● CPI Shock, Yen Carry Panic, Chip Risk

June Equities: Is the Real Correction Starting Now? A 2H Market Outlook Covering CPI, FOMC, FX, Yen Carry, and Semiconductors

June may represent more than a routine pullback. The U.S. CPI release could trigger a broad reassessment across rate expectations, FX, global liquidity, yen carry dynamics, and semiconductor earnings assumptions. This report summarizes (i) why the June 10 CPI may matter more than the June FOMC, (ii) why Korea and the U.S. may follow different rate paths, (iii) why yen-carry unwinds could reintroduce volatility, and (iv) why strong semiconductor earnings may still translate into equity headwinds. Key focus areas include expectation vs. outcome gaps, real policy rate differentials, market share shifts, and the direction of HBM and DRAM pricing.

1. In June, CPI matters more than the FOMC

The first major catalyst is the U.S. CPI release rather than the June FOMC. Markets typically react more to the data feeding the policy reaction function than to the statement itself.

- Key schedule: U.S. CPI release

- Next: FOMC decision, dot plot, and Fed communication

- Market focus: deviation from consensus, not the absolute inflation level

Equities are more sensitive to the gap between expectations and realized data. For example, if core CPI is expected at 3.0% and prints at 2.9%, risk assets may rebound even if inflation remains elevated. Conversely, a 3.1%–3.2% print can tighten financial conditions via repricing of Fed hawkishness, even absent an actual hike.

2. Inflation risk: focus beyond the headline print

The key question is not whether CPI rises, but whether energy-driven pressure is spreading across categories.

A headline increase driven primarily by energy may be interpreted as localized. Broad-based strength across food, core goods, and core services is more consistent with renewed inflation persistence.

- Headline CPI: potentially energy-led

- Core CPI: assess breadth across services, shelter, and goods

- Primary check: contribution shifts and spillover beyond energy

The CPI release functions as an early read on whether inflation is re-accelerating; both U.S. and Korean equities are likely to remain highly sensitive.

3. Why Korean equities may turn defensive ahead of CPI

Markets often reprice before the event. With a high-impact inflation print approaching, precautionary selling can emerge in advance.

Key transmission:

- Risk: upside CPI surprise

- Implication: more hawkish Fed messaging

- Result: rate-cut timing pushed out

When valuations are elevated and semiconductor/AI positioning is crowded, markets tend to react more asymmetrically to negative surprises, contributing to higher volatility.

4. Will the Fed hike again? Probability matters less than the fear premium

A near-term Fed hike is widely viewed as unlikely. However, markets can still destabilize if the perceived probability rises.

Real policy rates are central: the U.S. already maintains restrictive nominal policy rates, which may reduce urgency to hike again. Even so, markets can reprice quickly on incremental hawkish shifts.

- U.S.: restrictive policy settings already in place

- Interpretation: inflation uptick may not mechanically imply hikes

- Market behavior: high sensitivity to hawkish signaling

For June, the core issue is not hikes, but whether the Fed delays easing further.

5. Why Korea may diverge from the U.S.

Korea’s policy constraints differ. Even if inflation trends appear similar, Korea’s sensitivity to imported inflation and FX is structurally higher.

Imported prices transmit through producer prices into consumer inflation more directly, implying the Bank of Korea may react more quickly to renewed inflation pressure.

- Korea inflation drivers: import prices, FX, commodities

- Policy priority: pre-emptive containment risk

- Implication: while the Fed holds, Korea can face renewed tightening discussion

This divergence also influences USD/KRW. If Korea becomes relatively more restrictive while the U.S. stays on hold, the FX path could shift toward gradual KRW stabilization rather than sustained upside breaks.

6. FX is not just a number; it directly affects Korean equity resilience

A weaker KRW can support exporters in the short run, but it raises economy-wide input costs, weighs on domestic demand, and increases inflation pressure.

Semiconductor earnings may benefit mechanically from FX translation, but sustained KRW weakness can tighten conditions via higher costs and weaker consumption. Given Korea’s reliance on foreign flows, FX stability remains closely linked to KOSPI direction. A stronger KRW can be supportive for the index even if it moderates export earnings tailwinds.

7. Yen carry unwinds: why it is returning as a volatility driver

The yen carry trade links directly to global liquidity. As Japan tightens and the U.S. shifts toward eventual easing, U.S.-Japan rate differentials compress, reducing carry attractiveness and increasing unwind risk.

- Past: Japan ultra-low rates vs. U.S. high rates → carry expansion

- Now: Japan tightening vs. U.S. on hold / easing expectations → spread compression

- Result: renewed concern over carry liquidation

The key risk is speed. If Bank of Japan tightening signals intensify, markets may price a liquidity withdrawal shock that can affect U.S. equities, EM assets, and Korean equities.

8. Japan tightening is a global, not local, issue

Japan’s shift away from the ultra-low-rate regime changes the cost and availability of historically cheap JPY funding. This can affect global discount rates and liquidity conditions.

Through mid-2026, policy normalization across countries can re-emerge. Under such a regime, relatively less-hawkish U.S. policy could support U.S. assets, while other markets may face valuation headwinds.

9. Why semiconductors can deliver strong earnings yet face equity pressure

Equity prices reflect earnings relative to expectations, not earnings in isolation.

Samsung Electronics and SK hynix earnings may remain strong given AI-related demand, HBM, data center growth, and server upgrade cycles. However, if those expectations are already priced, results that merely meet consensus can still lead to consolidation.

- Real economy: semiconductor cycle remains constructive

- Capital markets: expectations appear elevated

- Conclusion: absent upside surprise, valuation pressure is plausible

This pattern has also been observed in mega-cap tech: strong prints do not guarantee positive price action when expectations are high.

10. Korea is being supported by semiconductors, increasing concentration risk

Semiconductors account for a large share of exports and growth contribution. This is both a strength and a risk: slower semiconductor growth can transmit more forcefully to aggregate activity.

Non-semiconductor sectors and domestic demand may lag, consistent with an uneven recovery profile.

11. The core earnings variables: Price (P), Volume (Q), and FX

Semiconductor earnings are driven by pricing, shipment volumes, and FX. Recent gains were supported by memory price increases and a weak KRW; forward sustainability requires monitoring.

- P: trajectory of DRAM, NAND, and HBM pricing

- Q: continuation of data center and AI-driven volume growth

- FX: persistence of KRW weakness as an earnings tailwind

Pricing is most sensitive. Spot market behavior in DDR4/DDR5 and NAND can raise peak-cycle concerns. HBM remains stronger, but increased supplier success can weaken pricing leverage.

Going forward, the market may focus more on the earnings growth rate than the earnings level. Even if profits rise, deceleration in growth can be priced negatively.

12. In the AI semiconductor cycle, market share competition is a key risk

AI and data center demand growth is structurally supportive. The primary question is distribution of value capture.

Korean memory leaders remain competitive, but dominance is less assured. Competitive and geopolitical supply-chain strategies matter.

- Micron: expanding presence in DRAM and HBM

- CXMT: accelerating domestic DRAM capacity and potential DDR5 expansion

- U.S./China: reinforcing domestic semiconductor value chains

This is increasingly strategic, not purely corporate. If technology leadership narrows, market share can erode over time.

13. HBM remains strong, but supplier expansion can pressure pricing

HBM is central to AI compute supply chains and currently commands premium pricing. The durability of that premium depends on how long supply remains constrained.

If additional suppliers scale successfully, buyers gain negotiating leverage. As bottlenecks ease, price pressure can emerge. Leadership rotations often begin during such normalization phases.

14. Under-discussed core points

Beyond a simplified “CPI up = down / CPI down = up” framework, five points are critical:

-

1) Markets price surprises, not levels.

Elevated inflation can still be risk-positive if it is below consensus; lower inflation can be risk-negative if it is above consensus. -

2) Korea may turn more hawkish than the U.S.

Different real rate levels and imported inflation sensitivity can drive earlier tightening bias. -

3) Semiconductor earnings and semiconductor equities are distinct.

Strong earnings can coincide with drawdowns if expectations are fully priced. -

4) The key risk is decelerating growth, not outright deterioration.

“Less good” can be priced harshly even when absolute results remain strong. -

5) Demand growth must be paired with market-share analysis.

Expanding AI demand does not ensure the same degree of value capture for Korean firms.

15. Practical monitoring checklist for post-June

- In CPI: evidence of broadening beyond energy

- FOMC: dot-plot shifts and Chair tone

- Bank of Korea: signals on renewed tightening risk

- USD/KRW path and foreign flow behavior

- Bank of Japan: additional hikes and carry unwind risk

- DRAM/DDR5/HBM pricing trends

- Samsung Electronics and SK hynix: results vs. expectations, not absolute levels

- Competitor momentum: Micron and CXMT market share trajectory

16. Summary: June is an expectations gap market

The current regime is defined by sensitivity rather than clear directional conviction. Inflation re-acceleration is not confirmed, but complacency is not warranted.

From a macro-to-equity linkage perspective:

- U.S. CPI drives the rate and liquidity narrative

- FX affects Korea’s relative asset attractiveness and foreign flows

- Yen carry dynamics influence global liquidity conditions

- Semiconductors anchor Korea’s earnings structure and index concentration

A coherent framework is: CPI → FOMC → FX → yen carry → semiconductor expectation reset.

< Summary >

June equities are primarily driven by the U.S. CPI as the main trigger. The key variable is the outcome relative to expectations, not the absolute inflation level. The Fed may not return to hikes, but markets can react sharply to hawkish signaling and delayed easing. Korea may respond more restrictively due to import-price and FX sensitivity. Yen carry unwind risk, tied to Japan’s tightening, can amplify volatility. For semiconductors, the market is likely to focus on growth-rate deceleration and market-share shifts rather than headline earnings strength. AI and data center demand remain supportive, but competitive pressure from Micron and CXMT warrants monitoring. A 2H framework requires integrating CPI, FOMC, FX, yen carry, and semiconductor pricing and market share into a single causal chain.

[Related Articles…]

- https://NextGenInsight.net?s=CPI

- https://NextGenInsight.net?s=semiconductors

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 6월 증시, 진짜 조정은 이제부터? CPI가 시장을 흔든다 | 클로즈업 | 월간특강 세미나 [3편]

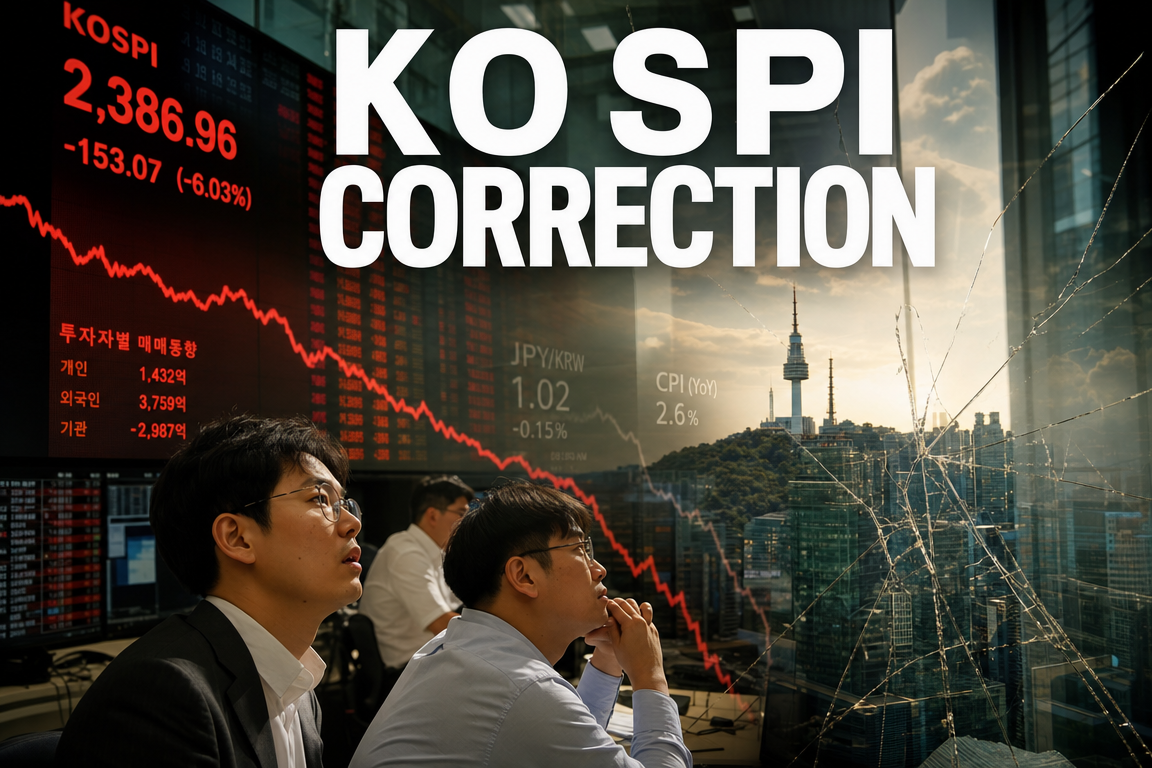

● Korea Stocks Crash, Samsung, Hynix Rout, AI Selloff

KOSPI Decline: Are Samsung Electronics and SK Hynix Still Investable? Key Drivers of the Current Pullback and Core Investment Considerations for Korean Equities and AI Semiconductors

The market focus currently centers on three issues:

First, whether the recent KOSPI decline reflects a one-day shock or an early signal that an overheated semiconductor-led concentration trade is beginning to unwind.

Second, whether the sell-off in Samsung Electronics and SK Hynix has largely played out or whether volatility may increase further.

Third, that this is not solely a Korea-specific development; it is linked to the global equity market structure concentrated in US AI and mega-cap technology leaders.

This report summarizes: why Broadcom’s results and guidance triggered outsized stress in Korea; why Korean equity volatility has exceeded that of the US; why leveraged investors face elevated risk; and the structural features of a late-stage concentration regime. The core message is that near-term risk is driven less by earnings prints and more by market structure and fragile capital flows.

1. What drove today’s sharp sell-off

The immediate trigger for the sell-off in Korean equities was disappointment around Broadcom’s earnings and, more importantly, the interpretation of weaker guidance relative to elevated expectations. This cooled sentiment in an overheated AI semiconductor trade.

US markets typically absorb such news with more diversification and internal shock absorbers. Korea differs materially: index performance is heavily concentrated in memory semiconductors, particularly Samsung Electronics and SK Hynix. As a result, modest US technology weakness can be amplified into larger index-level stress in Korea.

The transmission mechanism was visible through extreme moves, including sidecar activation and sharp declines in major constituents (e.g., double-digit losses in SK Hynix and mid-single-digit declines in Samsung Electronics).

2. Why Korean equities swing more than US equities

The primary driver is industrial and index composition.

US equity indices benefit from broader sector diversification: software, cloud, platforms, consumer, financials, and healthcare can offset weakness within AI-related names. Korean indices, in contrast, have concentrated AI upside exposure primarily through memory semiconductors, effectively compressing leadership into Samsung Electronics and SK Hynix.

This structural concentration increases beta and convexity: a move of 1 in US technology can translate into 2–3 in Korea, reflecting a market-structure vulnerability rather than sentiment alone.

3. Did Samsung Electronics and SK Hynix sell off due to deteriorating fundamentals?

The decline appears driven less by an abrupt fundamental deterioration and more by a positioning and expectation reset after significant capital crowding.

Earnings expectations did not disappear overnight; rather, the market had rapidly discounted a substantial portion of the forward upside. After strong multi-month advances (commonly cited near +90% for Samsung Electronics and +150% for SK Hynix in the recent upswing), the market becomes more sensitive to marginal disappointment.

In such regimes, valuation and expectation saturation tend to dominate over business quality in driving short-term price action.

4. The core issue is concentration, not the single-day drawdown

The key risk signal is not the magnitude of one-day losses, but the preceding concentration pattern.

While the prior three-month window may have appeared broad, the most recent one-month performance increasingly concentrated around Samsung Electronics and SK Hynix. Multiple sectors lagged or declined, including pharmaceuticals, utilities, consumer staples, machinery, defense, secondary batteries, power-related themes, chemicals, metals, construction, and brokers.

On shorter horizons (weekly), the number of advancing names contracted further, indicating weakening market breadth: indices held up while the average stock underperformed. This divergence typically reflects deteriorating internal market health.

5. Why KOSDAQ weakened first while large-cap KOSPI leaders held up

KOSDAQ had been weakening for an extended period. Capital rotated out of segments where earnings support or growth visibility weakened (e.g., gaming, parts of biotech, and secondary batteries) and into perceived higher-conviction large-cap semiconductor leaders.

This implies the index resilience was not broad-based; it relied on a narrow set of leaders. When those leaders begin to reprice, the market-level shock typically intensifies.

6. Why late-stage concentration can shift rapidly from greed to fear

Concentration markets can trend strongly on the way up, reinforcing momentum and underinvestment anxiety. The risk materializes during reversals.

Typically, weaker and neglected names break first, followed by second-tier leaders, and finally the core index anchors. When the final stage occurs, sentiment can shift rapidly from risk-seeking to risk-averse, and diversification benefits across underperformers may not hold; laggards often decline alongside leaders.

This dynamic is primarily structural and behavioral rather than company-specific.

7. The US exhibits similar concentration dynamics

The pattern is not unique to Korea. US equities have also been characterized by concentration in mega-cap technology and AI-linked names.

Headline index strength can mask sector dispersion, with relative weakness in areas such as utilities, materials, defense, and healthcare. Although the S&P 500 is structurally diversified, realized leadership has been heavily dependent on a small set of large technology and communication services companies.

This implies that a meaningful drawdown in US AI/mega-cap technology could transmit directly to Korean semiconductors.

8. How ETFs can amplify volatility

ETF flows can reinforce concentration.

When inflows rise, market-cap-weighted vehicles mechanically allocate more capital to the largest constituents, strengthening leaders and extending momentum. In outflows or rebalancing, the same mechanism increases selling pressure in those heavily owned leaders.

This creates a pro-cyclical effect: an “upside accelerator” during rallies and a “downside accelerator” during sell-offs, contributing to larger-than-historical daily swings.

9. Why leverage is particularly risky in the current regime

Leveraged products are most vulnerable when volatility expands.

If an underlying equity declines materially over a short period, leveraged ETFs typically experience larger drawdowns. In addition, path dependency and volatility drag can impair recovery even if the underlying rebounds.

In a regime where theme fundamentals may remain constructive but realized volatility is elevated, leverage can generate outcomes that are materially worse than directional expectations.

10. Is the semiconductor upcycle thesis still intact?

Over the medium term, the AI semiconductor theme, particularly HBM and memory technology upgrading, remains supported by structural drivers: AI server expansion, data center capex, and rising demand for high-bandwidth memory.

However, the market question has shifted from “Is the industry attractive?” to “Has price already discounted too much of the attractive future?” Sector fundamentals and equity timing are not equivalent; even strong industries can experience valuation-driven corrections.

11. The key risk: HBM pricing and forward guidance

The most sensitive forward variables are semiconductor pricing—especially HBM—and supply-demand guidance.

Markets generally discount 6–12 months ahead. If signs emerge of a future pricing peak or demand moderation, equities may reprice well before those fundamentals appear in reported results.

Given the reaction to guidance interpretation in the current episode, any formal signals of HBM price peak-out or demand deceleration could have outsized impact. The focus should be on whether expectations can continue to be revised upward, not only on current earnings strength.

12. KRW at 1,540 per USD: headwind or opportunity?

FX moves require context, particularly speed and drivers.

A rapid spike can signal systemic stress, while a gradual rise may reflect broad USD strength or macro differentials. Higher FX levels can increase import-cost pressure and potentially feed into inflation and rate expectations, which is a market headwind.

For domestic investors, higher FX raises the effective cost of US equity allocation, which can support relative interest in local equities. However, sustained support typically requires foreign inflows; recent conditions have included foreign selling after a sharp local run-up.

13. Jensen Huang’s Korea visit as a near-term catalyst

The market focus is less on the visit itself and more on potential messaging related to physical AI, robotics, data centers, and AI infrastructure.

Given the current concentration in two semiconductor names, credible catalysts that broaden the AI ecosystem beyond memory could support rotation into under-owned segments such as robotics, power infrastructure, AI components, automation equipment, and data center supply chains. Broader participation would improve market stability.

14. Portfolio action: buy or sell Samsung Electronics and SK Hynix?

A security-specific binary view is less effective than a risk-management framework.

It is difficult to justify either a definitive “end of cycle” conclusion or a high-conviction call for immediate renewed upside given the combination of large prior gains and elevated volatility.

For holders, all-in liquidation or unconditional holding is generally less robust than staged de-risking (e.g., reducing exposure incrementally over a defined horizon). For new entrants, chasing rebounds is less favorable than phased entry on pullbacks. Leveraged “dip buying” is among the highest-risk approaches in this volatility regime.

15. Key points (news-style summary)

① Immediate catalyst

Broadcom earnings-related disappointment and softer guidance interpretation cooled AI semiconductor risk appetite.

② Structural driver

Korean indices’ heavy weighting in Samsung Electronics and SK Hynix amplifies US technology shocks.

③ Internal market condition

Index resilience masked deteriorating breadth, with fewer advancers and accumulating weakness across multiple sectors.

④ Global parallel

The US also exhibits a concentration regime centered on mega-cap tech and AI leadership.

⑤ Primary risk

Not current earnings prints, but elevated expectations and sensitivity to changes in HBM pricing and forward guidance.

⑥ Strategy

Prioritize risk control via staged buying/selling over directional prediction.

16. Most underemphasized point: the market is structurally fragile

The core issue is not that Broadcom’s earnings were weak; that was a catalyst. The deeper risk is that the market has been supported by unusually narrow leadership.

A limited set of leaders (Samsung Electronics and SK Hynix in Korea; Nvidia and a small group of US mega-caps in the US) has carried index performance, with passive and ETF flows reinforcing the imbalance.

In this structure, small disappointments can break equilibrium. A high-quality business does not automatically imply an attractive entry point. The relevant question is the magnitude of embedded expectations and whether companies can continue to exceed them.

17. Key monitoring checklist

1) US AI semiconductor earnings and guidance

Broadcom, Nvidia, Micron: revisions to outlook and expectations will transmit to Korean semiconductors.

2) HBM pricing and supply-demand signals

Monitor for peak-out indicators and customer capex intensity.

3) Foreign investor flows

Assess whether foreign demand returns to Korean semiconductors despite FX headwinds.

4) Participation broadening beyond the two leaders

Rotation into robotics, physical AI, power infrastructure, data centers, and AI supply chains would support stability.

5) ETF flow dynamics

Passive inflows/outflows can materially amplify leader volatility.

18. Conclusion

The KOSPI decline should be viewed less as a single negative headline and more as evidence of vulnerability in an AI semiconductor concentration regime.

Samsung Electronics and SK Hynix may retain medium-term competitive positioning, but strong industry structure does not eliminate valuation and expectation risk. Current conditions favor risk management over conviction bets, diversification over concentration, and staged execution over momentum chasing.

A healthier market setup likely requires broader participation across the AI ecosystem rather than continued dependence on two semiconductor leaders. Until then, even strong rebounds may coexist with elevated volatility.

< Summary >

Broadcom-related disappointment triggered the sell-off, but the underlying issue is an overconcentrated leadership structure centered on Samsung Electronics and SK Hynix. Korea’s heavy semiconductor weighting amplifies volatility relative to US markets. Sector competitiveness may remain intact, but elevated expectations increase sensitivity to modest negative surprises. ETF and passive flows can magnify both upside and downside. Key watch items include HBM pricing, AI semiconductor guidance, foreign flows, potential catalysts tied to Nvidia’s leadership messaging, and evidence of broader AI ecosystem participation.

[Related Articles…]

- AI semiconductor investment strategy and key global equity market dynamics: https://NextGenInsight.net?s=AI

- FX surge and Korean equities: interpretation of foreign flow shifts: https://NextGenInsight.net?s=환율

*Source: [ Jun’s economy lab ]

– 코스피 하락, 삼전닉스 괜찮을까?