● AI-CAPEX-Showdown

Home Depot Upside, Google–Blackstone TPU JV, Meta 8,000 Layoffs: The Key Market Variable Is Whether AI Capex Remains Intact

Today’s tape reflected a convergence of factors: rising US long-end yields, the potential for JPY appreciation, Middle East geopolitical risk, semiconductor supply-chain uncertainty, and a reconfiguration of Big Tech AI infrastructure spending.

While the Nasdaq and semiconductors weakened on the surface, underlying flows continue to rotate toward AI semiconductors and data center infrastructure.

This report summarizes: why Home Depot’s results matter for the macro read-through; why a roughly KRW 37 trillion TPU-focused joint venture between Google and Blackstone could challenge a GPU-centric compute stack; why Meta’s 8,000-person reduction is better framed as an AI-driven productivity shift than a simple cost-cut; and what to monitor across US equities, rates, inflation, semiconductor supply chains, and AI capex.

1. US equity action: Weak indices, but the core tension is “macro tightening vs AI fundamentals”

US equities opened broadly lower:

- Nasdaq: down ~0.5%

- S&P 500: down at a similar magnitude

- Dow and Russell 2000: also negative

The primary pressures were:

- Upward pressure on US long-term Treasury yields

- Concerns over a potential JPY strengthening cycle and reduced yen-carry participation

This move is more consistent with a liquidity and discount-rate shock compressing high-multiple growth than with a sudden deterioration in corporate fundamentals.

2. Home Depot beat: A signal of US consumption resilience amid slowdown concerns

Home Depot delivered results above consensus and traded higher.

Home Depot is a useful macro proxy, reflecting housing-related activity, remodeling demand, household discretionary capacity, and DIY trends.

In a high-rate environment, housing transactions often slow, which can shift demand toward repairs and renovations of existing homes.

A better-than-expected print suggests US consumers have not fully retrenched and that “everyday, housing-adjacent” spending remains comparatively resilient.

This should not be extrapolated into broad-cycle strength. The current setup appears bifurcated: essential and housing-related spend holds up better, while rate-sensitive and non-essential categories show weaker momentum.

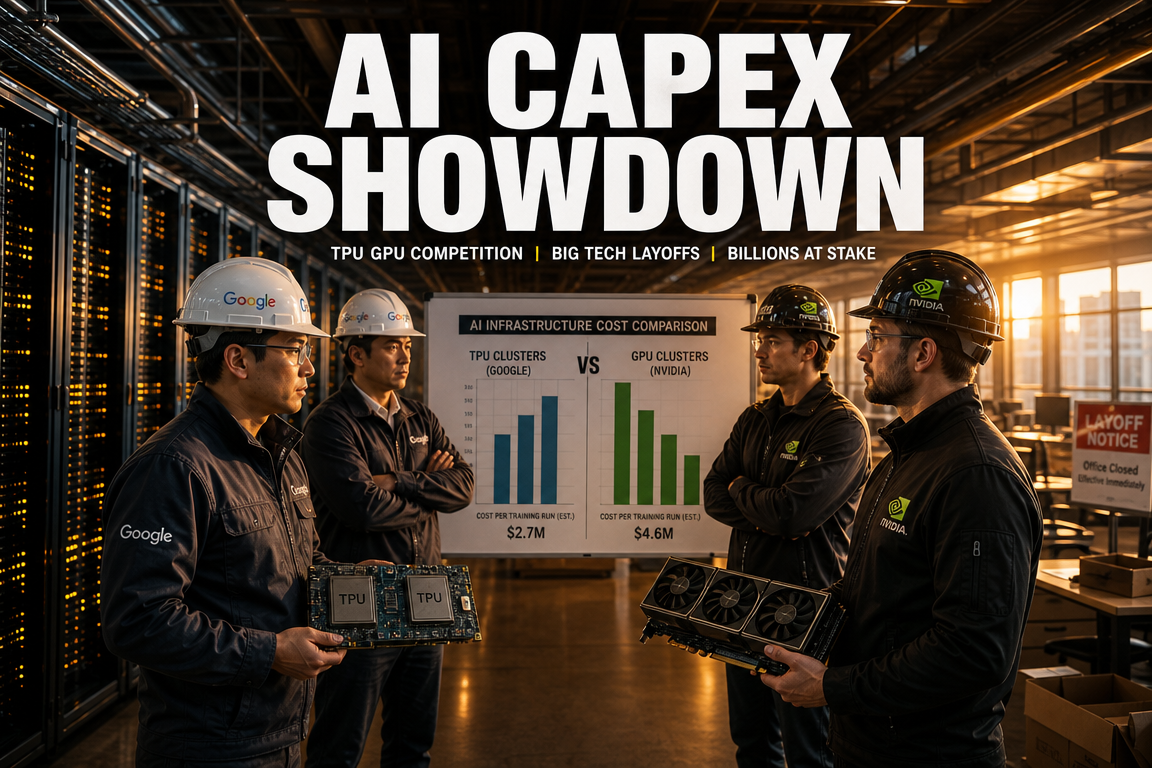

3. Google–Blackstone: ~KRW 37 trillion “TPU-dedicated” JV indicates a shift in AI infrastructure economics

One of the most consequential developments is the planned TPU-focused joint venture between Google and Blackstone, sized at approximately KRW 37 trillion.

This is less a headline investment and more an indicator that AI value capture is shifting from “models” toward “infrastructure.”

3-1. Why a TPU-dedicated vehicle matters

AI infrastructure has been largely GPU-centric. Google has long developed its own TPU silicon and is now positioning it not only for internal workloads but also as an externalized platform asset.

The participation of a large-scale capital provider such as Blackstone signals increasing institutional acceptance of TPU-based compute as a bankable infrastructure business, not merely a technical experiment.

3-2. Key market messages

- Data center AI investment is expected to remain elevated

- Competition expands from a GPU-only paradigm toward customized AI accelerators

- Big Tech aims to own more of the silicon and compute ecosystem, not only procure chips

- Private capital is beginning to allocate directly into AI infrastructure

AI exposure assessment should extend beyond software to semiconductors, power, cooling, servers, data center real estate, and cloud infrastructure.

4. Meta begins 8,000 layoffs this week: Not just cost reduction, but an AI productivity transition

Meta’s initiation of an ~8,000-person workforce reduction is structurally significant.

Rather than a pure cyclical retrenchment, it aligns with AI-driven productivity shifts inside large organizations. AI investment and headcount reduction are increasingly linked.

4-1. How to frame Meta’s action

- AI automation and agent deployment can expose role redundancy

- Capital allocation is shifting from labor spend toward AI infrastructure capex

- A “fewer people, more servers” operating model is becoming more prevalent

Importantly, workforce reductions do not imply lower AI investment; they can support higher capex intensity in GPUs, networking, model training, and data centers.

5. “US ceiling, Japan floor”: The macro variables constraining risk assets

This session is best understood through two macro constraints.

5-1. US ceiling: Long-end yields and the risk of 5.5% on the 30-year

Market commentary has highlighted the possibility of the US 30-year yield approaching 5.5%.

That level increases valuation pressure on long-duration growth equities, particularly high-multiple AI-linked names, by raising discount rates and compressing present values.

If higher energy prices reinforce inflation pressures, expectations for Fed easing can shift out, compounding the headwind.

5-2. Japan floor: Potential JPY appreciation and the unwind risk to carry

Japan is showing signs of stabilization, including stronger-than-expected GDP and lowered USD/JPY targets by major banks, reinforcing the possibility of JPY appreciation.

This matters because a meaningful portion of global risk appetite has been supported by yen-funded carry. If the yen strengthens and Japanese yields rise, capital can rotate back toward Japan and away from US tech and Asia semiconductor exposure.

A portion of the current drawdown appears driven by mechanical position adjustment rather than a demand collapse.

6. Another driver of semis weakness: Supply-chain cost shock, not demand erosion

Recent semiconductor downside has prompted questions about AI demand peaking. Available indicators do not yet support that conclusion.

A more relevant factor is supply-chain and input-cost risk.

6-1. Helium and energy cost sensitivity

Semiconductor manufacturing depends on specialty gases such as helium, not only electricity.

Elevated Middle East risk can disrupt Qatar-linked helium supply, logistics costs, and energy pricing.

This can pressure margins for manufacturers (e.g., leading foundry and memory producers) and raise input costs for AI data center operators, increasing sensitivity of earnings to cost inflation.

Semiconductor volatility may therefore reflect cost and supply constraints interacting with macro-driven positioning.

7. Why institutional capital continues to accumulate semiconductors

A key datapoint is positioning. 1Q 13F-related commentary suggests hedge fund semiconductor exposure remains near historical highs, while software exposure has moderated.

This indicates that despite near-term volatility, large pools of capital continue to underwrite a multi-year AI semiconductor and infrastructure cycle.

A simplified positioning interpretation:

- Retail investors de-risk into fear

- Passive flows reduce exposure mechanically as rates and FX shift

- Active “smart money” re-accumulates core AI assets into drawdowns

Distinguishing these flows is central to interpreting the current tape.

8. Why S&P 500 targets of 7,900–9,000 persist

Some strategists continue to publish S&P 500 targets in the 7,900 to 9,000 range despite pullbacks.

The underlying logic is:

8-1. Core bullish framework

- Residual system liquidity remains substantial

- AI can lift corporate productivity structurally

- Index-level earnings can be disproportionately driven by a narrow set of AI beneficiaries

This implies further index concentration risk: a small cohort of large AI-linked companies can dominate aggregate performance.

9. The dominant question: Has Big Tech begun to cut AI capex?

Despite numerous headlines, the key variable is whether Big Tech is reducing AI capital expenditures.

So far, evidence is limited. Meta is cutting headcount while maintaining AI investment; Google is scaling TPU infrastructure; Microsoft continues data center build-out.

Near-term volatility has increased, but AI infrastructure competition appears to be intensifying.

10. Headline summary

- Home Depot beat consensus, indicating downside resilience in US domestic demand

- Google and Blackstone plan a ~KRW 37 trillion TPU-focused JV, accelerating AI compute infrastructure competition

- Meta’s 8,000 layoffs are better interpreted as productivity-driven restructuring than AI capex retrenchment

- Rising US long-end yields and potential JPY strength are destabilizing global liquidity conditions and pressuring tech multiples

- Semiconductor weakness appears driven more by supply-chain cost risk and macro positioning than by demand collapse

- Hedge funds and other institutional allocators remain overweight semiconductors and AI infrastructure

11. Undercovered but central points

- The current correction is more consistent with liquidity reallocation than AI demand destruction

- Big Tech is reducing labor cost while expanding AI infrastructure investment

- TPU-centric initiatives suggest early diversification away from a single-vendor GPU compute stack

- Equity direction may become increasingly driven by AI capex persistence, sometimes more than near-term CPI prints

- Data center and AI infrastructure spending has reached a scale where near-term reversal is operationally difficult

12. Investor monitoring checklist

- US 10-year and 30-year Treasury yield trends

- Brent and WTI trajectories; indicators of Middle East risk stabilization

- Persistence of JPY strength and moves in Japanese government bond yields

- Guidance and outlook from Nvidia, Broadcom, AMD, TSMC, and major memory manufacturers

- Data center investment plans from Google, Meta, and Microsoft

- Whether AI-related capex is decelerating or being reallocated with greater precision

In sum, near-term volatility is likely to remain sensitive to rates, FX, energy, and geopolitics. From a medium-term perspective, the decisive factor is whether the structural AI semiconductor and data center investment cycle remains intact. Current evidence points more to “reallocation” than “retrenchment.”

< Summary >

Home Depot’s results suggest resilience in US domestic demand. The Google–Blackstone TPU initiative signals an escalation in AI infrastructure competition. Meta’s 8,000 layoffs align more with an AI productivity transition than with recession-driven austerity. US equities are pressured by higher long-end yields, potential JPY appreciation, and geopolitical risk, while institutional capital remains positioned toward semiconductors and data centers. The central question remains whether AI investment is being reduced; to date, the signal is “reconfiguration,” not “cutbacks.”

[Related Articles…]

- AI Infrastructure Capex Reallocation and the Next Winners in US Equities (https://NextGenInsight.net?s=AI)

- Opportunities in Semiconductor Pullbacks: What Smart Money Is Watching (https://NextGenInsight.net?s=Semiconductors)

*Source: [ Maeil Business Newspaper ]

– 홈디포, 컨센서스 상회 호실적 상승ㅣ구글-블랙스톤, 37조원 ‘TPU 전용’ 합작 법인 설립ㅣ메타, 이번주부터 8000명 감원 시작ㅣ홍키자의 매일뉴욕