● Samsung, SK Hynix, Crash, Panic, AI, Bubble

Why the KOSPI, Samsung Electronics, and SK Hynix Sold Off Despite Record-Strong Samsung Results

Today’s key issue was not simply why Samsung Electronics fell despite strong earnings.

The real point is that a KOSPI sell-off, Samsung Electronics earnings, SK Hynix ADR developments, the memory semiconductor cycle debate, and concerns over a peak in AI infrastructure spending all hit the market on the same day.

On the surface, the move looked like profit-taking after earnings. In practice, it reflected a combination of foreign capital flows, leveraged ETF volatility, Wall Street research, and uncertainty over big tech capital expenditure.

This was not a market that fell because earnings were weak. It was a market that priced in a slowdown in the next cycle before the data fully confirmed it.

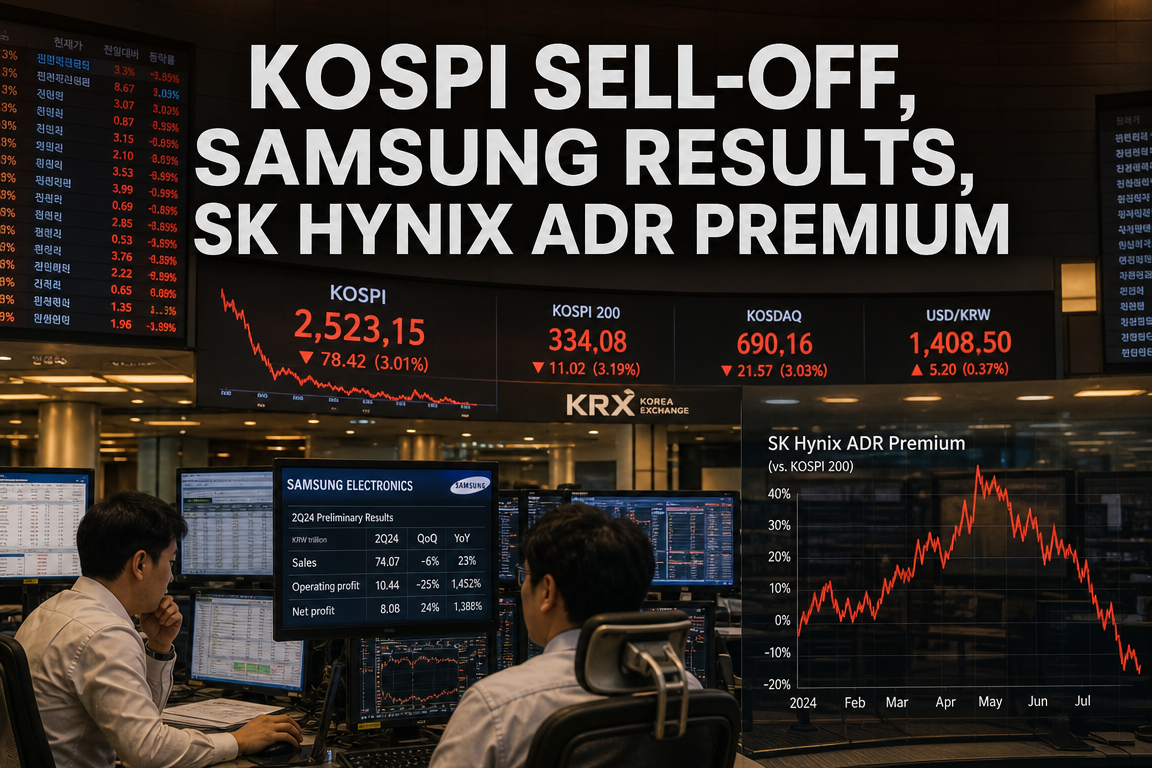

1. Market Overview: KOSPI Fell More Than 8% Intraday, Closed at -4.91%

The KOSPI briefly fell more than 8% intraday, indicating a severe panic-driven session.

It ultimately closed down 4.91%.

Selling-side sidecars and circuit breakers were triggered during the session.

The scale of the move points to a temporary liquidity vacuum rather than a normal correction.

-

KOSPI: Down more than 8% intraday, closed at -4.91%

-

Samsung Electronics: Down about 6.9%

-

SK Hynix: Down about 6%

-

Market events: Sidecars and circuit breakers triggered

The main positive was that losses narrowed after the circuit breaker event.

A move from an 8% intraday drop to a 4.91% close suggests panic selling was followed by some bargain hunting and short covering.

2. Samsung’s Results Were Strong, So Why Did the Stock Collapse?

Samsung Electronics released preliminary earnings.

The original text cited operating profit of “89 trillion won,” but in the context of Samsung’s quarterly results, 8.9 trillion won is the more reasonable interpretation.

The result exceeded consensus estimates.

However, the market had not priced in merely solid earnings. It had priced in a major upside surprise.

This created the problem.

-

Earnings were strong, but expectations were even higher.

-

A result only about 5% above consensus was not enough to satisfy investors.

-

Memory semiconductor stocks had already risen sharply over a short period.

-

The preliminary release became a catalyst for profit-taking.

This was not an earnings shock. It was a expectations shock.

The session followed a classic “buy the rumor, sell the news” pattern.

3. A Bigger Driver Than Earnings: Leveraged ETFs and Concentrated Positioning

Samsung’s share price did not collapse immediately after the preliminary release.

The market initially hesitated.

Investors were trying to determine whether the result should be treated as a bullish catalyst or a reason to reduce exposure.

Once the stock turned lower, leveraged ETFs and short-term capital accelerated the move.

Retail money has recently been heavily concentrated in KOSPI leveraged ETFs, semiconductor leveraged ETFs, and leveraged products tied to secondary batteries and AI themes.

In such a setup, volatility rises sharply once direction becomes clear.

-

The market initially debated how to interpret the earnings release.

-

Once the decline began, leveraged ETF selling increased.

-

Index weakness triggered ETF selling, and ETF selling deepened index weakness.

-

Position unwinding mattered more than earnings quality.

In this session, the key issue was not earnings but position crowding and forced deleveraging.

4. Why SK Hynix Fell More Sharply: UBS and the ADR Angle

SK Hynix was pressured not only by Samsung’s earnings but also by a separate flow-related issue.

UBS reportedly issued a note on the company’s ADR structure.

The core message was that, for U.S. investors, the ADR may be more attractive than the Korean common stock.

In practical terms, the argument implied that investors should prefer the U.S.-listed ADR over the Korean listing.

5. Why SK Hynix ADR Could Trade at a Premium to the Korean Listing

An ADR is a depositary receipt representing shares of a foreign company traded in the U.S. market.

For U.S. investors, buying an ADR is far easier than buying the Korean stock directly.

-

Trading convenience: It can be bought and sold like a U.S. stock.

-

Lower friction: Less need for currency conversion, overseas brokerage logistics, and settlement complexity.

-

Access for constrained institutions: Global funds that cannot easily buy Korean shares may still buy ADRs.

-

Broader investor access: International retail investors can access the stock more easily.

-

Supply limitation: If ADR issuance is constrained, the instrument can trade at a premium, similar to a scarce asset.

The conversion structure between the Korean listing and the U.S. ADR is also important.

Conversion from ADR to the Korean common stock may be relatively easier.

By contrast, converting Korean shares into ADRs may require regulatory approval and may be more restricted.

In that case, even if the Korean stock trades at a discount, arbitrage into the U.S. ADR market may not function smoothly.

This can create a persistent structure in which the Korean listing remains discounted while the ADR trades at a premium.

The pattern is similar to the premium often observed in TSMC ADR versus the Taiwan-listed shares.

The original text referenced an average premium of around 16% for the TSMC ADR versus the local listing.

6. Why Foreign Selling Intensified: “SK Hynix Is Good, But the Korean Listing Is Less Attractive”

The key point is that the UBS note did not imply weak fundamentals for SK Hynix.

It implied the opposite.

SK Hynix remains fundamentally strong, but for U.S. investors the ADR may be more attractive than the Korean listing.

As a result, some foreign investors may have sold the Korean shares in anticipation of shifting exposure to the ADR later.

That likely contributed to the sharp decline in SK Hynix shares today.

7. Morgan Stanley’s View: The Memory Cycle Is Changing

Another source of pressure was Morgan Stanley’s research on the memory sector.

The message was that the industry backdrop is changing.

However, the note should not be interpreted as fully bearish on Korean memory producers.

Based on the original text, the bank appears to have maintained a broadly constructive stance, including an overweight-style view.

The issue was that the tone became less positive than before.

The market reacted sensitively to that moderation in tone.

8. Morgan Stanley’s Main Message: The Rate of Improvement May Have Peaked

The key issue in the Morgan Stanley note was not that memory fundamentals are deteriorating.

The core point was that the pace of improvement may already have passed its peak.

Equities tend to react more to the rate of change than to the absolute level.

Even with strong earnings, stocks can correct if the pace of improvement slows.

-

Can DRAM prices continue rising at the same year-over-year rate?

-

Can analysts still meaningfully raise earnings estimates?

-

Can AI infrastructure demand continue expanding at the current pace?

-

Can hyperscaler capex plans remain unchanged?

The market is now looking beyond current results toward the outlook for the third quarter, fourth quarter, and 2027.

9. The AI Cycle Is Not Over, But a Mid-Cycle Correction Is Possible

Morgan Stanley does not appear to view the AI cycle as over.

Since the launch of ChatGPT, memory-related stocks have gone through multiple corrections within a broader bull cycle.

This move may be another cyclical correction within a structural uptrend.

-

Late-2024 profit-taking correction

-

2025 correction related to tariff concerns

-

Geopolitical correction tied to U.S.-Iran tensions

-

Current correction driven by crowded memory positioning

In other words, the broader AI investment cycle remains intact, but the market may pause in the near term.

10. A New Debate: Is AI Compute Excessive, or Is It Being Monetized?

One of the most important debates in the market is whether AI compute capacity is being overbuilt.

The discussion intensified after reports that Meta could use AI infrastructure to support cloud services.

The negative interpretation is straightforward.

If Meta can sell spare compute capacity, then AI infrastructure spending may be excessive.

The positive interpretation is different.

It may simply reflect a smart monetization strategy for existing infrastructure.

The latter interpretation appears more plausible.

Still, markets dislike uncertainty.

That is why capex commentary from big tech earnings later this month matters so much.

11. The Late-July Big Tech Earnings Season Is the Real Inflection Point

The real inflection point for this memory correction is not Samsung’s preliminary results but the big tech earnings season beginning in late July.

What Microsoft, Meta, Amazon, and Alphabet say about AI infrastructure spending will be critical.

-

Will they keep AI server investment at current levels?

-

Will they remain constructive on GPU, HBM, and DRAM demand?

-

Will capex growth slow?

-

How will they describe AI monetization progress?

Ultimately, the next direction for Samsung Electronics and SK Hynix depends more on U.S. big tech spending than on Korean company earnings alone.

12. From Token Maximization to Token Minimization: AI Cost Control Is Emerging

Earlier this year, many companies encouraged employees to use AI as much as possible.

This can be described as token maximization.

Tokens are the basic unit of AI usage.

In simple terms, companies were telling employees to use AI freely.

That environment is changing.

As AI usage rises, IT budgets are coming under pressure.

Companies are increasingly facing the reality that AI is useful but expensive.

That has led to a shift toward token minimization, or reducing AI usage costs.

-

Greater use of open-source AI models

-

Rising interest in Chinese LLMs

-

Growing attention to Zhipu AI’s GLM models

-

Increased use of Alibaba’s Qwen models

-

Parallel use of high-performance and low-cost models

This is not just a software cost issue.

If AI usage is optimized or reduced, the implications extend to AI infrastructure spending, cloud revenue, and memory demand.

13. Why Micron’s Earnings and LTA Have Not Yet Triggered a Full Re-Rating

Micron’s recent earnings were very strong.

The reference to long-term agreements, or LTAs, led some investors to argue that memory valuations should be re-rated.

An LTA is a long-term supply agreement.

If customers commit to long-term memory purchases, earnings visibility improves materially for suppliers.

That should, in theory, justify a higher valuation multiple.

However, the market remains skeptical.

-

Memory has historically been highly cyclical.

-

The legal enforceability of LTAs remains uncertain.

-

Customers may later face inventory burdens if demand weakens.

-

The disclosure has been centered on Micron, and it remains unclear whether it applies broadly across the industry.

That said, if AI demand remains strong, LTAs may eventually be viewed as a structural change rather than a temporary feature.

14. A Price Reset Is Not Necessarily Negative

A decline in memory stocks does not automatically mean the cycle has ended.

In some cases, a market reset is necessary before the next leg higher.

Morgan Stanley’s tone is consistent with that view.

The correction may be part of a cycle extension rather than a cycle ending.

Investor interest in memory semiconductors has become highly concentrated.

When positioning is crowded, even small negative catalysts can trigger large sell-offs.

Such corrections are painful in the short term but may make the market healthier over time.

15. Memory Price Indicators Remain Supportive

Despite the sell-off in equities, memory pricing remains firm.

The original text noted that representative DRAM and NAND prices are still at or near record levels.

Two price metrics matter most.

-

Spot price: The current market price for immediate transactions.

-

Contract price: The negotiated price under long-term supply agreements.

Spot prices reflect near-term supply-demand conditions more quickly.

Contract prices have a more direct impact on suppliers’ actual earnings.

In previous downcycles, equity prices typically fell alongside spot and contract prices.

This time, pricing indicators have not yet broken down.

That supports the view that the memory cycle has not clearly turned downward.

16. Earnings Revision Breadth: Too Strong to Ignore, But Also a Potential Constraint

Morgan Stanley also highlighted earnings revision breadth.

In simple terms, this measures how widely analysts are raising earnings forecasts.

Memory-related estimates have already been revised higher by most analysts.

That is positive.

But markets always look ahead.

If almost everyone has already upgraded estimates, the room for further upward revisions may narrow.

That creates a near-term headwind.

17. Bloomberg and Michael Burry: The Supply Glut Debate Returns

Bloomberg published a piece suggesting that Michael Burry had been right on memory chipmakers.

Burry is known for a bearish view on memory cyclicality.

The article raised concern that the sector could face oversupply in the coming years.

It specifically pointed to the possibility that supply could exceed demand by 2027 or 2028.

That type of news directly affects foreign investor sentiment.

Even if current fundamentals are still intact, it encourages investors to think about a peak scenario.

18. Bank of America’s View: Prices May Keep Rising, But the Rate of Increase Could Slow

Bank of America also appears to have raised concerns about a slowdown in memory ASP growth.

ASP stands for average selling price.

The important point is that this does not necessarily mean prices will fall immediately.

Prices may still continue rising.

However, the pace of increase may slow.

The market is highly sensitive to that change in momentum.

As a result, stocks can correct even while memory prices remain elevated.

19. A More Constructive View: KB Securities and the Cisco Comparison

Not all commentary was negative.

KB Securities suggested that the current semiconductor market may be interpreted through the Cisco case from the late 1990s.

In the second half of 1999, Cisco’s stock also paused for a time.

At that time, investors worried that telecom customers lacked the cash flow to keep buying equipment.

The concern was whether customers could continue spending on Cisco products.

Later, Cisco’s earnings improved and the stock resumed its advance.

In that case, actual results outweighed concerns about customer balance sheets.

Applied to Samsung Electronics and SK Hynix, the message is simple.

If the next quarter again shows strong earnings, the current correction may prove temporary.

Ultimately, earnings can overcome skepticism.

20. A Positive Signal for SK Hynix ADR: Cornerstone Investors

An important part of the SK Hynix ADR listing is which investors participate as anchor buyers.

The original text mentioned Baillie Gifford, Coatue Management, and Situational Awareness among the investors involved.

These investors are known for their focus on long-term growth and AI-related themes.

Their interest in the ADR matters.

While it may create near-term pressure on the Korean listing, it also signals that global AI investors continue to view HBM and memory as important assets.

21. Key Points Often Missed in Other Coverage

First, today’s decline was a positioning event, not an earnings failure.

Samsung’s earnings were not weak.

But positioning had become too one-sided, and leveraged ETFs amplified the move.

The earnings release was the trigger; concentrated positioning was the fuel.

Second, SK Hynix ADR may create a structural discount for the Korean listing.

If the ADR trades at a premium, U.S. investors may prefer it.

That could leave the Korean shares relatively undervalued.

This is a more important structural issue than short-term price action.

Third, the AI debate has shifted from demand to monetization and efficiency.

Last year and earlier this year, the focus was on how much AI would be used.

Now the market is focused on how efficiently AI can be used.

If token minimization spreads, it could affect AI infrastructure spending.

Fourth, LTAs may be the key to a valuation re-rating, but the market is not convinced yet.

If long-term supply contracts are truly binding and stabilize customer demand, memory suppliers could be valued differently than in the past.

For now, however, investors remain skeptical that this time is different.

Fifth, the late-July big tech results are the real event for Korean semiconductor stocks.

What matters most is not Samsung’s preliminary earnings but the AI capex commentary from Microsoft, Meta, Amazon, and Alphabet.

If they say AI infrastructure spending will continue, the correction may be brief.

If they signal caution, the correction may last longer.

22. What to Watch Next

-

Big tech earnings: Focus on AI infrastructure spending and capex guidance.

-

Memory contract prices: Watch whether actual contract pricing weakens.

-

HBM demand: Monitor orders from Nvidia, AMD, and cloud providers.

-

SK Hynix ADR premium: Track whether a structural price gap develops between the ADR and the Korean listing.

-

Leveraged ETF flows: Assess whether retail positioning is being unwound.

-

AI cost optimization: Monitor how open-source and lower-cost LLM adoption affects cloud demand.

23. Final Assessment: The Sell-Off Was Severe, But It Is Too Early to Call the Cycle Over

Today’s session was clearly a shock.

However, it is still difficult to conclude that the memory cycle itself has broken down.

Samsung’s earnings were solid, and memory price indicators remain firm.

SK Hynix faced near-term flow pressure from the ADR issue, but global AI investors remain engaged.

That said, the market has moved beyond the simple view that AI exposure alone justifies higher prices.

Going forward, the focus is whether AI infrastructure spending is translating into revenue and earnings, whether big tech can keep investing, and whether memory pricing momentum can continue.

In other words, the market has already moved to the next question.

“AI demand remains strong. But can it accelerate enough to support further upside in stock prices?”

The answer will likely depend on late-July big tech earnings and second-half memory pricing trends.

< Summary >

The KOSPI fell more than 8% intraday before closing down 4.91%.

Samsung Electronics and SK Hynix also declined sharply.

Samsung’s earnings were strong, but expectations had become too elevated, and profit-taking plus leveraged ETF selling intensified the move.

SK Hynix was additionally affected by ADR-related flow pressure.

Research from Morgan Stanley, Bloomberg, and Bank of America reinforced concerns about a slowdown in the rate of change for memory semiconductors.

However, memory pricing remains firm, and it is too early to conclude that the AI cycle has ended.

The key event remains late-July big tech earnings and their guidance on AI infrastructure spending.

[Related Articles…]

- Semiconductor Cycle and AI Infrastructure Investment Trends

- Big Tech Capex Outlook and AI Investment Trends

*Source: [ 내일은 투자왕 – 김단테 ]

– 역대급 실적에도 삼전닉스 폭락한 진짜 이유

● Semiconductor-ETF-Risk-AI-Boom

Semiconductor ETFs: Are They Truly Safe? Risk Signals Investors Must Not Ignore in the AI Era

The reason capital is flowing into semiconductor ETFs is clear.

AI semiconductor demand is surging, the HBM market is expanding around Nvidia, and Samsung Electronics and SK Hynix are gaining attention as global leaders in memory semiconductors.

However, the key issue is not whether the semiconductor industry is attractive, but whether expectations have become overly one-sided.

Investors in semiconductor ETFs, leveraged ETFs, and thematic ETFs should pay close attention to the following risk signals.

These include the assumption that HBM technology will remain dominant indefinitely, global supply chain restructuring, the U.S.-China semiconductor conflict, the rise of sovereign AI, and the risk of relying on AI-generated investment decisions.

1. The appeal of semiconductor ETFs is straightforward

In recent markets, semiconductor ETFs are widely viewed as one of the defining investment vehicles of the AI era.

This is because companies such as Samsung Electronics, SK Hynix, Nvidia, TSMC, and Micron sit at the center of the AI semiconductor value chain.

In particular, the spread of generative AI is driving higher data center investment and rapidly increasing demand for high-performance GPUs and HBM.

In the past, semiconductors were mainly consumed in PCs, smartphones, and servers. Today, their application range is much broader.

They are embedded in EVs, autonomous vehicles, robotics, physical AI, smart factories, cloud infrastructure, and defense AI.

It is increasingly difficult to find a major industry that does not use semiconductors.

Internal combustion vehicles contain hundreds of semiconductors, while EVs require even more.

In autonomous EVs, semiconductor content rises substantially further.

As robotics and physical AI scale up, semiconductor demand may continue to rise structurally.

For this reason, many investors view semiconductors as the essential input of future industries.

That view is not incorrect.

The risk arises when long-term industry growth is confused with short- and medium-term stock appreciation.

2. The core issue: the semiconductor industry can grow while ETFs remain risky

The point of this discussion is not that the semiconductor industry will disappear.

Semiconductor demand is likely to keep expanding.

However, investors must distinguish between two separate outcomes.

Industry growth and continued ETF gains are not the same thing.

Even if the semiconductor industry expands, the market share of specific companies can decline.

Even if demand increases, margin pressure can rise as supply competition intensifies.

If the technology paradigm changes, current market leaders can weaken abruptly.

At this point, ETF investors often assume that diversification equals safety.

In practice, however, they may be holding companies tied to the same industry, the same technology, and the same demand cycle.

What appears diversified on the surface may in fact be concentrated exposure to a single narrative.

3. The HBM boom is strong now, but assuming permanence is risky

One of the main reasons Samsung Electronics and SK Hynix are attracting attention is HBM.

HBM, or High Bandwidth Memory, is high-performance memory that supplies data quickly for AI workloads.

In simple terms, AI needs to access and process large amounts of information rapidly.

If standard memory is a small desk, HBM is a wider, multi-layered desk.

It allows critical data to be placed in immediate reach rather than retrieved from distant storage repeatedly.

This is why demand for HBM has surged alongside Nvidia GPUs.

SK Hynix has been positively re-rated for its position in the HBM market, while Samsung Electronics has seen its HBM competitiveness become a key driver of its share price.

However, there is an important risk.

HBM is a core technology in the current AI semiconductor market, but there is no guarantee that it will retain that position permanently.

Technology industries are regularly disrupted by new approaches.

If a faster, cheaper, or more efficient data-processing method emerges, expectations centered on HBM could be revised quickly.

Even the announcement of a new architecture or a method that reduces memory bottlenecks can affect related stock prices.

Markets react before new technologies are fully commercialized.

In other words, even a signal that an alternative may be viable can pressure valuations across semiconductor ETFs and related stocks.

4. The larger risk is geopolitical, not technological

Many investors analyze semiconductors primarily through technology.

In reality, the industry is now shaped by national strategy, security concerns, global supply chains, and U.S.-China competition.

The most important historical reference is Japan’s semiconductor sector.

In the 1970s and 1980s, Japan held a dominant position in the memory semiconductor market.

At its peak, Japan’s memory semiconductor share reached roughly 70% to 80%.

Then U.S. pressure began.

The United States concluded that Japanese semiconductor firms had gained excessive market dominance and responded with trade pressure and semiconductor agreements that slowed Japan’s momentum.

Korea later emerged as an alternative supply base.

Samsung Electronics and SK Hynix were able to grow not only because of technological capability, but also because of the restructuring of the global semiconductor order.

Today, however, Korea’s memory semiconductor share is also very high.

Samsung Electronics and SK Hynix together account for a significant portion of the global memory market.

The question is whether this structure can remain unchanged going forward.

As semiconductors become more critical, the United States, China, Japan, and Europe are likely to seek lower dependence on any single country.

This is the geopolitical risk semiconductor ETF investors must monitor carefully.

5. The United States and China are both building domestic semiconductor ecosystems

The United States is restructuring the semiconductor value chain around domestic capacity.

It is strengthening memory capabilities through Micron, expanding Intel’s foundry ambitions, and widening its domestic production base through the CHIPS Act and advanced packaging investments.

China is also committing massive capital to semiconductor self-sufficiency.

Chinese firms such as CXMT and YMTC have not yet matched Korean companies in leading-edge, high-value memory, but they are gaining share in lower-end and mid-range segments.

An important point is that even if performance is lower, domestic demand in China may still favor local semiconductors.

Initial quality gaps can be narrowed through continued use in the domestic market.

Over time, this process can create price competition that pressures Korean firms in global markets.

The same logic applies to the United States.

Just because the U.S. is not as strong as Korea in memory semiconductors today does not mean it will remain unable to build capacity.

The country has focused on high-value logic and AI semiconductors, but if memory becomes strategically necessary, it can deploy capital, technology, and policy support quickly.

Markets often price in such shifts early.

Even before a factory is completed or the technology gap narrows, a policy signal to reduce dependence on Korea can move semiconductor stocks sharply.

6. In the sovereign AI era, semiconductors are also likely to be reorganized around national interests

A major theme in the AI industry is sovereign AI.

Sovereign AI refers to each country’s effort to build AI infrastructure aligned with its own language, data, culture, and security requirements.

As AI becomes a core national capability, countries are becoming less willing to rely entirely on foreign cloud platforms and models.

They are increasingly seeking domestic data centers, domestic AI models, and domestic semiconductor infrastructure.

This trend has direct implications for the semiconductor market.

If sovereign AI expands, countries will seek stable access to AI semiconductors and memory semiconductors.

This may create opportunities for Korean semiconductor companies, but it may also intensify pressure for local production in other markets.

In short, the global supply chain is shifting from efficiency-first to security-first.

The market is moving away from a model in which companies simply buy from the lowest-cost, highest-performing supplier.

It is moving toward a model in which resilience and continuity matter more.

This structural change may affect the long-term return profile of semiconductor ETFs.

7. Even an 800 trillion won investment plan should not be viewed through a purely optimistic lens

Korea is pursuing large-scale investment in the semiconductor sector.

This includes semiconductor clusters, advanced fabs, back-end processing, and the expansion of the materials, parts, and equipment ecosystem.

Some plans have been described as involving several hundred trillion won.

These investments are necessary to preserve Korea’s long-term competitiveness.

But investors should ask another question.

If the United States, China, Japan, and Europe each strengthen their own supply chains, can Korea’s export demand remain at the current level?

Could large-scale capacity expansion lead to oversupply?

Could a slowdown in AI investment lead to downward revisions in high-performance memory demand?

Semiconductors are a strongly cyclical industry.

When demand is strong, investment increases. When investment rises, supply expands a few years later.

If demand does not keep pace with supply growth, prices may fall and earnings can weaken.

For that reason, semiconductor investment should not be based solely on the assumption that “AI means higher prices.”

Supply, demand, pricing, technology, and policy all need to be assessed together.

8. Thematic ETFs are not always true diversification

The basic purpose of ETFs is diversification.

They reduce the risk of a single-stock collapse by spreading exposure across multiple companies and lowering volatility.

However, thematic ETFs are different.

Semiconductor ETFs, battery ETFs, AI ETFs, and robotics ETFs may hold multiple stocks, but those holdings can still be tied to the same underlying outcome.

For example, if semiconductor conditions weaken, the decline is not limited to Samsung Electronics.

SK Hynix, equipment suppliers, materials providers, and back-end processors may weaken as well.

If Nvidia corrects, the broader AI semiconductor value chain can be affected.

In that case, even an ETF containing 30 or 50 stocks may still amount to a bet on a single industry cycle.

In other words, holdings may be diversified in number, but not necessarily in risk factor.

This is the main illusion of thematic ETFs.

Investors may believe they are diversified because they own an ETF, when in fact they may be highly exposed to one sector’s outlook.

9. In leveraged ETFs, volatility management comes before return expectations

Leveraged semiconductor ETFs can look attractive during strong rallies.

When the underlying index rises, gains can increase by 2x or more.

However, losses also expand quickly in down markets.

Leveraged ETFs are often unsuitable for long-term holding.

If the underlying index moves up and down repeatedly, volatility decay can reduce returns even when the directional view is correct.

Adding leverage to a volatile industry such as semiconductors increases investment difficulty materially.

When the AI semiconductor cycle is strong, these products can generate substantial gains, but they can also react sharply to earnings reports, export controls, interest-rate shifts, and changes in capital spending plans.

For this reason, leveraged ETFs should not be treated as products to buy simply because the sector appears likely to rise.

They are more appropriately viewed as tools to use only when the investor can tolerate significant drawdown risk.

10. The key point investors often miss: markets discount disappointment in advance

The stock market does not move only on current earnings.

It prices in future expectations.

Semiconductor shares are strong today partly because current results are solid, but also because the market expects AI demand to keep expanding.

When expectations become too high, even small disappointments can cause large price moves.

For example, HBM supply may grow faster than expected, putting downward pressure on pricing.

Competitors may narrow the technology gap.

Nvidia demand expectations may soften.

The United States or China may expand domestic semiconductor usage.

AI data center investment may slow.

Markets often react before these changes appear in reported numbers.

That is why semiconductor ETF investors should not rely only on the statement that the industry is attractive.

They should also consider how much of that optimism is already embedded in valuations.

11. In the AI era, handing investment judgment over to AI is risky

Another important issue in this discussion, alongside semiconductor ETFs, is how AI is used.

Many investors now ask AI for stock ideas.

“Which ETF is best?”

“Should I buy Samsung Electronics?”

“What is the outlook for SK Hynix?”

“Recommend AI semiconductor stocks.”

The problem is that AI responses can sound convincing while still being wrong.

This is especially true in areas such as economics, finance, and international politics, where current information and interpretation matter.

AI can describe a summit that has not yet happened as if it already took place.

It can present old data as current information.

It can combine earnings results, policy developments, and interest-rate forecasts inaccurately.

Investors become vulnerable when they treat AI responses as definitive answers.

AI should be used as a tool to support judgment, not as a substitute for decision-making.

12. Collective intelligence: not asking AI for answers, but thinking with it

This leads to the concept of collective intelligence.

Collective intelligence combines human judgment and AI capabilities to improve decision-making.

Many people use AI by asking a single question and accepting the answer as the final result.

That approach is closer to outsourcing thinking to AI.

What matters is treating the first response as a starting point, not an endpoint.

After AI responds, ask again.

Challenge the output.

Request opposing arguments.

Ask for risks.

Compare the result with your own view.

For example, an investor reviewing a semiconductor ETF could ask:

- “Summarize the strongest counterarguments to the case for semiconductor ETFs.”

- “Which companies would be most affected if HBM demand slows?”

- “Break down the risks that the U.S.-China semiconductor conflict poses to Korean memory semiconductors by scenario.”

- “Identify any areas where my view of semiconductor ETFs may be overly optimistic.”

- “Explain the loss structure of holding a leveraged ETF for more than 6 months.”

Using AI in this way produces better judgments than simple information retrieval.

AI is not replacing the investor’s reasoning process; it is extending it.

13. The gap in AI usage between professionals and general users may widen further

Professionals can verify AI outputs.

If AI makes an error, they can identify it immediately.

“This is based on outdated material.”

“This policy has not been announced yet.”

“These figures do not match the latest earnings.”

They can correct the model and refine the analysis.

By contrast, users with limited domain knowledge may accept convincing answers without scrutiny.

In that case, AI can weaken judgment rather than strengthen it.

The same applies to investing.

If you buy a stock simply because AI recommended it, the decision is not truly yours.

If the stock falls, it is easy to conclude that “AI is not ready yet,” but the real issue is how the tool was used.

AI should be used to test assumptions, generate opposing views, and identify risks, not to replace independent reasoning.

This is one of the most important changes in stock investing during the AI era.

14. The most important points other coverage often misses

First, the real risk for semiconductor ETFs is not a decline in semiconductor demand.

The larger risk is that demand growth itself encourages countries to restructure supply chains around domestic interests.

As semiconductors become more strategic, pressure to reduce dependence on Korean firms may intensify.

Second, HBM is the leading technology today, but it may not remain the long-term standard.

If AI architectures change or a new method reduces memory bottlenecks, expectations centered on HBM may be revised.

In technology, “best today” does not guarantee “dominant tomorrow.”

Third, thematic ETFs may look diversified while actually concentrating risk.

Even if a semiconductor ETF holds many stocks, true diversification is limited if the holdings are exposed to the same industry cycle, policy risk, and AI investment expectations.

Fourth, the United States and China are both customers of Korean semiconductors and future competitors.

They currently depend on Korea for high-value memory due to technological gaps, but both are likely to pursue domestic alternatives over time.

Fifth, the core of the AI investment era is not AI itself, but the person using it.

Investors who accept AI-generated stock ideas, outlooks, or reports without verification become vulnerable.

AI should be used as a discussion partner, not an answer engine.

15. A checklist investors should review now

If you invest in semiconductor ETFs or AI-related semiconductor stocks, ask the following questions:

- Is my portfolio overly concentrated in one semiconductor theme?

- Am I mistaking a semiconductor ETF for true diversification?

- Do I understand the volatility decay structure of leveraged ETFs?

- Can I tolerate losses if HBM demand slows?

- Have I considered the impact of U.S. and Chinese semiconductor self-sufficiency policies on Korean companies?

- Have I accounted for the possibility that sovereign AI will increase demand while also accelerating supply chain restructuring?

- Am I independently verifying the investment information provided by AI?

- Have I considered the effects of interest rates, exchange rates, and global growth slowdown on semiconductor valuations?

16. Conclusion: semiconductors remain attractive, but current conviction may be excessive

The semiconductor industry will remain important.

Demand is likely to continue expanding across AI, EVs, robotics, autonomous driving, data centers, and defense technologies.

However, in investing, the most dangerous phrase is “this cannot lose.”

Believing that semiconductor ETFs are safe, that HBM will remain dominant indefinitely, or that semiconductors alone are sufficient for the AI era requires caution.

The correct response is not to avoid semiconductor investing altogether.

Rather, it is to analyze it more precisely.

Industry growth, technology shifts, global supply chains, the U.S.-China semiconductor conflict, sovereign AI, interest-rate trends, ETF structure, and leverage risk all need to be assessed together.

In addition, AI-era investors should not assign decision-making to AI.

They should question, challenge, and verify with AI to build collective intelligence.

Ultimately, the most important investment asset in the AI era is not AI itself, but the investor’s own judgment.

< Summary >

Semiconductor ETFs have gained popularity as AI semiconductor and HBM demand has increased.

However, industry growth and ETF returns are not the same.

HBM is currently strong, but expectations could change quickly if new technologies emerge.

The United States and China are strengthening domestic semiconductor supply chains, creating long-term risks for Korean semiconductor market share.

The spread of sovereign AI may increase semiconductor demand while also encouraging supply chain restructuring.

Thematic ETFs may appear diversified but can still represent concentrated exposure to one sector.

Leveraged ETFs require a clear understanding of volatility decay and downside risk.

Rather than relying on AI recommendations directly, investors should use AI to test assumptions and improve judgment.

[Related Articles…]

- AI Semiconductor Cycle: Key Variables After HBM

- Sovereign AI and the Restructuring of Global Supply Chains

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 반도체 ETF, 정말 안전할까? AI 시대 투자자가 놓치면 안 되는 위험 신호 | 경읽남과 토론합시다 | 이시한 교수님 [1편]