● Rate Shock, Trust Crack, Dollar Jolt

Warning from a Former Deputy Governor of the Bank of Korea: What the Sovereign Yield Shock Really Means

What is destabilizing is not only rates, but confidence in money.

Recent market conditions suggest more than a routine increase in sovereign yields. Three points are central:

1) The surge in long-term US yields reflects not only inflation concerns but also bond market supply-demand dynamics and rising real yields.

2) Geopolitical energy-price risk and the AI investment boom are jointly pushing long-term yields higher, weakening the explanatory power of a conventional business-cycle framework.

3) While conditions do not yet indicate a systemic financial crisis, market expectations for monetary stability are deteriorating.

This report summarizes why long-term yields have re-emerged as a core macro variable and how they link to FX, inflation, AI capex, and leadership transitions at the Federal Reserve and the Bank of Korea.

1. Why interest rates have again become the primary market variable

In recent years, KRW-USD dynamics were often the most sensitive indicator for Korea due to import prices, cross-border flows, and risk sentiment. Recently, long-term sovereign yields have moved to the forefront.

Long-term yields embed expectations for future inflation and growth, fiscal burden, monetary credibility, funding demand, and risk premia. Rapid repricing therefore signals a reassessment of future purchasing power and financial order, not merely a near-term policy-rate adjustment.

2. News-style brief: what is happening in sovereign yields

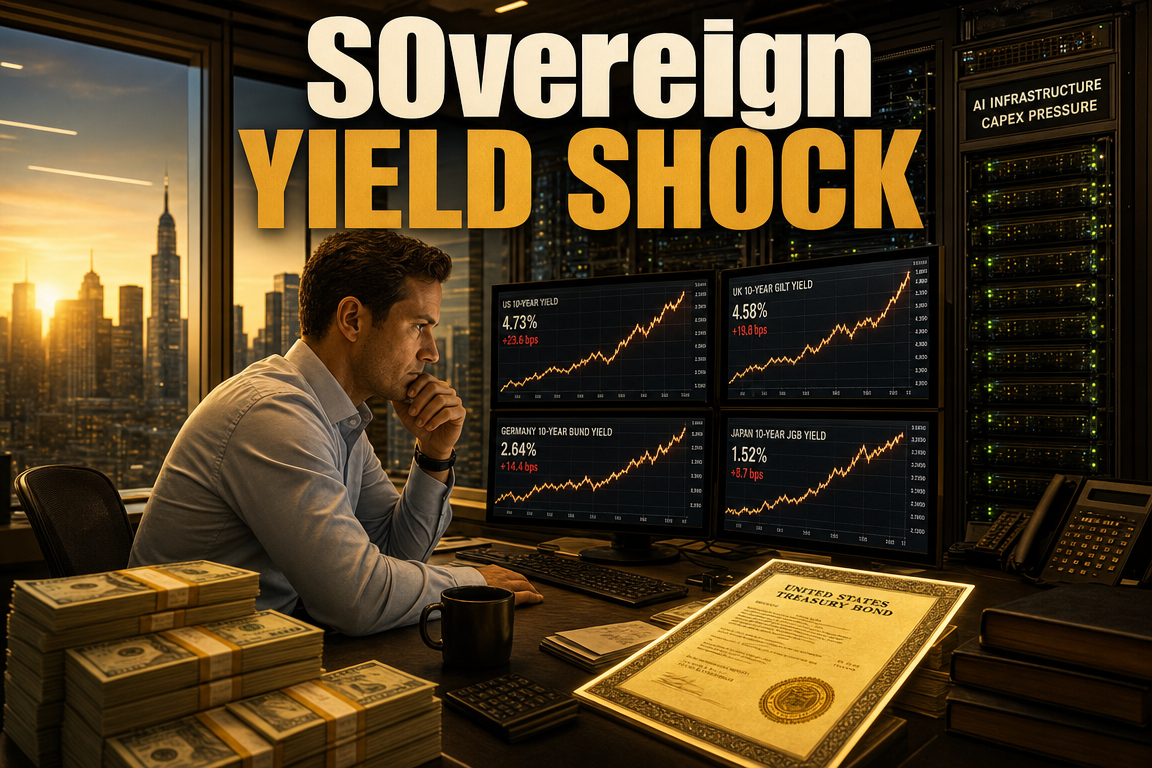

2-1. Why the US 10-year yield above 4.5% is treated as a threshold

Markets have viewed 4.5% on the US 10-year as a key psychological and technical level. Above this range, equity valuation pressure increases as the discount rate rises, elevating volatility across risk assets. The repeated pattern of equity relief when yields stabilize underscores that long-term rates are functioning as a system-wide risk benchmark.

2-2. Why Japan’s rates must be monitored alongside US yields

This episode cannot be assessed solely through the US lens. Japan’s long-term yields have risen meaningfully versus prior regimes, with direct implications for global capital flows. Higher Japanese yields can affect US Treasury demand, FX volatility, and Asian financial stability through adjustments to yen-funded carry positions. US yield repricing therefore also signals broader shifts in global funding and positioning.

3. Why yields are rising: two primary drivers

3-1. Driver 1: renewed inflation expectations

Prolonged Middle East instability has increased oil-price sensitivity, with potential spillovers from energy into transportation, production costs, and broader consumer prices. Because energy prices are highly visible to households, they can lift inflation expectations quickly. If shocks persist, inflation can broaden from a narrow energy impulse into more generalized price pressures, increasing the burden on central banks to re-anchor expectations and amplifying long-end rate sensitivity.

3-2. Driver 2: bond supply-demand imbalance and rising real yields

Inflation expectations alone do not explain the move. More fundamental is the supply-demand balance for sovereign bonds and the rise in real yields.

With expanding fiscal deficits, the US continues large-scale Treasury issuance, increasing the market’s absorption requirement and raising term premia. At the same time, structural demand from traditional buyers appears less stable than in prior cycles, influenced by reserve management, FX intervention needs, and shifts in global reserve allocation.

Real yields are not only “inflation-adjusted yields”; they also reflect the economy-wide intensity of borrowing demand. When both governments and private firms increase funding needs, market rates tend to rise. Current conditions indicate concurrent public and private demand pressures.

4. Why this rise is more consequential: AI capex may raise the neutral rate

A critical risk is that AI-related investment may structurally increase real-economy funding demand. Corporate spending is accelerating across semiconductors, data centers, power infrastructure, networks, cloud capacity, cooling systems, software stacks, and talent acquisition. This resembles a multi-year capex cycle rather than a short-lived theme.

If capital demand remains structurally elevated, the neutral rate (the rate consistent with stable inflation and full employment) could be higher than in the pre-pandemic era. This challenges the prevailing assumption that rates will revert to a low regime once inflation cools, and it increases the probability that long-term yields remain elevated for longer.

5. Not a financial crisis yet, but complacency is premature

5-1. Why conditions look closer to “financial instability” than “financial crisis”

The assessment is that current long-term yield repricing is a significant warning signal but not yet a systemic crisis. Typical crisis dynamics involve dysfunction in short-term funding markets, a collapse in interbank trust, and an abrupt surge in risk premia. These indicators have not yet displayed crisis-level stress.

5-2. Why the move is still dangerous: real-economy-driven upward pressure

Risk is elevated because the increase may be rooted in structural, real-economy forces rather than transient panic. Oil risk, fiscal deficits, AI capex, supply-chain restructuring, and geopolitical risk can jointly lift funding demand. Such pressures are difficult to reverse through communication alone, increasing the likelihood that markets interpret the shift as a higher-rate regime change.

6. Why “confidence in money” is the core issue

Rates, FX, and inflation are all prices of money: the cost of money, the external price of money, and the purchasing power of money. A combination of rising sovereign yields, FX volatility, broader inflation risk, and higher asset-price volatility can be interpreted as instability in money’s expected value.

Confidence has not collapsed, but it weakens when market participants begin to question future purchasing power, long-duration asset safety, and the central bank’s ability to re-establish stability. That questioning itself is an early-stage erosion of credibility.

7. The central bank’s role: safeguarding monetary credibility

A central bank’s function extends beyond setting policy rates. Its core mandate is to preserve purchasing power and ensure continued confidence in the currency.

- If inflation rises materially, tightening is required to restore credibility.

- If growth deteriorates sharply, liquidity provision prevents funding blockages.

- If market functioning is impaired, stabilization tools are used to protect system trust.

In this context, central banks serve as institutional anchors for the monetary order.

8. How to interpret leadership changes at the Fed and the Bank of Korea

8-1. Institutions are generally resilient to leadership change

Leadership transitions matter, but central banks operate within highly institutionalized frameworks: committee decision-making, internal research processes, market scrutiny, and disciplined communications. Policy shifts typically occur gradually.

8-2. Why leadership still matters: the policy “bias” can change

Leadership influences priorities and the framing of policy trade-offs. Changes in balance-sheet strategy, liquidity facilities, and views on financial conditions can alter how markets interpret the same rate decision. If future Fed leadership places greater weight on system restructuring, balance-sheet reduction, and reduced financial-sector dependence, global liquidity could tighten relative to prior regimes, affecting USD liquidity, Treasury demand, and emerging-market conditions.

9. Key monitoring points for Korean investors and wage earners

9-1. Monitor long-term yields ahead of equities

Equities are often downstream of rates. Growth and technology stocks are particularly sensitive to long-term yields. Even with strong AI narratives, faster increases in discount rates can pressure valuations. Track the US 10-year yield, real yields, and inflation-expectation indicators in parallel.

9-2. Track FX and sovereign yields together

In a highly open economy, FX and long-term yields are linked. Higher US long-term yields can support USD strength, increasing KRW depreciation pressure and foreign outflow risk, tightening domestic financial conditions.

9-3. Treat AI as a structural funding shift, not only an equity theme

AI is expanding capex across power, semiconductors, data centers, networks, cooling, security, and industrial automation. The macro implication is a potential shift in long-term rates and capital allocation, not merely sector rotation.

10. Under-discussed but material points

10-1. The core may be structural money demand, not only “tightening fear”

Common commentary focuses on delayed rate cuts due to inflation. A more consequential angle is that both public and private sectors are increasing funding needs simultaneously, supporting a structurally higher long-end yield profile.

10-2. AI is both a productivity force and an upward rate pressure in the build-out phase

AI may eventually be disinflationary through productivity gains, but the near-term sequence is heavy up-front investment. Before productivity benefits materialize, capex can raise real funding demand and support higher real yields.

10-3. Confidence erodes through prolonged volatility, not only extreme crises

Monetary confidence can weaken gradually when long-term yields spike repeatedly, FX remains unstable, living costs broaden, and asset prices remain highly volatile. Central banks manage expectations and credibility, not only realized data.

11. Forward-looking framework: five variables to watch

1) Whether the US 10-year yield stabilizes above 4.5%

2) Whether oil-driven inflation expectations broaden into core inflation

3) Whether AI-related capex continues to lift real yields

4) Whether Japanese yields and JPY dynamics reshape global capital flows

5) Whether the Fed and the Bank of Korea succeed in stabilizing expectations via communication and policy consistency

This is not a single-variable rate story. Inflation, fiscal dynamics, AI capex, FX, and central-bank credibility are interacting concurrently. Monitoring should focus on the re-pricing of money’s value and the durability of policy credibility, rather than reacting to any single headline.

< Summary >

The current rise in sovereign yields reflects not only inflation risk but also expanding fiscal deficits, increased issuance and supply pressure, and AI-driven capex that may lift real yields. While conditions do not yet indicate a systemic crisis, the move can be interpreted as an early signal of weakening confidence in monetary stability. AI should be analyzed as a driver of long-term funding demand that can influence the rate regime. Investors should monitor long-term yields, FX, oil and inflation expectations, and central-bank leadership and communication jointly.

[Related Articles…]

- AI investment expansion and its impact on long-term yields: https://NextGenInsight.net?s=AI

- Prolonged FX instability and potential impacts on Korea: https://NextGenInsight.net?s=FX

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 한국은행 부총재(전)의 경고, 국채금리 발작… 돈의 신뢰가 흔들리고 있다 | 경읽남과 토론합시다 | 이승헌 교수 [1편]