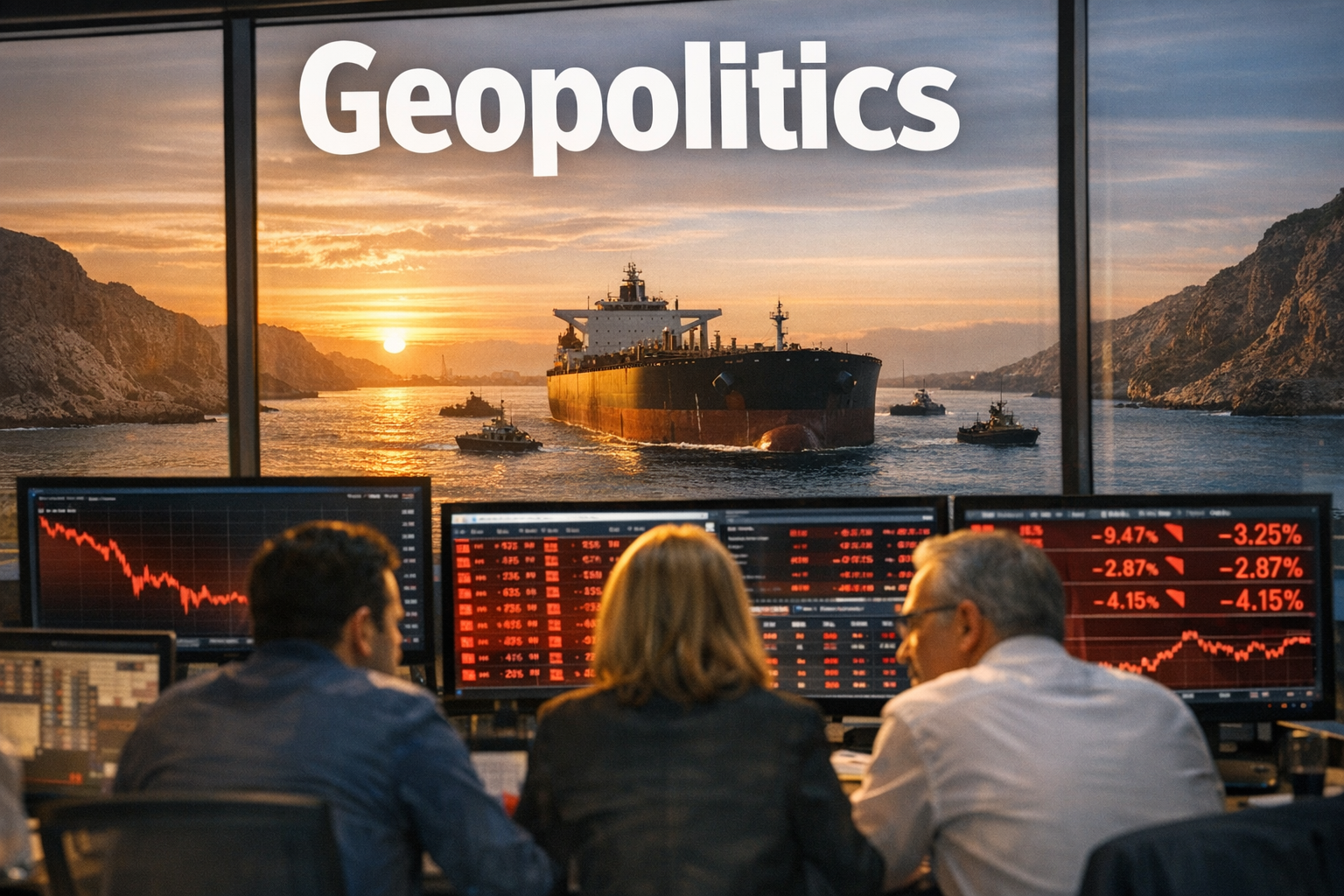

● Middle East War Shock, Liquidity Rally Dead, Stagflation Threat Ahead

Prolonged Middle East Conflict: The Key Variable Is the End of the Liquidity-Driven Rally

The critical issue in the current environment is not simply whether crude oil prices rise or fall.

If the Middle East conflict becomes protracted, it may alter the baseline trajectory of the global economy.

Growth, inflation, rate cuts, and the direction of asset markets such as equities and real estate may require a comprehensive reassessment.

A central risk is that the liquidity-driven rally anticipated by many investors could end sooner than expected, not due to recession alone but due to renewed inflation pressures consistent with a stagflation-type setup.

This report summarizes:how markets shifted after the pandemic,why the Russia–Ukraine war initiated a tightening regime,and why a prolonged Middle East conflict may reshape the 2025–2026 economic outlook.

1. Why Markets Are Volatile: Not the Conflict Itself, but Potential Regime Change

War-related headlines typically direct attention to oil first.

However, the current Middle East risk cannot be assessed as a simple commodity price shock.

The key question is whether the conflict is contained and short-lived or escalates and persists, forcing a re-pricing of the macro path.

- If contained/short-term: elevated volatility may be the primary effect

- If prolonged/escalatory: a reset of real activity, inflation, monetary policy, and asset-market trajectories becomes plausible

The market is moving from “temporary shock” to “revision of the base case.”

Short-term volatility can be measured in days or weeks; a macro path change can affect 12–24 months of asset-allocation strategy.

2. Two Recent Regime Shifts: The Pandemic and the Russia–Ukraine War

2-1. 2020 Pandemic: Real-Economy Shock + Easing + Liquidity-Driven Rally

The initial impact of the pandemic was a sharp contraction in real activity.

Consumption, production, mobility, and employment weakened simultaneously, driving a global growth shock.

Governments and central banks responded with coordinated stimulus.

- Ultra-low or zero policy rates

- Large-scale liquidity provision

- Expansionary fiscal policy and supplementary budgets

- Financial-market stabilization measures

The outcome was clear: despite weak real activity, abundant liquidity supported a rapid repricing of risk assets, including equities and real estate.

- Sharp real-economy contraction

- Ultra-accommodative monetary policy

- Large liquidity expansion

- Strong asset-market appreciation

The 2020–2021 rally was largely built on this framework.

2-2. 2022 Russia–Ukraine War: Supply Shock + Inflation Spike + Tightening Regime

The next inflection point was the Russia–Ukraine war.

Unlike pandemic-era demand disruption, the core issue shifted to supply chains and energy pricing.

Energy, food, and industrial commodity prices rose sharply, driving global inflation higher.

US CPI exceeded 9%, parts of Europe saw double-digit inflation, and Korea also experienced elevated inflation prints.

Policy priorities shifted toward inflation control over growth support.

- Rapid policy-rate hikes

- Quantitative easing ended or was reduced

- Valuation pressure across risk assets

- Corrections concentrated in growth and higher-duration assets

- Supply shock

- Inflation surge

- Accelerated tightening

- Liquidity withdrawal and risk-asset repricing

If the pandemic created a liquidity-driven rally, the Russia–Ukraine war contributed to its reversal.

3. Why a Prolonged Middle East Conflict Is High-Risk: Growth Down, Inflation Up

If the conflict persists, the principal risk is not oil prices alone, but a structure in which growth and inflation deteriorate simultaneously.

This aligns with a stagflation risk profile.

3-1. Growth: Downside Pressure on Global Activity and Korea’s Exports

A prolonged conflict can weaken business and consumer confidence.

Shipping and logistics risks rise, energy costs increase, and firms may become more conservative in investment and hiring.

Export-dependent economies such as Korea are particularly sensitive.

- Higher probability of export deceleration

- Rising manufacturing input costs

- Increases in shipping, insurance, and logistics costs

- Pressure on corporate margins

- Potential drag on private consumption

As a result, GDP may track below prior expectations.

3-2. Inflation: Higher Oil Prices Can Reignite Inflation Expectations

The Middle East is central to global energy markets.

If escalation risk rises, markets can price a geopolitical risk premium before any physical supply disruption occurs.

Higher crude oil and gas prices can feed into transportation costs, power prices, production costs, and broader consumer inflation.

The key transmission channel is expectations: once inflation expectations rise, central banks face tighter constraints.

3-3. Monetary Policy: Expected Rate Cuts May Be Delayed or Paused

Markets typically expect rate cuts when growth slows.

However, renewed inflation complicates the reaction function.

If growth weakens while inflation remains elevated, central banks may be unable to ease as quickly as markets anticipate.

The widely priced sequence—“slower growth → rate cuts → liquidity expansion → asset appreciation”—may shift to:“slower growth + inflation rebound → delayed cuts → asset repricing.”

4. Why the Liquidity-Driven Rally May End

For investors, the dominant support for recent risk-asset strength has been the expectation of an imminent shift from peak rates toward easing.

If inflation re-accelerates due to sustained geopolitical risk, this premise weakens.

- Rising inflation reduces the probability of a dovish pivot

- The pace of rate cuts may slow

- Expected liquidity may not translate into realized liquidity

- Overvalued assets may face sharper repricing risk

In this scenario, the liquidity-driven rally may end not because of recession, but because of renewed inflation.

5. Asset-Market Implications: Equities, Bonds, Real Estate, Commodities

5-1. Equities: Increased Probability of a Selective Market

Liquidity-driven rallies tend to lift most sectors simultaneously.

Under stagflation risk, dispersion typically increases and index-level breadth weakens.

- Higher valuation pressure on growth equities

- Preference for firms with pricing power

- Potential relative strength in energy, defense, and materials

- Pressure on cost-sensitive sectors (consumer, transport, chemicals)

- Greater differentiation by sector and company

5-2. Bonds: Growth Supports Rates, Inflation Limits the Move

Slowing growth is usually supportive for bonds.

However, inflation risk can offset this and increase rate volatility.

- Front end: reflects expectations for delayed easing

- Long end: tension between weaker growth and higher inflation expectations

- Higher bond-market volatility risk

5-3. Real Estate: Slower Recovery if Rate-Cut Expectations Fade

Real estate is highly sensitive to interest rates.

If rate cuts are pushed back, the recovery in transactions and prices may proceed more slowly than expected, particularly in credit-sensitive segments.

5-4. Commodities and Energy: Highest Near-Term Sensitivity

As Middle East risk increases, energy and traditional safe havens tend to react first.

- Higher probability of crude oil appreciation

- Greater volatility in natural gas

- Potential strength in gold

- Upward pressure on shipping and transport costs

These markets can move materially on expectations alone, even before supply disruptions occur.

6. Why the Setup Is Particularly Adverse for Korea

Korea can be affected through multiple channels simultaneously.

6-1. Increased Energy Import Burden

Korea has high dependence on energy imports.

Higher oil prices transmit directly into import prices and production costs, weighing on the trade balance, corporate profitability, and headline inflation.

6-2. Dual Pressure: Export Deceleration and Global Growth Weakness

If global activity slows, Korea’s export outlook deteriorates.

Key industries—semiconductors, chemicals, machinery, autos—may face weaker demand alongside higher costs.

6-3. KRW Volatility and Foreign Flow Sensitivity

Elevated geopolitical risk typically strengthens USD preference.

This can pressure the KRW and increase volatility in foreign portfolio flows.

While a weaker KRW may support some exporters, it also increases the local-currency cost of energy and raw-material imports, creating a net macro headwind.

7. What to Monitor: 7 Key Indicators

- Whether crude oil is a temporary rebound or a structural uptrend

- Risk escalation in key shipping routes (Strait of Hormuz, Red Sea)

- Re-acceleration in US CPI and market-based inflation expectations

- Changes in the Fed and major central banks’ rate-cut signaling

- Rebound in Korea’s import prices and producer prices

- Rising frequency of margin/cost pressure references in earnings

- Evidence of rotation from liquidity-driven leadership to defensive positioning

These indicators help distinguish a short-lived headline shock from an event requiring a revised economic outlook.

8. Situation Summary (News Format)

- Issue: Rising probability of a prolonged Middle East conflict

- First-order impact: Higher volatility in oil and energy prices

- Second-order impact: Rebound in global inflation expectations

- Third-order impact: Slower or delayed rate cuts by major central banks

- Fourth-order impact: Increased likelihood of the end of the liquidity-driven rally

- Fifth-order impact: Lower global growth trajectory and more selective asset performance

- Korea impact: Higher import prices, weaker exports, KRW weakness, margin pressure

- End state risk: Stagflation dynamics (weaker growth with higher inflation)

9. Underappreciated but Central Point: Potential Breakdown of the Market’s Core Assumption

The key issue is not “war drives oil higher,” but the potential invalidation of the market’s core assumption.

Asset prices have been supported by the belief that “rates will ultimately decline.”

A prolonged conflict increases the probability that inflation constraints delay easing, forcing a re-evaluation of valuations built on rate-cut expectations.

Markets typically tolerate weaker growth more than a regime where growth is weak and rate cuts are constrained.

Korea is structurally more vulnerable in this setup due to export dependence, energy import exposure, and FX sensitivity.

Accordingly, this geopolitical risk should be treated as a macro variable with the potential to reshape 2025–2026 asset-allocation strategy.

10. Practical Positioning Considerations for Individual Investors

High-conviction single-path positioning increases risk.

A scenario-based framework is more appropriate.

- Base case: rate cuts proceed broadly as expected

- Revised case: conflict-driven inflation risk delays easing

- Adverse case: oil spike and growth slowdown produce stagflation-like conditions

Portfolios should reassess concentrated exposure to high-duration growth assets, excessive leverage, and positions dependent on rapid easing.

Cash-flow durability, pricing power, and resilience under uncertainty may become more valuable portfolio attributes.

11. Conclusion: The Core Risk Is Not an “Oil Shock,” but a Forced Revision of the Macro Path

The pandemic era reinforced accommodation and liquidity expansion.

The Russia–Ukraine war reinforced inflation and tightening.

If the Middle East conflict is prolonged, the next phase may involve stagflation risk and an earlier-than-expected end to the liquidity-driven rally.

The relevant question is whether the shock disrupts the four key pillars simultaneously: growth, inflation, monetary policy, and asset pricing.

Current conditions increase that probability.

The priority is not headline monitoring alone, but reassessing portfolio assumptions tied to inflation, rates, and liquidity.

< Summary >

A prolonged Middle East conflict is not only a geopolitical issue; it can alter the global macro trajectory.

The pandemic drove accommodation and a liquidity-driven rally, while the Russia–Ukraine war drove inflation and tightening.

If the current conflict persists, the probability of stagflation dynamics increases.

Rate cuts may be delayed, weakening the liquidity-driven support for asset prices.

Korea is particularly exposed via energy import costs, export sensitivity, and KRW volatility.

The key is to monitor not only oil, but the joint evolution of inflation, rates, and cross-asset market regimes.

[Related Articles…]

- Stagflation Regime: Portfolio Checks for Individual Investors

- Growing Probability of Delayed Rate Cuts: Key Variables for the 2025 Global Economy and Korean Equities

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 유동성 장세 끝내는 새 변수. 중동전쟁 장기화가 바꿀 경제 흐름 | 클로즈업 – 중동전쟁 전망 2편

● Korea Stocks Shock Rally, Reform Fueled Repricing Ahead

Will Korean Equities Continue to Rise? The Core Message Is Structural Change, Not a KOSPI Point Forecast

As volatility increases, the key variable is not near-term price action but whether Korea’s economy and capital markets materially improve their structural quality over the next five years.

This report focuses on why investors should separate short-term fear from long-term fundamentals; how corporate governance reform and commercial law revisions could influence valuation; why the US retirement system (401(k)) strengthened US equities; and why Korea’s medium-term path may resemble either a US-style growth model or a Japan-style stagnation model. The central issue is whether structural “discount” factors in Korean equities can diminish.

1. The critical lens in risk-off markets: fear moves prices, but does not necessarily impair long-term enterprise value

Key premise:

- Geopolitical shocks, global risk events, and sharp index declines can depress sentiment.

- These factors do not automatically and permanently damage long-term corporate fundamentals.

Investor implication:

- The decisive question is not whether the index is at a specific near-term level, but where corporate earnings power and national productivity stand in 5–10 years.

- Prior crises (e.g., systemic financial shocks and pandemic-driven drawdowns) ultimately hinged on recovery capacity and growth trajectory, not the initial decline magnitude.

2. How to respond to macro shocks: extend the investment horizon rather than attempt tactical reactions

Core guidance:

- Individuals cannot control wars or macro shocks; the controllable variable is time horizon.

- A 6-month horizon amplifies headline risk; a 10-year horizon can convert volatility into lower average cost via staged deployment.

Operational principles:

- Short horizons increase the probability of reactive selling.

- Longer horizons improve the ability to absorb volatility and compound.

- Leverage is a key risk because it shortens the investor’s time to endure drawdowns.

3. Criteria for selling: not return targets, but deterioration in long-term outlook

Common error:

- Selling based on arbitrary profit thresholds (e.g., +10%, +20%) resembles price betting rather than fundamental investing.

Fundamental sell discipline:

- The sell decision should mirror the buy thesis: exit when the long-term business outlook structurally worsens.

Examples of valid sell triggers:

- Structural industry disruption

- Technological change that renders the business model obsolete

- Persistent erosion of competitive advantage

- Verified personal liquidity requirements

Non-triggers:

- Short-term price declines, fear-driven selling, or temporary flow dislocations alone are insufficient.

4. Value investing in Korea: outcomes depend on informed patience, not passive endurance

Definition:

- Value investing is purchasing high-quality assets at attractive prices and holding through cycles.

Observed gap:

- Many investors claim a value approach while trading on headlines, stop levels, and short-term targets.

Long-term edge:

- Understanding compounding and maintaining a durable process (unlevered, staged buying, separation of living expenses and investment capital) increases the probability of capturing long-duration returns.

Korea-specific note:

- In a market historically associated with persistent undervaluation, credible governance reform plus improved flows can drive re-rating.

5. Why starting early matters more than security selection: compounding is time-dominant

Reality:

- Sector selection and thematic positioning matter, but time in the market typically dominates in long-term wealth formation.

Compounding logic:

- Earlier participation allows slower accumulation with less reliance on high-risk return targets.

- Later participation increases the required speed and risk to reach similar end outcomes.

Education and behavior:

- Early exposure to diversified vehicles (e.g., ETFs, high-quality equities, dividend strategies, broad-market allocations) can create durable behavioral advantages.

6. Korea’s critical five-year window: a potential fork between US-style growth and Japan-style stagnation

Structural constraints highlighted:

- Household balance sheets overly concentrated in real estate

- Low entrepreneurial activity

- Heavy private education burden and intense credential competition

- Aging demographics and low fertility

- Limited financial literacy

- Insufficient long-duration capital flowing into public markets

Market implication:

- Equity valuation is a function of both earnings growth and institutional credibility. Structural reforms can change the market’s multiple, not only earnings.

7. Why the US regained strength: the 401(k) system expanded both public markets and innovation capital

Key mechanism:

- Retirement reform created sustained, automatic inflows into capital markets.

System features:

- Payroll contributions routed into long-term investments

- Employer matching adds incremental capital

- Persistent inflows support market depth and corporate financing

- Capital formation reinforces innovation and scaling

Relevance to Korea:

- If retirement assets shift from principal-protection bias toward long-term diversified investment, market structure and valuation support can improve.

8. In the AI era, financing capacity matters as much as technology

AI competitiveness requires:

- Talent, data, power, semiconductors, and large-scale capital

US advantage:

- Concentration of global talent

- Rapid mobilization of venture and public-market financing

- Fast capitalization of viable ideas and iterative scaling via capital markets

Korea implication:

- Industrial strengths (e.g., manufacturing, semiconductors, IT infrastructure) are necessary but not sufficient; financing channels that quickly allocate capital to innovation are critical.

9. Commercial law reform and governance improvement: a practical catalyst for a Korean equity re-rating

Core thesis:

- Korea’s “discount” has been driven materially by governance and shareholder-return credibility, not only by growth limitations.

Key issues historically cited:

- Large cash balances with weak shareholder returns

- Limited commitment to share cancellation

- Low payout ratios

- Insufficient board oversight

- Decision-making concentrated around controlling shareholders

Potential valuation effect:

- Even without outsized earnings growth, improved governance can raise the valuation multiple (i.e., re-rating).

10. Why US firms prioritize dividends and buybacks/cancellation

Governance incentives:

- Strong monitoring by boards, shareholders, litigation risk, and institutional scrutiny discourages inefficient cash hoarding.

Capital allocation discipline:

- Excess cash increases agency risk and can lead to low-return projects.

- Returning capital via dividends and buybacks can improve capital efficiency and shareholder alignment.

Korea relevance:

- Policy and market pressure toward higher payouts, share cancellation, and board accountability can strengthen capital efficiency and investor confidence.

11. Activist funds: potentially a normalization mechanism rather than a negative shock

Functional role:

- When intrinsic value materially exceeds market price, activism can accelerate governance and capital allocation reforms that narrow the gap.

Potential outcomes in low-valuation markets:

- Re-rating of undervalued companies

- Stronger shareholder-return policies

- Improved board function

- Increased foreign investor participation due to higher trust

Comparative reference:

- Similar mechanisms have contributed to market revitalization in other governance-reform contexts.

12. Why Japan is a relevant comparison: a realistic precedent for re-rating via governance reform

Observation:

- Markets can re-rate materially even without exceptional macro growth when governance, capital efficiency, and shareholder returns improve and foreign confidence returns.

Implication for Korea:

- The premise that the market “cannot structurally rise” is not supported if discount drivers are reduced.

13. Structural constraints: real estate concentration, limited financial literacy, weak entrepreneurship

Three core issues:

- Excess household wealth locked in real estate rather than productive investment

- Insufficient financial education, reinforcing reliance on labor income

- Low startup formation, limiting the pipeline of new listed companies and growth sectors

Capital market linkage:

- A stronger public-market ecosystem requires both productive household allocation and a robust innovation-to-listing pipeline.

14. Why entrepreneurship is constrained: limited financial knowledge and high aversion to failure

Root causes:

- Education systems emphasize correct answers over problem discovery.

- Social and financial penalties for failure reduce risk-taking.

Requirements for improvement:

- Financial literacy

- Greater tolerance for iterative failure

- Long-duration capital supply

- Education reform aligned with creativity and problem identification

15. Private education burden and low fertility: long-term valuation and growth variables

Transmission channels:

- Education cost inflation influences household formation, consumption, entrepreneurship, and quality-of-life expectations.

- Persistent low fertility and aging reduce labor supply, shrink domestic demand, compress talent pipelines, and raise fiscal burdens.

Equity market implication:

- Long-term growth expectations and risk premia can be affected by demographic and social cost structures.

16. Conditions for sustained upside in Korean equities

16-1. Persistent long-duration inflows into public markets

- Retirement assets and tax-advantaged accounts should increasingly support long-term diversified investment, improving stability and financing depth.

16-2. Governance and shareholder-return reforms must translate into measurable actions

- Higher payouts, share cancellation, non-core asset disposals, and stronger board accountability should be observable in reported outcomes.

16-3. A steady pipeline of innovative listed companies

- New entrants across AI, robotics, biotech, advanced semiconductor supply chains, energy, defense, platforms, and deep tech should expand market breadth.

16-4. Financial education as a mainstream life skill

- Broader understanding of capital formation and long-term investing supports healthier participation and reduces reactive behavior.

16-5. Education and entrepreneurship culture reform

- A shift from credential maximization toward problem-solving enterprise formation can support higher trend growth and a stronger equity risk premium.

17. Key takeaways (report-style)

- Market assessment: Current declines are largely sentiment-driven and geopolitical in nature; distinguish these from structural impairment of fundamentals.

- Investment discipline: The primary response is horizon extension and staged allocation, not short-term timing.

- Sell discipline: Sell based on structural deterioration in business outlook, not on short-term returns.

- Korea outlook: The next five years may determine whether Korea moves toward a growth-oriented capital-market model or a prolonged stagnation path.

- Re-rating drivers: Commercial law reform, governance improvement, stronger shareholder returns, rising activism, and foreign confidence can reduce the structural discount.

- Structural reform agenda: Reducing real-estate concentration, expanding financial education, strengthening entrepreneurship, and easing private education burdens are long-term support factors.

- AI-era implication: Competitiveness depends on both technology and the ability to mobilize capital efficiently.

18. Underemphasized but material points

- Equity upside is more dependent on system-level reform than on single-name selection.

- US market strength is supported by automatic long-duration capital inflows, not only by technology leadership.

- AI leadership is closely linked to financial system capacity.

- Education cost structures and fertility trends affect long-term valuation through growth expectations and risk premia.

- A partial shift from real estate-heavy household allocation toward financial assets and innovation capital can improve market depth and valuation credibility.

19. Consolidated conclusion: focus on structural re-rating rather than short-term optimism

Key framing:

- Earnings cycles are transient; governance and market-structure reforms can change valuation multiples.

Re-rating prerequisites:

- Durable shareholder-friendly policies

- Meaningful participation of retirement assets in diversified long-term investment

- Education and entrepreneurship reforms that expand the innovation pipeline

- Better capital allocation to AI and advanced industries

- Improved foreign investor trust through credible governance progress

Risk to the thesis:

- If real estate concentration, education cost inflation, demographic decline, and weak entrepreneurship persist without reform traction, long-term multiple expansion may remain constrained even if cyclical rebounds occur.

20. Practical investor checklist

- Prioritize the continuity and enforceability of policy and governance reform over short-term index levels.

- Track realized changes in payouts, share cancellation, and governance metrics after legal and policy initiatives.

- Reassess retirement accounts and long-term allocations for diversification and horizon alignment.

- Evaluate Korea through both industrial competitiveness (e.g., semiconductors, manufacturing-linked sectors, AI-related supply chains) and capital-market structure improvements.

- Maintain liquidity planning and avoid forced selling by preserving time horizon.

- Interpret macro outlook beyond GDP to include education burden, demographics, entrepreneurship, financial literacy, and market-structure reform.

Related Links

- KOSPI rebound signals and foreign flow dynamics: https://NextGenInsight.net?s=KOSPI

- AI investment strategy and Korea market beneficiaries: https://NextGenInsight.net?s=AI

*Source: [ Jun’s economy lab ]

– 앞으로 한국주식 계속오릅니다. 흔들리지 마세요(ft.존리 대표1부)

● UAE Fuels KF-21 Export Surge, West Sea Showdown, Iran Strike Shock, Chunmoo Europe Breakout

UAE-Led KF-21 Export Upside, U.S.–China Standoff in the Yellow Sea, Iran Strike Scenarios, and Chunmoo’s European Hub Strategy — Consolidated Investor Brief

This is not a stand-alone defense headline. It links global supply chains, geopolitical risk, defense-industry investment, energy pricing, and Korea’s prospective growth engines.

This report covers five core points:1) Why U.S. Forces Korea (USFK) F-16 training in the Yellow Sea can be read as strategic signaling in U.S.–China competition.

2) Why Chunmoo and KF-21 are not merely weapons exports, but indicators of Korea’s export strategy and industrial policy.

3) Potential shocks to crude oil, inflation, and financial markets if an Iran strike scenario materializes.

4) How China’s nuclear-submarine developments and the Taiwan variable could reshape East Asian security architecture.

5) The under-discussed point: Korea’s defense sector is evolving from exporting contracts to exporting operational “order” (delivery reliability, sustainment, and partnership frameworks).

From a macro perspective, these dynamics connect to Korea’s exports, manufacturing, advanced technology, AI-enabled defense transformation, and global capital flows—relevant for equities, FX, commodities, and industrial policy.

1. Yellow Sea F-16 Training: Why Markets and Diplomacy React Now

Potential signal of a changing USFK role

The key issue is that USFK may increasingly operate not only for peninsula defense but also as a forward-positioned asset in broader U.S.–China strategic competition.

A plausible interpretation is that the activity tested China’s response—reaction time, surveillance coverage, and air-defense/air-policing patterns.

The Yellow Sea is a high-sensitivity theater:

- For China: proximity to coastal defenses and political centers.

- For Korea: overlap of air-defense identification and operational burden.

- For the United States: a high-resolution environment to observe Chinese responses.

Why the Korean government would be sensitive

Korea’s security alliance with the United States coexists with deep economic linkage to China. Trade exposure, semiconductor supply chains, manufacturing value chains, and raw-material sourcing keep China-related risk material.

Military signaling can transmit directly to economic channels. If China interprets actions as coercive, responses may emerge via trade friction, non-tariff barriers, supply-chain pressure, or targeted sector constraints.

News-style summary

- USFK F-16 training in the Yellow Sea can function as strategic signaling, not routine training.

- It may have included intent to map Chinese response patterns.

- Korea’s sensitivity likely reflects potential diplomatic and trade spillovers.

- Peninsula security developments increasingly transmit into supply-chain and financial-market variables.

2. The U.S.–China Yellow Sea Standoff: Implications for Korea’s Economy

Security headline, investment transmission

As U.S.–China tensions intensify, Korea faces stronger “choice pressure.” Global markets are increasingly pricing a geopolitical premium: resilience and reliable supply often outrank pure cost efficiency.

Yellow Sea tensions can affect semiconductors, batteries, shipbuilding, defense, logistics, energy, and shipping costs—especially amid ongoing supply-chain reconfiguration.

Three economic points

1) Higher geopolitical risk can increase KRW volatility; foreign flows are sensitive to uncertainty.

2) Defense, shipbuilding, and aerospace may receive valuation support as demand for deployable capability rises.

3) China-exposed export sectors may face structural pressure due to Korea’s continuing linkage to China’s cycle.

3. Trump–Xi–Kim Meeting Speculation: Why “Big Deal” Narratives Appear

USFK as a potential negotiating asset

USFK can become a strategic bargaining instrument. In a new negotiation cycle involving China and North Korea, force posture, mission scope, and basing could re-enter discussions.

For Korea, this matters because security uncertainty can influence sovereign risk perception, investment sentiment, and market discount rates.

Core point

The main issue is not the meeting rumor itself, but the possibility that the United States may treat the peninsula as part of a broader U.S.–China package, increasing complexity for Korea’s diplomacy and industrial strategy.

4. Iran Strike Risk: Direct Transmission to Oil and Inflation

Why large-scale air posture signals matter

An Iran strike scenario is a high-impact macro risk: crude spikes and maritime logistics disruption are primary channels.

A widening conflict can move Brent crude, LNG freight, insurance premia, and shipping rates, complicating inflation and rate-cut expectations.

Economic transmission channels

- Hormuz Strait tensions -> crude transport risk

- Oil price increase -> manufacturing input-cost pressure

- Inflation re-acceleration risk -> weaker expectations for policy easing

- Safe-haven demand -> USD strength, EM FX pressure

- For energy importers such as Korea -> worsened trade balance risk

Domestic instability and regime-change scenarios

Beyond limited strikes, extended uncertainty (no-fly zones, regime-change pathways) is typically more disruptive than short conflicts.

For Korea, priority indicators are oil, logistics costs, and FX. Higher import prices can pressure CPI and corporate margins simultaneously.

5. Chunmoo Norway Deal: Why “No Advance Payment” Can Be Structural

Not only a sale, but an exported trust framework

A contract without advance payment signals elevated confidence in Korea’s delivery execution and reliability relative to typical defense procurement risk controls (advance payments, guarantees, milestone-based disbursements).

Why it matters economically

Defense exports are high value-added and create long-duration revenue streams: sustainment, munitions, software upgrades, parts replacement, training, and local production.

This supports export upgrading and manufacturing competitiveness through multi-year cash-flow characteristics.

News-style summary

- Norway’s Chunmoo deal is a signal of changing contract terms driven by trust in execution.

- “No advance payment” implies improved credibility and delivery confidence.

- Defense exports embed sustainment and upgrade annuities.

- This supports Korea’s long-term growth narrative and export diversification.

6. Poland–Norway Hub Formation: Korea’s Entry into Europe’s Security Supply Chain

From exports to network position

Korea’s edge is not only price. Buyers assess delivery speed, localization flexibility, technology-transfer options, political reliability, and operational suitability.

Poland and Norway can function as hubs within Europe’s defense supply chain. Once a hub is established, regional diffusion can accelerate.

Europe’s rearmament, expanded defense financing mechanisms, and replenishment demand after the Ukraine war increase structural opportunity.

Industrial linkages

- Precision-guided munitions

- Rocket and missile systems

- Radar and electronic warfare

- Military vehicles and self-propelled artillery

- Aircraft engine and MRO

- AI-enabled battle management systems

7. KF-21: Why It Is a High-Temperature Export Asset Now

Deployment proximity as competitive advantage

KF-21 is approaching operational deployment while some competing platforms remain earlier in development. In fighter exports, delivery timeline and field readiness can outweigh marginal specification differences.

Buyers prioritize: delivery schedule, operational readiness, weapons integration, and sustainment maturity.

Why demand for F-35 alternatives is growing

Not all countries can or will adopt F-35 due to acquisition and operating costs, operational autonomy constraints, approval dependency, and technology controls.

A defined market exists for mid-tier high-performance fighters; KF-21 targets this segment.

Why the UAE variable matters

The UAE is a signaling customer: capability-focused, operationally demanding, and able to benchmark U.S., European, and Asian offerings. Interest from such a buyer can influence broader market perception.

This should be treated as rising export optionality rather than confirmed outcome; the key is that KF-21 has entered serious buyer consideration sets.

8. KF-21 Key Test: Operational Capability, Not “Value for Money”

Frequent misframing

Positioning KF-21 only as a cost-effective platform understates the decision drivers. Export success depends on mission reliability, survivability, and upgrade capacity.

Modern air combat requires integrated systems: sensor fusion, data links, electronic warfare, weapons integration, software roadmap, and AI-enabled tactical support.

KF-21’s export trajectory is likely to depend on post-fielding performance and credibility in operational service.

9. China’s Nuclear Submarines and Korea’s SSN Debate: The Next Phase in East Asian Security

Qualitative shift in China’s naval build-up

China is moving from quantitative expansion to qualitative capability: nuclear submarines, blue-water operations, and strategic deterrence.

This can drive changes in planning for Korea, Japan, Taiwan, and the United States, and may revive Korea’s debate on nuclear-powered submarines.

Economic and technology relevance

SSN-related debate extends beyond defense: reactor miniaturization, high-performance materials, batteries, shipbuilding, undersea sensors, AI autonomy, and data processing.

Spillovers can reach shipbuilding, nuclear engineering, materials, communications, robotics, and AI.

10. Taiwan and Critical Infrastructure Strike Scenarios: Why Tail Risk Is High

Mutually destructive dynamics are market-negative

Extreme cross-strait scenarios include attacks on critical infrastructure rather than only amphibious operations. Targets could include dams, nuclear facilities, ports, and semiconductor fabrication capacity, creating outsized economic shock.

Taiwan is central to global semiconductor supply. Conflict risk transmits into IT hardware, autos, defense, AI servers, and data centers.

Why internal Chinese economic stress matters

Domestic pressures—property-sector weakness, labor stress, and local-government fiscal issues—can increase incentives for external conflict as a cohesion mechanism. This is a risk factor rather than a deterministic path.

11. Fourth Industrial Revolution and AI Trend Lens

Defense as a primary AI application domain

Defense is increasingly software- and data-centric. Fighters, missiles, air defense, submarines, and ISR are evolving into integrated data systems.

Key capabilities: sensor fusion, autonomous target recognition, predictive maintenance, digital twins, and networked battle management.

Technology areas to monitor

- AI-enabled ISR analytics automation

- Manned–unmanned teaming

- Digital-twin maintenance optimization

- Battlefield cloud and edge computing

- Electronic-warfare response algorithms

- Integrated analysis across satellite, drone, and radar data

KF-21 and Chunmoo should be evaluated as platforms within an AI-enabled operational stack, not as standalone hardware.

12. The Under-Covered Key Point

Korea is exporting “reliable order” alongside products

Coverage often emphasizes units and contract size. The structural shift is Korea’s positioning as a partner offering fast delivery, stable sustainment, flexible negotiation, technology-transfer options, and comparatively lower political friction.

This is a transition from product export to participation in security architecture and supply-chain structure.

Why it matters beyond defense

Reputational capital from defense execution can spill into nuclear power, shipbuilding, semiconductor equipment, batteries, infrastructure, smart cities, and AI solution exports.

National execution credibility can become a cross-sector premium.

13. Investor and Industry Checklist

Near-term indicators

- Military tension levels in the Yellow Sea and Taiwan Strait

- U.S. and Israeli operational signals related to Iran

- Brent crude and USD index movement

- Expansion of KF-21 engagement countries

- Additional Chunmoo exports and European localization discussions

Medium- to long-term indicators

- Expansion of Korea’s MRO and sustainment footprint

- Exportability of AI-enabled defense systems

- Linkage between European defense financing and Korean suppliers

- Geopolitical-risk premium applied to Korea’s strategic industries

- Korea’s role in reconfigured global supply chains

14. One-line conclusion

Yellow Sea signaling, Iran strike risk, China’s nuclear submarine advances, Taiwan tail risks, and Chunmoo/KF-21 export momentum are connected components of a single macro-geopolitical cycle.

As global instability rises, Korea faces higher exposure while also gaining opportunities to scale as a strategic-industry supplier, with defense, advanced manufacturing, AI-enabled battlefield technologies, and supply-chain reconfiguration at the center.

< Summary >

- USFK training in the Yellow Sea can be interpreted as U.S.–China strategic signaling, with spillovers into Korea’s diplomacy and economy.

- Iran strike risk is a primary variable for oil, inflation, FX, and broad market volatility.

- Chunmoo and KF-21 are indicators of export upgrading and potential long-run growth drivers, not only defense sales.

- China’s nuclear submarine trajectory, Taiwan risk, and China’s economic slowdown can increase East Asian security uncertainty.

- The key structural shift is Korea’s move toward exporting trust, sustainment, and partnership frameworks, not only platforms.

[Related…]

- KF-21 export optionality and Middle East defense market restructuring points (NextGenInsight.net?s=KF-21)

- Implications of Chunmoo’s European expansion for Korea’s defense investment landscape (NextGenInsight.net?s=Chunmoo)

*Source: [ 달란트투자 ]

– UAE 드디어 일 저질렀다. KF-21 수출 잭팟 터졌다 | 김대영 군사평론가 풀버전