● Micron Shock Hits Big Tech, Nasdaq Slips

A New Bearish Narrative That Shook the Nasdaq: Why Strong Micron Results Turned Into a Negative for Big Tech

The key issue in this market was not simply that the Nasdaq declined.

What mattered was that the index reversed sharply intraday despite positive catalysts, including strong Micron earnings, softer inflation data, and continued enthusiasm around AI semiconductors.

More importantly, the market is beginning to view Big Tech not only as an AI growth play, but increasingly as an AI cost burden.

Rising memory prices, data center investment pressure, Apple’s price increases, falling GPU rental rates, and the progress of Chinese AI models are now converging into a new risk factor for U.S. equities.

1. Why Today’s Market Action Was Unusual: Good News Failed to Lift the Nasdaq

At the open, sentiment was constructive.

Micron’s earnings exceeded expectations by a wide margin, and the PCE inflation report was also more favorable than forecast.

Under normal conditions, this combination would support gains in the Nasdaq, semiconductors, and large-cap technology stocks.

- The Nasdaq rose more than 2% early in the session.

- It then reversed and fell to around 0.43% lower.

- The Dow Jones Industrial Average rose about 0.68%.

- The S&P 500 declined about 0.12%.

- Kospi night futures fell about 2.93%.

This pattern indicates that the weakness was concentrated in growth stocks, especially Big Tech and AI-related names, rather than reflecting broad recession fears.

2. The Weakness Was Concentrated in Big Tech and Hyperscalers

The day’s underperformance was not broad-based across technology.

It was most visible in hyperscalers.

Hyperscalers are companies that operate large-scale cloud and data center infrastructure.

Examples include Microsoft, Google, Amazon, Meta, Apple, and Nvidia.

These companies have been widely viewed as major beneficiaries of the AI cycle.

This time, however, the market focused on them as companies facing rising AI infrastructure costs.

The question has changed.

In the past, the market asked: “How much can AI grow?”

Now it is asking: “Can Big Tech absorb the cost of AI investment?”

3. Why Strong Micron Results Became a Negative for Big Tech

Micron’s results were clearly strong.

The key implication is that memory prices and margins may remain elevated for an extended period.

For Micron, that is a positive development.

It supports higher selling prices and improves the economics of longer-term supply arrangements.

Viewed from the other side, however, the same dynamic is different.

If Micron can sell memory at higher prices, Big Tech and hyperscalers must buy memory at higher prices.

- For Micron, this means higher revenue and improved margins.

- For Big Tech, it means higher data center costs.

- For semiconductor suppliers, it is a positive.

- For AI cloud operators, it is a cost pressure.

This is the core of the new bearish narrative.

Strong semiconductor earnings are no longer automatically interpreted as positive for Big Tech as a whole.

4. What Apple’s Price Increases Signaled

Another catalyst was Apple’s price increases.

Apple raised prices on Macs and iPads and indicated that further increases in other product lines may follow.

The market did not treat this as a routine pricing decision.

It interpreted it as evidence that higher memory costs are starting to be passed through to consumers.

Price increases may help Apple defend margins in the near term.

The risk is demand.

Higher prices for Macs and iPads could reduce unit sales.

That would not only affect Apple, but could also pressure the broader supply chain.

- Consumers face higher prices.

- Apple faces the risk of slower unit sales.

- Suppliers may face lower order volumes.

- The market may need to reassess technology valuations.

This dynamic can intensify both inflation concerns and consumption slowdown concerns in U.S. equities.

5. The Data Center Boom Could Become a Third Inflation Wave

The Wall Street Journal suggested that the data center boom could trigger a third inflation wave.

The first wave followed post-pandemic supply chain disruptions and the reopening cycle.

The second wave was linked to energy, geopolitics, tariffs, and oil shocks.

The third wave, according to this view, could come from the AI data center investment cycle.

AI data centers require substantial power, land, cooling systems, servers, GPUs, memory, and networking equipment.

If demand is concentrated enough, prices for related assets, commodities, and electricity could rise.

The issue is that these costs begin to show up in Big Tech earnings statements.

What was previously viewed as proof of future growth is now being treated as a present-day cost burden.

6. Why Big Tech Free Cash Flow Is Under Pressure

Historically, one of Big Tech’s main strengths has been strong free cash flow.

These companies generated significant cash, then used it for buybacks, dividends, and new investment.

That picture is changing as AI data center spending rises.

Cash generated by these companies is being deployed rapidly into data centers, GPUs, and memory purchases.

- Lower free cash flow reduces buyback capacity.

- Reduced buybacks weaken downside support for share prices.

- Higher AI capex can compress near-term margins.

- Debt issuance or other external funding needs may increase.

If Big Tech becomes more dependent on external funding, management will be less able to ignore share-price volatility.

Falling stock prices may lead management teams to slow the pace of AI investment.

That could, in turn, reduce data center spending, semiconductor orders, and growth across the AI infrastructure supply chain.

7. What Would Undermine This Bearish Narrative

To offset these concerns, Big Tech needs to show clear evidence that AI is generating revenue.

The market needs proof that AI cloud and AI services are translating into actual sales and earnings.

Until now, investors have rewarded companies that invest heavily in AI.

Going forward, they may favor companies that can demonstrate a return on AI investment.

- AI cloud revenue growth

- Rising enterprise AI usage

- GPU utilization and rental pricing

- Paid conversion rates for AI services

- Improvement in operating income relative to data center capex

The AI investment narrative in U.S. equities is moving from a pure growth story toward an efficiency and monetization test.

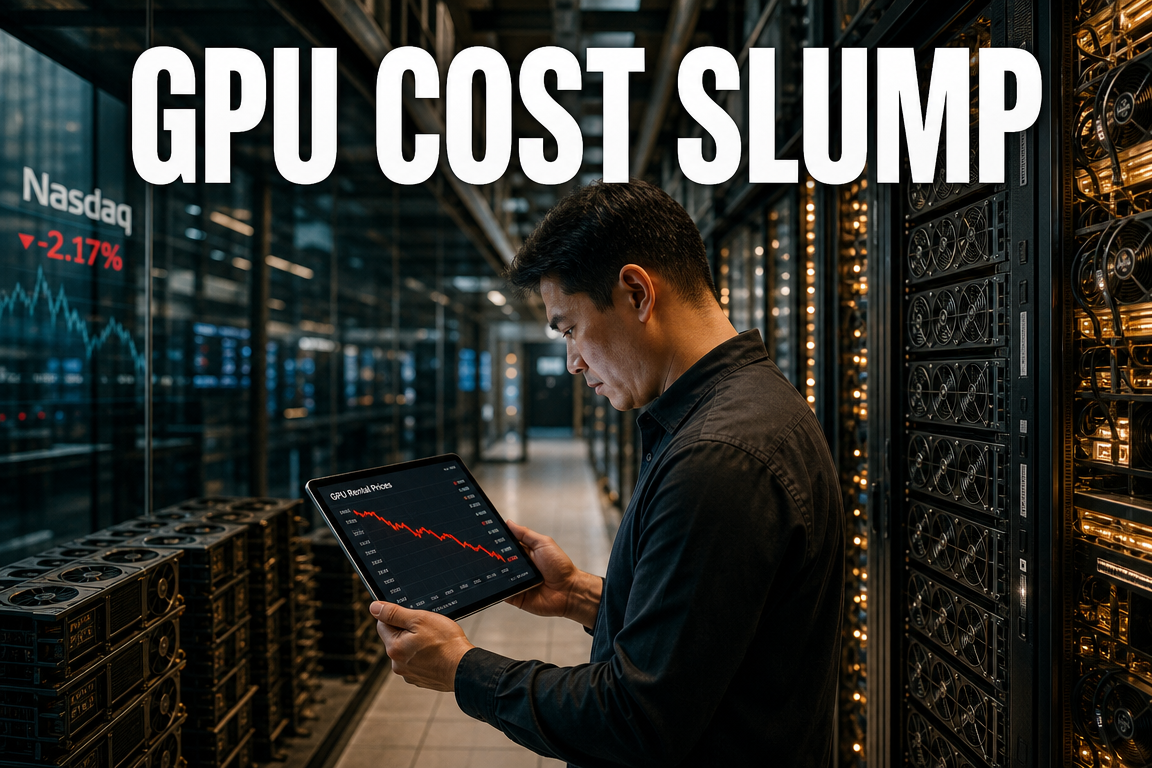

8. Why Falling GPU Rental Prices Matter

GPU rental pricing was also highlighted as an important indicator.

It provides an indirect measure of AI demand.

When demand is strong, pricing rises as more users seek GPUs for training and inference.

When demand weakens or supply increases, prices decline.

| GPU Type | Change From Peak Rental Price | Market Interpretation |

|---|---|---|

| H100 | Down about 25% | Possible slowing in the pace of existing AI demand |

| H200 | Down about 53% | Possible supply increase or near-term demand weakness |

| B200 | Down about 27% | Possible gap between new GPU expectations and realized demand |

GPU rental pricing alone does not prove that AI demand has peaked.

However, in a market where AI infrastructure spending has risen quickly, lower rental prices are likely to attract scrutiny.

9. The Rise of Chinese AI Models Could Challenge Big Tech’s Investment Case

An often overlooked factor is the growing adoption of Chinese AI models.

Usage of lower-cost Chinese language models has been rising quickly on platforms such as OpenRouter.

The reason is straightforward.

Top-tier models such as Claude are strong, but they are expensive.

Chinese models are cheaper and have improved materially in performance.

In coding, in particular, language models are among the most commercially relevant AI tools.

According to LLM Arena rankings, Claude models remain near the top, but Chinese GLM models are moving up the leaderboard.

- Chinese AI models have a stronger price advantage.

- Coding performance is improving rapidly.

- Enterprises have less reason to rely exclusively on expensive U.S. models.

- Wider adoption of lower-cost models could weaken the return logic for large-scale U.S. AI investment.

This is not an immediate single-day catalyst for the Nasdaq.

However, it is a meaningful variable for the long-term AI competition and for Big Tech valuations.

10. The Most Important Point Often Missed by Other Coverage

The key issue is not simply that Micron reported strong earnings.

The more important point is that profit within the AI value chain is shifting.

Until now, the market treated AI as one broad theme of shared upside.

If Nvidia benefited, Big Tech benefited. If memory semiconductors benefited, cloud companies benefited.

That relationship is now breaking apart.

- Memory semiconductor companies benefit from higher prices.

- GPU suppliers benefit from demand for high-performance chips.

- Data center equipment vendors benefit from rising infrastructure spending.

- Big Tech, by contrast, must absorb these costs.

In other words, even if the AI industry continues to grow, not all AI-related stocks will necessarily rise together.

Investors will increasingly need to distinguish between companies that receive the revenue and companies that bear the costs.

That distinction is likely to drive divergence across semiconductor stocks, Big Tech, cloud companies, and AI software names.

11. Implications for Korean Investors: A Mixed Outlook for Kospi and Semiconductors

The sharp decline in Kospi night futures reflects Korea’s sensitivity to the semiconductor and AI cycle.

Companies such as Samsung Electronics and SK Hynix, which have significant memory exposure, may benefit from Micron’s positive pricing backdrop.

However, there are also reasons for caution.

If memory prices rise too quickly, Big Tech customers will face higher costs.

If AI data center spending slows, memory demand could eventually weaken as well.

- In the short term, rising memory prices are supportive for Korean semiconductor stocks.

- In the medium term, the sustainability of Big Tech AI capex is critical.

- In the long term, AI monetization will be the key variable.

Accordingly, Korean semiconductor investors should monitor not only memory pricing, but also Big Tech capex, cloud revenue growth, and AI monetization trends.

12. Key Indicators to Watch Going Forward

Whether this bearish narrative becomes temporary or develops into a more durable headwind for the Nasdaq will depend on the following indicators.

- Micron, Samsung Electronics, and SK Hynix guidance on memory pricing

- Further product price increases from Apple

- Cloud growth rates at Microsoft, Google, and Amazon

- Big Tech capital expenditure guidance for AI data centers

- Additional declines in GPU rental prices

- Growth in paid AI usage and enterprise adoption

- Performance improvements and usage growth in Chinese AI models

- Whether data center-related costs begin to appear more clearly in U.S. inflation data

One of the most important issues will be how management teams explain the payback period for AI investment during earnings calls.

If they can present a convincing monetization framework, concerns may ease.

If costs continue to rise without clear revenue contribution, Nasdaq volatility may remain elevated.

13. Conclusion: The Next Stage of the AI Rally Is Cost Validation

This market move does not mean the AI rally is over.

It does suggest that the nature of the rally is changing.

Investors are no longer rewarding AI spending on scale alone.

They are now asking whether AI investment is translating into earnings, whether Big Tech can absorb data center costs, and whether higher memory prices can be passed on to customers.

The new bearish narrative for the Nasdaq is not based on traditional macro factors such as recession or rate hikes.

It is centered on cost inflation and capital return concerns within the AI sector itself.

Going forward, investors will need to assess AI growth alongside AI cost structure.

Within the same AI theme, Big Tech, semiconductors, and data center-related names may increasingly trade on different fundamentals.

< Summary >

Strong Micron results were positive for semiconductor vendors but were interpreted as a cost burden for Big Tech, which must purchase memory at higher prices.

Apple’s product price increases suggest that higher memory costs are beginning to pass through to end users.

Expanding AI data center investment may reduce Big Tech free cash flow and create a new inflationary pressure.

Falling GPU rental prices and the advance of Chinese AI models could pressure the return case for AI investment.

Going forward, the key issue for the Nasdaq is less about AI growth and more about AI monetization and cost control.

[Related Articles…]

- AI Infrastructure Spending and Monetization Outlook

- Nasdaq Volatility and Semiconductor Market Trends

*Source: [ 내일은 투자왕 – 김단테 ]

– 나스닥을 집어삼킬 새로운 하락 내러티브?

● Inflation, Stalled, Fed, Alert, Oil, Risk

U.S. PCE Inflation Immediate Analysis: Inflation Shock Avoided, but the Real Risk Markets Must Not Miss

The most important point in this U.S. PCE inflation release is that the numbers matched market expectations, but the trend remains uncomfortable.

In other words, there was no inflation shock severe enough to jolt equity markets immediately, but the data was not reassuring enough to remove concerns over the Federal Reserve’s policy path.

When viewed alongside Treasury yields, the dollar index, international oil prices, Middle East risk, U.S. GDP, and the Bank of Korea’s policy outlook, this PCE release is not just a price indicator. It is a key variable shaping the direction of financial markets in the second half of the year.

This report summarizes the PCE release, the Fed’s rate outlook, warnings from global investment banks, international oil and Middle East risk, the Bank of Korea’s policy stance, and the key response points investors should monitor.

1. U.S. PCE Inflation: In Line with Expectations, but the Trend Is Rising

The latest headline PCE inflation rate came in at 4.1%.

Core PCE inflation was reported at 3.4%.

The key point is that both figures matched market expectations exactly.

Since markets had already anticipated headline PCE at 4.1% and core PCE at 3.4%, Treasury yields and the dollar index did not surge immediately after the release.

In practical terms, the market interpreted the data as already priced in.

As a result, near-term concern over further rate hikes eased somewhat immediately after the release.

However, stopping there would miss the more important issue.

On a month-over-month basis, both headline and core inflation are showing renewed upward momentum.

That means there was no immediate shock today, but the possibility of renewed inflation pressure in June and July remains.

2. Market Reaction: Why Treasury Yields and the Dollar Index Stabilized

Because U.S. PCE inflation matched expectations, upward pressure on Treasury yields eased in the short term.

When inflation comes in above expectations, yields often rise as markets price in a higher probability of Fed tightening.

By contrast, when inflation is in line with expectations, the market tends to assume the Fed may not need to act more aggressively.

That second interpretation dominated after this release.

The dollar index followed a similar pattern.

If the probability of Fed rate hikes declines, upward pressure on the dollar can weaken.

Overall, the release supports the view that inflation remains a concern, but not one severe enough to disrupt markets immediately.

3. A More Important Data Point: U.S. GDP Revision Complicates the Rate Debate

In addition to the PCE report, the revised U.S. Q1 GDP figure also deserves attention.

The estimate was revised up from 1.6% to 2.1%.

This indicates that the U.S. economy remains stronger than previously assumed.

A stronger economy gives the Fed more room to consider rate hikes if necessary.

If growth and employment remain resilient, the Fed can focus more directly on price stability.

Put simply, the Fed must balance two objectives: inflation and employment.

At present, the employment and growth side of the equation has not deteriorated sharply.

The more pressing issue is inflation.

That is why markets remain alert to the possibility that the Fed could raise rates again if inflation accelerates.

4. Fed Policy Outlook: Hold Still Looks More Likely Than an Immediate Hike

Following the release, the market has lowered the perceived probability of a Fed rate hike.

FedWatch pricing still reflects a higher probability of holding rates steady.

Based on this data alone, a July FOMC rate increase does not appear highly likely.

That said, it would be premature to rule out a rate hike later this year.

The June inflation data, due in July, and the July inflation data, due in August, will be critical.

This PCE report may still reflect a pre-transmission stage before the Middle East conflict and higher energy prices fully feed into core inflation.

Investors should therefore monitor whether energy-driven cost increases spread into goods, services, and housing.

That will likely determine the Fed’s next move.

5. Global Investment Banks’ Warning: Why Bank of America and Deutsche Bank Still See Hike Risk

One notable aspect of this analysis is the outlook from major global investment banks.

Bank of America sees room for the Fed to raise rates as many as three times this year.

Deutsche Bank has also raised the possibility of two hikes.

Their argument is straightforward.

First, U.S. employment remains strong.

Second, U.S. growth has held up better than expected.

Third, core inflation pressure is rising again.

Fourth, oil prices are unlikely to fully return to pre-conflict levels.

In other words, the Fed still has an environment in which rate hikes remain possible.

The key distinction, however, is that not all major banks are forecasting an aggressive tightening cycle.

The market consensus still leans more toward holding rates steady.

So the realistic interpretation is not that a hike is already decided, but that the rate-hike debate could return if inflation accelerates again.

6. Dot Plot Interpretation: More Policymakers Are Open to a Hike

The latest FOMC dot plot showed an important shift.

Previously, there were almost no policymakers signaling a rate hike, but recently more members have marked the possibility of a hike.

This is particularly important because some of the officials with voting power have also left that option open.

For markets, that is a concern.

It means the internal view at the Fed has not fully dismissed the possibility that renewed inflation pressure would require a rate hike.

Of course, the final consensus under Chair Powell may still evolve.

But based on the dot plot alone, markets cannot fully ignore the possibility of another hike.

7. International Oil and Middle East Risk: The Main External Variable

The most important external factor in interpreting this PCE report is international oil.

After the Middle East conflict began, oil prices surged and then partially stabilized.

The key question is whether prices can fully return to pre-conflict levels.

At this stage, that appears unlikely.

Although shipping through the Strait of Hormuz has recovered somewhat, conditions have not fully normalized to pre-war levels.

In addition, parts of the oil industry value chain, including upstream, midstream, and downstream segments, have already been disrupted.

Once production, refining, storage, and logistics are shaken, prices do not normalize quickly.

Even if oil prices stabilize, their year-over-year effect can still weigh on inflation.

Inflation is typically measured on a year-over-year basis.

If oil remains above the level seen a year earlier, energy inflation can continue to contribute positively to the index.

8. The Key Question Is Whether Energy Inflation Spreads into Core Inflation

Inflation tends to spread like wildfire.

First comes energy.

Then transportation costs rise.

After that, goods and food prices follow.

Finally, services, wages, and housing costs may also be affected.

Based on the May PCE data alone, there is not yet strong evidence that the energy shock has fully passed through to core inflation.

However, the June inflation data, to be released in July, could tell a different story.

If energy price increases begin to filter into goods and services, concern over another Fed hike will likely intensify.

If the pass-through remains limited, markets may once again start pricing in a more supportive liquidity environment.

9. Gold and Bitcoin: Why They Did Not Rally Sharply Despite the Uncertainty

Gold usually rises when geopolitical risk increases.

That is because investors seek safe-haven assets.

However, this time the situation was different.

Middle East risk rose, but inflation concerns and rate-hike fears also increased.

Gold does not generate yield.

When Treasury yields rise, gold becomes relatively less attractive.

Bitcoin is also highly sensitive to liquidity conditions.

When the probability of higher rates rises, liquidity-sensitive assets face pressure.

By contrast, semiconductor stocks tend to attract capital because they can demonstrate earnings strength.

That is why sectors such as NVIDIA, Micron, Samsung Electronics, and SK hynix remain in focus.

Uncertainty alone is not enough to sustain gains in gold or crypto. Favorable liquidity and rates are also required.

10. Bank of Korea Policy Outlook: Korea May Be More Sensitive Than the U.S.

For Korean investors, the key issue is the Bank of Korea.

The U.S. already has a relatively high policy rate.

If the U.S. policy rate is already in the 3.5% to 3.75% range, it is difficult to justify an immediate hike against core PCE at 3.4%.

Policy is already restrictive.

Korea faces a different situation.

Because Korea’s policy rate is lower, the Bank of Korea may react more sensitively if currency weakness and inflation pressures appear together.

In other words, the same 3% inflation reading can lead to different policy responses in the U.S. and Korea.

The Bank of Korea must also consider won weakness, import price pressures, and higher oil costs.

As a result, markets should be cautious about the possibility of a rate hike at the July policy meeting.

11. Equity Market Perspective: Separate Structural Trends from Short-Term Noise

The most important mindset for investors is to distinguish between structural trends and short-term noise.

If a large wave of structural downside emerges, defensive positioning is warranted.

Examples include an inflation shock, an earnings shock, an unexpected Fed hike, or a sharp rise in Treasury yields.

In such cases, the equity market can undergo a meaningful correction.

That is a structural wave.

By contrast, some pullbacks are driven mainly by fear rather than by a deterioration in fundamentals.

Those are short-term waves.

Panicking in response to short-term noise can mean missing better entry points.

This PCE release is closer to an in-line event than to an inflation shock.

Accordingly, it is difficult to view it as a market-disrupting negative in the near term.

The June and July inflation prints will determine whether this is a structural wave or short-term noise.

12. Why Semiconductor Earnings Matter: Liquidity Ultimately Favors Execution

In recent months, semiconductor earnings have been a key signal for the market.

Results from Micron, NVIDIA, Samsung Electronics, and SK hynix have had a direct effect on global investor sentiment.

Gold and crypto do not report earnings.

Equities do.

AI semiconductors, memory chips, and data-center related companies are already showing revenue and profit improvement.

If liquidity remains available, capital is likely to move toward sectors with visible earnings growth.

This matters when assessing both PCE inflation and the Fed’s rate outlook.

Stable rates support growth and technology stocks.

Conversely, a renewed rise in yields would pressure valuations.

13. The Most Important Point Missing from Most Coverage

The most important issue in this PCE analysis is not the 4.1% or 3.4% reading itself.

The key issue is the lag between an energy shock and its transmission into core inflation.

Most coverage focuses only on the headline numbers and immediate market reaction.

But inflation does not move all at once.

When oil prices rise, services prices do not adjust immediately.

There is a lag through transportation costs, production costs, raw materials, price pass-through, and consumer pricing.

That is why a May PCE reading in line with expectations should not be interpreted as an all-clear.

The real test comes with the June inflation data released in July and the July inflation data released in August.

If goods and services inflation rise together, the debate over another Fed hike could return quickly.

If the transmission remains limited, markets may again price in a more favorable liquidity backdrop.

In that sense, this PCE report is more of a preview than a conclusion.

14. Key Upcoming Events to Watch

First, the June CPI and PCE reports, both due in July, should be monitored.

The key question is whether higher energy prices are passing into core goods and services.

Second, Chair Powell’s comments at the July FOMC will matter.

His communication is more important than the dot plot.

Third, investors should track international oil prices and the normalization of shipping through the Strait of Hormuz.

If oil does not stabilize, inflation expectations may remain elevated.

Fourth, U.S. employment data and GDP trends should be watched.

Strong growth and employment give the Fed more room to focus on inflation.

Fifth, the Bank of Korea’s policy meeting and the KRW/USD exchange rate should be monitored.

Korea is more directly affected by currency weakness than the U.S.

15. Investor Strategy: Focus on Conditions, Not Direction Alone

The market is in a phase where simple directional calls are difficult.

Inflation shock has been avoided, but inflation pressures remain.

Rate-hike concerns have eased, but have not disappeared.

Oil prices have stabilized, but are unlikely to return quickly to pre-war levels.

Accordingly, investors should avoid framing the outlook as either “no rate hike” or “equities will rise regardless.”

A conditional approach is more appropriate.

If June and July inflation data remain stable, growth stocks and semiconductors should benefit.

If Treasury yields rise again, high-valuation growth stocks will face pressure.

If oil prices turn higher again, inflation and currency volatility may both increase.

If semiconductor earnings continue to improve, liquidity is likely to rotate toward earnings-driven equities.

In the end, investors should focus less on headlines and more on how the data connect.

< Summary >

U.S. PCE inflation came in at 4.1% headline and 3.4% core, in line with market expectations.

There was no immediate inflation shock, and rate-hike concerns eased modestly after the release.

However, the inflation trend is still rising, making the June and July data more important.

U.S. GDP was revised up to 2.1%, giving the Fed room to remain attentive to inflation.

Bank of America and Deutsche Bank still see the possibility of rate hikes this year.

International oil and Middle East risk remain key variables for second-half inflation.

The most important issue is whether energy costs spread into goods and services inflation.

The Bank of Korea may react more sensitively than the Fed because of exchange-rate and inflation pressures.

For equities, the near-term direction is likely to depend more on upcoming inflation data and semiconductor earnings than on the PCE release alone.

[Related Articles…]

U.S. PCE Inflation and Fed Rate Outlook

Oil Prices and Inflation Risk Review

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [LIVE] 미국 PCE 물가 심층분석 : ‘인플레 쇼크’ 오는가? [즉시분석]