● Rate Shock, Inflation, FX Chaos, Debt Risk

Bank of Korea Base Rate Hike Immediate Analysis: Inflation, KRW-USD Exchange Rate, and Household Debt Shift the Policy Stance

This Bank of Korea rate hike is not a simple “rates are up” event.

Consumer inflation has returned to the 3% range, the KRW-USD exchange rate remains elevated, and Seoul apartment prices and household debt growth are weighing on financial markets at the same time.

Added to this are post-Middle East war pressures from higher global oil prices and import costs, the divergence in money supply growth between Korea and the United States, and the narrowing of the Korea-U.S. policy rate gap, all of which help explain why the Bank of Korea has raised rates for the first time in 3 years and 6 months.

The key point is straightforward.

The Bank of Korea has begun placing higher priority on price stability, exchange rate stability, and financial stability than on growth support.

1. Bank of Korea raises the base rate for the first time in 3 years and 6 months

The Bank of Korea Monetary Policy Board has decided to raise the base rate.

Since the last rate hike was in January 2023, this decision marks the first increase in about 3 years and 6 months.

It also represents a policy reversal after roughly 1 year and 2 months of rate cuts and later holding the rate steady.

- Until January 2023, policy remained in a tightening phase to respond to high inflation.

- The Bank of Korea then maintained a relatively high base rate around 3.5%.

- From October 2024 to May 2025, it lowered the base rate four times.

- Since May 2025, it held the rate unchanged for about 1 year and 2 months.

- In July 2026, it shifted back to a rate hike.

The original text includes some references to a “hold,” but the central point is that the Bank of Korea raised the base rate.

As a result, the Korea-U.S. policy rate gap has narrowed from 1.25 percentage points to around 1.00 percentage point.

This reflects Korea’s rate increase while the United States kept rates unchanged.

2. Why now: three policy lenses used by the Bank of Korea

When setting policy, the Bank of Korea primarily weighs three factors.

First is price stability.

Second is financial stability.

Third is growth stability.

This rate hike appears to reflect a stronger emphasis on price stability and financial stability.

If the economy were in a severe downturn, a rate hike would have been difficult.

Instead, the Bank of Korea appears to believe the Korean economy can still absorb the move, supported by semiconductor exports and other factors.

3. Price stability: CPI at 3.2% and import cost pressures have risen again

The most direct driver of the rate hike is the rebound in inflation.

Korea’s consumer price inflation has risen to 3.2%.

That is a notable change from the 2.6% level referenced at the previous Monetary Policy Board meeting.

- The previous CPI reading was around 2.6%.

- Recent CPI has risen to 3.2%.

- Core inflation has also increased to around 2.5%.

- Import price inflation in dollar terms remains around 8%.

- In won terms, import prices are up in the 20% range, which is a heavier burden.

The key issue is import prices.

Korea relies heavily on imported energy and raw materials.

When global oil and commodity prices rise, the effects filter through to producer prices and consumer prices with a lag.

When the KRW-USD exchange rate is also high, the won cost of those imports rises further.

In other words, even if global oil prices stabilize somewhat, a weak won can keep import cost pressures elevated.

That is a major concern for the Bank of Korea.

With inflation back in the 3% range, keeping rates too low could unanchor inflation expectations.

4. Exchange rate stability: KRW-USD weakness was a key trigger

The exchange rate is as important as inflation in this decision.

The KRW-USD rate has remained at a high level, even outside of crisis conditions such as the Asian financial crisis or the global financial crisis.

The original text notes that the exchange rate was trading near the upper end of the 1,500 won range, which is a significant source of pressure.

A weaker won may help exporters in some respects.

However, it increases costs for importers, energy, food, and everyday consumer goods.

Exchange rate weakness therefore feeds into inflation pressure.

Authorities have used foreign exchange reserves to intervene through dollar sales.

Based on the original text, net FX sales of about $22.4 billion in Q4 2025 and about $13.6 billion in Q1 2026 were cited.

Such measures can reduce short-term volatility, but they are limited in addressing structural currency weakness.

That is why a base rate hike is a more fundamental policy tool.

Higher rates narrow the Korea-U.S. differential and can improve the relative appeal of won assets.

This is not a cure-all for exchange rate weakness, but it is a practical response when currency volatility is feeding inflation pressure.

5. The hidden risk in M2 growth: Korea’s liquidity expansion outpaced the U.S.

One of the most important factors in this analysis is M2 money supply growth.

The original text highlights that Korea’s M2 growth rate has moved faster than the United States.

- Korea’s M2 growth rate was cited at 11.7% before revision.

- U.S. M2 growth was cited at roughly 4.7% to 5.6%.

- Even after revision, Korea’s liquidity growth remains faster than that of the U.S.

M2 is a key measure of liquidity in the financial system.

Rapid money growth can lift asset prices, add to inflation pressure, and weaken the currency.

If Korea’s money supply grows faster than that of the U.S., the won is more likely to face depreciation pressure.

That can translate into further upward pressure on the KRW-USD exchange rate.

The original text suggests that Korea’s M2 growth may continue through May and June 2026, then slow in July and August.

By contrast, U.S. M2 growth may begin accelerating more meaningfully from August 2026.

If this path materializes, the exchange rate outlook in the second half of the year should be assessed not only through rate differentials but also through relative money supply growth.

This is one of the less discussed but most important points.

Interest rate differentials matter, but money supply growth may be a deeper driver of exchange rates and asset prices.

6. Property and household debt: Seoul apartment gains are becoming a financial stability risk

Another reason for the rate hike is the housing market and household debt.

When Seoul apartment prices rise strongly, mortgage borrowing tends to increase, which in turn pushes household debt higher.

Excessive household debt raises financial stability risks.

The original text argues that while nationwide apartment prices appear to be rising, the real driver is Seoul-based price strength.

Price gains in the six metropolitan cities and other regions are not as strong as those in Seoul.

In other words, the current housing issue is not broad-based overheating but concentrated price pressure in Seoul.

The government is also considering or advancing tax changes that would increase the burden on multiple-home owners and ultra-high-priced homes.

Combined with tighter financial regulation, housing market regulation, and a higher base rate, this may help slow Seoul apartment price gains.

This rate hike is therefore not only about inflation.

It also reflects concerns over housing prices, household debt, and broader financial stability.

7. Growth stability: the economy remained strong enough to absorb the hike

A rate hike creates pressure on growth.

Higher borrowing costs can weigh on consumption and investment, and raise corporate funding costs.

Even so, the fact that the Bank of Korea raised rates suggests it does not view the economy as being in a severely fragile state.

The Bank of Korea has projected Korea’s 2026 GDP growth at 2.6%.

That is 0.6 percentage points higher than the February forecast.

Growth in 2027 is also expected to remain relatively stable.

Part of that improvement is tied to semiconductor exports.

Still, the economy appears resilient enough for the Bank of Korea to prioritize price stability and financial stability over additional support for growth.

In summary, inflation is elevated, the exchange rate is unstable, and Seoul housing and household debt remain a concern.

At the same time, growth is holding up better than expected.

That combination strengthens the case for a rate hike.

8. Global rate trends: policy is no longer moving in one direction everywhere

This rate hike is not an isolated domestic event.

It comes amid a global policy environment in which central banks are diverging based on local conditions.

- Japan has already moved into a rate hike cycle.

- The euro area has also raised rates.

- Korea has now raised its base rate.

- Australia, New Zealand, Indonesia, and the Philippines have also used rate hikes to respond to inflation and exchange rate pressure.

- By contrast, the United States, the United Kingdom, Canada, and Sweden have maintained a hold stance.

This is a period of highly differentiated policy responses.

Middle East conflict has added volatility to global oil prices, and inflation and currency pressures differ across countries, making synchronized central bank action less likely.

For Korea, high dependence on imported commodities and high sensitivity to exchange rates mean that a U.S. hold does not necessarily justify a Korean hold.

This rate hike reflects Korea’s own economic structure.

9. Bank of Korea Governor Shin Seong: holding rates was no longer sufficient

The original text also highlights remarks from the new Bank of Korea Governor Shin Seong.

The interpretation is that if the Middle East conflict persists, inflation pressures may continue, and exchange rate instability may require a policy response.

Over the past 1 year and 2 months, the Bank of Korea held rates steady while monitoring conditions.

But as import prices, consumer inflation, the exchange rate, and Seoul apartment prices all became more burdensome, a simple hold was no longer sufficient.

The hike also sends a signal to markets.

The Bank of Korea does not intend to react too slowly when inflation and the exchange rate weaken at the same time.

10. Policy outlook: likely pause in August, with a possible additional hike in October

The original text also outlines the likely policy path ahead.

After the July 16, 2026 rate hike, the Bank of Korea may pause in August.

It likely needs time to assess the effects of the hike on inflation, the exchange rate, housing, and growth.

- July 16, 2026: Bank of Korea rate hike decision.

- August 2026: likely hold if inflation and the exchange rate do not worsen materially.

- October 2026: possible additional rate hike.

- If inflation and the KRW-USD rate deteriorate again in July or August, another August hike cannot be ruled out.

The Federal Reserve schedule also matters.

The next U.S. rate decision is expected at 3:00 a.m. Korea time on July 30.

The original text suggests the Fed is likely to hold rates at that meeting.

If the Fed holds while the Bank of Korea keeps open the possibility of further tightening, the Korea-U.S. rate gap could narrow further.

That would support the exchange rate, but it would also add pressure to domestic borrowing costs and asset markets.

11. Market implications: how to view FX, bonds, equities, and property

Foreign exchange

The rate hike may partially reduce pressure on the won.

However, the KRW-USD rate is not determined by rate differentials alone.

Global oil prices, U.S. money supply growth, dollar strength, trade balances, and foreign capital flows also matter.

Bonds

A rate hike can lift short-term yields quickly.

If the market had already priced in the move, longer-term yields may be more limited, reflecting growth concerns.

Equities

Higher rates are generally negative for growth stocks and high-valuation names.

By contrast, banks and insurers may benefit relative to the broader market in a rising-rate environment.

Still, household debt risks should also be monitored for the financial sector.

Property

The hike is a headwind for Seoul apartment prices.

Higher mortgage costs reduce affordability and may curb speculative demand.

In combination with stronger tax policy and financial regulation, the rate hike may put pressure on high-end homes and multiple-home owners.

Household consumption

Highly indebted households may face greater interest expense.

That can weaken consumption.

This is one reason the Bank of Korea may prefer to wait in August rather than hike again immediately.

12. The most important point that is often underemphasized in other coverage

First, the true purpose of the rate hike is not only inflation control but also defense of the currency.

CPI at 3.2% matters, but so do the KRW-USD exchange rate and import cost pressure.

If the exchange rate does not stabilize, inflation will not stabilize easily either.

Second, FX intervention through reserve use has limits.

Dollar sales can reduce short-term volatility, but they cannot solve structural won weakness.

Monetary policy and liquidity management must work together.

Third, M2 growth is the key second-half currency variable.

If Korea’s M2 growth remains faster than that of the U.S., won depreciation pressure may persist.

Investors should track not only rate decisions, but also the relative pace of money supply growth in Korea and the U.S.

Fourth, Seoul property is not the direct target of monetary policy, but it is a major input.

The Bank of Korea does not directly set house prices.

But if Seoul apartment gains feed household debt growth and financial instability, they will affect rate decisions.

Fifth, this rate hike signals a change in policy priorities rather than a recession warning.

The Bank of Korea appears to believe the economy can still withstand the move.

Accordingly, it has shifted weight toward inflation, the exchange rate, and financial stability.

13. Key indicators to monitor going forward

- July and August CPI: if inflation remains in the 3% range, pressure for another hike may rise.

- KRW-USD exchange rate: the key issue is whether it remains anchored in the 1,500 won range.

- Import price inflation: a leading indicator reflecting oil, commodities, and the exchange rate.

- M2 growth: track the gap between Korea and the United States.

- Seoul apartment price index: a core measure of housing pressure and household debt risk.

- Household loan growth: a direct indicator of financial stability risk.

- U.S. FOMC rate decision: important for the Korea-U.S. rate gap and exchange rate direction.

< Summary >

The Bank of Korea has raised its base rate for the first time in 3 years and 6 months.

The main drivers are CPI at 3.2%, exchange rate instability, import price pressure, rising Seoul apartment prices, and concerns over household debt growth.

The Korea-U.S. policy rate gap has narrowed to about 1.00 percentage point.

The Bank of Korea appears to be placing greater weight on price stability and financial stability than on growth support.

An August pause is possible, but additional tightening remains on the table if inflation and the exchange rate stay weak.

The most important hidden variable is the gap between Korea and U.S. M2 growth.

To assess the second-half outlook for the exchange rate and asset markets, investors should monitor not only the base rate but also liquidity growth, import prices, Seoul property, and household debt.

[Related Articles…]

- KRW Exchange Rate Outlook and Key Second-Half Market Drivers

- How Bank of Korea Rate Changes Affect Property and Household Debt

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [속보] 한국은행, 3년 6개월만의 금리인상, 물가·환율 불안에 금리인상 단행 [즉시분석]

● Apple-Asia-AI-shock-AI-chip-slump

CXMT Reshapes the Semiconductor Cycle Debate; Why Apple Hit a Record High After Partnering With Alibaba

Today’s market focus was not simply that Apple rose and semiconductors fell.

The key points are threefold.

First, Apple set a new all-time high after moving to accelerate its China-specific on-device AI strategy with Alibaba and Baidu.

Second, ASML’s results pointed to a semiconductor supercycle, while the CXMT and CoreWeave developments reinforced concerns that memory semiconductors remain a cyclical industry.

Third, the impact of AI investment on U.S. growth and inflation, especially the debate over “dark output” not fully captured in GDP data, may shape the Federal Reserve’s rate path and the direction of U.S. equities.

On the surface, the session looked like a straightforward move higher in the Nasdaq, strength in Apple, and weakness in semiconductors. In reality, it reflected a collision between AI investment, semiconductor oversupply risk, China’s semiconductor ambitions, and the inflation debate.

1. U.S. Market Action: A Volatile Session Ended Higher Across the Three Major Indexes

U.S. equities were highly volatile overnight.

The market opened higher, turned negative intraday, and then rebounded late in the session as buying returned.

The Dow Jones Industrial Average rose 0.29%.

The S&P 500 gained 0.38%.

The Nasdaq advanced 0.62%.

Overall, investors rotated back into mega-cap technology names as earnings expectations for large-cap tech improved.

By contrast, semiconductors, which had rallied strongly recently, weakened as profit-taking met sector-specific risk.

Crude oil was largely stable, despite ongoing geopolitical tension related to Iran.

2. Sector Rotation: Capital Moved Into Big Tech While Semiconductors Sold Off

Sector performance showed clear differentiation within technology.

XLK, the technology sector ETF with heavy semiconductor exposure, fell 1.11%.

By contrast, XLC, which includes Meta and Alphabet, rose 1.73%.

The market was effectively signaling that AI remains constructive, but that the memory semiconductor price cycle has become more vulnerable.

This is the most important framework for understanding the session.

The long-term AI investment narrative remains intact.

However, rapidly rising memory prices and growing concern over future Chinese supply expansion prompted investors to reduce near-term risk exposure.

3. M7 Performance: Apple, Google, Amazon, and Meta Advanced; Tesla Lagged

Among the M7, Apple stood out most clearly.

Apple rose more than 4% and reached a new all-time high.

Alphabet gained 3.17%.

Amazon advanced 3.02%.

Meta rose 3.07%.

Tesla was the only M7 name to decline, falling 0.43%.

Markets are increasingly focusing not just on whether a stock is AI-related, but on whether AI translates into revenue growth and market-share recovery.

By that standard, Apple, Alphabet, Meta, and Amazon were viewed positively, while Tesla was left behind.

4. Apple’s Record High: China AI Strategy With Alibaba and Baidu

Apple’s sharp gain was driven by expectations around its AI strategy in China.

The company is moving to apply AI capabilities from Alibaba and Baidu to iPhones and iPads sold in China.

China remains a critical market for Apple.

Investor sentiment was also supported by reports that Apple recovered to second place in China smartphone market share in the second quarter.

For Apple, global AI models alone are not sufficient to navigate Chinese regulation and local ecosystem requirements.

Partnerships with domestic players such as Alibaba and Baidu are a practical solution for operating services in China.

This is not just a technology collaboration.

It could support iPhone sales recovery, expand on-device AI adoption, and help defend service revenue in China.

As a result, the market interpreted the move as both a reduction in China risk and a possible restart of the AI iPhone cycle.

5. Buffett Effect: A Comment That Supported Alphabet

Alphabet also benefited from comments by Warren Buffett.

In a CNBC interview, Buffett said he personally made the final decision to buy Alphabet in Berkshire Hathaway’s portfolio last year.

He also said he regretted not buying Google earlier.

The market viewed this as a strong positive signal.

Buffett also expressed some caution regarding the aggressive data center spending of hyperscalers and the AI infrastructure buildout, suggesting that parts of the investment cycle may be speculative.

Still, his remarks on Alphabet were clearly constructive.

He also indicated familiarity and confidence in Apple, given Berkshire Hathaway’s large position in the company.

Overall, the market interpreted Buffett’s remarks as a vote of confidence in both Alphabet and Apple.

6. ASML Results Pointed to a Semiconductor Supercycle

ASML’s second-quarter results were strong.

ASML is a critical supplier of lithography equipment used in advanced semiconductor manufacturing.

Its EUV systems are considered essential for leading-edge chip production.

Second-quarter revenue came in at 9.3 billion euros, above expectations.

Net income reached 2.9 billion euros, also above consensus.

Gross margin was 54%, better than anticipated.

More important was guidance.

ASML projected third-quarter revenue of 11.0 billion to 12.0 billion euros.

It also guided gross margin to 55% to 57%.

Full-year revenue guidance was raised materially, from 36.0 billion to 40.0 billion euros to 43.0 billion to 45.0 billion euros.

This indicates that customers continue to expand semiconductor manufacturing capacity.

The message is consistent with strong AI chip demand and continued investment by foundry and memory manufacturers.

7. ASML’s Largest Customer Base Is in Korea: Focus on Samsung Electronics and SK Hynix

ASML’s regional shipment mix also deserves attention.

In the second quarter, Korea accounted for 43% of shipments, the largest share.

In the first quarter, Korea accounted for 45%.

This reflects the importance of Samsung Electronics and SK Hynix as key customers.

Taiwan also represented a significant share, likely reflecting demand from TSMC.

ASML said it plans to produce 65 EUV systems this year, and to increase that by 30% next year.

For DUV systems used in mature-node production, the company plans to increase output by 30% this year and again by 30% in each of the following two years.

On this basis, the semiconductor cycle could remain strong at least through 2028.

However, strong demand does not necessarily mean semiconductor stocks can keep rising.

If supply grows too quickly, price pressure will eventually emerge.

8. Why Semiconductor Stocks Fell: CoreWeave’s Memory Contract Hedging Review

The first catalyst for semiconductor weakness was a report on CoreWeave.

CoreWeave is a neo-cloud company focused on AI data centers and GPU cloud infrastructure.

According to a Reuters report, the company is reviewing financial hedging measures tied to long-term memory semiconductor supply contracts for AI data centers.

The core issue is that memory prices are currently high, but future declines could make fixed high-cost contracts expensive.

This reinforces the view that memory semiconductors remain a highly cyclical business.

The market response reflected that concern.

Even if AI data center demand remains robust, there is no guarantee that memory prices will continue rising indefinitely.

When buyers themselves consider hedging against lower future prices, investors naturally begin to question whether the memory cycle is nearing a peak.

9. Why Semiconductor Stocks Fell: CXMT IPO and Oversupply Fears

The second issue was China’s CXMT.

CXMT is China’s leading DRAM producer and is widely viewed as a top-four global memory supplier.

The company is currently pursuing an IPO in Shanghai, and institutional demand reportedly reached 460-to-1.

However, the offering price and valuation were set below market expectations.

The IPO price was 8.66 yuan per share, or roughly $1.28.

At that level, the implied market capitalization is approximately 579 billion yuan, or about $85.2 billion.

That falls well short of the 1 trillion yuan valuation some market participants had expected.

Chinese media described the conservative valuation as a reflection of the cyclical nature of semiconductors.

The concern is that CXMT will likely use the capital raised to expand production capacity and increase R&D investment.

CXMT aims to increase wafer output rapidly and ultimately narrow the gap with Micron, while also pursuing a longer-term challenge to Samsung Electronics and SK Hynix.

If China expands memory output aggressively, the oversupply problems seen in steel, solar, and batteries could repeat in semiconductors.

This was the main reason the sector sold off today.

10. Apple’s Potential Purchase of CXMT Chips Also Matters

Markets also viewed the possibility that Apple may source chips from CXMT as a negative factor.

Stronger local supply-chain integration in China would help Apple manage its relationship with Chinese regulators.

However, it would be an unwelcome development for Korean and U.S. memory suppliers.

Inclusion of Chinese memory in Apple’s supply chain would mean more than a simple procurement decision.

It would signal that the supplier has been recognized for quality, stability, and scale by a major global customer.

If CXMT gains a larger role in Apple’s supply chain, pricing power across the global DRAM market could shift over time.

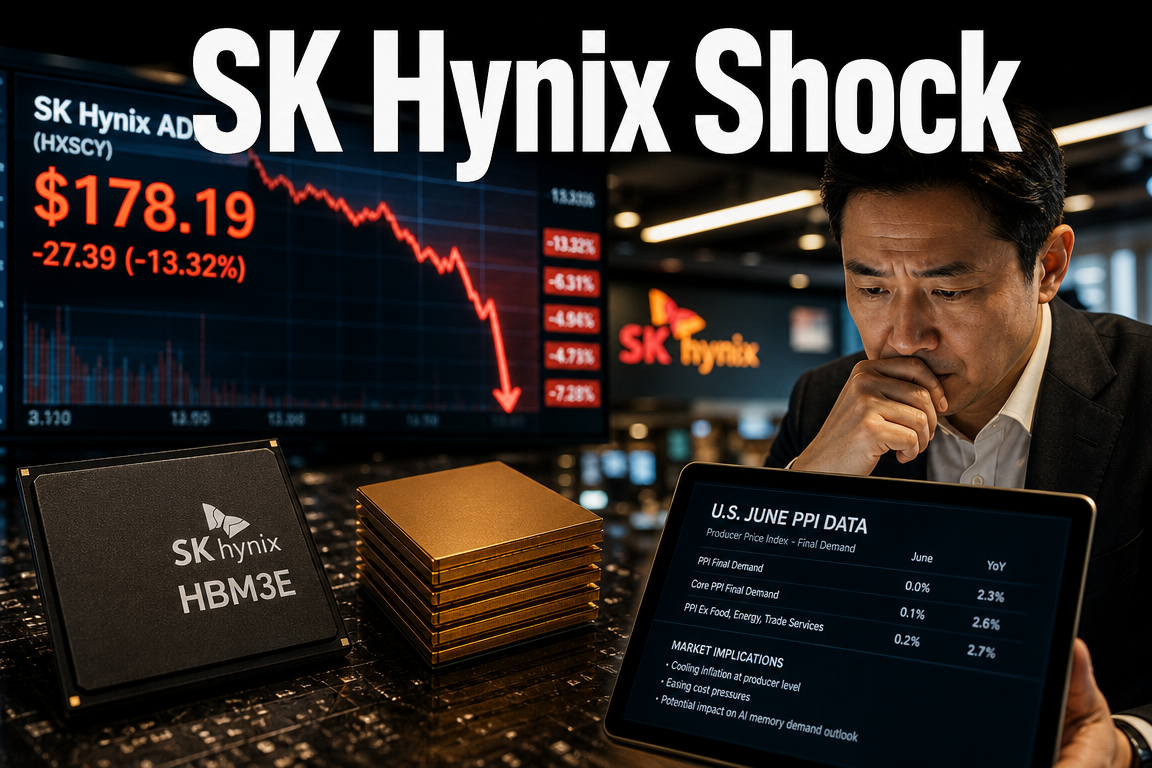

11. SK Hynix ADR Weakness: Premium Compression and Leveraged Product Flow

SK Hynix ADR also saw significant volatility.

After a large premium had built up between the Korean-listed shares and the ADR, profit-taking emerged.

As the conversion mechanism between the local shares and ADR became more efficient, investors moved to lock in gains.

The ADR fell sharply intraday, reaching around $176.

After SK Hynix rose more than 8% in Korea on the prior session, the ADR dropped more than 9% in the U.S., reducing the premium gap to roughly 26%.

Additional volatility was attributed to the launch of leveraged SK Hynix ADR products in the U.S. market.

Leveraged products can amplify buying in an uptrend, but they can also intensify selling pressure late in the session during declines.

For semiconductor investors, this means monitoring not only the local shares, but also ADRs, leveraged ETFs, and derivative flows.

12. Micron and SanDisk Slumped: The Entire Memory Group Came Under Pressure

Memory semiconductors were broadly weaker on the day.

SK Hynix ADR declined.

Micron fell 8.02%.

SanDisk dropped 8.12%.

Moves of that magnitude point to more than simple profit-taking.

The market is again questioning whether memory prices are close to a peak.

AI server demand remains strong.

HBM demand also appears solid.

But whether pricing strength can extend across DRAM and NAND is a separate question.

CXMT’s potential capacity expansion is becoming one of the most important medium-term variables for the memory industry.

13. Inflation Data Was Supportive, But Semiconductor Risk Dominated the Session

Earlier in the session, inflation data was interpreted positively.

PPI trends were stable, leading to expectations that July and August inflation could also remain manageable.

Normally, lower inflation pressure raises expectations for Fed rate cuts and supports U.S. equities.

But semiconductor risk dominated the session.

Investors focused more on the possibility of a turning point in the memory cycle than on a benign inflation backdrop.

It was a day when sector-specific risk took precedence over macro data.

14. Kevin Warsh’s View: Is AI Investment Inflation or a Productivity Shift?

Comments associated with Kevin Warsh also drew attention.

He maintained a firm anti-inflation stance.

He also emphasized that the key tool of monetary policy remains interest rates.

What stood out was the question of whether AI investment and rising semiconductor prices should be considered inflationary.

Warsh’s remarks can be interpreted as suggesting that AI-driven increases in chip prices do not necessarily constitute traditional inflation.

There are two reasons.

First, semiconductor prices can normalize if supply is expanded through additional factory investment.

Second, if price increases coincide with higher productivity and wage gains, they should not be viewed in the same way as general inflation.

This distinction will become increasingly important in U.S. economic analysis.

Depending on whether AI is seen as a cost driver or a productivity enhancer, the Fed’s policy response could differ.

15. A Key Issue Not Fully Captured in Other Coverage: The “Dark Output” Debate

One of the most important issues today is deeper than Apple’s record high or the CXMT story.

It is the fact that AI-driven productivity gains are not fully captured in GDP data.

Economists have recently described this as “dark output.”

When companies adopt AI, internal work in document drafting, code generation, customer service, data analysis, design, and R&D can improve dramatically.

However, those productivity gains are not immediately reflected in GDP statistics.

For example, spending on GPUs and data centers is captured in GDP.

But the effect of one employee completing five times more work with AI is difficult to measure directly.

Output from AI inference, automated analysis, internal decision-making improvements, and code generation all create economic value, but the measurement is imperfect.

That is the essence of dark output.

Goldman Sachs previously estimated that AI’s contribution to U.S. growth was close to zero, partly because of this measurement issue.

Imports of AI chips and equipment may not translate directly into GDP growth, but the productivity gains they enable are still not fully reflected in the data.

This debate could affect U.S. GDP, inflation, rate-cut expectations, and large-cap tech valuations.

16. The Core AI Dilemma: Spending Is Visible, But Performance Is Hard to Measure

AI investment is increasing rapidly.

Hyperscalers are investing heavily in data centers, GPUs, networking, and power infrastructure.

AI-related capital expenditure has reached a scale that is difficult to ignore at the macro level.

The problem is that it remains unclear how much of that spending is translating into measurable productivity gains.

Companies say AI is improving efficiency.

Investors want that efficiency to show up in revenue, margins, and cash flow.

The Fed needs to determine whether AI is inflationary or disinflationary.

Statistical agencies need to decide how to account for AI-generated output in GDP.

Ultimately, the next phase of the AI investment cycle will depend less on how much capital is being spent and more on how much real productivity is being created.

17. Investment Takeaway: AI Optimism and Semiconductor Cycle Concerns Are Now Colliding

The market is currently balancing two competing narratives.

One is the long-term growth story driven by expanding AI investment.

Under that framework, Nvidia, ASML, TSMC, SK Hynix, Samsung Electronics, and Micron are viewed as major beneficiaries.

The other is the risk of oversupply in memory semiconductors.

In that scenario, CXMT’s capacity expansion, China’s semiconductor self-sufficiency strategy, and the possibility of Apple using Chinese supply chains are viewed as negative factors.

The key question for investors is whether AI demand can continue absorbing incremental supply.

HBM demand is likely to remain strong.

But if China’s memory expansion accelerates, standard DRAM and NAND could face pricing pressure.

For that reason, semiconductor exposure now requires more granular selection rather than treating the sector as a single trade.

HBM, advanced packaging, EUV, AI servers, and commodity memory should be evaluated separately.

18. Key Variables to Watch Going Forward

First, monitor CXMT’s post-IPO expansion pace.

The key question is how much of the capital raised is converted into actual capacity growth.

Second, track whether Apple meaningfully adopts CXMT chips.

There is a major difference between testing and full supply-chain integration.

Third, watch memory pricing negotiations.

If AI infrastructure companies such as CoreWeave begin hedging long-term contracts, it may signal broader peak-cycle concerns.

Fourth, ASML’s order flow and delivery schedule remain important.

Strong guidance suggests that leading-edge semiconductor investment has not yet slowed.

Fifth, investors should watch how the Fed interprets AI productivity.

If AI is increasingly viewed as a productivity-enhancing force that lowers inflation, it could alter the policy outlook.

19. One-Sentence Summary of the Session

Today’s market reflected a simultaneous embrace of the view that AI remains intact and concern that memory semiconductors may be near a cyclical peak.

Apple set a new high on China AI strategy expectations.

Alphabet strengthened on Buffett-related support and AI optimism.

ASML confirmed that the long-term semiconductor investment cycle remains strong through its results.

At the same time, CXMT and CoreWeave raised warning signals for memory semiconductor investors.

Going forward, the key issue in semiconductors will be not simply whether AI is positive, but which chip categories are capturing the benefits of AI demand.

[Related Articles…]

AI Investment Cycle and the Hidden Driver of U.S. Growth

Semiconductor Cycle and China Memory Supply Risk

*Source: [ Maeil Business Newspaper ]

– [문지웅의 빅머니 LIVE] 中CXMT 반도체 사이클 논쟁에 기름 | 알리바바 손잡은 애플 사상최고가