● AI-Beta ETF, Next Big Winner

How to Capture the Next U.S. AI Market Leader: Key Takeaways on the KIWOOM U.S. AI Tech High Beta ETF

This is not a standard ETF introduction. It explains (i) why U.S. equities have recently rotated through sharp rallies across themes such as memory semiconductors, optical networking, quantum computing, power infrastructure, and aerospace, and (ii) why individual investors struggle to track these shifts in real time. It then outlines how “next leader” identification has changed, why a high-beta framework can surface early leadership candidates, and how the KIWOOM U.S. AI Tech High Beta ETF (scheduled to list on May 12, 2026) is designed to reflect this market structure.

1. Market Context: This Is No Longer a “Buy Mega-Cap Tech Only” Environment

Market attention has broadened beyond traditional large-cap technology names. As AI-related benefits diffuse into small- and mid-cap innovation segments, the set of high-performing names has diversified.

Themes taking leadership in rotation include:

- Memory semiconductors

- AI data centers

- Optical networking

- Quantum computing

- Power equipment and grid infrastructure

- Nuclear power

- Aerospace

This environment can create opportunity but also increases the risk of performance-chasing, as broad interest often peaks after significant price appreciation.

2. Why Capturing the Next Breakout Is Structurally Difficult

Innovation themes rotate rapidly (e.g., memory → optical networking → quantum → power infrastructure). For individual investors, continuously tracking industry dynamics, earnings, technology shifts, technicals, and flow data is operationally challenging.

Additionally, many thematic ETFs are launched after themes are already widely recognized, reinforcing the perception that late-stage products may coincide with mature positioning.

In response, one approach shifts from explaining known themes to statistically identifying where the market is currently most sensitive.

3. Core Concept: What “High Beta” Means

High beta refers to stocks that, on average, move more than the broader market. If the S&P 500 rises 1% and a stock tends to move 2%–3%, that stock is considered higher-beta.

Implication:

- Up markets: potential for amplified gains

- Down markets: potential for amplified losses

This is structurally a high-risk, high-return exposure.

4. Why High-Beta Names Often Overlap With Current Market Leaders

Many market-favored stocks share elevated price sensitivity driven by narrative, expectations, and positioning rather than fundamentals alone. Themes such as AI infrastructure build-out, data center investment, quantum commercialization, or aerospace expansion can be priced in ahead of realized earnings.

In this context, beta can serve not only as a volatility measure but also as a proxy for concentrated investor attention.

5. ETF Structure: AI + Frontier Tech Exposure via 30 High-Beta Stocks

KIWOOM U.S. AI Tech High Beta ETF (listing planned for May 12, 2026) is structured as follows:

- Excludes U.S.-listed stocks below a specified size threshold

- Builds an innovation universe focused on AI and frontier technology

- Selects the 30 stocks with the highest beta within that universe

- Determines weights using both market capitalization and beta

- Rebalances quarterly to reflect updated innovation leadership

A key design element is that the portfolio is not limited to AI semiconductors. By incorporating “frontier tech,” the strategy is positioned to capture leadership even if innovation shifts beyond core IT segments (e.g., nuclear, aerospace, power infrastructure, digital assets, quantum).

6. Why Quarterly Rebalancing Matters

High beta is not permanent. As companies mature and market capitalization increases, beta can compress. Conversely, newly emerging innovators can see beta rise sharply as market attention shifts.

Quarterly rebalancing is intended to:

- Reduce persistence risk (holding prior leaders after sensitivity declines)

- Increase responsiveness to newly emerging leadership cohorts

The structure is designed for systematic rotation rather than static exposure.

7. Portfolio Interpretation: A Multi-Theme Innovation Basket

Based on the described pre-listing portfolio, holdings reportedly include a mix of names such as Sandisk, Vertiv Holdings, Coherent, Celestica, and Rocket Lab, indicating diversified exposure rather than single-theme concentration.

Representative thematic exposures include:

- AI semiconductors

- AI data centers

- Optical networking and communications infrastructure

- Digital asset-related equities

- Aerospace

- Power infrastructure

- Quantum computing

This resembles a consolidated allocation to multiple innovation vectors rather than a narrow industry ETF.

8. Historical Behavior: Strategy Composition Shifts With Market Regimes

A rules-based framework allows evaluation via historical selection under consistent criteria. The described examples indicate:

- Around 2024: heavier exposure to early AI leaders (e.g., Nvidia, AMD, Super Micro Computer, Palantir)

- Subsequently: increased representation of names such as Broadcom, Micron, and power-related stocks

- More recently: additions skewing toward optical networking, aerospace, and emerging infrastructure names

This pattern is consistent with an AI investment cycle spreading across adjacent beneficiaries, with beta used as the mechanism to track that diffusion.

9. Illustrative Case: Early Identification of Nvidia (Back-Test Reference)

The manager’s description highlights that, in simulation, the methodology would have included Nvidia as early as 2016—prior to its current mega-cap status—at a stage when narrative-driven sensitivity and innovation positioning were more pronounced.

The stated intent is less about owning already-consensus mega-caps and more about reducing the probability of missing future large winners during earlier phases of market recognition.

10. Potential Advantages: Investor Fit

Key potential benefits include:

10-1. Systematic exposure to emerging leaders without single-stock selection

Rules-based selection may reduce reliance on discretionary stock picking across rapidly shifting innovation themes.

10-2. Reduced dependence on a single theme

The approach is not constrained to semiconductors, aerospace, or quantum as standalone allocations.

10-3. Quarterly updates to incorporate evolving leadership

Rebalancing cadence is designed to keep exposure aligned with fast-moving market focus.

10-4. Diversification versus individual stocks

A 30-stock structure can reduce idiosyncratic risk relative to concentrated single-name positioning.

10-5. Upside participation in risk-on regimes

High-beta construction aims to increase participation during broad equity uptrends.

11. Risks and Constraints

This is structurally a high-volatility product.

11-1. Larger drawdowns in risk-off regimes

When sentiment deteriorates, high-beta stocks can decline faster than the market, particularly where valuation is expectation-driven.

11-2. Potential tilt toward small- and mid-cap equities

High beta is more frequently observed in smaller companies; in mega-cap-led markets, relative performance may lag.

11-3. Higher behavioral difficulty for long-term holding

Even if long-term returns are attractive, interim volatility can be difficult for investors to tolerate.

11-4. Greater dependence on narrative and flows

When positioning and narratives weaken, price responses can reverse sharply.

12. Practical Use Case

The strategy is better suited as a satellite allocation for aggressive growth exposure rather than a core defensive holding.

Potentially suitable for investors who:

- Want broad exposure to U.S. AI and innovation growth themes

- Prefer a systematic approach to reduce the risk of missing rotating leaders

- Seek higher sensitivity in up markets

- Operate trading-oriented or higher-risk portfolios

Less suitable for investors prioritizing dividends, defensiveness, or low volatility.

13. Complementary Framework Mentioned by the Manager: Combining With Momentum

The manager also referenced pairing high beta with momentum. High beta targets amplification; momentum targets trend persistence. A combined framework may balance “high sensitivity” with “confirmed directionality,” consistent with multi-factor portfolio construction.

14. News-Style Summary

- The KIWOOM U.S. AI Tech High Beta ETF is scheduled to list on May 12, 2026

- Invests in 30 high-beta U.S.-listed innovation companies

- Covers AI and frontier technology to increase thematic breadth

- Rebalances quarterly to reflect evolving innovation leadership

- Potential exposure spans semiconductors, data centers, optical networking, quantum, power infrastructure, and aerospace

- Higher upside potential in up markets; elevated drawdown risk in down markets

- May serve as a systematic tool to access emerging leaders for investors who do not want single-stock selection

15. Key Point Often Underemphasized in Coverage

The central point is not the product label but the change in market structure. AI exposure has broadened from a narrow set of mega-cap leaders to a wider ecosystem including infrastructure, power, optical networking, memory, cooling, aerospace, and quantum.

The framework implies a shift from “identifying one dominant AI leader” to “tracking where the next rotation within the AI ecosystem is occurring.” The ETF is positioned as a systematic method for following innovation-theme rotation rather than a guaranteed-return vehicle.

< Summary >

The KIWOOM U.S. AI Tech High Beta ETF is a high-volatility, growth-oriented ETF selecting 30 high-beta U.S. innovation stocks. Its core design is quarterly rotation across current innovation beneficiaries spanning AI, data centers, optical networking, power infrastructure, aerospace, and quantum. It may outperform in risk-on environments but can experience deeper drawdowns in risk-off regimes. The strategic intent is to systematize exposure to rotating innovation leadership rather than depend on discretionary selection of individual market leaders.

[Related Articles…]

- https://NextGenInsight.net?s=AI

- https://NextGenInsight.net?s=ETF

*Source: [ 소수몽키 ]

– 샌디스크 마이크론을 놓쳤다면? 다음 대장주를 미리 찾는 방법

● Warsh Rate Cut Shock, AI Deflation, Treasury Turmoil

Is Kevin Warsh’s Rate-Cut Scenario Plausible?

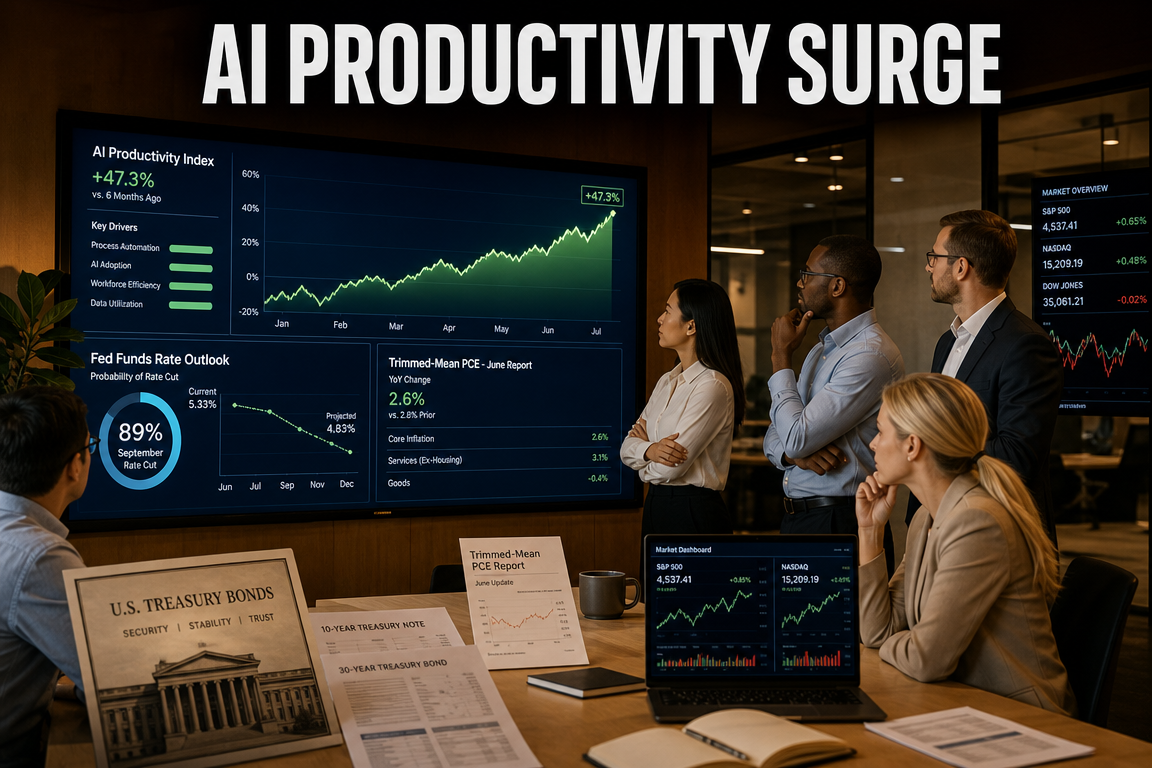

A Structured Review: May Treasury Volatility to the “AI Productivity” Rationale

The issue centers on three points:

1) Warsh seeks to revise the Federal Reserve’s inflation-assessment framework.

2) He argues for a dual strategy: cutting policy rates while continuing balance-sheet reduction.

3) He positions AI-driven productivity gains as a rationale for lower inflation pressure and a policy pivot.

This is not merely “a new argument for rate cuts.” It potentially affects the Fed’s policy framework, US Treasury yields, global financial conditions, and forward asset-price dynamics.

This report summarizes why these arguments are emerging, why May Treasury yield volatility could intensify, the likelihood of internal Fed disagreement, and why AI/productivity is a weak near-term justification for easing. A final section highlights the under-discussed core risk: policy credibility.

1. Issue Overview

Fed Leadership Risk and the Market’s Key Question

The market’s core question is straightforward:

“Would a Warsh-led Fed accelerate the pace of rate cuts?”

Answering requires assessing three pillars:

- Inflation-measurement framework revision

- Concurrent balance-sheet runoff and rate cuts

- AI productivity as a disinflationary tailwind

The central constraint is not the internal coherence of the argument but whether it is accepted by FOMC participants. The outcome can affect rate expectations, Treasury yields, the USD, global risk appetite, and spillovers into markets sensitive to FX and foreign flows.

2. Pillar 1

Framework Revision: Why Trimmed-Mean PCE Matters

2-1. Current Fed Inflation Anchor

Key US inflation indicators include CPI, PPI, and PCE. The Fed has emphasized PCE, particularly core PCE, to gauge underlying inflation trends by excluding volatile food and energy components and reducing policy overreaction to transitory shocks.

2-2. What Trimmed-Mean PCE Measures

Trimmed-mean PCE excludes extreme price moves on both tails and averages the central distribution. The objective is to reduce outlier influence and isolate “trend” inflation.

2-3. Why It Supports a Rate-Cut Narrative

Trimmed-mean PCE can present a lower inflation signal than alternative measures in certain periods. A shift in the preferred indicator can shift the interpretation of the same macro environment from “inflation remains elevated” to “inflation is stabilizing,” thereby strengthening the case for cuts.

2-4. Why It Could Trigger Controversy

Adopting a new preferred metric may be perceived as opportunistic rather than neutral. If the methodology systematically trims upside inflation surprises, markets may interpret the change as understating inflation risk. This can become a credibility issue for a data-dependent central bank and raise doubts about institutional independence.

3. Pillar 2

Can the Fed Cut Rates While Shrinking the Balance Sheet?

3-1. What Balance-Sheet Reduction Implies

The Fed’s balance sheet expanded through large-scale purchases of Treasuries and MBS during crisis periods. Balance-sheet reduction withdraws liquidity via non-reinvestment of maturities and other runoff mechanisms, operating as a parallel tightening channel.

3-2. Warsh’s Claim: Less Liquidity, Lower Rates

The argument: balance-sheet runoff delivers tightening while policy-rate cuts deliver easing; used together, they can calibrate aggregate stance. The design also reduces the optics of easing before inflation is fully contained.

3-3. Why Treasury Yield Volatility Could Increase

Runoff weakens a structural source of Treasury demand, while Treasury issuance is likely to remain elevated. This combination can pressure long-end yields upward even if the policy rate is guided lower. The result may be a weaker transmission of “easing” to financial conditions.

Higher 10-year yields can reinforce USD strength and tighten conditions for emerging markets through capital flows and FX volatility, with implications for markets exposed to foreign participation and export sensitivity.

3-4. Asset-Market Implications

Rate cuts are typically supportive for equities. However, if long-end yields rise, valuation headwinds can intensify for duration-sensitive segments, including growth and AI-related equities. The policy mix could therefore generate a split outcome: dovish headline, mixed realized easing.

4. Pillar 3

AI Productivity as a Disinflationary Argument

4-1. Why AI Links to Inflation

AI adoption can raise productivity by enabling automation and higher output per unit of labor. Higher productivity can reduce unit costs and expand supply capacity, potentially lowering inflation pressure over time.

4-2. Where the Argument Is Reasonable

AI-driven efficiency gains are observable in software, customer support, analytics, marketing automation, coding assistance, and manufacturing optimization. As a structural force, AI could be disinflationary over the medium to long term.

4-3. Why It Is Weak as a Near-Term Rate-Cut Justification

The primary constraint is timing. Near-term inflation is still dominated by energy, wages, shelter, supply chains, and geopolitical risks. For example, an escalation in Middle East risk can lift oil prices and propagate cost shocks through transport and inputs. AI adoption is unlikely to offset such shocks on a monthly or quarterly horizon.

5. US Inflation Assessment

Why May Became More Critical

5-1. Reasons Inflation Could Re-accelerate

As base effects fade, services inflation may remain sticky and shelter and wage dynamics may not soften quickly. Geopolitical risks can further raise energy and input prices.

5-2. What Trimmed-Mean PCE May Miss

A more aggressive trimming approach can reduce sensitivity to broadening price shocks. While useful for trend detection, it can lag shifts in inflation psychology and risk underweighting pressures that affect consumer and market expectations.

5-3. Why This Connects to May Treasury Volatility

If markets conclude the Fed is interpreting inflation too optimistically to justify earlier cuts, long-end yields may react more sharply. Bond markets often price forward inflation risk and fiscal supply dynamics. This can produce a steeper curve: front-end easing expectations with higher long-end yields, complicating equity valuation and risk premia.

6. Why Internal Fed Consensus Is Difficult

6-1. The Chair Does Not Act Unilaterally

Policy is set by committee. A framework change is more sensitive than routine rate adjustments because it affects credibility, interpretability, and the perceived policy reaction function.

6-2. Why Division Risk Could Rise

Existing differences already exist across inflation interpretation, labor-market assessment, policy lags, and financial stability concerns. A push to change the inflation benchmark could face resistance from members emphasizing continuity and institutional stability. The proposal may be politically salient but institutionally costly.

7. Market Impact Summary (News-Style)

7-1. Rates / Bonds

Even with rate-cut signaling, balance-sheet runoff and Treasury supply pressure may prevent long-end yields from stabilizing. Bond markets may prioritize credibility and inflation risk over the policy-rate path.

7-2. Equities

Near-term risk appetite may improve on easing expectations. However, rising long-end yields would compress multiples for duration-sensitive segments, including growth and AI-linked equities. Equity direction may track Treasury yields more than the policy rate.

7-3. USD and FX

Policy ambiguity or higher US long-end yields can sustain USD strength, increasing upward pressure on USD crosses and tightening conditions for FX-sensitive markets.

7-4. Real Economy

AI productivity is supportive, but diffusion across the economy requires time. The link from AI to near-term inflation prints is uncertain, limiting its usefulness as an immediate easing rationale.

8. Under-Discussed Core Point

Policy Credibility Risk, Not the Rate-Cut Headline

The key risk is not whether cuts occur, but whether the Fed’s policy credibility and reaction function become harder to interpret.

If the Fed changes the inflation benchmark, cuts rates while shrinking the balance sheet, and cites medium-term AI productivity as near-term justification, markets may interpret this as a shift in the policy “language” and function.

When the reaction function appears to change, markets typically demand higher risk premia. Potential outcomes include higher long-end yields, a wider term premium, and renewed volatility. A dovish message can therefore produce outcomes associated with tighter conditions.

9. Bottom Line

Will the Three Pillars Materialize?

1) Trimmed-mean PCE is statistically meaningful, but using it to justify a framework shift now entails high credibility and political costs.

2) Balance-sheet runoff alongside rate cuts is mechanically feasible, but it may exacerbate Treasury yield instability and is not unambiguously market-friendly.

3) AI productivity is a plausible medium-term disinflation force, but insufficient as a near-term justification for cuts.

Overall, the framework provides a coherent blueprint to support rate cuts, but execution requires internal consensus and market trust. Markets may focus less on the policy-rate trajectory and more on Treasury yields and communication risk.

10. Investor Watchlist

- Whether FOMC members publicly reference trimmed-mean PCE or similar alternative inflation measures

- The interaction between balance-sheet runoff pace and Treasury issuance volume

- Divergence between policy-rate expectations and long-end Treasury yield moves

- Evidence of AI-driven productivity and cost improvements in reported earnings and operating metrics

- Whether geopolitical risk and energy prices feed into renewed inflation pressure

Warsh’s easing rationale rests on three pillars: adoption of trimmed-mean PCE, concurrent balance-sheet reduction, and AI-driven productivity gains.

The narrative is internally consistent but faces obstacles in FOMC consensus-building and market credibility. The primary risk is that Treasury yields rise despite rate-cut expectations, tightening conditions through a higher term premium.

AI may support medium- to long-term disinflation but is not a robust near-term basis for policy easing. The central issue is the potential instability caused by a perceived shift in the Fed’s policy framework and communication function.

[Related Articles…]

-

US Treasury Yield Surge and Asset-Market Repricing: Key Variables to Monitor Now

https://NextGenInsight.net?s=국채금리 -

The AI Productivity Revolution and the Global Economic Outlook: Sector Winners and Key Risks

https://NextGenInsight.net?s=AI

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 케빈워시의 금리인하 추진 ‘3가지 기적의 논리’, 5월 국채금리 불안 커질까? [즉시분석]