● Nasdaq-Surge, CPI-Showdown, AI-Memory-Boost

Nasdaq Rebound Signal: In the Current Market, CPI and AI Memory Demand Matter More Than Geopolitical De-escalation

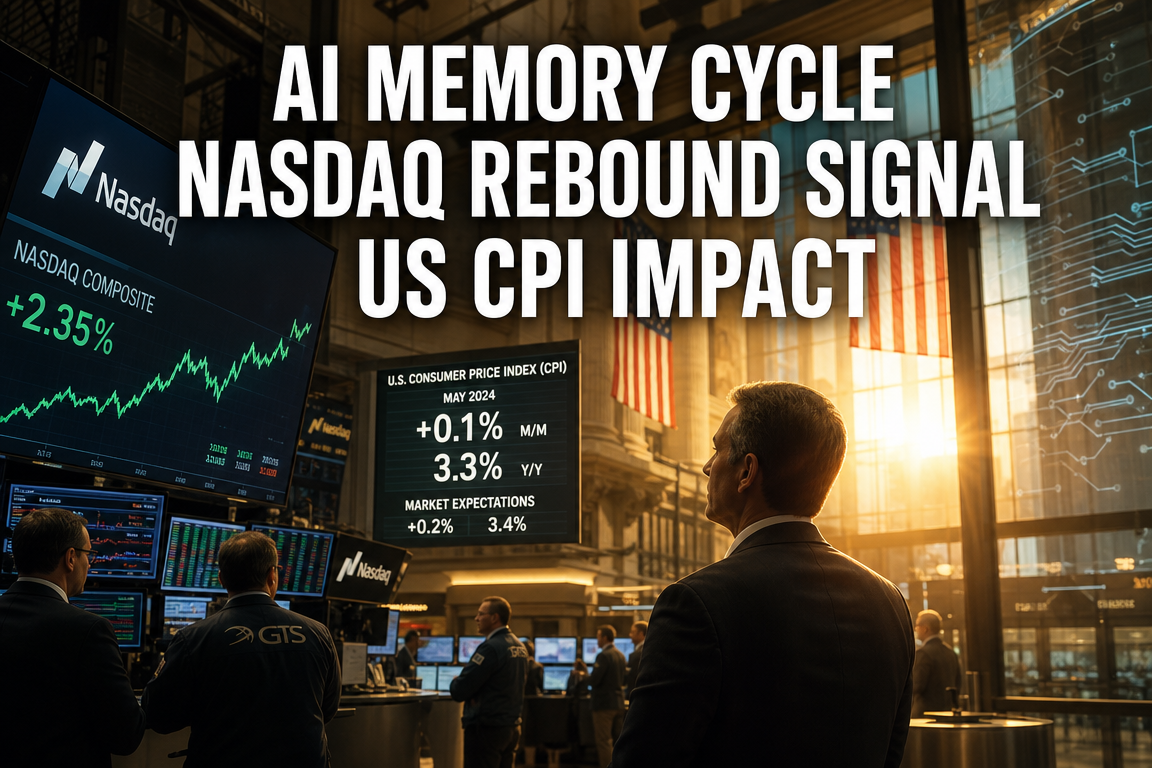

This move should not be viewed as a routine tech bounce. Key questions are why the Nasdaq strengthened abruptly, whether the rebound is a temporary event or an early trend shift, how the Nvidia and Micron narratives affected semiconductor sentiment broadly, and how this week’s US CPI could influence global equities and the KOSPI.

A more material focus than “Israel-Iran tension easing” is the evolving interpretation of memory demand within the AI infrastructure capex cycle.

1. Today’s Nasdaq Rebound: Headline Drivers vs. Core Factors

Geopolitical risk relief as the initial catalyst

News that Israel halted strikes on Iran reduced immediate risk aversion. In geopolitical escalations, crude oil, Treasury yields, and safe-haven demand typically react first; this time, risk appetite improved, supporting growth equities led by the Nasdaq.

US mega-cap technology shares, given elevated valuations, tend to respond strongly to reductions in uncertainty. Geopolitical risk relief was the first-order trigger.

“For now” warrants caution

The language implying a temporary halt suggests the risk can re-emerge. A renewed escalation could lift oil prices, revive inflation concerns, and raise rate sensitivity, pressuring risk assets.

While geopolitics can drive short-term price action, medium-term direction is primarily determined by inflation, rates, and earnings. CPI is the next critical gate for assessing durability.

2. Nvidia Memory Narrative: A Misinterpretation Has Been Partly Resolved

Why “Nvidia uses less memory” mattered

Market commentary suggested Nvidia could cut memory usage materially, raising concerns that HBM and DRAM demand tied to AI systems could weaken. This was not a component-level issue; AI server expansion remains the central driver of semiconductor investment, with GPU-memory configurations at the core. Any perceived reduction in memory intensity directly affects valuation frameworks for memory suppliers.

The prevailing conclusion: reallocation rather than demand destruction

Recent deeper analyses increasingly frame the issue as system-level configuration changes, not a decline in total memory consumption. The implication is a shift in where memory attaches within next-generation architectures rather than a collapse in demand.

This distinction is material: demand destruction would imply a cyclical peak; reallocation is consistent with ongoing system optimization.

Vera CPU-related allocation as a monitoring point

Interpretations that memory is being reallocated toward the Vera CPU support a broader thesis: data centers are moving from GPU-only scaling to integrated optimization across CPU, networking, memory, and power efficiency.

AI infrastructure competition is increasingly platform-based, emphasizing total system throughput, energy efficiency, connectivity, and bottleneck reduction.

3. Micron Target Price Upgrades: Why the Market Reacted Immediately

Micron as a barometer for AI memory demand

Additional upgrades to Micron are best read as improving memory-cycle interpretation rather than a single-stock event. Within global equities, Micron functions as a high-frequency proxy for whether AI buildouts are translating into realized memory pricing and revenue momentum.

Reinforcing expectations for memory-cycle recovery

Recent market leadership has been uneven: GPUs were strong, while the memory follow-through was debated. A constructive stance on Micron reduces concerns that memory will lag AI compute deployment. If high-value AI server memory demand remains firm, earnings normalization for memory vendors could accelerate.

Direct relevance for the KOSPI

Strength in Nvidia and Micron typically improves sentiment toward Korean memory exporters. This can translate into improved positioning toward Samsung Electronics and SK Hynix, supporting the pathway from Nasdaq strength to a semiconductor-led KOSPI move. The key framing is not “US equities rose,” but “semiconductor cycle expectations improved.”

4. This Week’s Primary Inflection: US CPI

Markets revert to inflation and rates

The US CPI release on Wednesday is the week’s central event. Even with improved risk sentiment and stronger semiconductor positioning, an upside CPI surprise would pressure rate-cut expectations.

Technology equities, which discount more distant cash flows, are highly sensitive to rate expectations. Sustained Nasdaq upside likely requires supportive CPI and stable yields.

Scenario if CPI is benign

If CPI prints near expectations or shows continued disinflation, risk appetite may remain constructive. Large-cap technology, AI, and semiconductors could retain momentum. Stabilizing Treasury yields would support risk assets, and any moderation in USD strength could improve EM flows, potentially benefiting KOSPI foreign inflows.

Scenario if CPI is hot

If CPI is above expectations, the relief rally may reverse quickly. If accompanied by renewed oil strength or renewed Middle East tensions, inflation risks could reprice upward. Rate-cut expectations would be pushed out, and profit-taking would likely concentrate first in higher-valuation technology.

The market is effectively testing whether inflation conditions permit the current rebound.

5. News-Style Key Takeaways: What to Track Now

Global equities

- Reports of a halt in Israel’s strikes on Iran reduced near-term geopolitical risk.

- Reduced safe-haven demand supported a Nasdaq-led rebound in growth equities.

- The Middle East remains a headline risk; durability is uncertain.

Semiconductors and AI

- Concerns about reduced Nvidia memory usage are increasingly viewed as configuration reallocation rather than demand deterioration.

- The focus has shifted from collapsing total memory demand to changing system design and allocation.

- Micron target price upgrades have supported expectations for improving AI memory fundamentals.

- This is likely supportive for Korean semiconductor sentiment.

Macro

- The key weekly event is US CPI.

- A stable CPI would preserve rate-cut expectations and could extend the technology-led rally.

- A hotter CPI would likely destabilize the Nasdaq rebound.

6. Underemphasized Point in Common Media: Not “Less Memory,” but AI Infrastructure Upgrading

Many narratives treat Nvidia, Micron, and the Nasdaq as separate topics. The more relevant interpretation is that they reflect a single flow: the AI industry is shifting from standalone chip performance to end-to-end system optimization, requiring more precise analysis of memory dynamics.

This rebound is less about “semiconductor stocks rose” and more about “the AI infrastructure investment cycle has not materially rolled over.”

Geopolitics may dominate near-term volatility, CPI may govern the next move, but medium-term direction will likely be driven by the persistence of AI-related capex and its translation into realized earnings.

Key implications for investors focused on Korea

For Korea-based positioning, the priority is whether the rebound strengthens export and earnings expectations for semiconductors. If CPI is benign and AI memory demand remains firm, KOSPI leadership may skew toward semiconductors. If geopolitical risks re-escalate or CPI surprises to the upside, foreign flows could reverse quickly.

7. Forward Calendar and Monitoring Framework

Near-term checklist

- US CPI results

- US Treasury yield movements

- Re-escalation risk in Middle East headlines

- Additional Nvidia and Micron research updates

- Foreign flow trends and positioning in Korean semiconductor equities

Medium-term checklist

- Continuity of AI data center capex growth

- Sustainability of memory pricing uptrend

- Direction of rate-cut expectations and the US dollar

- Whether semiconductor recovery leads to upward earnings revisions

8. One-sentence conclusion

Geopolitical relief initiated the Nasdaq rebound, CPI will determine near-term follow-through, and the core signal is that AI-driven semiconductor demand, particularly memory, remains resilient.

< Summary >

- The initial driver of the Nasdaq rebound was easing Israel-Iran tensions.

- Nvidia-related “memory reduction” concerns are increasingly interpreted as reallocation rather than weakening end demand.

- Micron target price upgrades reinforced expectations for improving AI memory fundamentals.

- US CPI is the central variable this week; the print may determine whether the technology rally extends.

- Korea’s equity outlook could improve on semiconductor leadership, but geopolitical and inflation risks remain key constraints.

[Related Posts…]

- Nasdaq rebound dynamics and key checkpoints for US equities: https://NextGenInsight.net?s=Nasdaq

- Semiconductor cycle recovery and AI memory investment strategy summary: https://NextGenInsight.net?s=Semiconductors

*Source: [ 내일은 투자왕 – 김단테 ]

– 나스닥 대반격의 시작 (6월 9일)

● AI-Infrastructure-Surge

The Primary Beneficiaries Highlighted by Both Jensen Huang and Elon Musk: Key Takeaways for an Unstable Market

The current correction is less a routine drawdown and more a repricing phase reflecting how U.S. equities, the Nasdaq, semiconductors, AI infrastructure, and rate-cut expectations are being reorganized.

This report summarizes: (i) the drivers behind the recent market dislocation, (ii) why liquidity absorption is being priced more aggressively than further tightening, (iii) why Google’s large-scale financing is a near-term headwind for mega-cap equities but supportive for AI infrastructure suppliers, and (iv) why both Jensen Huang and Elon Musk identify memory as the critical bottleneck.

Rather than focusing on headline volatility, the analysis isolates the underlying mechanism of the correction, identifies segments that declined alongside the broader market but may recover earlier, and outlines priority considerations for 2H positioning.

1. The Recent U.S. Equity Sell-Off: The Primary Catalyst Was Not the Headline Narrative

U.S. equities sold off sharply late in the week.

The Nasdaq declined by approximately 4% on a weekly basis, and semiconductor-related indices fell by a similar magnitude, pressuring year-to-date market leaders.

While tighter policy risk, inflation concerns, and weaker rate-cut expectations were cited, the more influential driver was liquidity absorption.

In practical terms, with rates elevated and system liquidity constrained, a cluster of large IPOs and major financing events increases the risk of capital being diverted from public markets.

2. The Core Issue: Not Additional Tightening, but “Capital Sink” Risk

Market sensitivity has been driven by three factors:

- Renewed tightening concerns

- Liquidity absorption risk from large IPOs and equity issuance

- Profit-taking narratives, including calls for an early peak in the memory cycle

The second factor has carried the greatest weight.

With a potential SpaceX listing, a reported Anthropic listing push, and Google’s large-scale equity financing, markets have shifted from “positive growth news” to “can available capital absorb this supply?”

The correction appears more consistent with funding-cycle pressure than with deteriorating operating fundamentals.

3. Google’s Large Equity Financing: Headwind for Mega-Caps, Tailwind for AI Infrastructure

One of the most notable developments was Google’s announcement of large-scale financing to expand AI investment, described as among the largest equity issuance efforts in U.S. corporate history, with indications that demand expanded the size.

The key implications are:

- Even cash-rich platforms are not relying solely on internal cash to fund AI capex

- Other mega-cap peers may pursue similar financing structures

This is a near-term negative for mega-cap equities due to dilution effects and the signal of higher forward investment burden.

However, the more material question is the destination of the capital.

Expected beneficiaries include AI infrastructure supply chains: data centers, servers, memory, GPUs, CPUs, networking, power infrastructure, and optical interconnect.

Accordingly, the same event can be a headwind for platform equity multiples while supporting order visibility for infrastructure vendors.

4. Structural Shift: Mega-Caps Are Evolving from High-Cash-Return Platforms into Capex-Intensive Operators

Over the prior decade, large technology platforms generated substantial free cash flow and emphasized shareholder returns, including buybacks.

The current phase implies a shift toward AI investment levels that may exceed internally generated cash flow.

This changes the equity framework:

- Previously: margins, advertising trends, and cloud growth were primary drivers

- Now: speed and scale of AI infrastructure acquisition increasingly differentiate outcomes

Competition is expanding from software to supply-chain access across hardware, power, data centers, and semiconductors.

Near-term, this can pressure costs and valuation; medium-term, it reinforces demand signals across semiconductors and AI infrastructure.

5. Shared Signal from Jensen Huang and Elon Musk: Memory Is the Binding Constraint

A key datapoint is the convergence in messaging from Jensen Huang and Elon Musk, both of whom influence the AI ecosystem and have visibility into immediate bottlenecks.

Both identified memory as the core constraint.

5-1. Musk: Memory Is a Binding Constraint for Data-Center-Scale AI Expansion

In investor communications related to a potential SpaceX listing, Musk emphasized memory as the principal limitation.

He noted that high-performance memory supply in the U.S. is structurally insufficient and that future domestic capacity may still be inadequate versus projected demand.

Operationally, AI data centers cannot scale on GPU availability alone: high-bandwidth memory and high-performance storage are required to translate theoretical compute into realized throughput.

5-2. Huang: Supply Must Expand Materially

At Computex, Jensen Huang reiterated the importance of the memory supply chain.

Ongoing engagement with SK Hynix has been interpreted as evidence that HBM supply constraints remain a central bottleneck.

Markets increasingly recognize that Nvidia’s shipment capacity can be constrained by memory availability:

- Strong GPU demand is insufficient if memory supply limits server shipments

- Shipment delays slow AI server deployments and capacity expansion

Memory is therefore not a peripheral component but a gating factor that determines effective production volume across the AI cycle.

6. Why Memory Equities Sold Off, and Why They Remain a Priority Watchlist

Memory-linked equities declined materially during the correction.

Micron, SanDisk, and memory-focused ETFs, among year-to-date leaders, pulled back approximately 15–20% from recent highs.

The dominant bearish narrative is a cycle peak.

Based on currently available information, price action appears more consistent with profit-taking after strong performance than with definitive evidence of demand rollover.

If mega-cap AI capex continues to expand and key industry leaders continue to cite supply shortages, memory may continue to be a primary area for re-risking on weakness.

The decision framework is:

- Is AI investment structurally slowing?

- Or is the drawdown primarily liquidity-driven?

Current signals are more consistent with the latter.

7. The AI Agent Theme: CPUs May Become the Next Leadership Segment

At Computex, Jensen Huang repeatedly emphasized AI agents.

This is relevant because market positioning remains heavily concentrated in GPUs.

If AI agents scale, always-on compute becomes embedded across devices and workflows, which can increase CPU relevance.

Intel, AMD, Arm, and Qualcomm have also emphasized the AI agent framework, consistent with a broader compute expansion thesis.

7-1. Why CPUs May Re-Accelerate in Importance

AI agents are not single-turn chat interfaces; they continuously ingest data, schedule tasks, connect applications and devices, and execute multi-step workflows.

This increases the need for system-level orchestration, distributed processing, and local inference where CPUs remain critical.

As a result, broader adoption of AI agents may support simultaneous growth across GPUs, CPUs, and edge-device semiconductors.

7-2. Common Messaging from Qualcomm, Arm, and Intel

While phrasing differs, the core points converge:

- AI agents operate continuously

- Billions of devices may enter an upgrade cycle

- Deployment expands from smartphones and PCs to vehicles, robotics, and edge systems

This implies that semiconductor allocation frameworks may need to expand beyond server AI accelerators to device-wide AI enablement.

8. Optical Interconnect: Underfollowed but Potentially Central to the Next Wave

While memory and CPUs dominate attention, optical connectivity is also critical within the AI infrastructure cycle.

As data centers scale, the limiting factor can shift from raw compute to the speed and efficiency of chip-to-chip and server-to-server communication.

This has renewed attention on companies such as Marvell.

8-1. Why Connectivity Is Becoming the Constraint

Next-generation AI data centers compete on system-scale performance.

Large clusters—tens of thousands to hundreds of thousands of chips—must function as a single distributed computer.

In this architecture, bottlenecks can migrate from compute to interconnect bandwidth and latency, increasing demand for optical solutions relative to copper-based alternatives.

8-2. Why Marvell Is Being Re-Rated

Marvell is viewed as having exposure to custom AI silicon, networking, and optical interconnect.

Incremental attention has been supported by reported Nvidia interest, alignment with hyperscaler in-house silicon roadmaps (including Amazon), and index-related factors.

Volatility remains elevated, but the company is frequently cited as a potential medium-term leader within AI infrastructure.

A common framing is:

- AI infrastructure phase 1: GPUs

- Phase 2: memory

- Next: connectivity and networking

9. June Outlook: Elevated Volatility Risk

June includes multiple potential volatility catalysts:

- Inflation data releases

- FOMC outcomes and Fed communications

- Potential SpaceX listing developments

- Broader spillover of large financing events

In this regime, even constructive developments can be priced as risk events due to capital-demand sensitivity.

Near-term, the market may remain range-bound with uneven price action rather than a linear rally.

However, the move does not necessarily indicate an end to the AI-led cycle, given that the key assumption—continued mega-cap AI investment—has not yet reversed.

10. Priority Investment Considerations During the Correction

10-1. Mega-Caps: Favor Selectivity

Mega-caps remain central to AI competition, but financing and cost pressures may be reflected first in their equities.

Performance may increasingly differentiate based on demonstrated investment efficiency rather than broad-based multiple expansion.

10-2. AI Infrastructure: Potentially Higher Conviction on Weakness

Segments directly linked to hyperscaler spending—memory, semiconductors, CPUs, optical interconnect, servers, data centers, and power infrastructure—may be interpreted as benefiting from structurally supported demand, despite near-term drawdowns.

10-3. Memory Remains the Central Pivot

The fact that both Jensen Huang and Elon Musk identify memory shortages as the key bottleneck is a high-signal indicator.

In environments where physical constraints dominate narratives, bottleneck identification can be more actionable than thematic storytelling; current evidence points to memory as the primary gating factor.

10-4. AI Agents: Potential Device Upgrade Cycle and Broader Semiconductor Demand

AI agents may expand upgrade demand across PCs, smartphones, vehicles, robotics, and edge devices.

This suggests a multi-year hardware re-investment theme rather than a short-lived tactical trade.

11. Underappreciated Core Point

The relevant question is not only why the market declined, but what strengthened during the drawdown.

While tightening risk, inflation concerns, and IPO supply are widely discussed, the more structural changes are:

- Mega-caps are funding AI expansion with external capital, not reducing investment

- AI competition is shifting from software to physical infrastructure acquisition

- Supply-chain providers—memory, CPUs, and optical interconnect—may be direct beneficiaries of this capex cycle

Accordingly, the correction is more consistent with near-term funding and liquidity constraints than with fading AI demand.

This distinction helps separate assets to avoid from those that warrant continued tracking and selective accumulation.

12. One-Line Conclusion

The market is not declining primarily due to fear, but due to the scale and simultaneity of AI-related capital movements; near-term volatility may persist, while medium-term AI infrastructure demand signals are becoming clearer.

Memory, CPUs, and optical interconnect remain key segments that may regain attention earlier as conditions stabilize.

< Summary >

The recent U.S. equity correction is being driven less by tightening itself and more by liquidity absorption risk from large-scale capital events such as a potential SpaceX listing and Google’s equity financing.

Google’s financing is a headwind for mega-cap equities but can be interpreted as structurally supportive for AI infrastructure categories where the capital is deployed, including memory, semiconductors, data centers, and optical interconnect.

The convergence of Jensen Huang and Elon Musk on memory shortages as the primary bottleneck is a high-signal datapoint.

AI agent adoption may broaden demand beyond GPUs to CPUs and upgrade cycles across smart devices, vehicles, and robotics.

June volatility may rise due to inflation, the FOMC, and IPO/financing events; the current setup appears more consistent with a liquidity-driven pause than a confirmed end to the AI capex cycle.

[Related Posts…]

- AI Infrastructure Capex Expansion: Key Semiconductor Beneficiaries Reassessed for 2H

- Memory Cycle Re-Acceleration Potential: Key Monitoring Framework

*Source: [ 소수몽키 ]

– 젠슨 황과 머스크가 증시 살린다? 동시에 찍어준 주인공 주식들