● Korea, Flashpoint, Samsung, Strike, Alarm

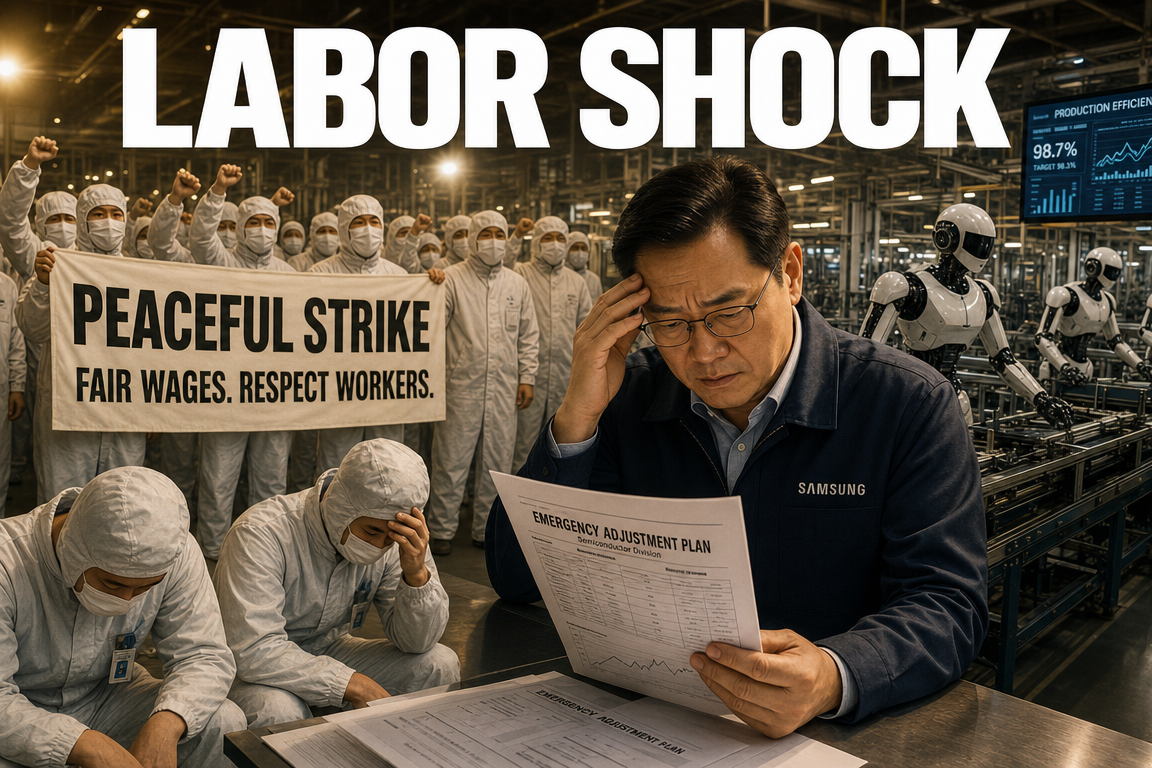

Prime Minister Kim Min-seok’s Warning on “Emergency Adjustment Authority”: Why the Samsung Electronics Union Strike Is Not a Simple Labor Dispute

This issue should not be viewed solely as a wage and incentive conflict between Samsung Electronics and its union. The key consideration is why the government raised the possibility of emergency adjustment authority, and how semiconductor production disruption could propagate through Korea’s economy, exports, financial markets, and AI competitiveness.

News coverage often focuses on “preventing a strike” or “possible emergency adjustment.” The more material angle for investors is the linkage to semiconductor supply chains, national competitiveness, capital markets, and AI infrastructure expansion.

1. Core message: the government has effectively issued a final warning

Prime Minister Kim Min-seok stated that if a strike is expected to cause significant damage to the national economy, the government may have no choice but to consider available measures, including emergency adjustment.

While framed as a general principle, the statement signals that the government views the matter as high severity. The remark that the negotiation on the 18th is “effectively the last opportunity” indicates strong pressure on both labor and management to conclude talks without delay.

This is not a simple request for restraint; it formalizes the likelihood of stronger state intervention if a strike materializes.

2. Key facts (summary)

- The Samsung Electronics union has signaled the possibility of a general strike.

- The government is treating the situation as an issue with potential economy-wide consequences, not a firm-specific dispute.

- The Prime Minister warned that semiconductor production disruption could lead to lower exports, financial-market instability, deterioration in suppliers’ operations, weaker employment, and slower domestic investment.

- If emergency adjustment authority is invoked, the union must immediately halt industrial action, and strikes are prohibited for 30 days.

- During that period, negotiations must resume; if no agreement is reached, the process may move to mediation.

- The primary inflection point is the negotiation outcome on the 18th.

3. Why the government is intervening: this is not “one company’s problem”

Although the surface issue is collective bargaining, the event exposes a structural vulnerability in Korea’s economic model. Semiconductors are a central export pillar, and Samsung Electronics sits at the center of that ecosystem. As a result, production disruption is unlikely to be contained to the company’s revenue line.

3-1. Direct export shock risk

Semiconductors are Korea’s flagship export. Beyond export share, semiconductors function as foundational inputs for multiple industries:

Smartphones, servers, consumer electronics, automotive, displays, industrial equipment, and data-center infrastructure.

Accordingly, a semiconductor supply disruption can pressure not only semiconductor exports but also downstream manufacturing and exports, with implications for the trade balance and growth.

3-2. Spillovers to suppliers and regional economies

The semiconductor sector is an interconnected network spanning materials, components, equipment, logistics, cleanroom services, maintenance, testing, and packaging.

A halt in a single process step can ripple through vendor and supplier operations. This can tighten cash flows for SMEs and mid-sized suppliers, leading to deferred capex and reduced hiring, extending the impact to regional economies and labor markets.

3-3. Sensitivity of financial markets and investor sentiment

Markets are highly sensitive to uncertainty. For a company with significant influence on the KOSPI and foreign flows, rising concerns over production disruption can affect equities, FX, and broader risk sentiment.

In Korea, the semiconductor cycle often functions as a macro leading indicator; therefore, labor disruption risk can be priced as a macro variable rather than a firm-specific event.

4. Why emergency adjustment authority matters: legal effect and market interpretation

Emergency adjustment authority is a mechanism for government intervention when a labor dispute is deemed likely to materially harm the national economy or endanger daily life.

Once invoked, industrial action must cease immediately and strikes are restricted for a defined period. Because it is rarely used, its signaling value is high. The government’s explicit reference indicates that it is treating semiconductor operational continuity as a strategic national risk.

4-1. Not only a legal issue: a policy signal

Mentioning emergency adjustment authority is not limited to pressuring labor. It communicates that semiconductors are viewed as a national strategic industry and that the government is prepared to intervene to mitigate market and supply shocks.

This signal is relevant not only to labor and management but also to investors, overseas customers, and global supply-chain partners: Korea intends to avoid prolonged semiconductor supply disruption.

5. Strategic context: semiconductors as AI-era infrastructure

Semiconductors are no longer a conventional manufacturing input; they are core infrastructure for AI, cloud, data centers, autonomous driving, defense, robotics, and smart factories.

Memory semiconductors are critical for AI servers and data-center scaling. Production stability at Samsung Electronics and peers is therefore linked not only to earnings but also to Korea’s AI competitiveness and infrastructure roadmap.

5-1. Direct linkage to data centers, compute capacity, and AI scaling

National competitiveness increasingly depends on compute capacity. As AI models scale, the importance of high-bandwidth memory, server-grade semiconductors, storage, and power efficiency increases.

If disruptions at key manufacturers persist, they can affect domestic data-center expansion and AI infrastructure investment plans, reframing the dispute as an industrial-base resilience issue.

6. The market’s primary concern: trust and supply reliability, not one-day losses

Headline estimates often emphasize daily loss figures. More material for global customers is long-term supply reliability.

Once supply uncertainty becomes credible, customers accelerate dual-sourcing and supply-chain diversification. This can translate into share loss to competitors and durable shifts in commercial relationships.

6-1. Competitive positioning versus China and Taiwan

Global semiconductor competition has intensified. China is accelerating technology self-reliance, and Taiwan maintains strong advanced manufacturing capabilities, particularly in foundry. Competitive intensity is also rising in memory.

In this environment, visible internal disruption risks can prompt customers to evaluate alternative supply options more aggressively, making the issue as much about medium-term market position as near-term financial impact.

7. Political and economic signals embedded in the statement

The Prime Minister’s remarks served as a warning to both sides:

- To labor: a general strike would impose excessive costs on the national economy.

- To management: engage more actively to reach an agreement.

The government’s priority appears to be preventing material production disruption, rather than aligning with either party.

7-1. Significance of the joint presence of industry and labor ministries

The presence of the ministers responsible for industry policy and labor policy indicates an integrated policy stance: industrial competitiveness and labor stability are being treated as a combined agenda.

The government appears to categorize the issue as a multi-dimensional risk spanning industry, employment, exports, and investment.

8. The key point often missed: concentration risk in Korea’s economic structure

The central question is not only “how costly is a strike.” The more structural issue is why Korea’s economy is so exposed to the operational stability of a small number of firms and sectors.

High dependence on semiconductors and large conglomerates increases the probability that a single labor dispute escalates into a macroeconomic risk.

8-1. Core issue: risk concentration

This is not merely a debate about whether to strike. It highlights a concentrated economic structure in which exports, growth, equity-market performance, investment, and employment are heavily tied to a narrow industrial base.

Over time, this strengthens the case for supply-chain diversification, broader industrial portfolio development, and stronger risk-management frameworks across advanced manufacturing.

9. Three scenarios to monitor

9-1. Base positive scenario: agreement on the 18th

A negotiated compromise avoids a general strike. Under this outcome, market concerns may ease quickly, reducing uncertainty for Samsung Electronics, the semiconductor sector, and supplier networks.

9-2. Intermediate scenario: prolonged dispute with stronger government intervention

Even without an immediate agreement, the government may act to limit strike escalation through formal procedures. Physical disruption risk may be reduced, but labor-management trust damage could persist, producing a mixed market response.

9-3. Adverse scenario: visible production disruption and customer attrition risk

If a general strike results in measurable production disruption, longer-term trust erosion may exceed short-term loss estimates. Potential impacts include slower exports, supplier distress, weaker investment sentiment, reduced foreign inflows, and spillovers to AI infrastructure and advanced-industry strategy.

10. Investor-oriented conclusion

The Samsung Electronics union strike risk is not a routine wage negotiation headline. It is a composite risk spanning semiconductor operational stability, export performance, financial-market confidence, and AI-era national competitiveness.

The government’s reference to emergency adjustment authority functions as a policy signal that semiconductors are being treated as a strategic national asset and that supply disruption will not be passively tolerated. While a last-minute adjustment remains plausible given policy and market constraints, the episode underscores the need for longer-term economic risk dispersion.

11. Key monitoring points for investors and general readers

- The negotiation outcome on the 18th is the primary catalyst.

- Whether emergency adjustment authority is formally invoked could materially affect market sentiment.

- Monitor not only Samsung Electronics but also SK Hynix, semiconductor materials/components/equipment names, logistics, and capital equipment.

- Potential spillovers may extend to KRW dynamics and foreign investor positioning.

- Interpret the issue in conjunction with AI infrastructure build-out, data-center expansion, and supply-chain resilience.

< Summary >

The Prime Minister’s statement frames the potential general strike as a national economic risk rather than a firm-level labor dispute. Semiconductor production disruption could transmit to exports, supplier networks, employment, financial markets, investment sentiment, and AI competitiveness. The central risk is not daily loss estimates but the integrity of global supply credibility and national competitive positioning. The negotiation outcome on the 18th is the key inflection point, and the reference to emergency adjustment authority should be read as a policy signal that semiconductors are being treated as a strategic industry. The episode also highlights Korea’s structural concentration risk in a narrow set of industries and firms.

[Related]

- Semiconductor cycle outlook and signals for Korea’s export recovery: https://NextGenInsight.net?s=Semiconductors

- Impact of expanding AI infrastructure investment on Korean equities: https://NextGenInsight.net?s=AI

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [속보] 김민석 국무총리, “파업 고집하지 말것”, “긴급조정권 발동할 수 있다” [즉시분석]

● China’s Robot Speed Shock

The Real Reason It Is Difficult to Outcompete China in Humanoid Robotics: Speed of Market Deployment Matters More Than Technology

China’s most consequential advantage in humanoid robotics is not simply technical capability. The core issue is rapid real-world deployment across retail, restaurants, logistics, lobbies, and factory test sites to accumulate operational data.

This report summarizes why China is advancing quickly in humanoids, how the US and South Korea are pursuing different strategies, and the near-term investment priorities and industrial responses South Korea should consider. Many commentaries stop at “China is cheaper” or “China has deployed more units,” but the more material point is that China treats robots less as finished products and more as field data-collection devices.

This dynamic is also linked to China’s EV supply chain, e-commerce platforms, demographic pressures, US-China strategic competition, manufacturing automation, and the diffusion of physical AI.

1. Key Takeaways (At a Glance)

- China is deploying humanoid robots into real commercial and industrial settings even before full maturity.

- The US approach is primarily productivity-driven, focused on factory automation and manufacturing efficiency.

- For South Korea, relying on Chinese imports or waiting for US prices to fall is unlikely to sustain long-term competitiveness.

- China’s advantage is systemic: supply chain depth, distribution, consumer familiarity, policy support, and data accumulation reinforce each other.

- Humanoid competition is not only a hardware race; it is increasingly tied to broader industrial restructuring and geopolitical-economic realignment.

2. Why China Is Difficult to Beat “With Robots”

China’s core strength is market penetration, not perfection

China’s humanoids still face bottlenecks in dexterous hands, thermal management, task accuracy, OS stability, and sim-to-real gaps. However, China continues deploying units into daily-life environments—department stores, corporate lobbies, restaurants integrated with payment and facial recognition systems, and factories (often for testing rather than productivity). The primary objective is data acquisition.

Long-term competitiveness is increasingly determined by how quickly systems learn from real-world edge cases.

“Deploy first” is becoming more important than “build best”

Humanoids resemble EV market dynamics: early-stage success depends more on deployment speed and market capture than on peak initial performance. China has repeatedly applied this playbook in EVs, solar, batteries, and drones—scale first, lock in supply chains, reduce costs, expand use cases, and ultimately influence standards.

For investors, deployment volumes, supply-chain localization, distribution expansion, and data accumulation rates may be more valuation-relevant than standalone technical announcements.

3. How Chinese Humanoids Enter Daily Life

Starting with retail staff, lobby reception, and basic service

In some Chinese cities, humanoids are already placed in department stores as greeters, performers, promoters, and basic guides. Performance remains below human service quality, but normalization is the key: presence becomes routine, and consumers—children and seniors included—become accustomed to AI-enabled interactions such as facial recognition and automated payments.

This should be viewed as social adoption infrastructure, not merely product rollout.

Building familiarity ahead of capability

China is using media exposure, offline events, in-store experiences, and public deployment to reduce friction in consumer acceptance. Adoption depends on perceived safety and familiarity as much as performance. China is pushing this simultaneously at national and industry levels.

4. Manufacturing: Still “Intern” Stage, Not “Full-Time Worker”

Factory deployment has not yet translated into clear productivity gains

Current factory deployments in China are often testing, demonstration, optimization, and repetitive data collection rather than sustained productivity improvement. Service environments may resemble “full-time roles,” but manufacturing remains closer to an “internship phase.”

Why China keeps deploying anyway

Manufacturing is where humanoids could ultimately deliver the highest economic value. China is linking pilots with EV manufacturers (e.g., BYD), logistics firms (e.g., JD.com), and large industrial players, even when near-term ROI is uncertain, to position for future automation standards.

5. Three Major Bottlenecks in Humanoids

1) Robot OS (the “brain”)

Humanoids require an integrated, field-ready operating stack beyond a standalone AI model: sensor ingestion, vision, localization, motion planning, and real-time response must run concurrently. This is central to physical AI.

2) The simulation-to-reality gap

Robots can perform well in simulation but degrade materially in real settings due to floor materials, lighting reflections, human motion, object displacement, unplanned collisions, and grip-force variance. Real deployment data is therefore critical, reinforcing China’s deployment-first approach.

3) Dexterous hands

Hands remain among the hardest challenges. Fixed industrial robot arms differ from mobile humanoids that must perceive unfamiliar environments, grasp varied objects, manipulate them, and modulate force precisely. Tasks such as cooking, assembly, screw driving, and fine handling remain difficult.

Additional bottlenecks: heat and weight

More sensors, actuators, and motors increase weight and thermal load. There are three broad approaches:1) ultra-low-cost, low-function hands,2) non-anthropomorphic grippers/suction designs,3) high-precision multi-finger hands converging toward human-like capability.China is moving quickly toward the third direction.

6. Why China’s Model Is More Threatening: Replicating the EV Playbook

Expanding the market with low-cost models

China is introducing small humanoids or quasi-humanoids at very low price points to seed the “home robot” concept, prioritizing market formation over top-end performance—similar to early mass-market EV adoption dynamics.

Coordinating distribution with manufacturing

Chinese e-commerce platforms can function as full-stack commercialization hubs: sales, installation, after-sales service, and consumer financing. Many countries can build robots but lack integrated go-to-market and service infrastructure. China already has this linkage, allowing manufacturing + platforms + logistics + payments + distribution to move in tandem.

This is an industrial advantage that can outweigh pure technical leadership.

7. Why China’s Humanoid Share Is High

Advantage in real deployment and model breadth

Chinese firms have high visibility in service, logistics, factory pilots, education, and events. The key metric is not “units sold” but “units deployed.” Deployment increases data; data improves control and algorithms; improved performance supports further sales and funding, creating a reinforcing cycle.

Converting EV supply chains into humanoid supply chains

Motors, batteries, sensors, control systems, and precision manufacturing capabilities from the EV ecosystem map directly into humanoids. Existing manufacturing clusters can be repurposed rapidly. More generally, industrial transitions may depend less on building new capacity from scratch and more on speed of conversion from existing bases.

8. Why China Pushes Humanoids Despite Relatively Low Labor Costs

Demographics, manufacturing hegemony, and strategic competition

While China’s labor pool is large, low fertility and rapid aging are advancing. Maintaining manufacturing capacity implies reducing labor dependence via automation. In addition, prolonged geopolitical tension increases the value of self-reliant production, assembly, and supply-chain resilience. Humanoids are treated as next-generation production infrastructure.

Strategic target: general-purpose labor that does not strike

The long-run goal is a general-purpose workforce that can operate in human-built environments: turning door knobs, using tools, handling machines, moving through warehouses, and serving customers—an expansion beyond traditional industrial robots.

9. China’s Social Message: Positioning Robots as Household Companions

Branding robots as “co-living” assistants rather than threatening machines

Through entertainment, events, and media, China is building emotional familiarity, positioning humanoids for elder care and household assistance. While the US narrative emphasizes factory productivity, China pairs industrial ambitions with consumer-life integration, accelerating acceptance and demand formation.

10. The Most Important Misconception South Korea Must Avoid

“Use Chinese products” or “wait for cheaper US products” is a strategic risk

In advanced industries, procurement-only strategies do not build competitiveness. Import reliance may be efficient in the short term but can erode industrial understanding and applied capability. South Korea historically sustained competitiveness by understanding end-to-end systems and specializing where it can win; humanoids and AI require similar capability retention. Even if not best-in-class, maintaining parallel competence is strategically important.

Government for foundations; firms and investors for applications

At the national level, priority areas include AI models, AI semiconductors, data centers, robot operating systems, and core components. For firms and investors, focus can shift toward monetizable applications: manufacturing-specific automation, vertical robots, logistics, inspection, service robots, and industrial software—areas aligned with South Korea’s strengths.

11. Where South Korea Has Opportunities

1) Industry-specific intermediate solutions over fully general-purpose humanoids

South Korea lacks China’s scale to deploy consumer humanoids broadly. It can compete in defined scenarios: manufacturing, precision assembly, quality inspection, semiconductors, batteries, automotive, and logistics automation. This favors applied physical AI and intermediate-form robots rather than “complete humanoid” competition.

2) Export opportunities into the US market

US security and data concerns constrain broad adoption of Chinese humanoids, creating openings for South Korean suppliers. Areas include US-South Korea technology collaboration in chips, sensors, factory automation platforms, and AI software integration.

3) The “brain” and application software

Humanoids will not be won on hardware alone. Differentiation depends on how well robots perceive environments, move safely, and learn tasks quickly. This links directly to AI models, vision, sensor fusion, industrial software, and digital twins—domains where collaboration between South Korean IT and manufacturing firms is feasible.

12. Investor Checklist

Prioritize industrial connectivity over “robot theme” exposure

Investing only in end-product humanoid manufacturers is insufficient. Focus areas include:

- reducers, motors, actuators, sensors

- batteries and power management

- vision systems, facial recognition, spatial perception software

- logistics automation, smart factories, industrial AI

- e-commerce platforms and distribution integration

- data centers and AI infrastructure capital expenditure

Humanoids are an ecosystem theme spanning semiconductors, batteries, cloud, industrial automation, e-commerce, and mobility. Equity performance may be driven more by rates, FX, capex cycles, policy support, supply-chain execution, and verified deployments than by isolated headlines.

13. The Most Under-Discussed Point

China’s advantage is using the entire society as a testbed

China is not treating humanoids as isolated corporate products. Cities, department stores, platforms, logistics, factories, media, policy, and consumer experience function as a unified testbed. This is ecosystem building, not product building.

The implication is that catching up is constrained less by “robot technology gaps” and more by weaker structures for coordinated deployment, distribution, data capture, and social acceptance.

14. Outlook

Near term: expansion in service robots and factory test deployments

Visibility is likely to increase first in service contexts (events, lobbies, retail, logistics, basic guidance). Factory usage is expected to remain concentrated in testing and limited repetitive tasks.

Medium term: dexterous hands and robot OS as key battlegrounds

Over the next 2–4 years, precision hand control, thermal reduction, lightweighting, multimodal perception, and field-ready robot OS capabilities are likely to be decisive for measurable productivity gains.

Long term: structural impacts on labor and capital markets

Broad humanoid adoption could contribute to labor-market restructuring, policy debate around income support, manufacturing productivity shifts, service-sector changes, margin expansion, and portfolio allocation adjustments. This is a macro-industrial transition theme, not only a technology trend.

15. What South Korea Should Do Now

1) Track China and the US simultaneously; sustain foundational technology while scaling applications.

2) Accelerate long-term investment in data centers, AI infrastructure, robot components, and industrial software.

3) Evaluate Chinese procurement not only on price but also on domestic ecosystem sustainability and capability accumulation.

4) Prioritize manufacturing-specific automation and US-exportable solutions over generalized humanoid “complete systems.”

5) For investors, emphasize supply chains, data, platforms, contracted demand, and verified deployments over short-term thematic spikes.

< Summary >

- China’s humanoid advantage is driven more by deployment speed and data accumulation than by peak technical maturity.

- China is applying an EV-style strategy: expand the market first, then consolidate supply chains and distribution.

- Manufacturing deployments remain largely in testing phases, while service and daily-life penetration is accelerating.

- South Korea should not rely solely on Chinese imports or waiting for US price declines; it must retain foundational capability and build applied competitiveness.

- Humanoids represent a cross-sector growth axis connecting AI, manufacturing automation, supply chains, e-commerce, and labor-market transformation.

[Related Articles…]

- https://NextGenInsight.net?s=AI

- https://NextGenInsight.net?s=robots

*Source: [ Jun’s economy lab ]

– 로봇으로 중국 이기기 힘든 진짜 이유(ft.이벌찬 기자 2부)