some issuers relied on private credit, refinancing and repayment capacity is under scrutiny. The sector’s prior high valuations can magnify downside during re-rating.

7-4. Systemic crisis risk

A 2008-style systemic event is generally assessed as less likely at present, given broader recognition of the issue and ongoing efforts to limit direct contagion to core banks. The more probable outcome is a managed-credit deterioration rather than an unrecognized shock.

8. Post-War Upside Themes for Korean Corporates

Post-conflict activity in the region may resemble modernization-scale investment rather than simple restoration.

8-1. Energy infrastructure reconstruction

Fast restoration demand may emerge across:

- Refining, petrochemicals, storage

- Power generation and related infrastructure

Korean firms’ competitive advantages include EPC execution track record and delivery reliability, which are often decisive in regional procurement.

8-2. AI data-center buildout and expansion

The conflict has reinforced the strategic importance of digital infrastructure. A likely pathway is combined investment in AI data centers and power infrastructure.

Potential Korean beneficiary areas:

- Semiconductors

- Power equipment and grid solutions

- Cooling systems

- Telecom infrastructure

- Batteries

- Nuclear and SMR-adjacent technologies

8-3. Energy modernization integrated with AI

Reconstruction may incorporate AI-enabled forecasting, grid optimization, and smart operations rather than replicating legacy assets. Korea’s strengths in manufacturing data, automation, and communications infrastructure may be relevant.

9. Portfolio Positioning Principles

9-1. Avoid reactive short-term trading on war headlines

Geopolitical outcomes are inherently difficult to forecast and are frequently mispriced in real time.

9-2. If no clear single-name edge, index exposure is a valid approach

In high-volatility regimes, frequent sector rotation can underperform broad benchmarks. Diversified exposure via core indices can be an efficient default.

9-3. Equity ownership as partnership underwriting

Equities represent participation in underlying businesses. Macro shocks rarely eliminate viable business models overnight. Investment selection should prioritize business durability and investor understanding.

10. Why Domestic Policy Matters for Korean Equities

Korea’s value-up agenda is a potential structural catalyst:

- Re-rating pressure on low PBR names

- Greater emphasis on buyback cancellation and dividends

- Broader shareholder-value and governance initiatives

While policy alone does not sustain an equity bull cycle, it can reduce persistent “Korea discount” dynamics, particularly during global risk-off episodes.

11. Underemphasized Points That Matter Most

- War risk is most damaging when it changes the inflation and rate trajectory

- Korea is structurally more exposed due to energy dependence and manufacturing intensity

- The US 10-year yield is a more actionable real-time signal than headlines

- Private credit and SaaS stress are additional latent financial variables

- Post-war reconstruction may center on AI infrastructure and energy modernization, not only physical repair

12. Practical Monitoring Checklist

- International crude oil trend

- US 10-year Treasury yield

- US CPI and inflation expectations

- USD strength and USD/KRW

- Ocean freight rates and supply-chain disruption signals

- Semiconductor cycle indicators and continuity of AI capex

- Follow-through on Korea’s value-up policy measures

Markets respond to quantified variables more than narratives; rates and FX often transmit the earliest change in risk conditions.

< Summary >

The war has affected Korean equities, but the dominant drivers are crude oil, inflation, and interest rates. Unlike 2022, the current regime is broadly disinflationary, reducing the likelihood of an identical drawdown. If the conflict persists and oil/supply-chain shocks accumulate, the KOSPI path can weaken via earnings downgrades and rate repricing. If resolved early, semiconductors, low PBR re-rating, value-up policy, and AI infrastructure themes may reassert, supporting a rebound. Additional monitoring is warranted for US private credit, SaaS stress, and redemption-gate risks. Post-war reconstruction may create opportunities in energy infrastructure, modernization, and AI data-center expansion where Korean firms have established execution advantages.

[Related Links…]

- KOSPI rebound signals and foreign flow shifts: https://NextGenInsight.net?s=KOSPI

- How expanded AI infrastructure investment affects Korean semiconductors: https://NextGenInsight.net?s=AI

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [모아보기] 중동전쟁 끝나면 한국증시 급반등하나… 2022년과 다른 지금, 시장을 흔드는 진짜 변수 3가지 | 경읽남과 토론합시다 | 김학균 센터장x나탈리 허 변호사

● Trump Shooting Fallout, Oil, Rates, AI Rally

Equity Market Outlook After the Failed Attempt on Trump: The Key Drivers Are Oil, Rates, and the AI Rally, Not US Political Risk

This event is often simplified as “failed assassination attempt = market shock,” which can obscure the primary market drivers. Current price action appears more sensitive to Middle East-driven oil upside, potential inflation re-acceleration, changes in the Federal Reserve’s rate path, and renewed risk appetite centered on AI semiconductors and the space industry. This report summarizes the transmission channels to US equities, Nasdaq, KOSPI, the USD, rates, and crude, and highlights key points that are often underemphasized.

1. Why the Market May Remain Relatively Composed

While politically significant, the incident is not easily interpreted as an immediate systemic financial risk. Three considerations matter:

First, the event is being treated primarily as an extension of domestic US political and social polarization rather than direct foreign-state involvement. This reduces the probability of an immediate escalation into broad geopolitical conflict.

Second, rapid crisis communication from Trump likely dampens near-term escalation narratives. The absence of an immediate push for an Iran-backed storyline may also reduce short-term uncertainty.

Third, prior episodes suggest such events can consolidate Trump’s political standing and base. Markets may interpret this less as “higher regime uncertainty” and more as “greater probability of Trump’s political consolidation,” which can increase policy visibility.

Overall, the headline risk is high, but the near-term probability of a Nasdaq drawdown driven solely by this event or a US Treasury market “panic” appears limited.

2. News-Style Summary: Key Market Variables to Monitor

2-1. Politics

- Trump is more likely to emphasize a unifying message than an immediate retaliation framework.

- Ahead of elections, a combined “victim” narrative and “unity” positioning could support polling.

- If investigations become strongly associated with a particular political ideology, US polarization may intensify further.

2-2. Foreign Policy

- US-Iran diplomacy may become more difficult.

- Heightened focus on executive security can reduce diplomatic flexibility.

- Even if negotiations resume, internal divergence between Iran’s civilian leadership and military/security apparatus may limit implementation credibility.

2-3. Equities

- Near term, the dominant drivers remain the AI semiconductor rally, space-industry momentum, and earnings expectations rather than US political headlines.

- Strength in CPU-linked names (e.g., AMD, Intel) indicates AI capex is broadening beyond GPUs into CPUs, servers, cooling, and optical networking.

- Korean equities may remain supported, led by KOSPI heavyweights and semiconductors.

2-4. Macro

- The primary variable is not the incident itself but oil upside risk from persistent Middle East tension.

- Higher oil prices can re-stimulate inflation, weakening expectations for Fed easing.

- The key macro determinant is the crude-to-inflation path and its impact on the rate trajectory.

3. Why the Event Could Be Politically Supportive for Trump

Markets focus less on the shock value and more on how the event changes electoral odds and policy direction.

Trump has historically used crisis moments to reinforce symbolism and consolidate support. A similar pattern is plausible, particularly if messaging emphasizes unity over retaliation, potentially improving both base consolidation and centrist appeal.

For markets, stronger political positioning can raise perceived policy predictability. Not all uncertainty is negative; clearer direction can be priced as market-supportive even amid elevated headline risk.

4. US-Iran: Three Practical Paths

A limited set of feasible outcomes frames oil, USD, rates, and equity market sensitivity.

4-1. Scenario 1: Full-Scale War or Expanded Ground Conflict

Low probability.

The military and political costs for a ground-conflict trajectory are high, including operational complexity, logistics, potential US casualties, and domestic political constraints. Markets have limited need to price an immediate “full-scale war” baseline.

4-2. Scenario 2: Diplomatic Agreement

Possible but difficult.

Iran is unlikely to relinquish nuclear-linked capabilities easily; Israel is unlikely to accept a settlement that leaves a structural threat; the US may seek an intermediate compromise.

Objectives diverge:

- Iran: regime security and retention of strategic assets

- Israel: removal of structural threats

- US: escalation containment, energy stability, and diplomatic deliverables

Even if reached, an agreement may not provide a strong or durable stability signal to markets.

4-3. Scenario 3: Maritime Interdiction and Prolonged Economic Pressure

Potentially the most probable path.

This approach pressures Iran’s funding channels and oil-export routes while avoiding direct large-scale conflict. The key variable is China: disruption of Iranian crude flows can tighten China’s energy balance, potentially shifting Beijing’s posture from endurance to resolution.

Maritime pressure is not only Iran-focused but can indirectly pressure China. This is generally less market-friendly because it can persist and keep oil risk premia elevated.

5. Equity Market Response: Separate the Near Term From the Medium Term

5-1. Near Term: Limited Shock Potential

Markets may treat the event as headline risk rather than a primary trend breaker.

Current risk assets are supported by strong internal momentum:

- AI semiconductor theme broadening

- US mega-cap tech strength

- expanding space-industry expectations

- improving earnings outlook

AI investment is transitioning from a GPU-centric phase to broader infrastructure exposure, including CPUs, servers, power, cooling/thermal management, networking, optical components, and memory. This breadth suggests sustained underlying risk appetite.

Accordingly, a single political headline is less likely to reverse the broader rally on its own.

5-2. Medium Term: Oil and Inflation as the Core Risk

The risk profile shifts if Middle East tension persists and maritime pressure continues.

A plausible chain is:oil upside -> CPI re-acceleration -> delayed Fed cuts or renewed “higher-for-longer” pricing -> valuation pressure.

If realized, this path can reinforce USD strength and increase stress on emerging markets, including KOSPI, via tighter financial conditions and foreign flow volatility.

Thus, markets may appear resilient initially, but the critical risk can arrive with a lag as inflation data confirm pass-through.

6. Dominant Themes: AI Semiconductors and the Space Industry

A key observation is that industrial fundamentals can outweigh political headlines.

6-1. AI Semiconductors

The market is not solely focused on Nvidia. Relative strength in AMD and Intel suggests AI infrastructure spending is diffusing across the stack.

Key linked segments:

- CPUs

- data center servers

- power infrastructure

- immersion cooling and thermal management

- optical networking and network equipment

- memory semiconductors

This broadening can affect not only US equities but also Korean exports and related KOSPI exposures across memory, advanced packaging, materials, and equipment.

6-2. Space Industry

Often viewed as a speculative theme, the space sector is increasingly linked to concrete industrial restructuring.

Price action in US space-related equities and ETFs, alongside expectations tied to SpaceX and broader commercialization, signals renewed market attention.

The investment case extends beyond launch vehicles into:satellite communications, defense, high-precision mapping, climate observation, autonomous-driving infrastructure, and data networks, with meaningful intersections with AI.

This implies major technology themes are increasingly interconnected rather than trading as isolated sectors.

7. Key Considerations for Korean Investors

7-1. KOSPI

In the near term, US tech strength can support Korean semiconductors. If AI server and semiconductor supply chains remain strong in the US, expectations for Korean memory, packaging, materials, and equipment names may improve.

7-2. FX and the USD

However, oil-driven inflation risk and reduced probability of near-term Fed easing can support USD strength. A stronger USD can amplify volatility in foreign flows and limit the pace of domestic equity upside.

7-3. Asset Allocation

A balanced approach is relevant:

- offensive exposure: AI and space-related growth themes

- defensive exposure: energy sensitivity hedges, USD exposure, and selective cash allocations

8. Underemphasized but High-Impact Points

8-1. Markets Often Fear Energy Prices More Than Political Events

Headline coverage focuses on the incident itself, but markets prioritize how oil affects CPI and how that, in turn, influences the duration of restrictive policy.

8-2. Maritime Pressure Targets Iran and Indirectly Pressures China

This linkage is often under-discussed. If China’s energy security is stressed, Middle East risk and US-China rivalry can become more correlated rather than independent.

8-3. The Current Tape May Be “Bad-News Insensitive”

Strong liquidity and momentum in AI and space themes can mute short-term drawdowns from political headlines. Assuming “bad news must equal immediate downside” can lead to positioning errors in momentum-driven regimes.

8-4. The Primary Risk May Be a Delayed Shock

A lack of immediate selloff does not remove risk. The more likely pathway is delayed:oil -> inflation -> higher-for-longer rates -> valuation compression.

Accordingly, markets should be monitored through data, not headlines, with particular attention to CPI, inflation expectations, oil, and long-end yields.

9. Calendar and Data to Track

- US CPI releases

- crude oil trend and shipping/freight rate changes

- shifts in Fed communication

- status of Iran-related negotiations

- Trump polling and election dynamics

- AI semiconductor guidance and earnings

- US space-sector IPO and policy developments

These inputs will clarify whether the incident remains primarily a political headline or evolves into a macro driver via oil and rates.

10. Conclusion: Emphasize Structure Over Sentiment

The incident is politically significant, but market pricing is driven by transmission mechanisms.

Near term, equities may remain supported by AI-led tech strength and space-industry momentum, and the Nasdaq/semiconductor-led rally may prove resilient.

Medium term, the dominant constraint is whether oil sustains higher levels and re-accelerates inflation, thereby shifting the Fed’s expected easing path.

The critical framework is the linkage:politics -> foreign policy -> oil -> inflation -> rates -> equities.

< Summary >

- The event has high headline impact but limited likelihood of immediate equity downside on its own.

- Markets remain more focused on AI semiconductors, the space theme, and US tech leadership.

- The central macro risk is oil-driven inflation and a corresponding shift in the Fed rate path.

- Practical US-Iran outcomes include: (1) full-scale conflict (low probability), (2) partial diplomatic compromise (difficult), and (3) prolonged maritime/economic pressure (higher probability).

- Maritime pressure can affect not only Iran but also China via energy supply stress, increasing geopolitical complexity.

- Near term, Nasdaq and semiconductors may stay supported; medium term, oil and CPI are likely to be decisive.

[Related Articles…]

- AI Semiconductor Supercycle: Will It Extend Through 2026? (NextGenInsight.net?s=AI)

- Delayed US Rate Cuts: Implications for Korean Equities (NextGenInsight.net?s=Rates)

*Source: [ Jun’s economy lab ]

– 트럼프 암살 실패 증시는 어떻게 될까?