● Nvidias Real Bottleneck Revealed, Local AI Armageddon

The Primary Constraint Observed at NVIDIA GTC Taiwan Was Not Semiconductors, but Local AI Computing Architecture

This is not a routine event recap. The discussion connected key trajectories across AI, semiconductors, data centers, physical AI, and AI agents.

Mainstream coverage tends to focus on incremental themes (GPU sales, robotics as “the future,” rising interest in agents). On site, the more material questions were clearer:

- What NVIDIA views as the largest technical constraint

- Why residential “home AI servers” could become necessary

- Why CPUs regain importance in an agent-centric era

- Why physical AI remains pre-inflection despite high expectations

This report summarizes the core messages in a news-style format and highlights implications for industry structure, market outlook, and investment focus.

1. The most important takeaway from GTC Taiwan: the bottleneck is no longer GPUs alone

Markets still frame NVIDIA constraints as supply-chain issues such as HBM availability, packaging capacity, power delivery, and data-center build-outs. These remain relevant.

However, the more important shift is that NVIDIA is increasingly defining the bottleneck at a higher layer:

- Where AI workloads should execute

- Which data must be processed locally versus in the cloud

- Which computing architectures can operationalize agentic AI and physical AI at scale

The constraint is moving from semiconductor supply to system design, and from system design to operational architecture.

2. News-style summary: five core messages emphasized by NVIDIA

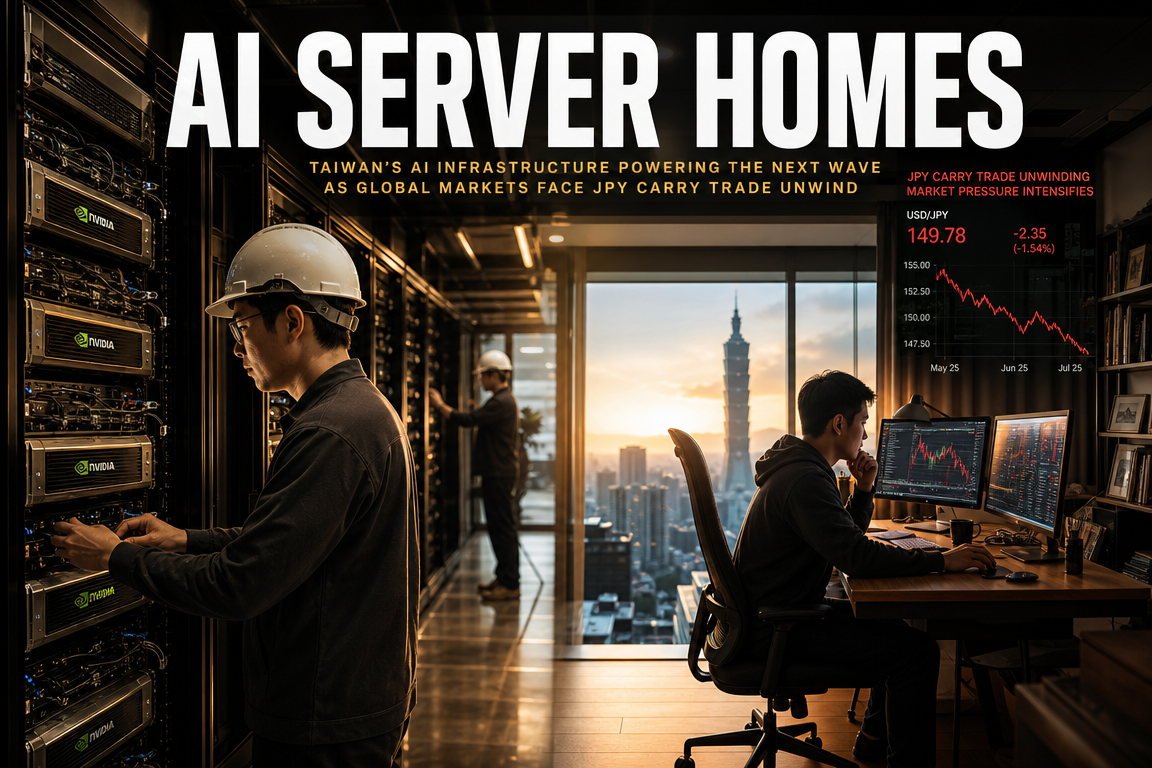

2-1. Preparing for an era in which every home may need an AI server

A key point in the AI agent sessions was the expectation that a “home AI server” becomes a standard component of future households.

This is not positioned as a high-end PC upgrade cycle. The primary rationale is sensitive-data handling:

- Authentication and identity data

- Financial data

- Documents and work artifacts

- Vehicle data

- Photos, voice, and ambient sensor data

NVIDIA’s implied operating model assumes AI runs continuously inside the home, reducing dependence on sending all data to the cloud.

This increases the relevance of RTX-based local AI machines, workstations, and standalone systems. The strategic direction is to extend AI compute endpoints beyond data centers into homes and enterprise internal environments.

2-2. The key technical constraint: deciding what runs locally vs what is sent to the cloud

A central on-site question was the largest technical challenge. NVIDIA’s answer emphasized that the constraint is not only compute performance, but the policy and boundary-setting for data placement and execution:

- Not all data can be processed locally due to capacity and cost

- Not all data can be sent to the cloud due to privacy, latency, reliability, and cost

This elevates hybrid architectures (neither 100% cloud nor 100% on-device) as the likely operating baseline.

Key determinants include:

- Privacy and compliance

- Latency requirements

- Power efficiency

- Connectivity and transmission costs

- Reliability and safety

- Offline operation requirements

Standardization of this hybrid boundary may become a major platform-level competitive axis.

2-3. Physical AI remains early-stage, but NVIDIA’s platform control is already advancing

Physical AI sessions conveyed a more conservative near-term stance than market narratives implying rapid mass commercialization of humanoids, autonomy, and industrial robotics.

Constraints remain concentrated in upstream capabilities rather than robot hardware alone:

- Simulation environment construction

- Synthetic data generation

- Policy learning and control

- Transfer validation from simulation to real-world

- Safety verification

- Pre-production iteration cycles

NVIDIA’s strategy is to control the platform layer used by competing robotics firms rather than competing as a single robot OEM. The ecosystem components cited include Isaac, Cosmos, Groot, digital twins, simulation tooling, and training infrastructure.

This structure positions NVIDIA to monetize regardless of which robotics providers ultimately win at the product layer, provided development and validation workflows depend on NVIDIA’s stack.

2-4. In an AI agent era, CPUs become strategically important again

Another notable theme was CPU revaluation.

Agent workloads are not single-pass inference. They include CPU-intensive orchestration and systems tasks:

- File-system operations

- Tool/function calling

- Sandbox and runtime management

- Retry and failure handling

- Integration with external applications

- Multi-agent scheduling and orchestration

The implication is that AI infrastructure investment expands from “GPU count” to full-stack infrastructure design: CPU, memory, storage, networking, power, and data-flow architecture.

2-5. CPUs also matter materially for reinforcement learning

A frequently overlooked point is CPU importance in reinforcement learning pipelines.

RL is iterative: execute, collect results, compute rewards, run simulations, and update policies. This structure can increase CPU utilization materially, especially in simulation-heavy domains such as robotics and physical AI.

Accordingly, evaluating AI semiconductor exposure based only on GPU supply provides an incomplete view; CPU architecture, memory bottlenecks, and data-movement costs become increasingly relevant.

3. Digital twins warrant reassessment: shifting from hype to operational infrastructure tooling

Digital twins re-emerged as a practical tool rather than a marketing concept. As data-center capex scales to very large levels, building without simulation becomes increasingly inefficient.

Pre-deployment digital-twin validation can reduce risk across:

- Power delivery

- Thermal behavior

- Network load and topology

- Rack layout and utilization

- Equipment efficiency

- Failure-point identification

This approach also extends beyond data centers to factories, logistics, automotive, robotics, and autonomous systems.

The framing presented: digital twins function as an industrial operating tool rather than a consumer metaverse narrative.

4. Investment framing: NVIDIA is evolving from a chip company toward an infrastructure-standard designer

Equity markets often treat NVIDIA as a leading semiconductor stock; this framing may be incomplete.

NVIDIA appears to target influence across four layers simultaneously:

- AI silicon

- Data-center infrastructure architecture

- AI development and deployment platforms

- Standards for robotics and agent ecosystems

Control of standards typically extends lifecycle durability beyond individual product cycles. If industries architect workflows and infrastructure around NVIDIA’s reference designs and tooling, competitive displacement becomes more difficult even when end applications change.

The differentiated advantage is less GPU performance in isolation and more ecosystem lock-in through end-to-end platform dependency.

5. How AI agents are changing developer workflows in practice

A representative on-site anecdote: a senior practitioner with decades of terminal-centric workflow reported materially reduced terminal usage after adopting coding agents over the prior months.

The practical implication is a shift from direct code production toward:

- Problem decomposition

- Agent instruction and supervision

- Workflow orchestration

This can lower barriers in areas such as front-end development, lightweight applications, prototyping, and automation tooling, enabling broader participation by non-traditional developers (e.g., designers, planners, domain specialists).

6. Macro linkage: why this trend matters beyond technology

These shifts have macroeconomic relevance.

6-1. A potentially extended capex cycle

AI infrastructure demand is not limited to server additions. It drives linked demand across:

- Data centers

- Power generation and grid upgrades

- Cooling systems

- Networking equipment

- Memory and storage

- Local AI devices

This supports the possibility of a longer-duration investment cycle, with implications for U.S. equities, semiconductor cyclicality, and global manufacturing activity.

6-2. Productivity gains may become more visible in reported outputs

If agents increase automation in operational workflows, labor cost structures and productivity metrics may change. Unlike prior AI waves criticized for slow monetization, agent systems may shorten the lag between adoption and measurable impact.

Early areas likely to show quantifiable effects include:

- Software development

- Customer service operations

- Content production

- Analytics workflows

- Back-office automation

6-3. Power and infrastructure constraints as potential inflation variables

AI expansion increases electricity demand. Data-center power consumption, cooling costs, and transmission/distribution capex can contribute to cost pressures, affecting inflation and rate sensitivity.

AI may function as a deflationary technology at the application layer while creating inflationary pressures through infrastructure constraints. This tension is relevant for interpreting future rates and industrial policy.

7. Key points underemphasized in typical coverage

7-1. The primary objective is platform intermediation across the AI lifecycle

The strategic goal is to route AI workflows through NVIDIA platforms across input, training, deployment, simulation, validation, and operations. Under this model, competitors cannot win solely via chip-level performance.

7-2. Physical AI’s early stage can be structurally favorable for platform providers

With end winners not yet determined, platform vendors can benefit as multiple robotics firms iterate concurrently, increasing demand for shared infrastructure layers.

7-3. CPU resurgence can reshape AI infrastructure allocation

As agent and RL workloads scale, CPUs, memory, storage, and data-flow management become more central. Semiconductor investment analysis may need broader exposure mapping beyond GPUs.

7-4. Local AI is likely driven by regulation and security, not preference

Relying exclusively on cloud processing for sensitive data faces increasing friction due to:

- Security and compliance requirements

- Data sovereignty constraints

- Latency and continuity requirements

On-device and edge AI may become core pillars rather than secondary trends.

8. Items to monitor

- The scope and pace of NVIDIA’s local AI device strategy

- Evolving CPU vs GPU workload allocation in agent deployments

- Whether synthetic data and simulation progress translates into physical AI commercialization

- The diffusion of digital twins from data centers into industrial sites

- The depth of NVIDIA collaboration with neocloud providers and CSPs

- The balance between AI-driven growth and AI-driven power/infrastructure inflation pressures

9. One-line conclusion

The primary constraint is no longer GPU supply alone; it is the computing architecture that determines where AI runs, how data is partitioned, and how agentic and physical AI are operationalized. NVIDIA is converting this constraint into an addressable market by defining and supplying the reference architecture.

< Summary >

NVIDIA is evolving from a GPU-centric semiconductor vendor into a company shaping AI infrastructure standards. Key themes observed at GTC Taiwan include local AI servers, hybrid data-placement architecture, renewed CPU importance, and platform leverage in physical AI.

Physical AI is not yet at mass-commercialization inflection, but training, validation, and simulation platforms are increasingly standardized around NVIDIA’s ecosystem.

In an AI agent era, investors should assess infrastructure holistically across GPU, CPU, memory, storage, networking, and power. Over the longer term, data-center capex, productivity effects, and power infrastructure demand are likely to remain material drivers for macro conditions, U.S. equities, and semiconductor cycles.

[Related Articles…]

- https://NextGenInsight.net?s=NVIDIA

- https://NextGenInsight.net?s=agent

*Source: [ 내일은 투자왕 – 김단테 ]

– 엔비디아의 가장 큰 병목은 바로 ‘이것’ (대만 엔비디아 GTC 브이로그)

● Markets on Edge, June Shock Ahead

June Market Inflection Point: Why This May Be More Than a Pullback and Could Signal a Structural Shift

The key issue for June is not simply whether markets rise or fall.

The focus is what can change the market’s direction, and how multiple triggers can interact.

This report consolidates four primary drivers: the possibility of a SpaceX mega-IPO, JPY carry-trade unwind risk, US inflation and FOMC policy signals, and semiconductor earnings alongside AI-semiconductor valuation pressure.

It also frames how US equities, Korean equities, FX, policy rates, and semiconductors can transmit risk through a single connected chain.

1. Why June Is Being Treated as a Genuine Inflection Point

Recent global equity strength has been narrow beneath the surface.

Major indices have been supported disproportionately by a small group of mega-cap technology names, particularly AI semiconductor-related stocks, while broader market breadth has been less robust.

In such environments, relatively small shocks can generate outsized volatility.

The current setup resembles a high-valuation regime with elevated sensitivity rather than a broadly supported risk-on market.

June matters because several events converge at once:

- US CPI release and inflation re-pricing

- FOMC and the Fed’s forward rate path reassessment

- BOJ policy shift risk and potential JPY carry-trade unwinds

- Validation of semiconductor earnings expectations

- Liquidity absorption risk from a mega-IPO

In summary, June concentrates liquidity, rates, earnings, and flows into the same window.

2. Trigger #1: A SpaceX Mega-IPO and Potential Market Pressure

Large IPOs are often interpreted as positive, but an IPO of exceptional size can absorb liquidity from listed equities.

If a high-profile growth asset such as SpaceX lists, institutions may fund allocations by trimming existing holdings, potentially creating selling pressure in current market leaders.

2-1. Practical Market Effects of a Mega-IPO

A mega-IPO typically affects markets through three channels:

- Portfolio rebalancing by institutions, increasing profit-taking in existing large caps

- Relative valuation re-rating, potentially compressing AI-related premia

- Liquidity absorption, increasing short-term flow-driven instability

In a market already priced for AI-led growth, the emergence of a new “flagship” growth asset can reduce perceived scarcity value of incumbent growth leaders.

2-2. Implications for Korean Equities

Korean equities are structurally sensitive to US mega-cap technology direction.

If US flows rotate toward a mega-IPO, foreign investor positioning in Korean semiconductor large caps may weaken temporarily.

Given index concentration, declines in major constituents can translate into disproportionate index-level pressure.

3. Trigger #2: JPY Carry-Trade Unwind Risk (Low-Visibility, High-Impact)

The JPY carry trade involves borrowing in low-yielding JPY and allocating into higher-yielding overseas assets.

Japan’s ultra-low-rate stance has functioned as a persistent source of global risk-asset liquidity.

3-1. Why an Unwind Is Risky Now

If the BOJ signals faster normalization or the JPY strengthens sharply, repayment costs rise and investors may liquidate overseas assets to reduce exposure.

This is the carry-trade unwind mechanism.

If it begins, volatility can rise rapidly:

- US equity selling pressure

- Capital outflows from emerging markets

- Upward pressure on USD/KRW

- Increased foreign selling in Korean equities

Although it appears Japan-specific, it functions as a global liquidity tightening event.

3-2. FX Transmission to Korean Assets

Korean assets are highly sensitive to FX.

A rapid rise in USD/KRW increases FX-loss risk for foreign investors and can reinforce equity selling incentives.

Given Korea’s semiconductor-heavy market structure and reliance on foreign flows, FX instability can materially weaken index resilience.

Key monitoring variables in June: JPY direction, BOJ communications, and USD/KRW alongside equity levels.

4. Trigger #3: Inflation and the FOMC (Rate-Cut Expectations Can Reprice)

One reason risk assets have remained supported is the expectation that the Fed will eventually cut rates.

However, recent dynamics suggest inflation may be stickier than expected.

Service inflation, shelter costs, and wage pressures remain relevant, and energy or other supply-side factors could reintroduce upside risk.

4-1. Why CPI Is a Market Anchor

US CPI is not merely a data point; it is a reference for resetting the expected timing and magnitude of rate cuts.

If CPI surprises to the upside, typical market transmission is:

- Rate-cut expectations pushed out

- Treasury yields rise

- Valuation pressure increases on growth equities

- Higher downside risk for the Nasdaq and high-multiple sectors

AI-linked mega caps are particularly sensitive because valuation relies heavily on discounted future cash flows.

4-2. The Key FOMC Focus

Market attention often centers on the policy rate decision itself. The more material inputs are the dot plot and changes in Fed officials’ inflation and growth assessments.

If the Fed emphasizes inflation re-acceleration risks, markets may reprice toward higher-for-longer, with broader implications across global asset prices.

5. Trigger #4: Semiconductor Earnings and the Risk of Over-Embedded Expectations

Semiconductors remain the market’s core leadership segment.

Key companies (e.g., Nvidia, Micron, Samsung Electronics, SK Hynix) have benefited from expectations around AI accelerators, HBM, DDR5, and data-center capex.

The key issue is not “good earnings,” but earnings that exceed already elevated expectations.

5-1. Why Strong Results May Still Be Insufficient

Equities price forward. If AI demand, memory-cycle recovery, and capex expansion are largely priced in, even improving fundamentals can lead to declines if results or guidance fail to clear the market’s implied bar.

Common late-cycle leadership pattern:

- Earnings improve, but

- Guidance underwhelms, or

- Margin expansion is slower than expected, or

- Competitive pressure increases, or

- Profit-taking accelerates

5-2. Sub-Segments to Track: HBM, DRAM, NAND, China Supply

Semiconductors should be assessed by sub-cycle:

- HBM: Central to AI server buildouts; current tight supply could evolve into capacity-driven competition

- DRAM: Core of the recovery; sensitivity rises if pricing momentum slows

- DDR5: Supported by server transitions; adoption pace depends on macro conditions and IT spending

- NAND: Recovering, but profitability improvements may lag DRAM

- Chinese memory suppliers (e.g., CXMT): Medium-term source of supply competition and pricing risk

The structural AI narrative can remain intact while near-term expectations and pricing dynamics drive volatility.

6. Scenario Framework: Four June Pathways That Could Move Markets

6-1. Scenario A: CPI Upside Surprise

If inflation prints above expectations, rate-cut timing is likely to be pushed back.

Treasury yields may rise, pressuring the Nasdaq and high-multiple growth stocks first.

In Korea, profit-taking could concentrate in semiconductor large caps.

6-2. Scenario B: BOJ Shift and JPY Rebound

If Japan normalizes faster than expected, carry-trade unwind concerns increase.

This can propagate broad risk-asset selling, higher USD/KRW, and stronger foreign outflows from Korean equities.

6-3. Scenario C: Semiconductors Beat, Stocks Fall

Even solid earnings can be treated as “sell the news” if expectations were excessive.

If Nvidia and memory names enter a simultaneous de-risking phase, sentiment can deteriorate quickly.

6-4. Scenario D: Liquidity Reallocation Toward a Mega-IPO

A symbolic mega-IPO can shift institutional flows, creating incremental pressure on existing growth leaders.

This is more likely to reduce upside momentum than to be a standalone catalyst for a sustained drawdown.

7. Investor Checklist: Variables Most Likely to Drive Direction

This is not an environment for unconditional optimism or pessimism. The priority is identifying which inputs can shift pricing.

- US CPI and core inflation trend

- FOMC dot plot and any shift toward a more hawkish tone

- BOJ outcomes and JPY direction

- Any rapid USD/KRW increase

- Earnings and guidance from Nvidia, Micron, Samsung Electronics, SK Hynix

- Continuity of AI data-center capex

- Mega-IPO timing and signs of institutional flow reallocation

8. Most Under-Discussed Point: Markets Break Through Linkages, Not Isolated Headlines

Markets typically react more to simultaneous, connected shocks than to a single negative headline.

8-1. Stress Often Starts in the Transmission Chain

Example sequence:

Higher CPI

→ higher US yields

→ valuation compression in growth equities

→ BOJ risk adds carry-unwind concerns

→ FX instability rises

→ foreign flow pressure increases

→ Korean semiconductor leadership comes under concentrated selling

The core June risk is therefore a structural inflection driven by connected macro, flow, and earnings dynamics.

8-2. AI Rally Fatigue as a Risk Amplifier

Markets remain positioned around the AI growth narrative.

As conviction becomes crowded, even small disappointments can generate larger price moves.

This does not imply the AI theme is invalid; it implies that sector fundamentals and equity pricing can diverge over time.

8-3. The Primary Watch Item Is Leadership Rotation, Not a Uniform Crash

If a correction occurs, it may manifest as rotation rather than broad collapse.

Leadership could shift from AI semiconductors toward defensives, stable cash-flow sectors, or policy-linked beneficiaries.

June therefore also functions as a test of next leadership composition, not only index direction.

9. Integrated View: June as the First Major Stress Test Within an Uptrend

June is a period in which optimistic pricing is tested against incoming data, policy signals, and flows.

- A SpaceX IPO can disrupt liquidity allocation

- Carry-trade unwind risk can generate outsized volatility

- Inflation and the FOMC can reprice rate-cut expectations

- Semiconductor earnings can stress high valuations

The market is less exposed to a single shock than to simultaneous verification of elevated expectations.

The critical discipline is tracking which variables confirm through hard data first.

10. One-Line Positioning Lens

June is better framed as a reality check for an over-accelerated market than as a binary “end of the bull market” question.

Key co-indicators: US yields, USD/KRW, semiconductor guidance, and JPY trend.

< Summary >

June markets may be influenced by four variables: a potential SpaceX mega-IPO, JPY carry-trade unwind risk, US inflation and the FOMC, and semiconductor earnings.

The core risk is not any single item, but the combined impact of liquidity tightening and valuation repricing when these drivers activate concurrently.

US and Korean equities are likely to remain sensitive to FX, policy rates, foreign flows, and AI semiconductor expectation levels.

The focus should be less on crash risk and more on leadership rotation and expectation normalization.

[Related Articles…]

- Semiconductor supercycle re-ignition: key checkpoints for Samsung Electronics and SK Hynix

- How to position Korean equities during FX spikes: foreign flows and USD/KRW dynamics (complete guide)

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [풀버전] 6월 증시, 진짜 변곡점이 온다. 증시를 꺾어놓을 ‘4가지 트리거’. 스페이스X 초대형 IPO·엔캐리청산·인플레·반도체 실적 | 클로즈업 | 월간특강 세미나