● Tesla Soars, Europe Sales Blast, SpaceX Merger Shock

Tesla Shares Rise on Auto Fundamentals: Interpreting the 46.5% Rebound in Europe and the SpaceX Merger Variable

This move was not a generic “Tesla is up” headline. The market reaction was driven primarily by automotive fundamentals, supported by improving European registration data, a growing European EV market, macro sensitivity (rate-cut expectations and oil), and optionality tied to AI/autonomy. A renewed SpaceX–Tesla merger narrative also resurfaced as a secondary variable.

The key point: this was a session in which the core auto business, not only AI-related narrative, contributed meaningfully to share performance.

1. One-line market summary: indices were quiet; Tesla moved independently

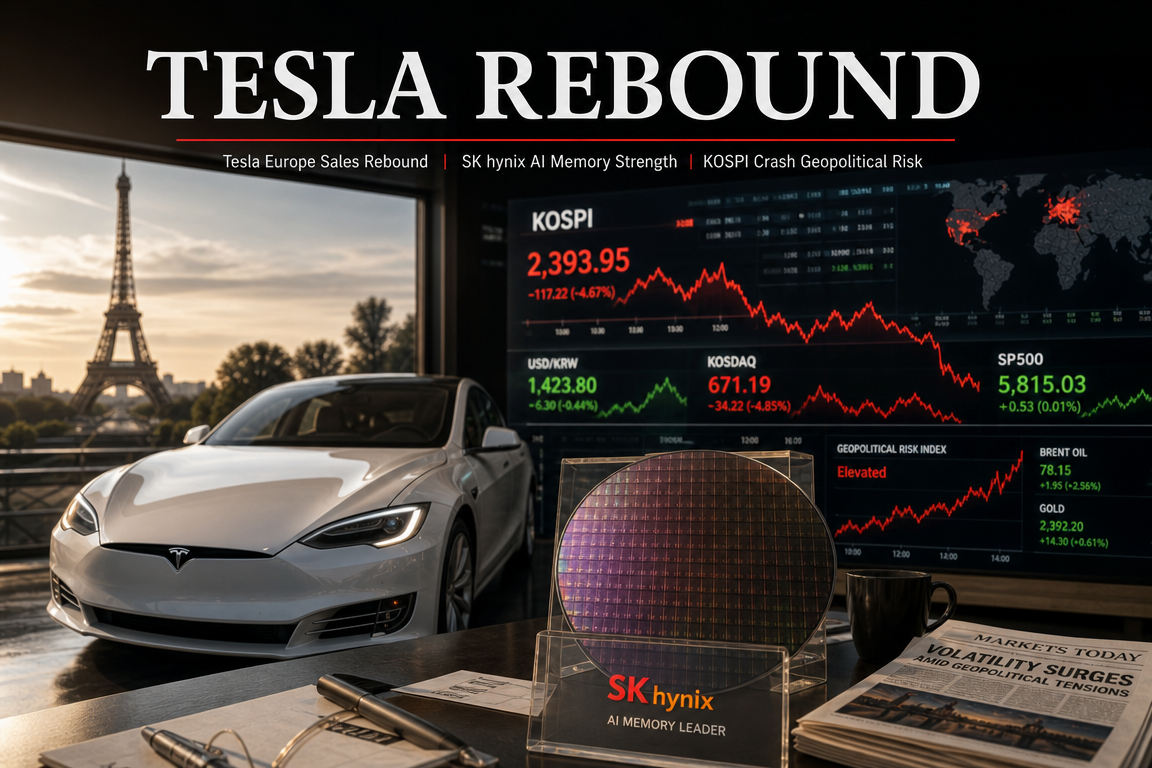

Tesla closed at $440.36, up 1.56%.

U.S. equities (S&P 500 and Nasdaq) finished near record levels, but overall index movement was broadly flat, indicating Tesla’s move was more idiosyncratic than market-driven.

Volume was below average, consistent with measured repricing rather than momentum chasing.

2. Primary catalyst: European registration data

Based on data cited from the European automobile manufacturers association, Tesla’s April registrations in Europe increased 46.5% year over year.

Importantly, the reported trend extends across three consecutive months (February–April), following a weak January, supporting the interpretation of a potential inflection rather than a single-month anomaly.

- February: year-over-year increase

- March: year-over-year sharp increase

- April: year-over-year increase of 46.5%

3. Base-effect vs. genuine recovery: the key debate

A base effect is a credible concern, given weak European performance in the prior year.

However, several elements make a “base effect only” explanation less sufficient:

- the improvement spans three consecutive months, not one

- year-to-date indicators are described as improving

- the broader European EV market is expanding

- selective signs of share stabilization or regain in certain core markets

Conclusion: the data likely reflect some base-effect contribution, but the persistence and context suggest more than statistical distortion alone.

4. The European EV market is expanding: not only a Tesla-specific dynamic

Europe’s January–April cumulative EV registrations are cited at approximately 740,000 units, up 29.1% year over year.

In April, EVs represented roughly 22% of new-vehicle registrations.

A growing market reduces the degree to which competitive gains must be purely zero-sum; multiple leading brands can expand simultaneously as penetration rises.

5. BYD sold more; why Tesla drew attention

BYD’s European growth was cited at +114.5% year over year, with reported unit volumes exceeding Tesla’s in the referenced dataset.

Headline comparisons may be misleading because BYD figures often include plug-in hybrids, while Tesla’s mix is effectively pure battery-electric. Product-mix differences matter, particularly under evolving European regulation and consumer purchasing patterns.

6. Country-level detail: where growth accelerated vs. softened

Reported Tesla strength:

- France: +100% or more

- Sweden: +100% or more

- Denmark: +100% or more

- Romania: +50% range

- Belgium: +40% range

- Netherlands: +20% range

Reported weakness:

- Portugal: decline

- Norway: sharp decline

Norway is characterized as a high-EV-penetration, mature market where percentage swings can appear amplified; stronger momentum in less-saturated markets may be a more constructive signal for incremental growth.

7. Why European EV demand may be re-accelerating: oil and consumer economics

Oil-price volatility has increased amid geopolitical risk, including Middle East tensions and shipping-route concerns.

Higher oil prices can raise the relative economic attractiveness of EVs, particularly in Europe where fuel costs and environmental policy are more directly reflected in household budgets.

8. Second engine: expectations for FSD approval in Europe

Longer-term attention is shifting to autonomy.

Management has previously indicated that European approval of FSD could support vehicle demand by strengthening the software value proposition. If approvals expand across major markets or converge at the EU level, Tesla’s competitive positioning may shift from price-only comparisons toward bundled software-driven value.

This would link near-term unit demand with a longer-duration software revenue narrative, without relying solely on speculative assumptions.

9. Technical levels and sell-side dispersion: why $420 and ~$453 matter

A resistance area near $453.5 has been highlighted by some technicians; a break above is framed by some commentators as enabling higher-end scenarios. Conversely, $420 is discussed as a key near-term support level.

Sell-side targets remain widely dispersed, reflecting uncertainty over whether Tesla should be valued primarily as an automaker or as an AI/autonomy platform:

- Bull cases: ~$450 to $600+

- Bear cases: ~$360 range

10. Larger debate: why SpaceX–Tesla merger speculation resurfaced

Merger speculation re-emerged following public commentary from an individual described as an early SpaceX investor, emphasizing “when” rather than “whether.”

The pro-merger argument centers on governance and control: SpaceX is viewed as having stronger centralized control, while Tesla is comparatively constrained. A combined structure could, in theory, simplify strategic alignment.

Key objections focus on conflicts of interest and shareholder fairness: valuation, voting/control terms, protections for Tesla shareholders, and the tangible nature of any synergies.

11. Auto recovery could reduce merger likelihood

Improving automotive fundamentals can reduce incentives to pursue a complex, controversial transaction.

If Tesla shows stabilization in deliveries and strengthening demand drivers (including autonomy-related optionality), the strategic need for a merger-driven growth narrative may diminish. Conversely, weaker auto performance and delayed AI monetization could increase the appeal of structural transactions to refresh the growth narrative.

12. Two checkpoints for holders around $440

Checkpoint 1. Does the European rebound persist through Q2?

April alone is insufficient to confirm a trend. May and June registration data—especially in France, the Netherlands, Sweden, and Denmark—should be monitored for continuity. A fade would increase the probability that the move was base-effect-driven.

Checkpoint 2. Does FSD progress translate into measurable demand?

Regulatory progress and actual order acceleration are distinct. The relevant evidence is whether autonomy capability meaningfully improves conversion and demand in Europe.

13. News-style key takeaways

- Tesla rose 1.56% in a broadly flat U.S. tape, indicating stock-specific repricing.

- The primary catalyst was a 46.5% year-over-year increase in April European registrations.

- Base effects likely contributed, but a three-month sequence reduces the likelihood of pure statistical distortion.

- Europe’s EV market is expanding (~29% YTD), allowing multiple leaders to grow.

- BYD comparisons require caution due to plug-in hybrid inclusion vs. Tesla’s BEV-only mix.

- Higher oil-price sensitivity can support EV demand in Europe.

- European FSD approval is a key variable linking vehicle sales and software monetization.

- SpaceX merger speculation resurfaced, but improving auto fundamentals could reduce strategic pressure to pursue it.

14. Under-emphasized implication: identity re-rating

The critical signal is not only higher registrations, but a potential shift in what is driving the equity story. Automotive execution is re-entering the valuation framework alongside AI/autonomy optionality, which could affect how risk is priced.

15. Integrated assessment

A balanced interpretation is:

- The 46.5% April European increase is constructive.

- It is premature to declare a confirmed multi-quarter reversal.

- Base effects likely exist, but the three-month persistence, market-wide EV growth, oil sensitivity, and autonomy expectations collectively support a more substantive interpretation than “optical improvement” alone.

Near-term focus should be on Q2 European registration continuity and whether autonomy-related milestones translate into incremental demand.

< Summary >

Tesla shares rose primarily on European sales data rather than broad market beta.

April European registrations increased 46.5% year over year; base effects are plausible, but three consecutive improving months reduce the likelihood of a one-off distortion.

A growing European EV market, oil-price sensitivity, and expectations for European FSD progress are supportive variables.

Confirmation requires monitoring May–June registrations and evidence that autonomy progress translates into orders.

Improving auto fundamentals could reduce the strategic rationale for a SpaceX merger, which remains a material governance and valuation variable.

[Related]

- Tesla equity and autonomy investment points: NextGenInsight.net?s=Tesla

- AI industry trends and global market shifts: NextGenInsight.net?s=AI

*Source: [ 오늘의 테슬라 뉴스 ]

– 오랜만에 자동차가 만든 +1.56% — 유럽 +46.5% 진짜 추세냐 베이스 효과냐, $440 주주가 검증할 두 가지 기준

● KOSPI Crash, SK Hynix Defies Shock, 3 Market Bombshells

3 Key Drivers Behind Today’s KOSPI Sell-Off, Interpreting SK hynix Relative Strength, and the Must-Watch Market Takeaways

Today’s price action reflects more than a routine pullback. The move appears to be driven by a combination of geopolitical risk, Bank of Korea rate-policy uncertainty, and overheating/valuation pressure. In parallel, understanding why SK hynix held up comparatively well is critical to interpreting current market leadership.

This is not merely an “index down” narrative. Key questions include why semiconductors and AI remain central to positioning, why SK hynix outperformed Samsung Electronics on the day, and what conditions would be required for a more durable rebound in the Korean equity market.

Overall, the decline is better characterized as a consolidation phase as the market reassesses direction, rather than a definitive end to the prevailing trend.

Why the KOSPI Declined: Three Primary Headwinds

1. Renewed U.S.–Iran tensions, increasing geopolitical risk

The first headwind was a shift in market perception toward higher military and geopolitical risk related to U.S.–Iran developments, reversing earlier expectations of de-escalation. This reduced risk appetite.

Geopolitical shocks can reprice equities quickly due to potential spillovers to oil, logistics, FX, and global capital flows.

Korean equities are typically sensitive to external shocks given their export exposure and reliance on foreign flows. As a result, Middle East-related risks and U.S. military developments often transmit rapidly to the KOSPI.

This move appears driven more by elevated external uncertainty than by a direct deterioration in corporate fundamentals.

2. Bank of Korea signaling: perceived higher probability of additional tightening

The second headwind was the market’s interpretation of a more hawkish policy bias from the Bank of Korea, including the possibility of rate increases depending on conditions. This raised discount-rate concerns and weighed on sentiment.

Higher rates increase corporate funding costs, raise discount rates for growth equities, and improve the relative attractiveness of cash and bonds versus risk assets.

After a strong run-up, even incremental policy uncertainty can have an outsized impact as investors reassess valuation and entry levels.

The key takeaway was not an imminent rate hike, but reduced confidence that liquidity expectations alone can support further multiple expansion.

3. Post-rally positioning and technical profit-taking

The third driver was technical: the index had rallied sharply, increasing the probability of profit-taking and consolidation.

Even without a major negative catalyst, short-term gains often trigger systematic de-risking and discretionary selling.

In this case, geopolitical and rate-related headlines likely catalyzed an unwind of already-elevated positioning.

Market Recap (News Style)

Domestic equities: closing highlights

The KOSPI ended lower amid heightened external uncertainty and increased sensitivity to rate-policy signaling.

Rising U.S.–Iran tensions weakened risk appetite, while a more hawkish interpretation of Bank of Korea messaging added pressure to foreign and institutional flows.

The move appeared concentrated in recently strong segments, consistent with profit-taking rather than broad-based market deterioration.

Semiconductors: differentiation within the sector

Performance diverged within semiconductors. SK hynix outperformed Samsung Electronics, reinforcing which narratives the market is currently assigning premium valuations to.

AI-linked demand expectations remain intact

AI infrastructure expansion remains a core theme. Demand expectations for high-bandwidth memory, server semiconductors, and data-center investment continue to be treated as medium- to long-term drivers despite near-term volatility.

Why SK hynix Outperformed: Key Interpretations Versus Samsung Electronics

1. Stronger positioning as a core AI-memory infrastructure exposure

SK hynix is increasingly being valued not only as a memory producer but as an AI infrastructure enabler, supported by its presence in the HBM ecosystem.

This matters because the market differentiates between cyclical recovery exposure and structurally advantaged AI supply-chain positioning, resulting in different valuation and flow dynamics.

2. Relative strength on a risk-off day signals durable demand for the exposure

Outperformance without a single dominant headline suggests positioning and flow support. When broader markets weaken, names that hold up tend to reflect higher conviction allocations.

Such stocks often decline less during drawdowns and lead early in recoveries, conditional on broader risk stabilization.

3. The key difference: clarity of narrative

Samsung Electronics remains a core benchmark holding with scale and diversification. However, near-term market preferences have tilted toward clearer, more direct AI monetization narratives.

SK hynix benefits from a more explicit “AI memory” linkage, while Samsung’s broader business mix can dilute thematic sensitivity over shorter horizons.

Is This a Risk Signal or a Healthy Consolidation?

Near-term caution, but no clear evidence of a trend break

At this stage, the move does not necessarily indicate a structural breakdown. Given the prior rally, a one-day pullback is consistent with consolidation.

However, the overlap of geopolitical and rate-policy uncertainty may extend volatility because these catalysts are not inherently transient.

The key test is whether leadership segments—particularly AI and semiconductor bellwethers—remain resilient. Thus far, leadership appears intact.

Conditions to monitor for a rebound

First, Middle East tensions must not escalate materially. Markets typically absorb geopolitical shocks faster when tail-risk probabilities decline.

Second, Bank of Korea communication should not turn incrementally more hawkish. Markets distinguish between cautionary remarks and a sustained tightening pivot.

Third, monitor whether foreign inflows re-engage large-cap semiconductors, which remain a primary driver of index direction.

The Underappreciated Point

The core issue is not the index decline, but where capital is concentrating

Many summaries stop at the three drivers of the decline. A more relevant signal is which exposures retain capital during volatility.

SK hynix resilience indicates that investors continue to treat AI semiconductors as the highest-conviction growth axis within Korean equities.

This suggests increasing selectivity: capital is less broadly allocated and more concentrated in exposures with clearer earnings linkage and structural demand drivers.

Sector selection may matter more than index direction

Market breadth appears narrower than in prior broad-based rallies. With global macro stability and the rate path still uncertain, sector and factor selection may dominate index-level positioning.

Current market leadership is centered on semiconductors, particularly AI-memory-linked names.

The key medium-term question: durability of the AI premium

SK hynix outperformance should be evaluated in the context of whether AI capex is cyclical or structural over a multi-year horizon.

Current pricing implies the market is leaning toward a more durable, multi-year demand cycle, supporting recurring bid interest in critical AI supply-chain participants.

Investor Framework

Short-term investors

Expect elevated volatility. Given that geopolitical and rate-policy risks can persist, avoid momentum chasing and prioritize pullbacks, confirmation of flows, and risk management.

Medium-term investors

Focus less on the index pullback and more on whether semiconductor and AI leaders remain technically and fundamentally supported. Consolidations that preserve leadership are often healthier.

Long-term investors

Assess which sectors can drive productivity gains and earnings growth through macro uncertainty. AI and semiconductors remain central, with Samsung Electronics and SK hynix as key Korea-linked exposures.

One-Line Interpretation

Today’s KOSPI decline reflected the combined impact of U.S.–Iran geopolitical risk, heightened rate-policy sensitivity, and post-rally profit-taking, while SK hynix resilience reinforced that AI and semiconductors remain the market’s primary leadership theme.

< Summary >

The KOSPI weakened due to overlapping geopolitical risk, perceived rate-hike risk, and technical overextension after a strong rally.

The move did not indicate a uniform breakdown; AI- and semiconductor-linked leaders remained comparatively resilient.

SK hynix benefited from stronger positioning as a flagship AI-memory exposure, supporting relative outperformance versus Samsung Electronics.

The key signal is not the index drawdown itself, but which sectors continue to command valuation and flow support.

Korean equities are increasingly characterized by selective strength centered on AI and semiconductors rather than broad-based index participation.

[Related Posts…]

- AI Semiconductor Investment Strategy and Key Beneficiaries: Trend Review

- How Rate-Hike Concerns Affect Korean Equities: Impact Analysis

*Source: [ 내일은 투자왕 – 김단테 ]

– 증시의 3가지 악재 (5월 28일)