● AI-Memory Supercycle, Hidden Risks, Buy Now

Is It Too Late to Buy SK Hynix and Samsung Electronics? The Real Core of the AI Semiconductor Supercycle and the Key Risks

The key issue is not simply, “SK Hynix has already surged, so is it too late?”

The real focus is threefold:

First, why AI semiconductor demand is driving explosive earnings for memory manufacturers.

Second, whether SK Hynix and Samsung Electronics should still be valued primarily on P/B, or whether the market is shifting to P/E.

Third, which leading indicators determine whether the trend can persist, and where the most material risks are concentrated.

This report consolidates HBM, DRAM, NAND, Big Tech capex, long-term supply agreements (LTAs), AI inference demand, memory pricing, and valuation debates.

Most coverage stops at “AI is strong, HBM is strong.” This report addresses why the market is increasingly reluctant to treat SK Hynix as a purely cyclical stock, and how the equity may re-rate if that thesis weakens.

1. Executive Summary (News-Style)

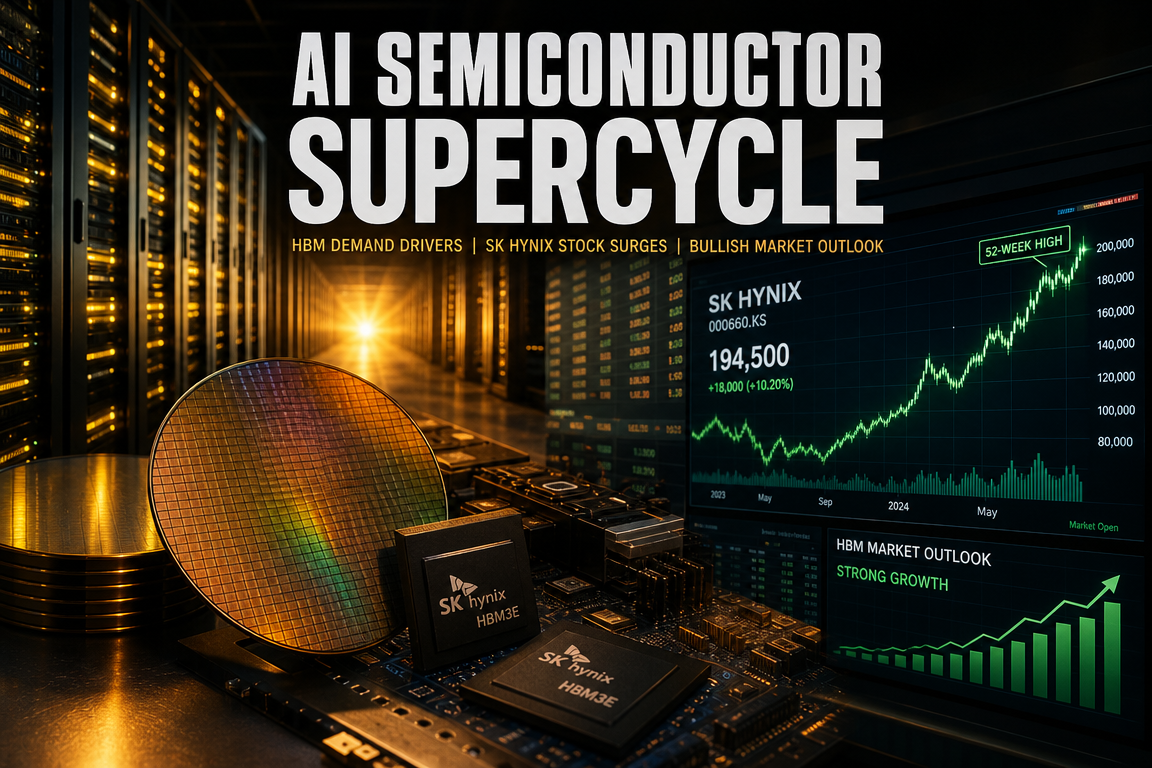

Key Point 1. The strength in SK Hynix and Samsung Electronics is not a generic semiconductor rebound. It reflects expectations of a structural shift driven by accelerating AI infrastructure investment and surging HBM demand.

Key Point 2. Memory has historically been categorized as cyclical; however, Big Tech LTAs and AI data-center expansion are changing the perceived quality and durability of earnings.

Key Point 3. Further upside requires more than “AI demand continues to grow.” The market will focus on whether Big Tech capex converts into sustained revenue and persists over multiple years.

Key Point 4. Forward tracking is increasingly centered on leading indicators such as OpenAI/Anthropic revenue, Google token processing metrics, spot/contract memory prices, and Big Tech RPO and capex.

2. What SK Hynix and Samsung Electronics Produce

Understanding memory requires a clear product taxonomy.

2-1. DRAM: Core “Working Memory”

DRAM is the short-term working memory used by PCs, servers, and smartphones. It is volatile memory (data is lost when power is off).

In AI servers, DRAM importance has increased due to the need to rapidly access and compute on large datasets during model execution.

2-2. NAND: Core Storage Component

NAND is the key input for storage such as SSDs. It is non-volatile memory.

If DRAM is the “workbench,” NAND is the “warehouse.”

AI adoption also expands storage demand: training datasets, inference logs, enterprise databases, and backups require persistent storage.

2-3. HBM: The Market’s Primary Focus

HBM stacks multiple DRAM dies vertically to optimize for high-performance compute workloads. It is typically integrated adjacent to GPUs to enable ultra-high bandwidth.

If Nvidia’s GPU is the compute engine, HBM is the high-speed data supply system. As a result, HBM has become one of the scarcest components in the AI compute stack.

3. Why SK Hynix and Samsung Electronics Have Rallied

3-1. The Key Driver: AI Inference Demand

The market response is increasingly tied to inference, not only training. Inference is the real-time process by which users query and receive outputs from generative AI systems.

Inference matters because AI is transitioning from R&D to scaled, daily usage across search, document workflows, coding, customer support, translation, automation, and agentic applications.

This usage intensity requires materially more memory than many investors initially assumed.

3-2. User Growth x Memory per User Growth

The mechanism is straightforward:

- More total users

- Higher memory use per user as tasks become more complex

- Rising concurrent sessions, increasing server memory requirements nonlinearly

Coding, reasoning, multimodal, and agentic workloads are more memory-intensive than basic Q&A.

Accordingly, memory demand is shifting from PCs/smartphones toward data centers.

3-3. Agentic AI Further Increases Memory Intensity

Agentic AI executes multi-step workflows: tool calls, search, state retention, and iterative reasoning. These require larger context and state, structurally increasing memory consumption.

If this trend persists, HBM, server DRAM, and high-performance SSD demand should remain supported.

4. Why Big Tech Capex Matters

4-1. Memory Earnings Are Ultimately Determined by Who Spends

SK Hynix and Samsung benefit because Big Tech is allocating substantial capital to servers and data centers.

Microsoft, Google, Meta, and Amazon have increased capex as AI infrastructure competition intensifies. This spending flows through to Nvidia, TSMC, SK Hynix, Samsung Electronics, and Micron.

Big Tech capex is therefore a direct driver of memory revenue and cash flow.

4-2. Rising RPO Is More Important Than Capex Alone

Capex should be assessed alongside whether it is tied to durable demand.

RPO (remaining performance obligations) acts as a contract-based proxy for future revenue. Rising RPO indicates AI-related demand is increasingly embedded in contractual business activity rather than being a short-lived investment cycle.

5. Why Supply Cannot Scale Quickly

5-1. Capacity Expansion Is Not a Push-Button Process

Memory supply cannot be expanded immediately. Land, cleanroom construction, power infrastructure, tool delivery, and process stabilization require time.

Meaningful output expansion often requires 18–24 months.

Therefore, rapid AI demand growth can create near-term supply tightness.

5-2. Tight Supply Typically Translates Into Pricing Power

When demand rises faster than supply, prices increase. In memory, pricing has an outsized impact on revenue and operating profit.

This dynamic is a primary driver of recent earnings acceleration at SK Hynix.

6. Why SK Hynix Earnings Are Exceptionally Strong

6-1. Price and Product Mix Improved Simultaneously

The earnings strength is driven not only by volume, but by a favorable environment to sell a higher share of premium products at higher prices.

HBM mix expansion, DRAM pricing strength, and overall supply tightness have materially improved profitability.

6-2. Why Operating Margins Have Reached Unusually High Levels

A key market surprise has been the magnitude of operating margin expansion, exceeding typical manufacturing benchmarks.

This reflects bargaining power shifting toward suppliers. HBM is difficult to substitute and critical for AI systems, increasing pass-through capability.

7. Core Valuation Debate: P/B vs P/E

This is central to the investment decision.

7-1. On P/B, Valuation Appears Elevated

P/B compares market capitalization to net asset value. Historically, memory companies were valued on P/B due to earnings volatility and cycle risk, which can distort P/E.

Under this lens, current valuation can be interpreted as above historical norms.

7-2. On P/E, Valuation Can Appear Low

P/E compares market capitalization to earnings. In a profit expansion phase, P/E can compress rapidly.

This supports the argument that current valuation may be inexpensive relative to history or global semiconductor peers.

7-3. The Determining Question

“Are current earnings temporary, or structurally more durable?”

If the market concludes the earnings model has structurally improved, a P/E-driven re-rating is possible. If not, valuation may revert to a P/B-centric framework.

8. Why the Market Argues “Earnings Quality” Has Improved

8-1. Memory Historically Exhibited Classic Cyclicality

PC and smartphone demand swings drove abrupt order cuts. Fixed capacity then amplified profit volatility. Product differentiation was limited, reinforcing commodity characteristics.

Investors therefore discounted peak earnings.

8-2. Demand Is Becoming More Data-Center-Centric

Data centers are becoming the primary demand pillar. AI services require continuous operation; once infrastructure is deployed, it becomes a platform for additional services.

This increases perceived repeatability and durability of demand.

8-3. LTAs Change the Rules

A central shift is the expansion of long-term supply agreements (LTAs).

If Big Tech commits to 3–5 year procurement, including prepayments, cancellation flexibility declines and revenue visibility improves.

This implies not only stronger sales, but improved order quality and earnings stability.

9. Reference Case: Transformer Industry Re-Rating

The market cites power transformers as an analog. Previously viewed as cyclical, the sector was re-rated as AI data centers and grid investment structurally increased demand.

As backlog accumulated and earnings durability improved, valuation became less anchored to asset value alone.

Proponents argue memory is undergoing a similar transition.

10. Leading Indicators to Monitor

Waiting for quarterly earnings is increasingly insufficient; leading signals matter.

10-1. OpenRouter Token Usage

Token usage can serve as a utilization proxy for AI services, particularly where usage-based pricing applies.

Limitations: it is not fully representative of the entire industry.

10-2. OpenAI and Anthropic ARR

Rapid growth in annualized recurring revenue reinforces that generative AI is monetizing in practice.

Limitation: these companies do not fully represent the entire AI ecosystem.

10-3. Google Token Processing and AI Metrics

Google occasionally discloses token processing growth in earnings materials and technical publications.

Acceleration would be consistent with rising usage and data-center load.

10-4. DRAM and NAND Spot and Contract Prices

These are the most direct indicators of memory conditions.

- Spot prices reflect near-term sentiment.

- Contract prices reflect terms with large customers.

Broad strength across both typically signals a firm environment; weakness can quickly impact equities.

10-5. Big Tech Capex and Free Cash Flow

Sustained infrastructure investment requires funding capacity.

If capex continues rising while free cash flow deteriorates materially, the market may question sustainability.

The focus is not only “how much they invest,” but “how long they can sustain it.”

11. Primary Risks

11-1. Big Tech Capex Deceleration

The most direct risk is slower data-center investment. Because this is the core driver of memory earnings, deceleration can undermine both fundamentals and valuation narratives.

11-2. Deterioration in Big Tech Free Cash Flow

AI competition supports investment intensity, but the market can ultimately challenge capital discipline.

Rising leverage or weaker cash generation could reduce capex growth rates.

11-3. Macro Risks: Inflation, Rates, Geopolitics

Higher oil prices, supply shocks, and stagflation concerns can compress valuation multiples for growth and semiconductor equities.

Even strong earnings may not translate to performance if discount rates rise.

11-4. AI Industry-Specific Risks

A slowdown in key players’ growth or financing constraints could negatively impact sentiment.

The sector remains sentiment-sensitive due to its growth-stage characteristics.

11-5. Liquidity Diversion From Large IPOs

Mega IPOs (e.g., SpaceX) could redirect capital and create short-term flow headwinds independent of fundamentals.

11-6. Algorithmic and Architectural Efficiency Gains

A technical risk is improved memory efficiency in models and systems. If inference can be delivered with materially less memory, HBM and server memory growth rates could decelerate over time.

12. Differentiating SK Hynix vs Samsung Electronics

12-1. SK Hynix: Direct Beneficiary of AI Memory

SK Hynix has strong positioning in HBM, creating higher operating leverage to AI demand.

The equity has already reflected this expectation to a meaningful extent.

12-2. Samsung Electronics: Larger Scale and Broader Portfolio

Samsung spans memory, foundry, mobile, and consumer electronics.

As a result, memory upcycles may translate into a different magnitude and timing of equity response versus SK Hynix, with potentially lower volatility.

13. Underemphasized but Critical Point

The key issue is not simply “HBM is strong” or “AI is strong.”

The most important re-rating driver is contract structure, not only demand.

Valuation shifts occur when earnings stability becomes credible. LTAs, prepayments, shared equipment investment, and improved visibility can reduce perceived cyclicality.

If this framework weakens, the market may quickly re-impose a cyclical discount even if near-term earnings remain strong.

14. Practical Answer: Is It Buyable Now?

The industry backdrop is favorable, but the setup may not be “buy and ignore.”

Current prices reflect not only earnings momentum but expectations of AI supercycle durability.

Any position requires ongoing monitoring of:

- Big Tech capex

- AI revenue growth

- Memory pricing

- LTA adoption

- Real-world AI usage metrics

This is closer to an “actively monitored” exposure than a passive holding.

15. Implementation Checklist (Investor Monitoring)

- Whether HBM and server DRAM pricing remains firm.

- Whether AI-related earnings expectations translate into realized revenue.

- Whether rates, oil, and inflation pressure semiconductor multiples.

- Whether SK Hynix remains in a P/E re-rating regime or shifts back toward P/B mean reversion.

- Whether Big Tech capex remains resilient despite free cash flow pressure.

16. Conclusion

The recent strength in SK Hynix and Samsung Electronics reflects expectations of structural change in memory driven by AI inference growth and HBM demand.

SK Hynix is more directly exposed to HBM upside, and the market is increasingly open to valuing memory manufacturers differently than in prior cycles.

Continuation of this re-rating requires confirmation of sustained Big Tech investment, expanding AI service revenue, firm memory pricing, and durable long-term contracting.

In summary, the primary question is less “Is this a good company?” and more “How durable is the current demand and investment regime?”

< Summary >

The key drivers of SK Hynix and Samsung Electronics’ share price gains are expanding AI inference and surging HBM demand.

Memory has historically been cyclical, but data-center-led demand and expanding LTAs are improving perceived earnings quality and durability.

This has created a market debate on whether SK Hynix should be re-rated on P/E rather than anchored to P/B.

Key indicators include Big Tech capex, AI service revenue, token usage, DRAM/NAND pricing, and long-term contracting trends.

Conditions are constructive, but the investment case requires continuous monitoring rather than a passive approach.

[Related Articles…]

- HBM Market Restructuring and Opportunities for Korean Semiconductor Companies (NextGenInsight.net?s=HBM)

- How Expanding AI Data Center Investment Impacts Global Equities (NextGenInsight.net?s=AI)

*Source: [ 내일은 투자왕 – 김단테 ]

– 하이닉스, 삼성전자 사요?

● Palantir-Style Defense Boom, Quantum Shock, Drone Warfare

Why a “Next Palantir” Could Emerge in Korea: AI Defense, Asymmetric Warfare, and Quantum Security in One Framework

This topic extends beyond the conventional defense industry.

It requires a single, connected view of:

- why low-cost drones can exhaust high-cost missile defenses,

- why Korea’s AI-enabled defense stack is becoming a credible opportunity,

- why software startups can become central participants in defense markets, and

- why quantum computing could disrupt both digital asset ecosystems and broader cybersecurity architectures.

This report organizes the macro backdrop (fiscal expansion, geopolitical risk, and technological competition) and translates it into investable themes across AI, cybersecurity, dual-use technologies, and defense software.

Key focus points:

- why adaptable, rapidly reconfigurable systems are increasingly prioritized over “perfect” standalone weapons,

- why defense competition is shifting from hardware to software and AI, and

- why post-quantum cryptography is a shared national-security and digital-asset market issue.

1. Key News Briefing: The Strategic Picture Markets Are Pricing In

Modern conflict is shifting from traditional, platform-centric warfare toward asymmetric warfare.

Where high-performance, high-cost systems previously defined advantage, low-cost attack tools—assembled from commercial components, open-source AI, and civilian communications—are now pressuring expensive defensive architectures.

This is not only a military shift. It links to fiscal spending, industrial policy, inflation dynamics, supply-chain reconfiguration, and rising cybersecurity investment.

In practical terms: as warfare changes, spending flows change, creating new opportunity sets for Korean manufacturing, software, and AI companies.

2. What Asymmetric Warfare Means: Why a USD 20,000 Drone Can Stress a USD 4,000,000 Missile

Asymmetric warfare describes conflict between actors with materially different capabilities.

Recent dynamics show low-cost, rapidly manufacturable attack systems can impose unfavorable economics on high-cost defense systems.

2-1. The Cost Structure Has Reset

A representative case is the exchange between low-cost drones and high-cost interceptor missiles.

If a defender repeatedly uses multi-million-dollar interceptors against tens-of-thousands-dollar drones, tactical success can still translate into strategic fatigue over time.

This is fundamentally a cost-efficiency problem.

Future defense procurement is likely to prioritize the ability to neutralize large volumes of threats at low marginal cost, not performance alone.

2-2. Why Drones Improved So Quickly

The driver is composable innovation.

Drone capability gains have been accelerated by integrating commercial technologies:

- small engines,

- GPS modules,

- smartphone-grade components,

- commodity cameras,

- open-source AI models, and

- commercial communications.

Compared with decade-long development cycles for legacy platforms, 12–24 month iteration cycles using civilian tech stacks have demonstrated battlefield relevance.

2-3. Reconfigurability Is Becoming More Valuable Than Perfection

The central change is speed of adaptation.

Operational realities increasingly reward systems that can be modified during conflict:

- shifting from RF links to wired control under jamming,

- adding computer vision to improve targeting,

- switching to surface or underwater drones to bypass defenses.

Legacy prime-contractor models are structurally slower to match this pace.

As a result, modular weapon systems are gaining priority over monolithic “finished” systems.

3. The Shift Korea Must Prioritize: From Hardware Strength to AI-Enabled Defense Systems

Korea has established strengths in heavy manufacturing and defense exports (e.g., artillery platforms, automated munitions handling, precision tracking).

However, the center of gravity is moving from standalone hardware competition to integrated, software-defined systems competition.

3-1. Defense Differentiation Is Moving to Software

Contemporary operations depend on software-led capabilities:

- target recognition,

- autonomous decision support,

- threat prioritization,

- real-time data fusion,

- multi-drone control,

- electronic-warfare adaptation, and

- cyber defense.

Building high-quality hardware is insufficient without intelligent operating and orchestration layers.

This transition expands the addressable defense market for Korean AI startups, cybersecurity vendors, telecommunications firms, and robotics companies.

3-2. Why a “Next Palantir” Could Emerge in Korea

The core model is not “defense manufacturing,” but:

- processing security and operational data,

- integrating intelligence across sources,

- accelerating decision cycles, and

- extending the same platform to civilian domains (finance, security, enterprise risk).

This is the dual-use technology model: one stack serving both defense and civilian markets.

Korea combines:

- strong industrial capacity,

- high-quality ICT infrastructure, and

- a meaningful AI talent and startup base.

If major defense primes adopt open-innovation approaches and absorb civilian capabilities at speed, a Korea-based Palantir-like platform company is plausible.

3-3. Why M&A and Strategic Partnerships Matter Now

If defense primes build all components internally, iteration speed declines. Startups move fast but lack scale, procurement experience, and certification pathways.

Practical partnership patterns include:

- drone startups + defense primes (co-development and field integration)

- AI video analytics firms + target recognition systems

- communications security vendors + hardened military data links

- robotics firms + integrated ground/surface/underwater unmanned systems

- cybersecurity vendors + military network defense and monitoring

Future growth is likely to depend on how quickly civilian technologies can be operationalized into defense-ready capabilities.

4. AI Defense as a Structural Market: The Macro Case for Sustained Capital Allocation

Defense is increasingly treated as a structural budget category rather than a short-lived theme.

Even if active conflicts de-escalate, replenishment and security modernization cycles persist.

4-1. Fiscal Spending Is Likely to Remain Elevated

Many governments have drawn down inventories. Rebuild requirements include:

- missiles,

- munitions,

- air-defense networks,

- ISR and surveillance systems,

- communications equipment, and

- hardening of data centers and critical facilities.

Spending is likely to expand beyond replenishment into modernization.

4-2. War Reprices Energy and Supply-Chain Costs

Geopolitical risk elevates energy procurement costs and increases the cost of supply-chain diversification.

This can reinforce higher cost structures and inflation pressures, while growth can be constrained by uncertainty.

In such environments, defense and security spending often retain budget priority.

4-3. Tech Competition and Defense AI Are Converging

AI compute, communications networks, satellite infrastructure, quantum security, and cyber defense are increasingly interdependent.

Major powers are scaling civilian and defense technology stacks in parallel.

AI-enabled defense is therefore increasingly positioned as a long-cycle strategic industry.

5. A Underweighted Point: The Set of “War Participants” Has Expanded

Conflict influence is no longer limited to uniformed forces.

Modern battlefields incorporate:

- hackers,

- developers,

- drone operators,

- information operations participants, and

- civilian-aligned groups.

Cyberattacks on air defense, communications disruption, and data exfiltration can shift outcomes without kinetic engagement.

For Korean companies, this expands the definition of “security industry” to include cybersecurity, data platforms, AI analytics, and cloud infrastructure.

6. Drones Are Not Only Airborne: Ground, Surface, and Underwater Unmanned Systems

The unmanned systems landscape is broadening:

- aerial drones: ISR, loitering munitions, surveillance, electronic disruption

- ground drones: close-range strike, logistics, hazardous-area entry

- surface drones: port and maritime infrastructure offense/defense

- underwater drones: subsea cable and maritime route threats

Surface and underwater systems can affect energy transport routes and maritime logistics, with second-order implications for supply chains and commodity pricing.

For public markets, this supports a broader lens across defense, shipbuilding, security, communications, and maritime infrastructure.

7. Why Quantum Computing Is a Systemic Risk: The Primary Exposure Is Security Infrastructure, Not Only Bitcoin

Quantum computing is a cross-cutting issue spanning finance, defense, government data, and enterprise cybersecurity.

7-1. Cryptography Considered Safe Today May Not Remain Safe

Current public-key cryptography is secure under classical computing assumptions.

At scale, quantum computing may materially reduce the cost and time to break widely used schemes, weakening existing trust infrastructure.

7-2. Why the “Store Now, Decrypt Later” Strategy Matters

Adversaries can exfiltrate encrypted data today and decrypt it in the future once quantum capabilities mature.

This applies across:

- financial transaction data,

- government documents,

- corporate trade secrets,

- security logs, and

- defense datasets.

Quantum security is therefore a present-day investment and transition problem, not a distant technology topic.

7-3. Bitcoin’s Key Risk May Be Governance, Not Only Technology

Even if quantum threats can be mitigated technically, Bitcoin’s decentralized governance makes coordinated cryptographic transitions difficult.

Accordingly, governance and consensus risk can exceed the purely technical risk in digital-asset ecosystems.

8. Korea’s Priority Readiness Areas: Post-Quantum Cryptography and Security Automation

The core requirement is not incremental security tooling, but rapid migration to quantum-resilient cryptographic architectures.

8-1. Post-Quantum Cryptography Is Becoming Mandatory

Stakeholders requiring transition planning include:

- government,

- financial institutions,

- cloud providers,

- telecom operators, and

- defense contractors.

Migration is multi-year and system-wide; delaying until quantum capability is widely available increases operational risk.

8-2. “Crypto Agility” Becomes a Core Security Capability

Security advantage shifts from designing a single strong algorithm to building systems that can rotate cryptographic primitives quickly and reliably.

This increases the strategic value of:

- cryptographic lifecycle management,

- automated policy enforcement, and

- enterprise-wide security orchestration.

This domain is a potential growth vector for Korean security software vendors.

9. Implications for Korea’s Economy and Industrial Strategy

Korea has an opportunity to reposition from an export manufacturing base toward an AI-enabled security and defense technology provider.

9-1. Potential Beneficiary Industry Groups

- major defense primes and component supply chains

- drone and unmanned systems startups

- AI vision, sensing, and data analytics firms

- cybersecurity and quantum-security vendors

- telecommunications, satellite, sensor, and semiconductor firms

- robotics and autonomy-control software companies

9-2. Policy Directions That Would Accelerate Market Development

- lower barriers for startups in defense procurement

- expand dual-use technology programs

- scale defense AI testbeds and field trials

- establish a national roadmap for post-quantum migration

- train software-centric defense talent

- support prime–startup co-development and validation pathways

10. Three Underreported Takeaways

10-1. The Core of Future Conflict Is a “Productivity War”

Advantage increasingly depends on who can modify, produce, and deploy systems faster and cheaper, not who fields the most expensive platforms.

Military capability is increasingly tied to:

- manufacturing productivity,

- software iteration speed,

- AI deployment competence, and

- supply-chain agility.

10-2. Defense Is Moving Toward an “Operating System” Model

Strategic advantage may favor actors that can integrate sensors, drones, communications, AI, and cyber defense into a unified platform.

This increases the value of orchestration, interoperability, and data-centric architectures over individual platforms.

10-3. Quantum Security Is a National Infrastructure Theme

Quantum computing discussions often narrow to digital-asset pricing.

The primary exposure is protection of government records, financial infrastructure, defense data, telecommunications networks, and industrial IP.

Likely winners are not limited to crypto-adjacent firms, but include providers of post-quantum cryptography, network security, security automation, and data protection.

11. Conclusion: Korea’s AI-Enabled Defense Cycle Is Entering an Early Phase

Korea has established manufacturing capability, ICT infrastructure, and defense export experience.

The required transition is toward an integrated strategy combining:

- low-cost countermeasures,

- rapid adaptation,

- modular architectures,

- AI and software-defined capabilities, and

- quantum-resilient security.

If executed, Korea can move beyond exporting platforms toward providing security and defense technology platforms—creating conditions under which a Korea-based Palantir-like company could emerge.

< Summary >

Asymmetric warfare is changing defense economics, as low-cost drones can force disproportionate spending on high-cost interceptors.

Korea’s next defense opportunity is centered on AI, software, unmanned systems, cybersecurity, and quantum security integration rather than hardware alone.

Fiscal expansion and technological competition support a multi-year market for AI-enabled defense and security modernization.

Quantum computing threatens broad security infrastructure across finance, defense, and government; post-quantum migration is becoming a near-term priority.

Korea has conditions to evolve from a manufacturing exporter into an AI-enabled security technology provider, increasing the probability of a Korea-based Palantir-like platform company.

[Related Articles…]

-

K-Defense Export Expansion and the Reshaping of the Global Security Market: Key Takeaways

https://NextGenInsight.net?s=defense-industry -

The Dawn of Quantum Security: The Next Investment Opportunity in AI Security

https://NextGenInsight.net?s=quantum-security

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [풀버전] 제2의 팔란티어가 한국에서? AI 방산 시장이 열리고 있다 | 경읽남과 토론합시다 | 이명호박사