● Semiconductor Shock, Kospi Fight, NPS Selloff, HBM Boom

Samsung Electronics and SK Hynix Earnings Will Shape the Direction of the KOSPI in July: NPS Rebalancing, Semiconductor Earnings, and the Policy Rate in One View

The key issue for the Korean equity market in July can be reduced to one question.

Will Samsung Electronics and SK Hynix beat market expectations, or not?

The market already has a broad sense that both companies’ earnings will improve.

The real issue is not whether earnings are good, but whether they are better than expected.

In addition, the July market will face a complex supply-and-demand battle as National Pension Service rebalancing, pension fund selling, the Bank of Korea’s policy rate, large IPOs in the U.S. and China, and continued growth in overseas equity investment by retail investors all converge.

One point often overlooked is the potential U.S. ADR listing of SK Hynix and its market impact.

This should be viewed not as a simple listing event, but as a variable that could affect Korean semiconductor valuation and foreign capital flows.

1. The most important driver for the KOSPI in July is semiconductor earnings

Semiconductors are no longer just one industry within Korea’s equity market.

The original analysis effectively treats the semiconductor industry as a macro indicator.

The reason is clear.

Semiconductors account for a large share of Korea’s exports, and Samsung Electronics and SK Hynix have an outsized influence on KOSPI market capitalization.

In practical terms, evaluating the Korean economy now requires more than monitoring consumer prices, the exchange rate, and policy rates.

HBM, DRAM, memory prices, AI server investment, and Micron’s earnings must also be monitored to assess the direction of the Korean market.

In particular, the earnings releases from Samsung Electronics and SK Hynix are key events that could determine the KOSPI’s direction in July.

If both companies deliver an earnings surprise, that could offset pressure from NPS rebalancing and policy-rate concerns.

If they disappoint, profit-taking could intensify after the recent price gains.

2. Earnings are solid, but the real issue is the consensus

Both Samsung Electronics and SK Hynix are likely to post stronger earnings.

However, the stock market does not rise simply because earnings improve.

The market always focuses on results relative to expectations.

The key term here is consensus.

Consensus refers to the average earnings forecast compiled by securities analysts.

If actual results exceed consensus, it is an earnings surprise.

If results fall short of consensus, it is an earnings disappointment, even if earnings improve year over year.

For example, even if Samsung Electronics posts a significant increase in operating profit, the stock may react negatively if the market had already expected a stronger number.

Conversely, if expectations are modest and the actual result is materially stronger, the stock can respond sharply.

The original analysis notes that Micron’s earnings exceeded market expectations.

This is interpreted as a sign that the global memory semiconductor cycle remains firm.

Accordingly, Samsung Electronics and SK Hynix may also have room to exceed existing consensus estimates.

However, one caution is necessary.

Consensus is not fixed.

It can rise continuously ahead of earnings releases.

In other words, if expectations move up too quickly, even strong earnings may fail to support further share-price gains.

3. NPS rebalancing is a source of downward pressure on the KOSPI

Another major variable in the Korean market in July is National Pension Service rebalancing.

The NPS allocates assets across domestic equities, overseas equities, bonds, and alternatives.

When the KOSPI rises sharply, the domestic equity share can increase without any additional buying by the NPS.

The original analysis refers to the NPS fund size at roughly KRW 1,700 trillion to KRW 2,000 trillion.

Even a small change in domestic equity allocation within such a large pool can have a significant market impact.

The analysis notes that the domestic equity target had previously been set at around 14.9% for 2026, but the domestic equity share rose materially as prices advanced.

It also mentions a decision to raise the domestic equity allocation to 20.8%, with a tactical and strategic range allowing holdings of up to 28.8%.

The issue is that if the domestic equity share approaches or exceeds that range, rebalancing may be required.

Rebalancing means trimming assets that have risen too much and reallocating to assets whose weight has fallen.

When pension fund selling occurs through this process, it creates downward pressure on the KOSPI.

The original analysis estimates that NPS rebalancing could amount to roughly KRW 55 trillion.

This does not mean that the amount will hit the market all at once.

It is more likely to be executed gradually, depending on market conditions.

However, the key issue is the direction of flow.

If the NPS needs to reduce domestic equity exposure, selling pressure may emerge whenever the KOSPI rises.

4. June volatility was partly driven by preemptive pension-fund selling

The original analysis suggests that one source of June KOSPI volatility may have been preemptive rebalancing by the NPS.

If the required year-end adjustment had been left to July, the market impact could have been much larger.

For that reason, the analysis raises the possibility of some preemptive selling in May and June.

This is an important supply-and-demand point for investors.

When stocks move sharply, it is not enough to think only in terms of “foreigners sold” or “retail bought.”

Asset allocation changes by a large institution such as the NPS can directly affect the KOSPI’s direction.

The NPS is not a short-term trading participant.

It moves according to target weights and investment policy.

As a result, once its selling direction is set, the process may continue for some time.

Investors should therefore monitor the possibility of continued pension-fund selling when the KOSPI rises in July.

5. Downward pressure on the KOSPI ① NPS rebalancing

The first source of downward pressure is the NPS rebalancing described above.

With domestic equity exposure already elevated, the NPS may need to adjust its allocation.

This could affect large-cap names such as Samsung Electronics and SK Hynix.

That said, rebalancing does not necessarily imply a sharp decline.

If semiconductor earnings are strong and foreign buying is present, the market can absorb pension-fund selling.

If earnings disappoint and foreigners do not buy, the rebalancing burden may weigh more heavily on the market.

6. Downward pressure on the KOSPI ② Large IPOs in the U.S. and China

The second source of downward pressure is large IPO activity in the U.S. and China.

The original analysis mentions major Chinese IPO candidates such as Huaneng Renewables and a memory semiconductor-related listing.

It also points to the possibility of record-scale IPOs in the Shenzhen market.

In the U.S., possible large listings from SpaceX, Anthropic, and OpenAI are cited.

Such global IPOs absorb investor capital across markets.

Investors have finite capital and must allocate it across opportunities.

When major IPOs open in the U.S. and China, capital available for the Korean market may be diluted.

This is especially relevant if AI, space, and semiconductor-related listings attract strong attention.

For the KOSPI, this could reduce foreign demand.

7. Downward pressure on the KOSPI ③ The Bank of Korea policy rate

The third source of downward pressure is the Bank of Korea’s policy-rate decision.

The original analysis refers to the July 16 rate decision and treats a rate hike as a possible variable.

It notes that inflation and the exchange rate remain concerns, and that a more hawkish stance by the new governor could leave room for a hike.

When policy rates rise, the relative appeal of equities may decline.

Higher deposit and bond yields can lead investors to question the need to take equity risk.

This is particularly relevant when stock prices have already moved higher.

The policy rate is the central bank’s key policy tool.

It influences government bond yields and ultimately market rates such as deposit and lending rates.

For that reason, the Bank of Korea’s rate decision affects equities, real estate, the exchange rate, and bonds.

8. Downward pressure on the KOSPI ④ Retail investors’ growing overseas allocation

The fourth source of downward pressure is the expansion of retail overseas investing.

The original analysis notes that individual investors are showing growing interest not only in domestic equities but also in overseas markets.

When the KOSPI has already risen significantly, some investors may realize gains in domestic stocks and reallocate to U.S. equities or global AI names.

This is not simply a change in preference.

If the Korean market is facing NPS rebalancing, policy-rate concerns, and valuation pressure from high expectations, overseas equities may appear more attractive.

Retail participation in the market has increased, and average investment sizes have also grown.

As a result, domestic and overseas investing can rise together.

However, when overseas allocation increases quickly, KOSPI liquidity can weaken relatively.

9. Why foreign buying matters most

If the NPS needs to reduce domestic equity exposure through rebalancing, the key question is who will absorb those shares.

The most important buyer is foreign investors.

If foreigners actively buy Samsung Electronics and SK Hynix, the KOSPI can withstand pension-fund selling.

If foreign buying is weak and only retail investors provide support, the market may feel pressure.

This is especially true because Samsung Electronics and SK Hynix represent a very large share of KOSPI market capitalization.

Foreign flows into or out of these two names can determine the direction of the broader index.

In the end, July is not a market that can be explained by earnings alone.

It is a market shaped simultaneously by earnings, supply and demand, interest rates, exchange rates, large overseas IPOs, and foreign capital flows.

10. Key earnings dates and monitoring points for Samsung Electronics and SK Hynix

The original analysis also highlights the importance of July earnings dates for Samsung Electronics and SK Hynix.

While dates may change, Samsung Electronics is presented as releasing preliminary results in early July and final results in late July.

SK Hynix is also described as following a similar late-July preliminary and final reporting schedule.

Investors should focus on the following points:

-

First, whether operating profit exceeds consensus.

-

Second, how quickly HBM sales and margins are improving.

-

Third, how much of the DRAM price recovery is reflected in earnings.

-

Fourth, whether AI server demand is sustainable rather than one-off.

-

Fifth, how management guidance is framed in the earnings conference call.

Equities tend to respond more to future outlook than to past results.

Accordingly, strong current earnings may not support the stock if the outlook is weak.

Conversely, even if current results are only in line with consensus, a strong forward outlook can support the share price.

11. A key issue overlooked by many reports: the potential U.S. ADR listing of SK Hynix

The original analysis singles out SK Hynix’s potential U.S. ADR listing as a major issue.

This should not be viewed merely as a case of “the stock can be traded in the U.S. as well.”

If SK Hynix trades in ADR form in the U.S., global investor access could improve materially.

ADR stands for American Depositary Receipt.

It is a security structure that allows U.S. investors to trade foreign companies more easily in the U.S. market.

In other words, U.S. investors could access SK Hynix without directly entering the Korean market.

This matters for three reasons:

-

First, foreign investor access improves.

-

U.S. institutional and retail investors could buy and sell SK Hynix more easily.

-

Second, valuation re-rating becomes possible.

-

As a representative AI semiconductor name, it could be evaluated alongside Micron and the Nvidia value chain.

-

Third, the Korean market’s supply-demand structure could change.

-

Demand previously limited to the domestic market could partially shift to U.S. ADR trading, while U.S.-based buying could also support the stock price.

The key point is that SK Hynix may no longer be evaluated only as a Korean semiconductor company.

If U.S. investors can access the company directly in the context of AI infrastructure, HBM, and global data-center investment, a premium may be justified.

12. The real core point often missed in other reports

The most important issue is not NPS selling itself, but whether semiconductor earnings surprises and foreign capital can absorb that selling.

Most reports describe “the NPS is selling,” “Samsung Electronics earnings are strong,” and “SK Hynix is rising” as separate items.

However, the market does not move in separate lanes.

Downward pressure from NPS rebalancing and upward pressure from semiconductor earnings surprises are colliding at the same time.

The factor that determines the outcome is foreign investors.

If foreigners buy Samsung Electronics and SK Hynix aggressively, NPS selling can be absorbed.

If foreigners stay on the sidelines or sell, NPS rebalancing becomes a justification for a KOSPI correction.

Another hidden point is that when consensus keeps rising, even strong earnings can become a negative catalyst.

If expectations rise too far, stock prices may fall even after good earnings.

Investors therefore need to focus not on whether earnings are good, but on whether they are better than expected.

Finally, the SK Hynix ADR issue could become an event that changes Korea’s semiconductor access to global capital.

This is not just a short-term trading factor; it may also relate to a reduction in the Korea discount.

13. July KOSPI scenarios

| Scenario | Key Conditions | Impact on the KOSPI |

|---|---|---|

|

Bullish scenario |

Samsung Electronics and SK Hynix earnings surprise, foreign buying expands, HBM growth confirmed |

The market absorbs NPS rebalancing pressure and the KOSPI could extend gains |

|

Neutral scenario |

Earnings are solid but broadly in line with consensus, with balanced NPS selling and foreign buying |

The KOSPI may move within a range |

|

Bearish scenario |

Earnings disappointment, no foreign buying, policy-rate pressure, capital diversion to overseas IPOs |

Profit-taking and pension-fund selling may trigger a correction |

14. Key indicators for investors to monitor now

-

Changes in Samsung Electronics operating profit consensus

-

SK Hynix HBM sales mix and profitability

-

Global memory semiconductor price trends after Micron’s earnings

-

NPS and pension-fund net selling volume

-

Whether foreign investors turn net buyers of the KOSPI

-

The Bank of Korea’s policy-rate decision and exchange-rate response

-

Timing of large IPOs in the U.S. and China

-

Growth in retail overseas equity investment

-

Any concrete announcement regarding SK Hynix ADRs

15. Conclusion: July KOSPI trading will depend on whether semiconductor earnings can overcome supply-side pressure

July’s KOSPI should not be viewed as a simple bull or bear market.

Upward and downward forces are both strong.

Downward pressure comes from NPS rebalancing, pension-fund selling, the Bank of Korea’s policy-rate risk, large IPOs in the U.S. and China, and increased overseas investment by retail investors.

Upward support comes from stronger semiconductor earnings for Samsung Electronics and SK Hynix, HBM growth, signs of improved memory-market conditions from Micron, and potential foreign inflows.

Ultimately, the issue is whether Samsung Electronics and SK Hynix can beat market consensus.

If both deliver earnings surprises, the KOSPI can overcome negative factors and move higher.

If they disappoint, elevated valuations and rebalancing pressure may combine to deepen the correction.

Investors should avoid making a one-directional call and instead monitor the full set of variables.

In Korea’s equity market, semiconductors effectively function as a macro indicator.

To assess the KOSPI properly in July, investors need to track Samsung Electronics and SK Hynix earnings, foreign flows, and NPS rebalancing together.

< Summary >

The main variable for the KOSPI in July is the earnings performance of Samsung Electronics and SK Hynix.

The key issue is not just whether earnings are strong, but whether they exceed consensus.

NPS rebalancing may act as a source of downward pressure on the KOSPI.

Large IPOs in the U.S. and China could divert global capital.

The Bank of Korea’s policy rate and the expansion of retail overseas investing also remain headwinds.

By contrast, a semiconductor earnings surprise and strong foreign buying could support further KOSPI gains.

The most important overlooked variable is the potential U.S. ADR listing of SK Hynix.

The KOSPI’s direction in July will depend on whether semiconductor earnings can offset supply-side pressure.

[Related Articles…]

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 삼성전자·SK하이닉스 실적, 코스피 운명 가른다 | 경제학교 월간특강 [3편]

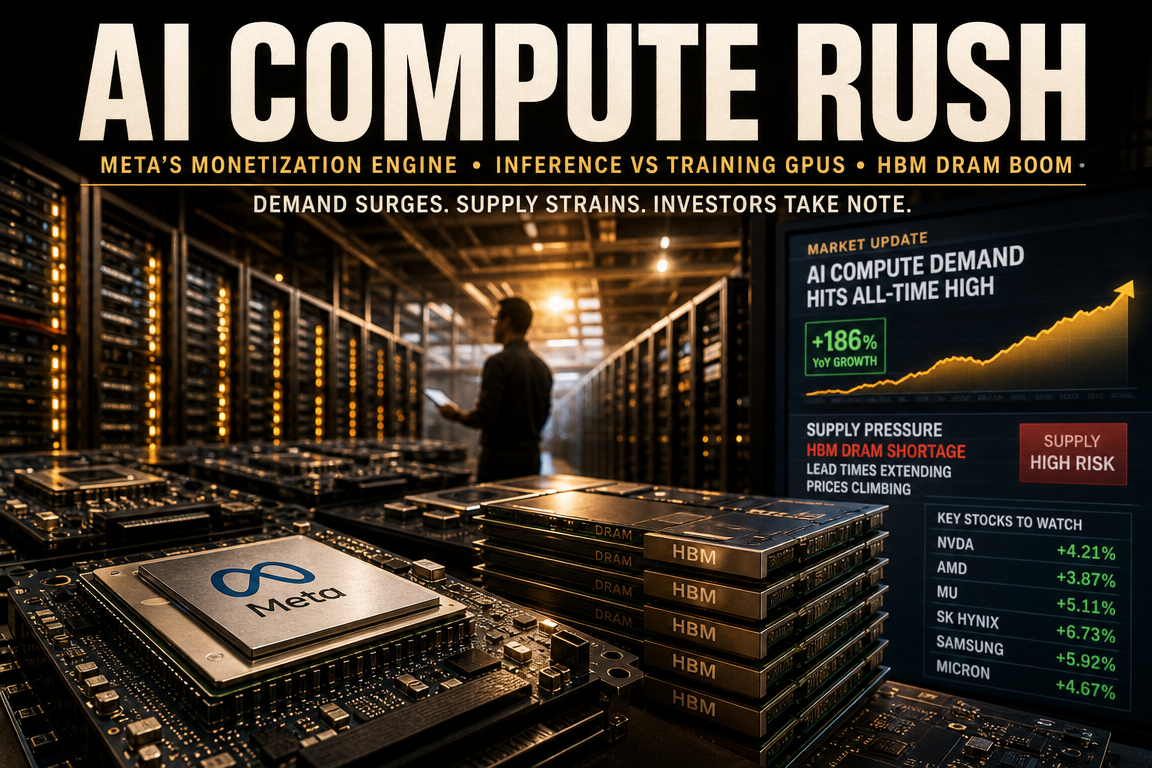

● Meta Shock – KOSPI, AI Cuts, Foreign Selloff

Kospi Weakens on Meta-Driven Shock as AI Capex Slowdown Signals and Foreign Outflows Dominate

This decline should not be viewed simply as a move in Meta’s share price.

The key issue is that Meta’s decision to monetize surplus AI compute resources and explore a cloud business signaled to Wall Street that large-cap tech companies may be moderating the pace of AI capital expenditure.

That signal weakened U.S. AI semiconductor and data-center-related stocks, including Micron, SanDisk, NVIDIA, AMD, and Intel, and the impact quickly spread to Samsung Electronics, SK hynix, and Korean semiconductor equipment and materials names.

In addition, foreign selling, concurrent institutional selling, a rebound in 10-year Treasury yields, and a weaker won all added pressure to the Kospi.

This report summarizes why the Meta-driven shock translated into a decline in the Kospi, why foreign flows matter, and where capital may rotate next if leading semiconductor stocks remain under pressure.

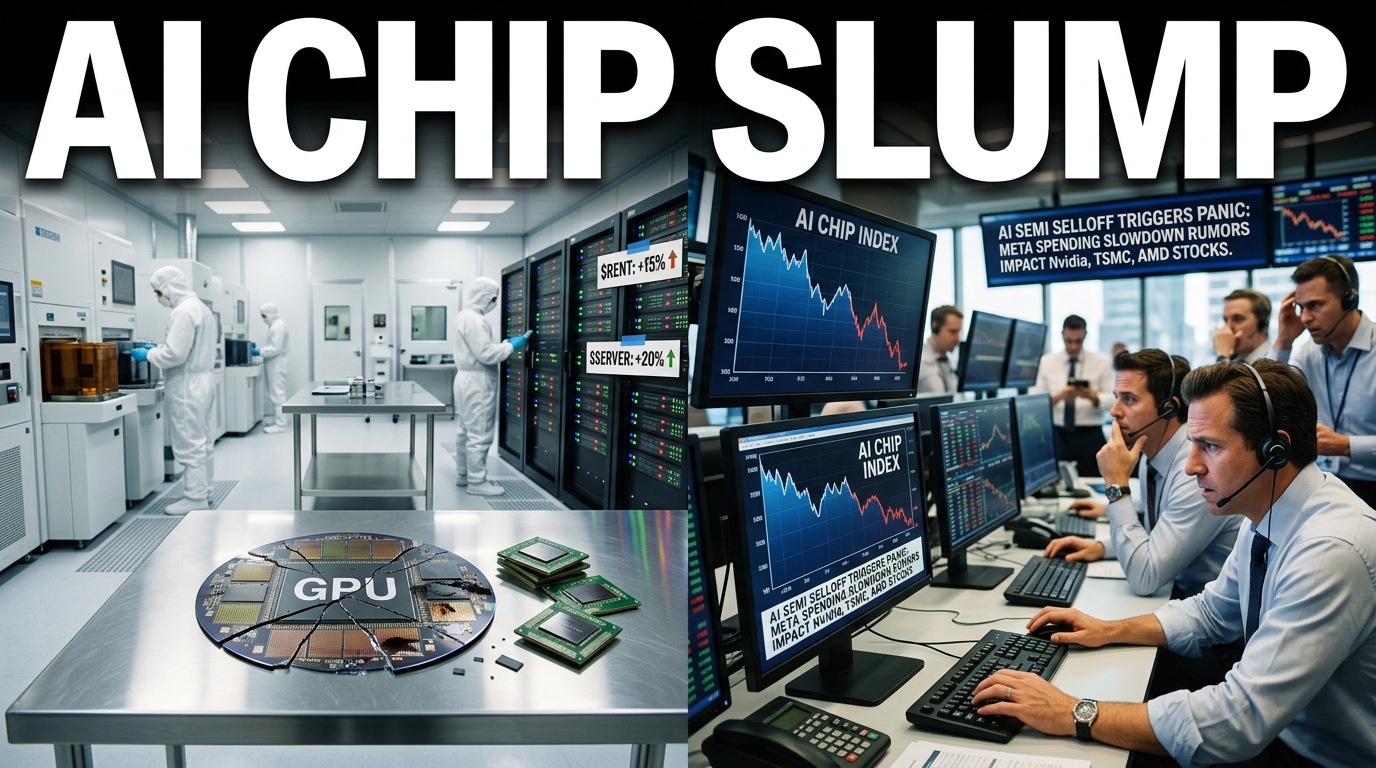

1. The immediate trigger: Meta-driven pressure and a sharp selloff in U.S. semiconductor stocks

The primary catalyst was the overnight decline in the U.S. market linked to Meta.

More precisely, the issue was not a negative event specific to Meta, but rather a strategic shift that pressured the broader AI infrastructure supply chain.

Meta advanced after reports that it would sell surplus compute capacity externally and pursue a cloud business.

Investors interpreted this as a sign that Meta may be moving beyond unrestricted AI infrastructure spending and toward monetization.

However, this was negative for companies that supply GPUs, HBM, memory, server equipment, networking gear, and optical communications components to Meta.

As a result, U.S. stocks such as Micron, SanDisk, Intel, AMD, NVIDIA, and other AI server and cloud infrastructure names came under pressure.

In Korea, the shock quickly spread to Samsung Electronics, SK hynix, and semiconductor equipment and materials companies.

2. Why Meta rose while semiconductor stocks fell

This is the most important point in the current move.

Meta’s shift from “increase AI capex” to “monetize existing resources” was interpreted as positive for profitability and cost efficiency.

For Meta, this is constructive.

The company has been carrying a heavy AI data-center investment burden, and monetizing those assets through external sales or leasing could improve returns.

For semiconductor suppliers, however, the implication is different.

If Meta is already monetizing surplus compute resources, investors may assume that incremental GPU, HBM, and memory demand could slow.

That is the mechanism behind the valuation reset across the AI semiconductor supply chain.

In short, Meta benefited from the narrative of monetizing existing assets, while suppliers were pressured by concerns that future orders may decelerate.

3. Wall Street’s message: large-cap tech must now prove AI profitability

The broader message from Wall Street is a shift in focus toward profitability discipline.

Meta’s stock rose as investors welcomed signs of slower capex growth and stronger monetization potential.

That raised expectations that Amazon, Alphabet, and Microsoft could eventually move in a similar direction.

Notably, cloud leaders such as Alphabet, Microsoft, and Amazon did not sell off sharply on the prospect of Meta entering cloud-related activity.

Markets appeared to focus less on direct competition and more on a broader shift from AI spending intensity to AI return generation.

This is a material change in the AI investment cycle.

Until now, the market rewarded companies for spending more on AI; going forward, it may place greater weight on monetization and earnings conversion.

This shift has direct implications not only for U.S. equities, but also for Korea’s Samsung Electronics and SK hynix.

4. Why the Kospi moved more sharply: heavy semiconductor concentration

Korea’s equity market reacted more strongly because of its high concentration in semiconductors.

Samsung Electronics and SK hynix are key index drivers for the Kospi.

When semiconductor equipment and materials stocks also weaken, the entire index becomes vulnerable.

The original report noted that SK hynix fell by a double-digit percentage and Samsung Electronics also declined sharply.

Semiconductor equipment and materials names such as Samsung Electro-Mechanics, Wonik group companies, and Hanmi Semiconductor also corrected.

In a market structure like this, even if individual company fundamentals are intact, a global shift in AI semiconductor sentiment can still drag the entire index lower.

SK hynix, which had been supported by HBM expectations, is particularly exposed when concerns emerge over a slowdown in AI spending.

5. Why simultaneous selling by foreign investors and institutions matters

Another key point is market flows.

Foreign selling is common, and retail investors often buy into weakness.

But when both foreign investors and institutions sell at the same time, the market is much more likely to break down materially.

Foreign selling may reflect not only stock-specific profit-taking, but also broader risk reduction, currency pressure, and portfolio rebalancing.

Foreign investors may reduce Korean exposure when the market has risen significantly.

They may also continue selling during declines.

That is because Korea is treated as an emerging-market exposure by global investors, and risk-off periods often lead to reduced allocations first in such markets.

When institutions sell alongside foreigners, retail demand alone is usually insufficient to stabilize the index.

For that reason, concurrent foreign and institutional selling is an important signal when assessing whether a move is a correction or the start of a broader downtrend.

6. Will retail dip-buying work again?

Retail investors have frequently bought aggressively during recent pullbacks.

If this decline proves to be only a correction, retail dip-buying may work again.

If, however, this is the beginning of a broader downtrend, retail buying may simply absorb stock being distributed by foreign and institutional investors.

The key distinction is the quality of any rebound.

What matters is not just a short technical bounce, but whether foreign selling stops, the won stabilizes, Treasury yields ease, and leading semiconductor names recover with strong trading volume.

Retail demand alone does not confirm a market bottom.

It is more important to verify whether the dominant flow of capital is changing.

7. Apple’s talks with Chinese memory suppliers add pressure to the memory cycle

Another factor behind the decline was news that Apple is negotiating with Chinese memory suppliers such as ChangXin Memory and Yangtze Memory.

This could weigh on established memory leaders such as Samsung Electronics, SK hynix, and Micron.

Chinese firms are unlikely to close the gap quickly in high-value AI memory products such as HBM.

However, competition in conventional PC, smartphone, and commodity memory markets could intensify.

As the original report noted, Micron’s recent results showed strong profitability not only in AI-related memory, but also in PC and smartphone memory.

If Chinese companies continue to expand capacity and secure financing through listings or other channels, pricing pressure in commodity memory could increase.

As a result, memory makers face both a slowdown risk in AI-related demand and a supply expansion risk from China.

8. Yield and exchange-rate movements are also unfavorable for the Kospi

When markets weaken, the first macro variables to monitor are yields and the exchange rate.

The report highlighted concern over the rebound in the U.S. 10-year Treasury yield.

Rising yields are negative for growth stocks and technology valuations.

This creates pressure on AI semiconductors, the Nasdaq, and other high-multiple growth names.

A weaker won is also unfavorable for Korean equities.

When KRW/USD rises, foreign investors face greater currency risk, increasing incentives to shift toward dollar assets.

If foreign selling continues while the won remains weak, a Kospi recovery may be limited.

One relatively supportive factor is lower oil prices.

Lower oil can ease inflation pressure and reduce costs for companies.

However, oil stability alone is unlikely to offset the combined pressure from yields and exchange rates.

9. The U.S. market remains fragile

The report noted that the U.S. market attempted an intraday rebound but then weakened again.

Although the Nasdaq tried to recover, it later turned lower, and the index recorded a substantial point decline over a short period.

This suggests that sentiment is weakening not only in Korea but across global technology stocks.

AI cloud, data center, memory, GPU, and networking stocks have been trading as a single theme.

They rose together during the upcycle and are now correcting together.

Accordingly, Korean investors should monitor not only the Kospi, but also the Nasdaq, the Philadelphia Semiconductor Index, Micron, NVIDIA, U.S. 10-year yields, and KRW/USD.

10. Some stocks rise even in a declining market: a sign of capital rotation

Even in a broad market decline, not all stocks move lower.

The report noted that Naver, Korea Electric Power, and some financial stocks held up relatively well or gained.

This may indicate a rotation of capital away from semiconductors into other sectors.

When leading semiconductor stocks pause, previously overlooked sectors can attract attention.

Potential alternatives can include platform companies, utilities, financials, defense, shipbuilding, and consumer sectors depending on market conditions.

That said, this should not be interpreted as automatic rotation.

A genuine leadership shift requires trading volume, institutional and foreign flows, earnings visibility, and policy support.

11. Pressure visible in Samsung Electronics and SK hynix charts

The original report emphasized the consolidation patterns in Samsung Electronics and SK hynix.

SK hynix had been trading near its highs for about a month, while Samsung Electronics had been range-bound for nearly two months.

After a strong advance, repeated failures to break higher can change investor sentiment.

At first, investors expect a pause before another leg higher.

But repeated resistance can create doubt about whether momentum has faded.

When other sectors begin to outperform at the same time, capital may shift out of semiconductors.

That does not mean Samsung Electronics and SK hynix are no longer important; both remain central to any broader market rebound.

12. The most important points not always highlighted elsewhere

First, this is not only about Meta; it reflects a change in the AI investment cycle.

The market is shifting from rewarding spending intensity to demanding monetization.

This has direct implications for AI semiconductor valuations.

Second, Meta’s stock strength is a mixed signal for semiconductor suppliers.

Higher profitability at Meta is positive for Meta, but it also raises concerns that future demand for equipment and memory could slow.

Third, the Kospi’s decline reflects its semiconductor concentration.

Because Samsung Electronics and SK hynix carry substantial index weight, a weaker AI sentiment can pull the broader market lower.

Fourth, foreign selling may reflect more than profit-taking.

Currency weakness, yield pressure, risk reduction, and portfolio reallocation may all be involved.

Fifth, the next leadership group may already be forming during the decline.

Stocks such as Naver, Korea Electric Power, and financials may offer clues to the next rotation.

13. Key indicators investors should monitor now

1) Whether foreign selling continues

If foreign outflows do not stop, Kospi recovery may remain limited.

2) Whether institutions also keep selling

Concurrent selling by foreigners and institutions significantly increases downside pressure.

3) KRW/USD trends

A stable won improves the likelihood of foreign flow recovery.

4) U.S. 10-year Treasury yields

Higher yields weigh on Nasdaq and AI growth stocks.

5) Micron and the Philadelphia Semiconductor Index

These are leading indicators for Korean semiconductor stocks.

6) Trading volume in Samsung Electronics and SK hynix

The key question is whether rebounds are supported by volume.

7) Relative strength in non-semiconductor sectors

Sectors that hold up during the decline may become the next leaders.

14. Positioning: avoid both panic and overconfidence

This decline should not automatically be treated as the start of a crash.

At the same time, the combination of AI semiconductor sentiment, foreign flows, yields, exchange rates, and China-related memory concerns makes it difficult to dismiss as a routine pullback.

At this stage, investors should review cash levels and portfolio diversification rather than chase weakness aggressively.

For those with large semiconductor exposure, reducing concentration risk may be appropriate.

For long-term investors with conviction in quality names, weakness may still offer a phased entry opportunity.

The key is not to make a single, immediate judgment.

Any recovery should be confirmed by foreign flows, the exchange rate, yields, and U.S. equity conditions.

There is no permanent leader and no permanent loser in the market.

When capital begins to rotate, flexibility matters more than conviction.

< Summary >

The core issue behind the Kospi decline is the market’s reading of Meta’s signal that AI investment growth may slow.

Meta rose on the prospect of monetizing surplus compute capacity and exploring a cloud business, but the signal was negative for the broader GPU, HBM, memory, and AI equipment supply chain.

Because the Kospi is heavily weighted toward Samsung Electronics and SK hynix, the index was hit harder.

Foreign and institutional selling, a weaker won, and higher U.S. 10-year yields added pressure.

Apple’s discussions with Chinese memory suppliers also increased concern over commodity memory competition.

At the same time, stocks such as Naver, Korea Electric Power, and financials have shown relative resilience, suggesting that sector rotation may already be underway.

For now, the appropriate approach is to monitor flows, yields, exchange rates, and U.S. semiconductor stocks rather than chase the decline.

[Related Articles…]

- AI Semiconductor Cycle and the Outlook for Korean Equities

- How KRW/USD Weakness Affects the Kospi and Foreign Flows

*Source: [ Jun’s economy lab ]

– 메타발 쇼크로 무너지는 코스피, 진짜 이유 분석