● Market Turmoil, Rate Shock, Middle East Risk, Samsung Rally

Why the KOSPI Is Volatile: U.S. Treasury Yields at 4.5%, Middle East Risk, and Samsung Electronics Labor Dynamics

The market reflected a convergence of macro and idiosyncratic risks. Key drivers included a sharp rise in U.S. sovereign yields, renewed Middle East geopolitical concerns with inflation implications, intraday positioning in semiconductor bellwethers, and domestic flow support from retail investors. The phrase “rates are gravity” is relevant insofar as higher discount rates compress equity valuations, particularly for long-duration growth exposures.

Key Takeaways (News-Style Summary)

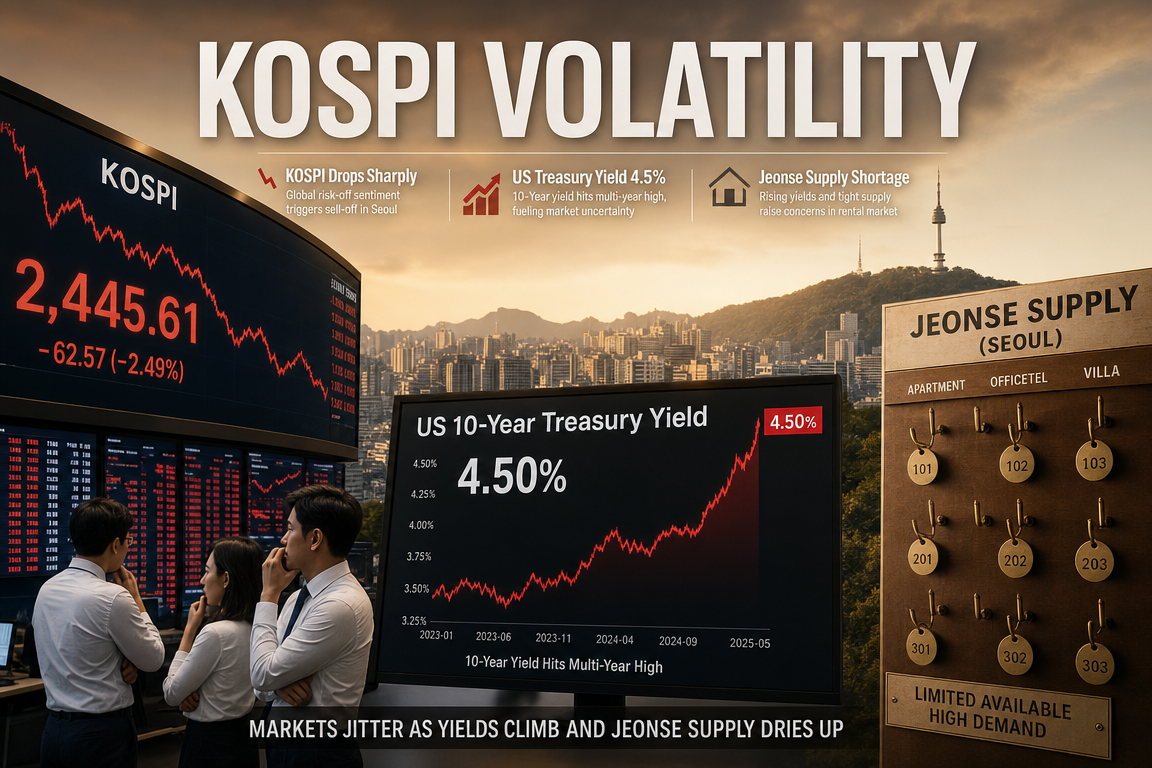

On the 18th, Korean equities faced significant downside pressure early in the session.

- The primary catalyst was higher U.S. bond yields. The U.S. 10-year Treasury yield moved above 4.5%, a widely watched psychological threshold, increasing valuation pressure across global risk assets.

- Geopolitical concerns in the Middle East added risk-off sentiment, raising the probability of higher oil prices and renewed inflation sensitivity.

- The KOSPI declined sharply intraday as risk aversion intensified.

- As declines deepened, retail investors provided notable dip-buying support.

- Buying concentrated in semiconductor large caps, including Samsung Electronics and SK Hynix, helping the index recover a meaningful portion of losses.

- Improved sentiment was also supported by market discussion of potential management-level de-escalation in Samsung Electronics’ labor negotiations, reducing perceived uncertainty.

1. Primary Driver: U.S. 10-Year Treasury Yield Above 4.5%

Why U.S. Yields Transmit Directly to Korean Equities

U.S. Treasury yields function as a global pricing anchor. As risk-free returns rise, the relative attractiveness of equities declines, and cross-border capital tends to rotate away from higher-volatility markets, including emerging market equities. Korea is particularly sensitive due to its meaningful reliance on foreign flows.

A move above 4.5% is significant less for the level itself than for what it implies: markets re-pricing the probability of “higher-for-longer” U.S. policy rates.

Why “Rates Are Gravity”

Equities are valued by discounting future cash flows. Higher rates increase the discount factor and reduce the present value of future earnings. This effect is typically more pronounced for growth and technology-linked exposures, including semiconductors, where expected cash flows are weighted further into the future. As a result, higher U.S. yields pressure the KOSPI, the Nasdaq, and global technology equities through the same valuation mechanism.

2. Why Middle East Risk Re-Activated Inflation and Equity Volatility

Geopolitics as an Inflation Variable

An escalation in Middle East risk is immediately reflected in oil price expectations. Higher oil prices raise transportation, input, and production costs, increasing inflation risks. This matters particularly when markets are positioned for eventual Federal Reserve easing; sustained energy-driven inflation can delay rate-cut expectations and tighten financial conditions.

Why the Impact Can Be More Adverse for Korea

Korea’s high dependence on energy imports can amplify macro sensitivity to oil price increases through corporate margins and the trade balance. If higher oil prices coincide with a weaker KRW, foreign investor risk appetite can deteriorate further. This creates a combined headwind across equities, FX, and inflation expectations.

3. Why the Market Did Not Fully Break: Retail Dip-Buying Support

Retail Flow as a Downside Stabilizer

A critical observation was not only the decline but who absorbed supply. Retail investors stepped in during the drawdown, contributing to intraday stabilization. This can be interpreted as continued medium-term conviction in large-cap semiconductors rather than purely technical buying.

Samsung Electronics and SK Hynix have outsized index influence; concentrated buying in these names can materially reinforce KOSPI downside support.

Why Flows Concentrated in Semiconductors

Markets are balancing short-term macro risks (rates, geopolitics, FX) against longer-term structural drivers (AI compute buildout, HBM demand, and data center capex). Consequently, sharp drawdowns have tended to attract incremental demand first in semiconductor bellwethers, reinforcing AI and semiconductors as the dominant thematic axis in Korean equities.

4. Additional Variable for Samsung Electronics: Labor Negotiations and De-Escalation Expectations

Why Labor Issues Affect Equity Pricing

Samsung Electronics’ index weight and institutional ownership profile make it highly sensitive to uncertainty shocks. Labor-related headlines weighed on sentiment, but expectations of management-led de-escalation supported a partial re-rating by reducing uncertainty.

Focus on Production Disruption Risk

If labor tensions persist, markets typically re-price the risk of production disruptions. In semiconductors, delivery schedules and customer trust are critical; thus, any reduction in disruption probability can improve sentiment beyond the single stock and toward perceived sector stability.

5. How to Frame Samsung Electronics and SK Hynix in the Current Tape

Samsung Electronics: Core Stability and Recovery Optionality

Samsung Electronics serves two functions:1) a defensive index stabilizer as a mega-cap benchmark holding, and

2) a cyclical recovery and AI-infrastructure beneficiary through semiconductor normalization.

Strength in Samsung Electronics can be interpreted as improved market breadth and resilience in Korea.

SK Hynix: High Beta to AI Memory Expectations

SK Hynix is widely treated as a primary AI-memory proxy due to HBM demand expectations. While long-term investors focus on competitiveness and cycle dynamics, near-term volatility remains high and is closely linked to U.S. rates, Nasdaq direction, and AI-related sentiment (including Nvidia-driven risk appetite).

6. Key Monitoring Points for the KOSPI Outlook

1) Whether U.S. Yields Extend Higher Above 4.5%

The primary risk is not the initial break above 4.5% but continued upside follow-through. Additional yield increases can pressure valuation multiples and destabilize foreign positioning.

2) Oil Prices and the Trajectory of Middle East Risk

Sustained oil strength can re-accelerate inflation sensitivity and push out expectations for Federal Reserve easing, tightening global equity conditions. Korea is likely to remain highly responsive due to imported inflation exposure.

3) USD/KRW and Foreign Flow Direction

Foreign investor activity remains a dominant driver of KOSPI direction. FX instability can reduce inflow propensity; conversely, FX stabilization alongside renewed semiconductor-led foreign buying could support a faster recovery.

4) Real Progress in Samsung Electronics Labor Resolution

Short-term price support can be driven by expectations, but trend durability typically requires observable de-risking and reduced operational uncertainty.

5) Durability of the AI Semiconductor Cycle

Korea’s strongest structural theme remains AI and semiconductors. If hyperscaler capex, memory demand, and cycle recovery expectations remain intact, the market may show resilience despite macro shocks.

Conclusion: Prioritize Structure Over Headlines

The session reflected simultaneous pressures from rates, inflation sensitivity, geopolitics, labor uncertainty, and flow dynamics, offset by sustained AI/semiconductor positioning. Near-term volatility may persist. The central framing remains conditional: easing in yields and oil, improved FX stability, and sustained semiconductor momentum would be supportive, while further increases in yields and escalation in geopolitical risk would likely prolong risk-off conditions.

< Summary >

- The break above 4.5% in U.S. Treasury yields was the primary driver of KOSPI downside pressure.

- Middle East risk raised oil and inflation concerns, adding an incremental headwind.

- Retail dip-buying, concentrated in Samsung Electronics and SK Hynix, reduced intraday drawdowns.

- Expectations of de-escalation in Samsung Electronics labor negotiations modestly improved sentiment.

- Key variables to monitor: U.S. yields, oil prices, FX stability, foreign flows, and the AI/semiconductor cycle.

[Related Posts…]

- https://NextGenInsight.net?s=KOSPI

- https://NextGenInsight.net?s=AI

*Source: [ 내일은 투자왕 – 김단테 ]

– 코스피가 혼돈의 카오스인 이유 (5월 18일)

● Rental Crisis, Supply Collapse, Forced Monthly Rent

Jeonse Listings Have Effectively Disappeared: The Immediate Risk Is the Rental Market, Not Home Sales

This report consolidates the key drivers behind the sharp contraction in jeonse (lump-sum deposit lease) supply in core Seoul districts, why the issue extends beyond jeonse pricing to a constraint on residential mobility, and why the next two years represent a higher-risk window.

Rather than summarizing headlines, it highlights under-covered risk signals in the housing market: declining jeonse supply, accelerating shift to monthly rent, the interaction of credit tightening and delayed supply, and the longer-term case for institutional (corporate) rental housing.

The central issue is not simply higher jeonse deposits. The market is shifting toward a structure in which households cannot freely choose location and tenure type, with broader implications for economic stability and living standards.

1. Core Update: Why the Market Describes Jeonse Supply as “Drying Up”

The primary message is that the most acute stress is in the rental market (jeonse and monthly rent) rather than the transaction (sales) market.

Historically, claims of “no jeonse listings” often proved overstated once searching on the ground. The current environment differs materially: in major preferred Seoul districts and flagship apartment complexes, jeonse listings are reportedly scarce in practice.

This matters because reduced listing availability forces tenants into monthly rent or hybrid structures, regardless of preference. The market is moving from “jeonse is expensive” to “jeonse is unavailable.”

2. Why Current Rental-Market Conditions Are High Risk

2-1. Supply contraction is more consequential than price increases

Public discussion often focuses on jeonse price changes. The higher-impact variable is declining jeonse supply.

A higher deposit may be solvable for some households via financing or savings. A lack of available units cannot be solved by purchasing power alone and reduces the ability to access desired districts, unit sizes, and complexes.

In Seoul and other core areas where proximity to jobs, education, and infrastructure is critical, supply shortages can affect commuting, schooling choices, household consumption patterns, and overall quality of life.

2-2. The shift from jeonse to monthly rent is accelerating

The transition toward monthly rent is occurring faster than expected.

While interest-rate cycles normally influence preferences between deposit-based and rent-based leases, the current pattern resembles forced monthly rent conversion driven by supply scarcity rather than tenant choice.

2-3. Deposits and rents are rising simultaneously

Pressure is not limited to one variable. The market is seeing increases in jeonse deposits, monthly-rent deposits, and monthly rent levels concurrently.

This is adverse for tenants because switching tenure types does not reduce total housing cost. If housing cost inflation exceeds income growth, real discretionary spending declines, with potential spillovers to domestic consumption.

3. “Most Severe on Record”: Why That Assessment Emerged

A key observation from long-tenured market participants is that, including forward visibility, current rental conditions may be among the most severe seen.

The significance lies in the view that there is limited near-term visibility on incremental jeonse supply. If constraints persist for two years or more, the issue should be treated as structural, not cyclical.

Households insulated by existing contracts may not yet fully experience the impact; stress is likely to rise as renewals and relocations accumulate.

4. Why the Issue Receives Limited Media Emphasis

Two factors reduce headline salience:

1) The sales market appears more national in scope, whereas rental stress is highly localized and concentrated in select Seoul districts.

2) Sale prices produce simple, headline-friendly numbers, while shortages manifest as “absence of listings,” which is harder to quantify and communicate.

Despite lower visibility, the immediate impact on households can be greater because it directly restricts the ability to move.

5. The Core Risk May Be Reduced Mobility, Not Higher Prices

A central interpretation is that the more fundamental issue is not rapid price increases but a constraint on relocating to preferred districts under a jeonse structure.

Housing market frictions affect labor mobility, education decisions, and household logistics. If jeonse is unavailable near a workplace, households may accept longer commutes or higher monthly payments, increasing economic inefficiency. Over time, reduced mobility can weigh on productivity.

6. Why Hybrid Jeonse/Monthly and Monthly Rent Are Expanding

6-1. Landlord incentives increasingly favor monthly cash flow

The prevailing dynamic is not tenants choosing monthly rent, but landlords converting existing jeonse into hybrid or monthly leases.

For landlords, converting part of the deposit to monthly rent can improve predictable cash flow, particularly when taxes, financing costs, and holding costs are considered.

6-2. Faster conversion dynamics in core districts (e.g., Gangnam, Seocho)

Core districts show higher sensitivity in conversion ratios alongside rapid deposit inflation.

An example cited: in Dogok-dong, monthly rent per KRW 100 million of deposit increased from approximately KRW 450,000 (as of January) to roughly KRW 550,000 within a few months, implying a meaningful rise in recurring household fixed costs.

7. Policy-Market Mismatch: Demand Restraint Without Rapid Supply Expansion

Policy discussion highlights a timing mismatch:

- Demand restraint can take effect quickly.

- Supply expansion requires lengthy lead times (planning approvals, redevelopment processes, construction, and occupancy).

- Near-term rental inventory therefore does not increase sufficiently.

When combined with credit constraints, land transaction permitting regimes, redevelopment restrictions, and overheating-zone constraints, both new supply and the circulation of existing stock can slow.

As a result, policies aimed at stabilization may unintentionally reduce available rental inventory.

8. Priority Framework: Housing Stability Over Price Targeting

The central policy framing is that the ultimate objective should be housing stability, not housing prices per se.

Not all non-owners have the same policy profile:

- Households that may purchase with marginal improvements in conditions

- Households structurally unable to purchase and therefore dependent on rental markets

The latter group is more exposed to supply contraction and rent conversion. If price stabilization efforts coincide with shrinking jeonse availability and rising monthly burdens, policy objectives may conflict.

9. Outlook: Why the Next Two Years Matter

The next two years will clarify whether the current shortage is temporary or a structural transition.

Contract rollovers and new lease signings can amplify realized stress over time. The rental market may tighten further if the following persist:

- Insufficient move-in supply

- Delayed redevelopment schedules

- Growing landlord preference for monthly rent

- Pass-through of tax and financing burdens

- Continued concentration of demand in preferred districts

In core Seoul and high-demand metropolitan areas, monthly rent or hybrid leases may become the default more rapidly than expected.

10. Institutional Rental Housing as a Policy Option

A key structural alternative discussed is institutional (corporate) rental housing, linked to a broader shift from a sales-driven development model toward an operations-driven housing model.

Given demographic change, household structure shifts, demand for flexibility, and asset-market volatility, housing may need to be treated as a long-duration service asset, not only a “build-and-sell” product.

10-1. Housing supply cannot be solved in isolation

The discussion also points to limits of strict zoning-based single-use development. Mixed-use configurations integrating residential, commercial, work, and services can support viable long-term operation and more predictable rental supply.

10-2. Why institutional rental is viewed as pragmatic

A market dominated by individual landlord decisions can generate rapid, destabilizing conversion from jeonse to monthly rent.

Institutional operators supplying long-term rentals can improve predictability of supply and tenancy stability. In high-demand Seoul and metropolitan submarkets, blended public-private models warrant consideration.

11. Under-Discussed Points with High Relevance

11-1. The core of the jeonse squeeze is loss of choice, not price

The primary problem is reduced ability to relocate to desired areas under preferred lease structures.

11-2. Housing-vulnerable households are hit first

Households unable to purchase are directly exposed to rental-structure shifts; shrinking jeonse supply and accelerated monthly conversion raise their burden disproportionately.

11-3. Sales-market controls and rental stability are not interchangeable

Transaction-market cooling measures may be necessary, but if they constrain rental supply, they can conflict with housing-stability objectives.

11-4. Monitoring rental-structure change is more informative than predicting sale prices

For 2026 housing-market assessment, focus should extend beyond Seoul sale-price direction to indicators such as jeonse-to-monthly conversion, rental-supply structure, move-in volumes, and adoption of operations-based housing models.

12. Practical Checklist for End-Users and Non-Owners

Key items to monitor:

- Live listing counts and turnover speed for jeonse units in target districts

- Existence of contractable inventory, not only jeonse price-to-value ratios

- Terms of hybrid conversion and the increase in monthly fixed costs

- Renewal feasibility in two years

- Scheduled move-in volumes and redevelopment timelines

- How credit-regime changes transmit into tenant costs

Similar headline prices can mask materially worse contract structures; analysis should incorporate transaction terms, supply, and lease composition.

13. One-Sentence Summary

The primary housing-market risk relevant to macro conditions is not the direction of transaction prices, but whether structural tightening in rental markets increases household burdens and weakens housing stability, with potential implications for consumption, mobility, and policy credibility.

< Summary >

Jeonse listings have contracted sharply in core Seoul districts.

The core issue is not only higher deposits but reduced housing choice due to insufficient jeonse supply.

Conversion from jeonse to monthly rent and hybrid leases is accelerating, while jeonse deposits, monthly-rent deposits, and rents are rising simultaneously, increasing household cost pressure.

Demand restraint acts faster than supply expansion, deepening rental-market imbalance.

Over the long term, policy focus should prioritize housing stability, with institutional rental housing and operations-based models emerging as a key structural option.

Housing-market assessment should prioritize rental-structure shifts and supply constraints over sale-price direction.

[Related Links…]

https://NextGenInsight.net?s=jeonse

https://NextGenInsight.net?s=real-estate

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 전세 매물, 정말 씨가 말랐습니다 | 경읽남과 토론합시다 | 김효선 위원 [3편]