● Wall Street SELL Frenzy

The Reason Wall Street Suddenly Shouted “SELL”: Samsung Electronics and SK Hynix Plunge, Has the AI Semiconductor Cycle Ended?

The core point of this article is not simply, “Samsung Electronics posted good earnings, so why did the stock fall?”

The truly important point is that Wall Street’s view of memory semiconductors has split into two camps.

One side believes “AI semiconductor demand will remain strong through 2027,” while the other warns, “from here on, we need to be careful about a peak-out.”

On top of that, SK hynix ADR U.S. listing, second-quarter earnings announcements from Big Tech, long-term supply agreements (LTAs), and the risk from China’s open-source AI models are all converging, making the market react very sensitively.

Today, based on the flow of Wall Street reports mentioned in the original text, let’s organize the causes of the sharp declines in Samsung Electronics and SK hynix, the AI memory semiconductor industry, U.S. stock market second-quarter earnings outlook, and the interest-rate outlook all at once.

1. News Core Point: Earnings Were Good, So Why Did the Stock Plunge?

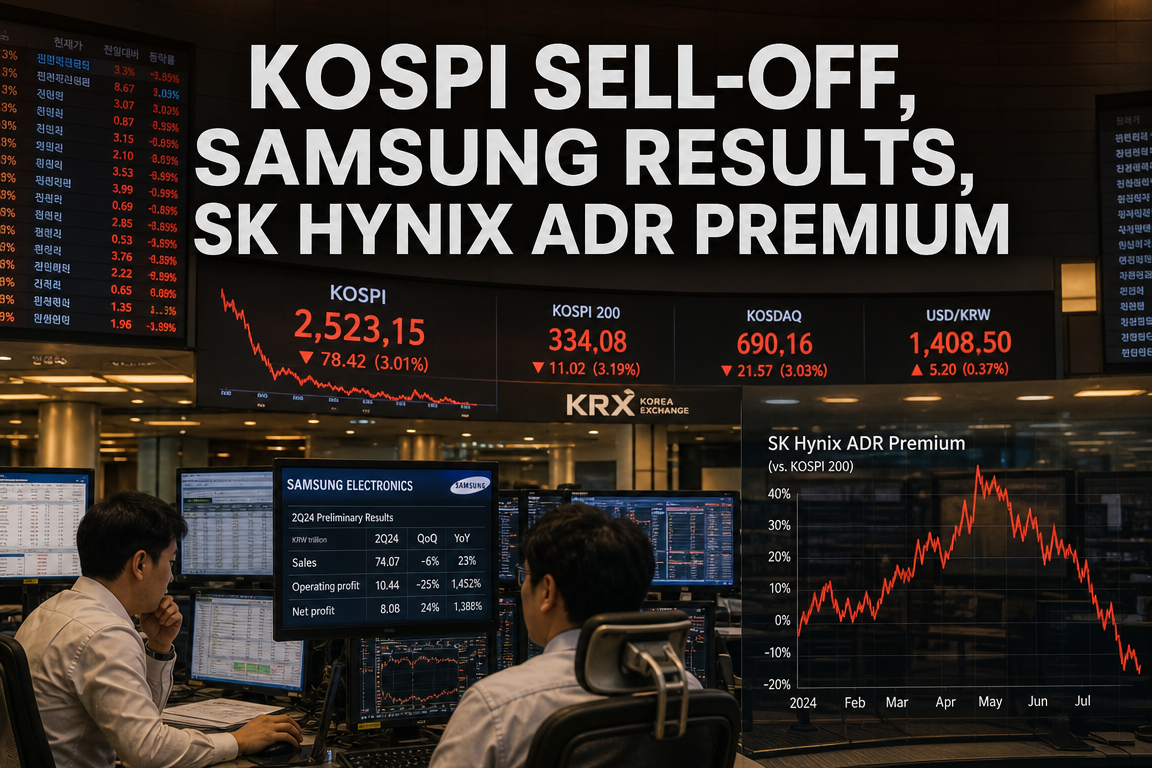

The first thing that shook the market was Samsung Electronics’ earnings surprise.

The original text explains that Samsung Electronics’ operating profit came in far above market consensus.

What stands out in particular is that even though the results beat consensus, the stock still plunged.

Normally, it is easy to think, “If earnings are good, the stock goes up,” but the real market is not that simple.

This decline was closer to a classic “buy the rumor, sell the news” pattern.

The market had already priced in much of Samsung Electronics’ and SK hynix’s earnings improvement, and once the good numbers actually came out, strong profit-taking emerged.

The KOSPI fell sharply, and not only SK hynix and Samsung Electronics, but also U.S. semiconductor stocks, Micron, SanDisk, and the Philadelphia Semiconductor Index came under pressure together.

In other words, this decline should be seen not as a simple Korea stock market issue, but as a reassessment of the entire global AI semiconductor value chain.

2. Wall Street Report ① UBS: “Buy the U.S. ADR Instead of the Korean-Listed Hynix”

The report cited as the direct supply-demand trigger for this sharp drop is UBS’s report.

UBS expressed the view that investors should sell SK hynix shares listed in Korea and buy the SK hynix ADR to be listed in the United States.

The reason this matters is not simply that “Hynix is bad.”

Rather, UBS’s logic is closer to “SK hynix itself is attractive, but the U.S. ADR could receive a higher premium.”

- For U.S. investors, ADR trading is more convenient.

- Trading costs and FX conversion burdens are lower.

- U.S. market liquidity is much deeper.

- Like TSMC, the ADR could trade at a premium to the local listing.

- Foreign capital that exits Korean stocks could flow into the U.S. ADR.

Because of this structure, short-term selling pressure may hit SK hynix listed in Korea.

On the other hand, if strong buying emerges after the U.S. ADR listing, a positive re-rating effect could later spill back into the Korean-listed stock.

In the end, the supply-demand situation around the SK hynix ADR around July 10 is a very important event.

3. Wall Street Report ② Morgan Stanley: “The Memory Current Is Changing”

Morgan Stanley took a somewhat ambiguous stance on memory semiconductors.

The key phrase in the report was “Changing Tides”, meaning a shift in the current.

This phrase itself weighed on the market.

Morgan Stanley posed three questions.

- Has AI investment ended?

- Can long-term supply agreements create a re-rating for memory companies?

- Is the memory cycle at a peak, or can it extend further?

Still, the conclusion was not fully negative.

The view was that AI investment could continue, long-term supply agreements are structurally positive, and it is still difficult to say the cycle has definitely peaked.

Even so, the market reacted nervously because of the headline.

Investors were more sensitive to the phrase “the current is changing” than to the conclusion that the sector remains attractive.

4. Wall Street Reports ③ Nomura, BofA, and JPMorgan: “AI Memory Demand Is Still Strong”

In contrast, Nomura, Bank of America, and JPMorgan presented a much more positive view of the memory industry.

Nomura sees rising global data center capital expenditures lifting memory demand over the long term.

Based on the original text, related data center investment was said to rise from about $60 billion in 2024 to about $1.4 trillion by 2030.

If that forecast is correct, AI infrastructure investment is not a short-term theme but a long-term industry cycle that could reshape the global economic outlook.

Bank of America gave a similar view.

Its analysis suggests that it may not be until 2033 that memory supply can fully catch up with demand.

JPMorgan also said the recent correction looks more like a buying opportunity, and that meaningful new supply before 2028 will not be easy.

In other words, within Wall Street, the view that still remains strong is not “the memory cycle is over,” but rather “there may be room for a rebound after the correction.”

5. UBS’s Long-Term Outlook: DRAM Shortages Possible Through 2027

UBS favored the ADR in the near-term supply-demand picture, but it acknowledged strong demand for the memory industry itself.

According to UBS’s outlook, DRAM demand could remain well above supply even in 2027.

It especially sees memory shortages not only in data center DRAM, but also in notebooks, smartphones, and PCs.

In that case, memory prices could remain elevated through 2028.

The original text explained that SK hynix and Samsung Electronics’ operating profit forecasts for 2026, 2027, and 2028 are far above consensus.

But there is an important point investors need to keep in mind.

These projections are based on the assumption that memory prices, HBM shipments, Big Tech AI investment, and long-term supply contract terms all remain favorable.

So more important than the numbers themselves is the direction.

At a minimum, Wall Street appears to believe that the profit levels of memory companies could become fundamentally different in 2026–2027 compared with the past.

6. Why Does the Argument for Undervaluation in Memory Semiconductors Arise?

Memory companies have traditionally traded at low P/E multiples.

The reason is simple.

The memory industry is a cyclical industry.

When prices rise, profits surge, but when supply increases, prices collapse and profits quickly deteriorate.

That is why the market has not tended to give Samsung Electronics and SK hynix high valuations.

But this AI cycle is different from the past.

- HBM demand is structurally increasing.

- High-performance DRAM demand for AI servers is steadily growing.

- Big Tech is trying to secure supply in advance through long-term supply agreements.

- HBM production partly crowds out general DRAM supply.

- Even if supply grows, actual effective supply may remain constrained.

If this structure is correct, memory semiconductor companies could be re-rated not as simple cyclical companies like before, but as key suppliers to AI infrastructure.

That is the center of the undervaluation case for Samsung Electronics and SK hynix.

7. What the Market Fears Most: Peak-Out in DRAM and NAND Prices

Another reason the stock plunged is concern about peak-out in memory prices.

Recently, spot prices for DDR5 DRAM rose to very high levels, and DDR4 and NAND prices also showed strength.

In this kind of situation, investors naturally ask:

“Can prices keep rising from here?”

Bloomberg sees the possibility of oversupply once new fabs are completed starting in the second half of 2027.

The logic is that if Samsung Electronics, SK hynix, and Micron each secure new production capacity, supply and demand could normalize in 2028.

However, there are variables in this analysis.

HBM is less efficient to produce than general DRAM and uses more wafers.

In other words, the more HBM is produced, the less general DRAM supply there may be.

Because of this, it is hard to simply say “more fabs = oversupply.”

Since the three major memory makers have also experienced past cycle collapses, they may be limited in their willingness to aggressively expand supply.

8. TrendForce Interpretation: Prices Are Not Falling, Just Rising More Slowly

TrendForce’s recent memory price outlook has also been widely discussed in the market.

Some interpreted it as a “sign of declining memory prices,” but the original text sees that interpretation as excessive.

The key is not a price decline, but a slowdown in the pace of increase.

For example, the previous view had DRAM average selling prices rising 3–8% per quarter, but the new forecast actually presented even higher increases, according to the explanation.

Bank of America also sees DRAM prices rising by double digits in the third quarter, with further upside possible in the fourth quarter.

So in the near term, the upward trend in memory prices is still alive.

The question is whether this trend can continue beyond 2027.

9. The Difference Between 2026 and 2027: From Price Gains to HBM Volume Growth

To understand this cycle, we need to separate 2026 and 2027.

Profit growth in 2026 is likely to be driven mainly by rising DRAM and NAND prices.

In other words, in P × Q, P, or price, is the key.

But starting in 2027, HBM could begin lifting both P and Q at the same time in earnest.

Looking at Nvidia’s next-generation AI chip roadmap, the transition from Blackwell in 2026 to Rubin in 2027 is likely to increase HBM content.

The original text explains that Blackwell Ultra may contain around 192GB of HBM, and Rubin could rise to around 288GB.

That is roughly a 50% increase in HBM content per chip.

On top of that, moving from HBM3E to HBM4 could also raise unit prices.

With both volume and price rising, HBM revenue could grow exponentially.

That is why Wall Street is projecting such large profit gains for Samsung Electronics and SK hynix in 2027.

10. AI Bottlenecks: Why Memory and Networks Are Becoming More Important Than GPUs

The core point that is relatively under-covered in other news is that the location of the AI bottleneck is shifting.

As AI models grow larger and inference demand rises, GPU performance is improving quickly.

But memory bandwidth and network performance are not improving as fast as GPUs.

That gap creates a bottleneck.

In particular, if technologies like KV cache offloading spread, demand for high-performance memory could increase even more.

As AI inference surges, memory capacity, bandwidth, power efficiency, and interconnectivity between servers become more important than simple GPU count.

In this structure, the strategic value of HBM and high-performance DRAM becomes even greater.

In the end, the core question in AI semiconductor investment is not “Should we only look at Nvidia?” but “Who solves the memory bottleneck needed to actually run Nvidia chips?”

11. NAND Outlook: AI Demand Is Pushing Storage Up as Well

If we only look at DRAM and HBM when discussing memory, we are seeing only half the picture.

NAND also matters.

According to Morgan Stanley’s outlook, NAND shortages could continue through 2027 and 2028.

As AI data centers expand, demand for training data, inference logs, vector databases, and model checkpoint storage rises as well.

In other words, AI investment is not only about GPUs and HBM, but is also linked to SSD and NAND demand.

As AI data centers grow, storage demand could also rise structurally.

12. Three Events to Watch Going Forward

From here on, it is more important to track three events than simply watch share-price swings.

12-1. U.S. Market Flow After the SK hynix ADR Listing

The first is how much U.S. capital comes in after the SK hynix ADR listing.

If U.S. investors buy aggressively, SK hynix could be re-rated as a global peer.

On the other hand, if the flow is weaker than expected, short-term disappointment selling could emerge.

12-2. Big Tech Second-Quarter Earnings at the End of July

The second is the second-quarter earnings of U.S. Big Tech companies.

It matters how much hyperscalers such as Microsoft, Google, Meta, Amazon, Apple, and Nvidia maintain AI capital expenditures.

In particular, the market may react more sensitively to CAPEX guidance than to revenue.

If Big Tech says, “We will continue increasing AI investment,” that is positive for memory semiconductors.

Conversely, if they say, “We will slow the pace of investment,” the short-term correction could last longer.

12-3. Long-Term Supply Agreement Content

The third is long-term supply agreements.

This is the most important.

If memory companies sign long-term price and volume contracts with Big Tech, earnings volatility declines.

Then the market may no longer view memory companies only as low-P/E cyclical companies like in the past.

If the share of long-term supply contracts rises to 50% or 70%, the re-rating potential increases.

On the other hand, if contract shares are low or price downside protection is weak, the view that “memory is indeed a cyclical industry” may persist.

13. The Most Important Point Rarely Discussed in Other YouTube Videos or News

The most important point is not the “memory price outlook,” but whether the profit volatility of memory companies can be reduced.

Stocks do not rise simply because earnings are good this quarter.

The market evaluates how repeatable and stable those earnings are.

In the past, memory companies did not receive high valuations even when profits were strong.

That was because the market believed profits could collapse one or two years later.

But if AI data center customers begin buying HBM and high-performance DRAM under long-term contracts, the story changes.

Long-term supply agreements could become the mechanism that transforms memory companies from simple manufacturers into key suppliers to AI infrastructure.

That is why the key for Samsung Electronics and SK hynix stock going forward is less about “How much was operating profit this quarter?” and more about “How stably are profits secured after 2027?”

If that is confirmed, Korean semiconductor stocks could be re-rated as they are compared with AI infrastructure companies in the U.S. stock market.

14. Risk ① The Rise of Chinese Open-Source AI Models

The most interesting risk mentioned in the original text is Chinese open-source AI models.

Recently, Chinese AI startups have been releasing models that are extremely cheap relative to performance.

Some benchmarks show scores competitive with top global models.

The problem is price.

If Chinese models can handle similar tasks at much lower cost, monetization at frontier AI companies like OpenAI or Anthropic could face pressure.

If AI service prices fall, Big Tech may lose the rationale for continuing to invest massive amounts of CAPEX.

Of course, there is also an opposing argument.

If AI models become cheaper and more accessible, usage could explode, increasing overall computing demand even more.

In other words, Chinese open-source AI models are a short-term pricing risk, but in the long run they could also be a factor expanding AI usage.

15. Risk ② The Possibility That Big Tech Will Talk About Slowing CAPEX

The second risk is what Big Tech says.

Recently, as Meta mentioned selling some computing resources and improving investment efficiency, the market started to see the possibility of a “slowing pace of AI investment.”

The interesting thing is that if companies say they will reduce CAPEX, share prices can rise in the short term.

Investors like cost reductions and better cash flow.

But from an AI semiconductor perspective, comments about CAPEX cuts are a burden.

If hyperscalers actually reduce their investment plans, HBM, DRAM, network equipment, and server demand outlooks could also weaken.

So the core of this second-quarter earnings season is not EPS, but CAPEX guidance.

16. U.S. Stock Market Second-Quarter Earnings Outlook: Are Tech Stocks Just Expensive?

The original text used FactSet Earnings Insight data to explain tech valuations.

The core point is that tech stocks may not be as expensive as they seem.

Analysts say the forward P/E for tech stocks has fallen below the five-year average.

The reason is not that stock prices rose less, but that future EPS expectations increased faster.

Forward P/E is calculated by dividing share price by expected earnings over the next 12 months.

If earnings expectations rise quickly, the P/E can fall even when the stock price rises.

Projections for revenue growth and EPS growth in S&P 500 tech stocks have recently been revised upward.

Therefore, it is still hard to justify viewing the entire U.S. market as an “AI bubble.”

Of course, some individual stocks may be overheated, but tech stocks as a whole are defending their valuations through strong earnings growth.

17. Interest-Rate Outlook and Oil: The Macro Environment Is Not as Bad as It Seems

Another variable investors worry about is interest rates.

But the original text explains that stable oil prices could reduce rate pressure.

After the Hormuz Strait risk eased, WTI crude quickly stabilized.

There is also analysis that by 2027, oil supply may exceed consumption.

If oil falls back to the low $60s per barrel, inflation pressure eases.

If inflation stabilizes, the Fed’s chance of cutting rates can revive again.

In other words, the interest-rate outlook is not necessarily only negative for tech stocks.

If earnings improve, oil stays stable, and rate-cut expectations hold, U.S. equities and AI-related stocks can receive higher valuations again.

18. Investment View Summary: Sell Now or Hold On?

This correction is a very uncomfortable phase for investors.

In particular, Samsung Electronics and SK hynix had risen a lot in a short period, so strong profit-taking can emerge.

But looking only at fundamentals, it is still hard to say they have broken down.

- AI semiconductor demand remains strong.

- HBM supply is structurally constrained.

- DRAM and NAND prices are in a short-term uptrend.

- If Big Tech CAPEX is maintained, the demand outlook can strengthen further.

- If long-term supply agreements are confirmed, memory companies may have re-rating potential.

Still, the risks are clear.

- Supply-demand volatility around the SK hynix ADR listing is high.

- Big Tech may mention slowing CAPEX.

- There is concern about new supply increases after 2027.

- Chinese open-source AI models may intensify debate over AI investment profitability.

- Profit-taking pressure remains after the short-term surge.

Therefore, right now, event confirmation is more important than either “sell unconditionally” or “buy unconditionally.”

In particular, you must check the late-July Big Tech earnings and statements related to long-term supply agreements from Samsung Electronics and SK hynix.

If those two come out positive, this correction could become a medium-term buying opportunity.

Conversely, if CAPEX slowdown and lack of LTAs are confirmed at the same time, the correction in memory semiconductors could last longer.

19. Checklist: Key Indicators to Watch Going Forward

- Trading volume and premium status in the U.S. market after the SK hynix ADR listing

- HBM supply agreement announcements from Micron, Samsung Electronics, and SK hynix

- Changes in Nvidia’s Blackwell and Rubin shipment outlooks

- AI CAPEX guidance from Microsoft, Google, Meta, and Amazon

- DRAM spot prices and the spread versus contract prices

- Whether NAND price increases continue

- Uptrend in usage of Chinese open-source AI models

- WTI crude oil and the direction of the U.S. 10-year Treasury yield

- Whether EPS forecasts for S&P 500 tech stocks are being revised upward

< Summary >

The sharp declines in Samsung Electronics and SK hynix were the result of profit-taking, a shift in ADR demand, and concerns about memory peak-out, rather than weak earnings.

UBS preferred the U.S. ADR over Korea-listed SK hynix, and Morgan Stanley mentioned the possibility of a shift in the memory backdrop.

Meanwhile, Nomura, BofA, and JPMorgan believe AI data center investment and HBM demand could remain strong through 2027.

The core point is long-term supply agreements.

If LTAs expand, memory companies could be re-rated not as simple cyclical industries, but as key players in AI infrastructure.

Going forward, the most important things to watch are SK hynix ADR supply-demand trends, Big Tech second-quarter earnings, AI CAPEX guidance, and HBM contract details.

Short-term volatility is large, but the fundamentals of AI semiconductors do not yet appear to have broken down.

[Related Articles…]

- AI Semiconductor Cycle and HBM Investment Strategy Overview

- Key Checkpoints for the U.S. Stock Market Second-Quarter Earnings Season

*Source: [ 월텍남 – 월스트리트 테크남 ]

– [속보]돌변한 월가”SELL” 오늘 월가 보고서 10개 내용 총정리 + 2분기 실적 미리보기