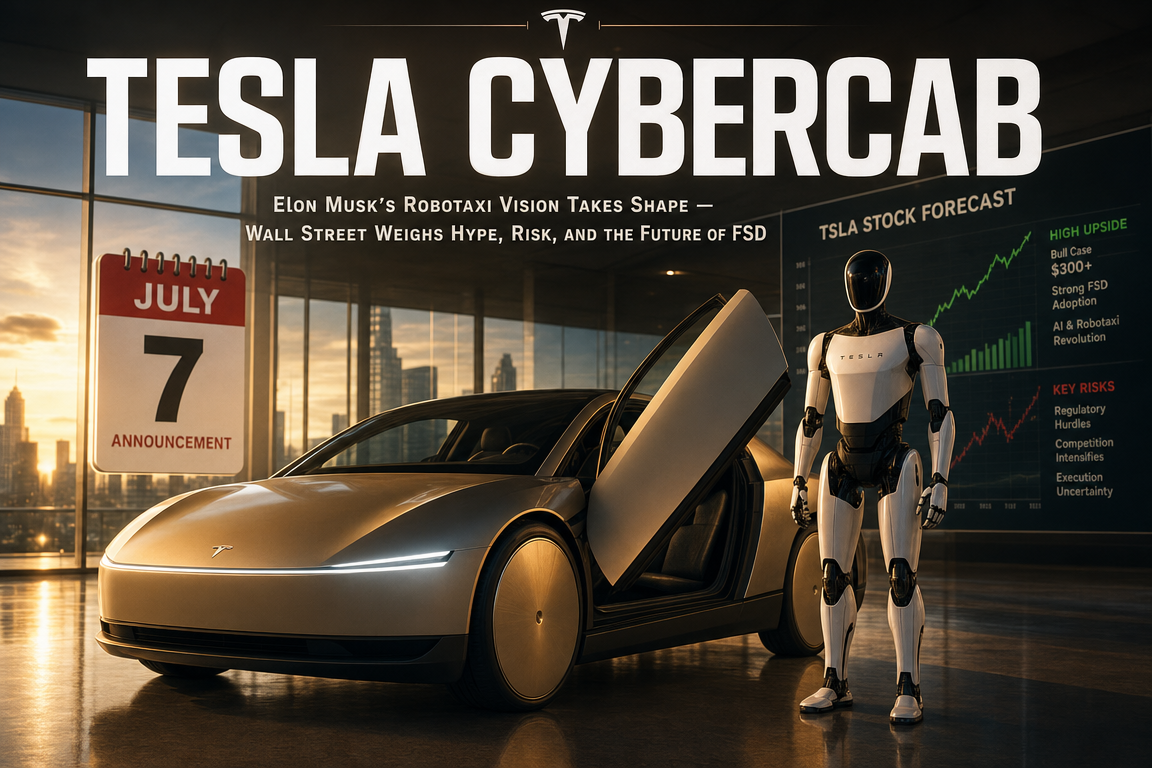

● Tesla Soars on July 7 Hype, Optimus Buzz, Cybercab Boom

Tesla Rallies 6.69%: The Primary Driver Is Not Optimus, but Anticipation Ahead of the July 7 Announcement

Tesla’s stock rose to $419.77 today, and the 6.69% gain is difficult to explain solely by rumors of Optimus mass production.

This report reviews the immediate drivers behind the move, the key variables in the July 7 Gigafactory Texas announcement, the potential expansion of Cybercab and robotaxi operations, Optimus production issues, and the main risks facing investors at the $419 level.

It also revisits a question often overlooked in other coverage: can Tesla be valued not merely as an automaker, but as an AI robotics platform company?

1. Market conditions improved broadly today

Tesla was not the only stock to rise today.

According to the source material, the S&P 500 gained 0.72%, the Nasdaq advanced 1.12%, and the Dow Jones Industrial Average rose 0.3%.

The broader U.S. market strengthened after June employment data came in weaker than expected, reviving expectations for interest-rate cuts.

Slower employment growth also raises recession concerns, but the market is currently reacting more strongly to the view that the Federal Reserve has a stronger case for easing policy.

In this environment, growth stocks, technology names, and AI-related equities tend to benefit because their valuations depend more heavily on future cash-flow expectations.

Tesla, viewed not only as an EV company but also as an AI, autonomous driving, robotics, and energy storage company, benefited from the stronger Nasdaq tone.

2. Tesla rose 6.69%, but the market’s real focus is different from the headline reason

Tesla closed at $419.77, up 6.69% from the prior session.

Some online communities attributed the move mainly to claims that Optimus mass production had been confirmed.

However, a closer reading suggests the main catalyst was not Optimus alone, but expectations for the July 7 Gigafactory Texas announcement.

In other words, today’s move appears to reflect forward-looking expectations for production expansion, robotaxi development, and Cybercab-related news rather than already confirmed results.

3. Deliveries were strong, but the stock initially declined

Tesla reported second-quarter deliveries of 481,126 units.

That represented 25% year-over-year growth and materially exceeded the market estimate of about 406,000 units.

Normally, such a result would support the share price.

Instead, the stock fell by nearly 7.5% at the time.

The reason was straightforward.

The market had already anticipated a strong delivery number, and Tesla’s valuation required a story beyond vehicle sales growth.

The reaction reflected a classic “buy the rumor, sell the news” pattern.

Today’s 6.69% gain has largely reversed that earlier decline.

The market is again evaluating Tesla less as a vehicle seller and more as an AI-driven autonomous platform.

4. Why is the July 7 announcement so important?

Ras Moravi, a senior Tesla engineering figure, said on a podcast that “interesting news” related to Gigafactory Texas scaling would be announced on July 7.

That statement materially increased market expectations.

The key issue is the venue and the theme.

Optimus is more closely associated with Fremont, while Cybercab and robotaxi operations are more closely tied to Gigafactory Texas.

For that reason, the market is focusing on the possibility that the announcement will involve Cybercab production, robotaxi network expansion, or factory automation scaling rather than a simple humanoid robot update.

5. July 7 also carries symbolic significance for Tesla

Investors are watching July 7 more closely because of its historical association with Model 3.

On July 7, 2017, Tesla produced the first Model 3 production unit at Fremont.

With that date now being referenced again nine years later, market participants are asking whether Tesla is preparing another announcement that could alter the company’s direction.

If Model 3 helped Tesla transition into a mass-market EV company, Cybercab could reposition Tesla as a robotaxi platform company.

That is why the upcoming event may matter not just as a product update, but as a potential inflection point in Tesla’s long-term valuation framework.

6. Optimus remains an important factor

At a global digital economy event in Beijing, a Tesla representative reportedly said that the Fremont plant had been converted to an Optimus production line and that mass production would begin within the year, with a long-term target of 1 million units.

The report spread through Chinese state-affiliated media and appears to have influenced gains in Chinese robotics-related stocks.

Optimus is a key part of Tesla’s long-term growth narrative.

Elon Musk has repeatedly said that Optimus could account for a significant share of Tesla’s future value.

At this stage, however, Optimus is better understood as a strategic option for future AI revaluation rather than a business that will materially contribute to near-term revenue and earnings.

It is therefore reasonable to treat Optimus as one contributor to today’s move, while recognizing that the strongest short-term catalyst is the July 7 Gigafactory Texas event.

7. Cybercab may be the main focus

Several Cybercab vehicles have reportedly been seen testing on the Gigafactory Texas test track.

The vehicles carried Cybercab markings, and the fact that multiple units were observed is significant.

This suggests movement beyond concept-stage presentation toward repeated testing and production preparation.

Reports also described Cybercab vehicles practicing passenger pickup and drop-off procedures in real-world settings.

That matters because robotaxi success depends not only on autonomous driving capability, but on service operations.

A robotaxi system requires vehicle dispatch, stop placement, passenger flow, safety response, accessibility, utilization, and remote monitoring.

8. Accessibility design in Cybercab is also relevant

The source material also said Cybercab has design features intended to support visually impaired users.

These include braille markings and sufficient space for guide dogs.

This is not a minor design detail.

For robotaxi services to function as part of broader transportation systems, they must serve elderly users, disabled users, and non-drivers.

If Tesla is integrating these requirements early in the design process, that could support regulatory approval and future urban deployment.

9. A negative view has also emerged: concerns over the Austin robotaxi fleet

Electrek published a critical report on Tesla’s Austin robotaxi service.

The main claim was that the number of unsupervised robotaxis had fallen from roughly 25 to around 14.

Tracker data reportedly showed about 17 unsupervised vehicles.

Although the service area expanded, the actual fleet size remained near 20 vehicles, limiting the visible pace of scaling.

This criticism is important for investors.

If Tesla’s valuation is being driven by AI and autonomous driving expectations, then the pace of real-world service expansion becomes a critical metric.

10. Tesla had already signaled an S-curve expansion model

In its first-quarter earnings call, Elon Musk said new products using a new supply chain tend to follow a long S-curve.

In other words, early growth is slow, but production and operating experience eventually support a faster expansion phase.

It has also been stated that Cybercab revenue could become meaningful next year rather than this year.

Accordingly, current criticism about the limited fleet size may be valid, but it does not by itself indicate that Tesla’s long-term robotaxi strategy has failed.

The key variables are future production speed, regulatory progress, and unit economics.

11. Tesla’s strategy differs from Waymo and Cruise

The source material notes that competitors such as Waymo and Cruise have had to seek exemptions from U.S. safety standards and, in such cases, face an annual cap of 2,500 vehicles.

By contrast, Tesla’s Cybercab is said to be designed to comply with existing safety standards, which would avoid that limitation.

If accurate, this would be significant.

In autonomous driving, regulatory scalability matters as much as technical performance.

Even a strong product has limited platform value if annual deployment remains capped in the low thousands.

By contrast, if Tesla can avoid regulatory bottlenecks and leverage factory-scale production, it may be able to build network scale more quickly in the robotaxi market.

12. Why did JPMorgan keep a neutral rating despite a $475 target price?

JPMorgan maintained a neutral rating on Tesla with a target price of $475.

The firm acknowledged that Model 3, Model Y, and energy storage results were better than expected.

It also cited a recovery in Europe and higher production at Gigafactory Berlin as positive factors.

However, JPMorgan said the second-quarter delivery beat alone does not justify Tesla’s current valuation.

The firm is waiting for more clarity on automotive margins, FSD progress, Cybercab production plans, and the commercialization of Optimus before the July 22 earnings release.

That assessment is broadly consistent with current market conditions.

For Tesla to be valued as an AI company, EV margins must remain stable while FSD and robotaxi initiatives begin to translate into revenue.

13. Rivian acquisition rumors are also affecting sentiment

Rivian’s CEO recently said in an interview that the company does not want to be sold, in response to rumors that Tesla might acquire Rivian.

The fact that he addressed the issue suggests that the rumor has circulated widely in the market.

Regardless of whether a transaction is realistic, the discussion reflects renewed investor attention on industry consolidation in EVs.

Given slowing EV demand, price competition, battery cost pressures, and manufacturing efficiency challenges, the gap between stronger and weaker players may widen further in the U.S. EV market.

14. Key risks for investors at the $419 level

With Tesla now trading in the $419 range, the main risk is that expectations have been priced in too quickly.

If the July 7 announcement falls short of market expectations, part of today’s 6.69% gain could be reversed.

In particular, a presentation that remains focused on broad vision without specific production volumes, timelines, regulatory milestones, or service expansion plans could trigger near-term profit taking.

By contrast, clear guidance on Cybercab production, Gigafactory Texas line conversion, robotaxi deployment, and FSD expansion could support further upside.

For investors at this level, the key issue is not tomorrow’s headline but the specificity of the announcement.

15. Key items to watch in the next announcement

-

First, determine whether the Gigafactory Texas announcement concerns Cybercab production.

-

The market reaction will differ sharply depending on whether the update is about factory efficiency or a real robotaxi mass-production roadmap.

-

Second, look for annual production targets.

-

Specific volume guidance is more important than general statements about imminent progress.

-

Third, check whether a robotaxi service expansion plan is disclosed.

-

Expansion beyond Austin, California, and Miami could materially affect Tesla’s platform valuation.

-

Fourth, watch for safety data on unsupervised FSD.

-

For Tesla to be re-rated as a robotaxi company, the market will need data on miles driven, accident rates, and intervention rates.

-

Fifth, verify whether Optimus and Cybercab are presented separately.

-

Optimus is a long-duration option, while Cybercab has a comparatively nearer-term path to revenue.

16. The central issue is often missed in other coverage

The core question is not simply what Tesla announces, but whether its valuation can shift from vehicle sales to scalable AI infrastructure.

The market already sees Tesla as expensive if it is valued only as an automaker.

But if Tesla is evaluated as an AI company with autonomous driving software, a robotaxi network, humanoid robotics, and energy storage capabilities, the valuation framework changes materially.

The central issue is scale, not demonstration.

A few Cybercabs on the road may not change investor perception significantly.

What matters is how quickly Tesla can manufacture vehicles, deploy them across cities, and generate revenue per vehicle.

If the July 7 announcement provides evidence on those points, Tesla could regain an AI-platform premium.

If it remains largely symbolic, short-term selling pressure is possible.

17. Conclusion: Tesla now trades between numbers and expectations

Today’s rally was driven by a combination of stronger second-quarter deliveries, broad strength in U.S. equities, rate-cut expectations, Optimus production rumors, and anticipation ahead of the July 7 announcement.

However, the most important variable is the expected Cybercab and robotaxi expansion news from Gigafactory Texas.

If Tesla only reiterates that it is preparing for the future, the market may be disappointed.

If it provides specific guidance on when, where, how much, and at what cost it plans to produce and operate, the investment narrative could strengthen again.

For investors near the $419 level, the main focus should be the specificity of the July 7 announcement, the margins discussed on July 22, and the actual FSD and robotaxi data that follow.

< Summary >

Tesla closed at $419.77, up 6.69%.

The move was driven not only by Optimus speculation, but also by anticipation of the July 7 Gigafactory Texas announcement.

Second-quarter deliveries exceeded expectations, but Tesla will still need tangible progress in FSD, Cybercab, robotaxi operations, and Optimus to support its current valuation.

If the next announcement includes concrete production targets, timelines, service expansion, and safety data, it could provide additional upside.

If it remains broad and vision-oriented, some of today’s gains may be given back.

[Related Articles…]

*Source: [ 오늘의 테슬라 뉴스 ]

– 내일 발표 하나에 오늘 오른 6.69% 반납될 수도 있습니다 — $419 테슬라 주주는?

● Samsung, AI, Chip, Boom, Shocks, Korea

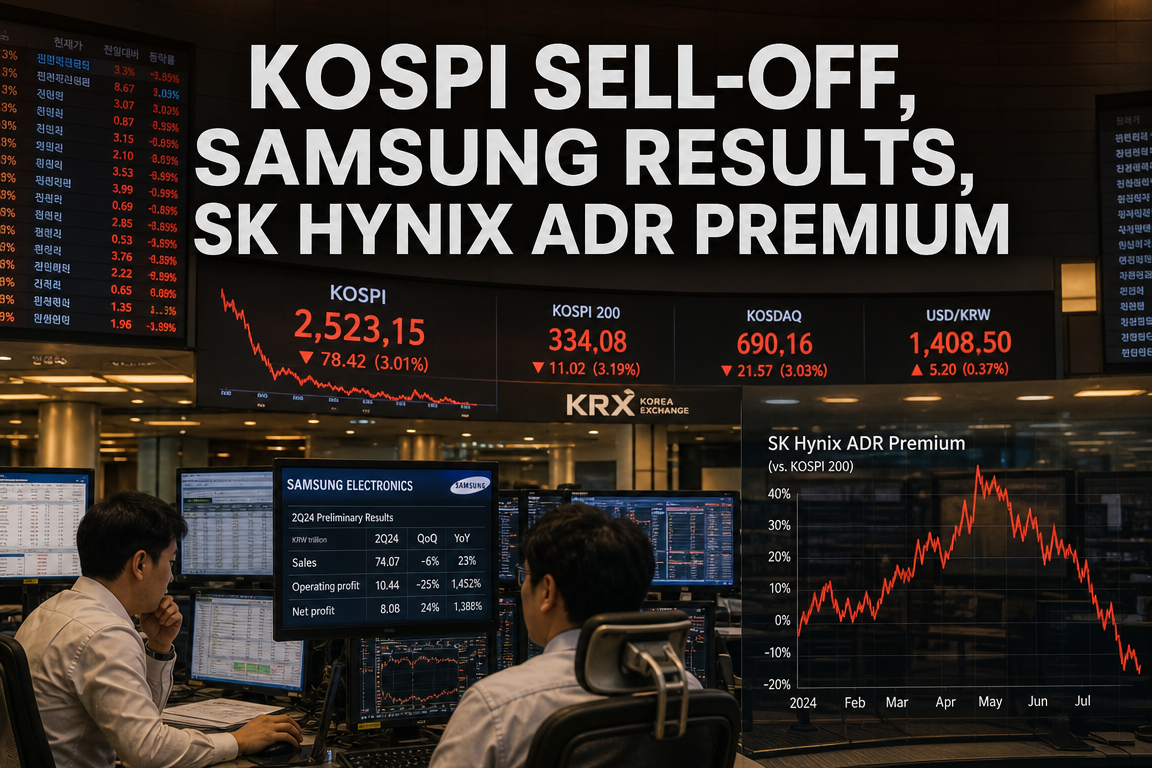

Samsung Electronics 2Q Preliminary Results Immediate Analysis: Operating Profit of KRW 89.4 Trillion, and the AI Semiconductor Supercycle Has Again Shaken the Korean Economy and Equity Market

The key point in Samsung Electronics’ latest earnings release is not simply that it posted a record result.

More important than revenue of KRW 171 trillion and operating profit of KRW 89.4 trillion is the combination of higher memory semiconductor prices driven by rising AI investment, the won-dollar exchange rate effect, the recognition of bonus-related provisions, and the extent of Korea’s dependence on semiconductors.

In particular, based on the original source, an estimated KRW 15 trillion to KRW 20 trillion in special management performance bonus reserves related to a labor agreement appears to have been reflected as a provision in second-quarter operating profit.

Excluding this provision, some estimates suggest that underlying operating profit may have exceeded KRW 100 trillion.

On the surface, this is an earnings surprise for Samsung Electronics. Beneath that, it is an event linking the semiconductor supercycle, AI data center investment, the KRW/USD exchange rate, export pricing, HBM competition, and the outlook for the Korean economy.

1. Key figures from Samsung Electronics’ 2Q preliminary results

- Revenue: KRW 171 trillion

- Operating profit: KRW 89.4 trillion

- Revenue growth vs. same period last year: 129.31%

- Operating profit growth vs. same period last year: 1,810.26%

- Revenue growth vs. prior quarter: 27.74%

- Operating profit growth vs. prior quarter: 56.21%

- Market revenue consensus: Approximately KRW 170 trillion

- Market operating profit consensus: Approximately KRW 85 trillion

According to the original source, Samsung Electronics reported second-quarter revenue of KRW 171 trillion and operating profit of KRW 89.4 trillion.

Market expectations had centered on revenue of around KRW 170 trillion and operating profit of around KRW 85 trillion, and the preliminary figures came in above those estimates.

Revenue was broadly in line with expectations or slightly above them, while operating profit clearly exceeded consensus, making this an earnings surprise.

In particular, the 1,810.26% year-on-year increase in operating profit indicates not just a recovery, but a significant shift in the company’s profitability structure.

These are preliminary figures estimated under Korean IFRS. As the final settlement has not yet been completed, business-unit details will need to be confirmed in the final release.

2. Why bonus-related provisions matter

The most notable item in second-quarter operating profit is the special management performance bonus reserve.

Based on the original source, an estimated KRW 15 trillion to KRW 20 trillion tied to a labor agreement appears to have been recognized as a provision.

In other words, this accounting expense reduced reported operating profit.

If this bonus-related provision is excluded, Samsung Electronics’ underlying second-quarter operating strength may have exceeded KRW 100 trillion.

This is a key point that can be overlooked if one looks only at headline earnings.

Reported operating profit of KRW 89.4 trillion is already exceptional, but the company’s internal earnings power may have been even stronger.

For investors, the relevant metric is not only the reported figure, but also operating profit adjusted for one-off expenses.

3. Why results improved: AI investment and memory semiconductor pricing

The main driver behind the improvement in Samsung Electronics’ results was rising AI investment.

As global large-cap technology companies increased spending on AI data centers, generative AI infrastructure, and high-performance servers, demand for memory semiconductors strengthened.

AI servers require substantially more high-performance DRAM, HBM, and NAND flash than conventional servers.

This likely lifted profitability in Samsung Electronics’ Device Solutions segment.

Although detailed segment results have not yet been disclosed, the DS division likely accounted for the majority of group earnings.

On the final earnings date, contribution by segment, including DS, mobile, display, and consumer electronics, is expected to become clearer.

4. A signal that the memory semiconductor supercycle has begun

The most important interpretation in the original source is the possibility that AI investment is pushing the industry into a memory semiconductor supercycle.

Semiconductor cycles are typically driven by pricing.

When demand rises and inventories decline, memory prices increase, and operating profit margins for companies such as Samsung Electronics and SK Hynix improve sharply.

In the second quarter, both DRAM and NAND prices are described as having risen strongly.

DDR5 spot prices are cited at around USD 35, USD 37, and USD 40 from April through June.

NAND prices are also described as rising to around USD 24, USD 26, and USD 28.82.

Higher prices improve revenue, but more importantly, operating profit tends to expand much faster than revenue.

In this case, revenue growth was 129.31%, while operating profit growth reached 1,810.26%.

This gap suggests that the improvement was driven less by volume growth and more by pricing power and margin expansion.

5. Why higher prices can drive operating profit sharply higher

Semiconductor earnings should not be assessed by revenue alone.

Revenue is price multiplied by volume.

Operating profit, however, is far more sensitive to pricing.

For example, if a product priced at 5,000 is sold in 10 units, revenue is 50,000.

If the price doubles to 10,000 and volume falls to 5 units, revenue remains 50,000.

However, transportation, storage, selling expenses, and variable production costs may decline, which can improve margins.

The same logic applies to semiconductors.

When prices rise sharply, operating profit can improve dramatically even if volumes do not expand meaningfully.

The original source also suggests that export volume may not have increased materially, or may have declined in some cases, because pricing gains were stronger than export volume growth.

In other words, this was not primarily a volume-driven earnings recovery, but a pricing-driven one.

6. The won-dollar exchange rate effect: positive for exporters, negative for domestic demand

Another important variable was the KRW/USD exchange rate.

Samsung Electronics and SK Hynix are major exporters.

When semiconductors are sold in dollars and translated into won, a weaker won generally increases revenue and profit in local currency terms.

The average exchange rate in the second quarter remained at relatively high levels, which likely supported Samsung Electronics’ earnings.

However, a weaker won is not universally beneficial.

It raises costs for companies and consumers that import raw materials, energy, food, and components.

This creates a divergence in which export-oriented large-cap companies benefit while domestic-oriented firms and households face higher pressure.

For that reason, Samsung Electronics’ results alone should not be interpreted as evidence that the broader economy has fully improved.

7. Korea’s economy has become too dependent on semiconductors

The key macroeconomic point is the share of semiconductors in Korea’s exports.

Based on the original source, semiconductors accounted for about 38.7% of exports in the first half of this year.

That compares with around 9% in 2011, the 20% range more recently, and 24.4% last year.

This means semiconductors are no longer just an industry, but a core macro variable for the Korean economy.

When assessing Korea’s outlook, semiconductors and export pricing need to be considered alongside interest rates, exchange rates, consumption, and property markets.

The original source states that semiconductor exports rose 162% year on year in the first half and led the overall export recovery.

Other major industries also showed some improvement, but semiconductors remained the primary driver of export growth.

8. Why strong semiconductor performance does not translate directly into household sentiment

This is a critical point.

Even if Samsung Electronics and SK Hynix post very strong earnings, the benefits are not felt equally across the population.

Based on the original source, total employment in Korea is around 28.5 million.

By contrast, Samsung Electronics and SK Hynix together employ fewer than 200,000 people.

As a result, only employees of the large semiconductor firms and some related suppliers directly benefit through bonuses and employment stability.

This is why one can see strong macro indicators while household sentiment remains weak.

Export performance and corporate earnings may be supported by semiconductors, while domestic demand and non-semiconductor industries follow a different trajectory.

Accordingly, policymakers and investors should distinguish between headline indicators that include semiconductors and those that exclude them.

9. The key takeaway often missed in market commentary: focus on export pricing, not only export value

Most coverage focuses on Samsung Electronics’ revenue and operating profit.

However, the more important question is why export value increased.

Export value reflects price, volume, and exchange rate effects.

In this case, the main driver of semiconductor export growth was likely higher prices and exchange-rate support rather than a sharp increase in volume.

That is very positive for margins, but it should not be interpreted as a broad-based recovery in demand.

If earnings are being driven by price rather than shipment growth, results can become more volatile when the cycle turns.

Investors should therefore track DDR5 prices, NAND prices, HBM pricing, the KRW/USD exchange rate, and inventory levels, rather than focusing only on export value.

10. Market share remains an important issue for Samsung Electronics and SK Hynix

Strong results do not eliminate competitive risk.

According to the original source, the combined memory semiconductor market share of Samsung Electronics and SK Hynix has fallen from around 80% in the past to about 67% currently.

The gap has been partly filled by competitors such as Micron, CXMT, and Nanya.

Samsung and SK Hynix still retain strong technological leadership in high-performance DRAM, HBM, and advanced memory.

However, the expansion of rivals in lower-end memory markets remains a medium-term concern.

A semiconductor supercycle benefits not only Samsung Electronics and SK Hynix, but also Micron and Chinese memory producers through the same price tailwind.

The key challenge is therefore not only to benefit from the upcycle, but also to protect market share and maintain the technology gap.

11. HBM market: the Korean duopoly is facing increased competition

HBM is the most important memory product in the AI semiconductor market.

HBM, or high-bandwidth memory, is essential for NVIDIA GPUs and AI accelerators.

At one point, Samsung Electronics and SK Hynix reportedly controlled most of the HBM market, with combined share near 98%.

More recently, Micron has entered the market more actively, with its share cited at around 21%.

Although the technology gap has not fully closed, Micron’s progress toward supply agreements with NVIDIA and mass production is an important development.

AI investment is an opportunity for Samsung Electronics and SK Hynix, but it also intensifies global competition.

Going forward, market leadership in HBM4, HBM4E, advanced packaging, and foundry cooperation will likely determine the next earnings cycle.

12. Equity market view: earnings are the core driver, while noise creates short-term volatility

Samsung Electronics’ preliminary results are likely to support the Korean equity market.

In particular, operating profit above market expectations is positive for investor sentiment toward large-cap semiconductor stocks.

Markets are always influenced by interest rates, exchange rates, geopolitical risk, conflict, U.S. elections, and liquidity conditions.

However, corporate earnings remain the primary determinant of equity value.

Share prices may fluctuate in the short term due to noise, but over time they tend to converge toward earnings and valuation fundamentals.

This release reduces uncertainty around Samsung Electronics’ earnings outlook to some extent.

That said, investors still need to assess whether the stock has already priced in expectations, whether earnings estimates may be revised further upward, and how HBM competitiveness develops.

13. Key dates and checkpoints to monitor

- Samsung Electronics final earnings release: Segment-level details need to be confirmed

- DS division operating profit: Confirm how much of group profit came from semiconductors

- HBM supply status: Track supply to NVIDIA and other major customers

- DDR5 and NAND prices: Determine whether the price uptrend continues in 3Q

- KRW/USD exchange rate: Assess whether the weaker won remains supportive

- SK Hynix earnings release: Reported as scheduled for July 29

- Micron competition: Monitor changes in HBM and DRAM market share

Even Samsung Electronics’ preliminary results alone are likely to support a positive market interpretation.

However, the final release will be more important for assessing DS division profitability, inventory valuation, bonus-related provisions, and HBM revenue mix.

SK Hynix’s results should also be reviewed to gauge the true strength of the memory semiconductor cycle.

The key question is whether this is a Samsung-specific improvement or a structurally stronger industry-wide cycle.

14. Key points investors should not miss

First, this result reflects not just one strong quarter, but a structural shift driven by AI infrastructure investment.

Second, operating profit rose much faster than revenue because memory prices and the exchange rate both supported margins.

Third, excluding the bonus-related provision, underlying operating profit may have been stronger than reported.

Fourth, it is difficult to argue that the entire Korean economy has improved when the gap between semiconductor and non-semiconductor sectors remains wide.

Fifth, maintaining technological leadership in HBM and high-performance DRAM is the most important strategic issue.

Sixth, in the equity market, earnings remain the core driver, while rates, conflict, and political issues are likely to act as short-term noise.

15. What this result means for the Korean economy

This release confirms once again that the Korean economy still moves around semiconductors.

Without semiconductors, Korea’s exports and growth would likely look much weaker.

At the same time, dependence on semiconductors has become a significant risk.

To assess Korea’s outlook properly, growth should be analyzed separately with and without semiconductors.

Even if Samsung Electronics performs well, that does not automatically improve conditions for small businesses, domestic firms, youth employment, or small manufacturers.

Accordingly, Korea needs both a semiconductor leadership strategy and a broader recovery in non-semiconductor industries.

AI semiconductors, HBM, advanced packaging, foundries, power infrastructure, and the data center ecosystem will become increasingly important as an integrated industrial strategy.

< Summary >

Samsung Electronics reported second-quarter preliminary revenue of KRW 171 trillion and operating profit of KRW 89.4 trillion.

Operating profit exceeded the market consensus of around KRW 85 trillion, making this an earnings surprise.

Excluding an estimated KRW 15 trillion to KRW 20 trillion special management performance bonus provision, underlying operating profit may have exceeded KRW 100 trillion.

The main drivers of the improvement were AI investment, higher memory semiconductor prices, and exchange-rate support.

However, it would be difficult to conclude that the broader Korean economy has improved evenly, given the gap between semiconductor and non-semiconductor sectors.

Investors should continue to monitor Samsung Electronics’ final DS results, HBM competitiveness, SK Hynix earnings, memory price trends, and the KRW/USD exchange rate.

[Related Articles…]

- Semiconductor Supercycle and the Outlook for the Korean Economy

- How AI Investment Is Reshaping the Global Memory Market

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [속보] 삼성전자, 2분기 영업이익 89.4조·매출 171조⋯ “또 역대 최대 실적” [즉시분석]