● Dollar Soars, Won Sinks, AI Chip Surge

Dollar Index Breaks Above 100; USD/KRW at 1,538: Key Takeaways for U.S. Equities and AI Semiconductor Strategy in 2H 2026

This is not a one-day rebound. The market is better understood by linking the Dollar Index move above 100, USD/KRW at 1,538, the sharp decline in oil, easing Iran-related geopolitical risk, and Citigroup’s expectation for an October rate cut. Additional drivers include renewed attention on Intel, Apple–NVIDIA–U.S. foundry reconfiguration themes, and why the AI semiconductor rally may not be over.

Headline risk suggests renewed tightening fears; however, market pricing is increasingly weighting AI-driven productivity gains and a policy-led semiconductor investment cycle.

This note covers U.S. equity performance, the effective policy signal from the Federal Reserve, FX implications, reasons for semiconductor strength, and an under-discussed angle: potential benefits to Wall Street capital from Middle East reconstruction financing.

1. Market Snapshot: Why U.S. Equities Rose

U.S. equities advanced broadly: Nasdaq up around 1%, S&P 500 higher, with the Dow and Russell also gaining. The underlying move was selective, led by semiconductors and AI infrastructure.

- Broadcom strength

- Micron surge

- Intel sharp rally

- AMD and Qualcomm higher

- Lam Research, SanDisk, Vertiv and other AI infrastructure chain strength

The market is not uniformly strong across sectors; structural leadership remains concentrated in AI and semiconductors. This matters for portfolio construction, as it clarifies where the current equity impulse is concentrated.

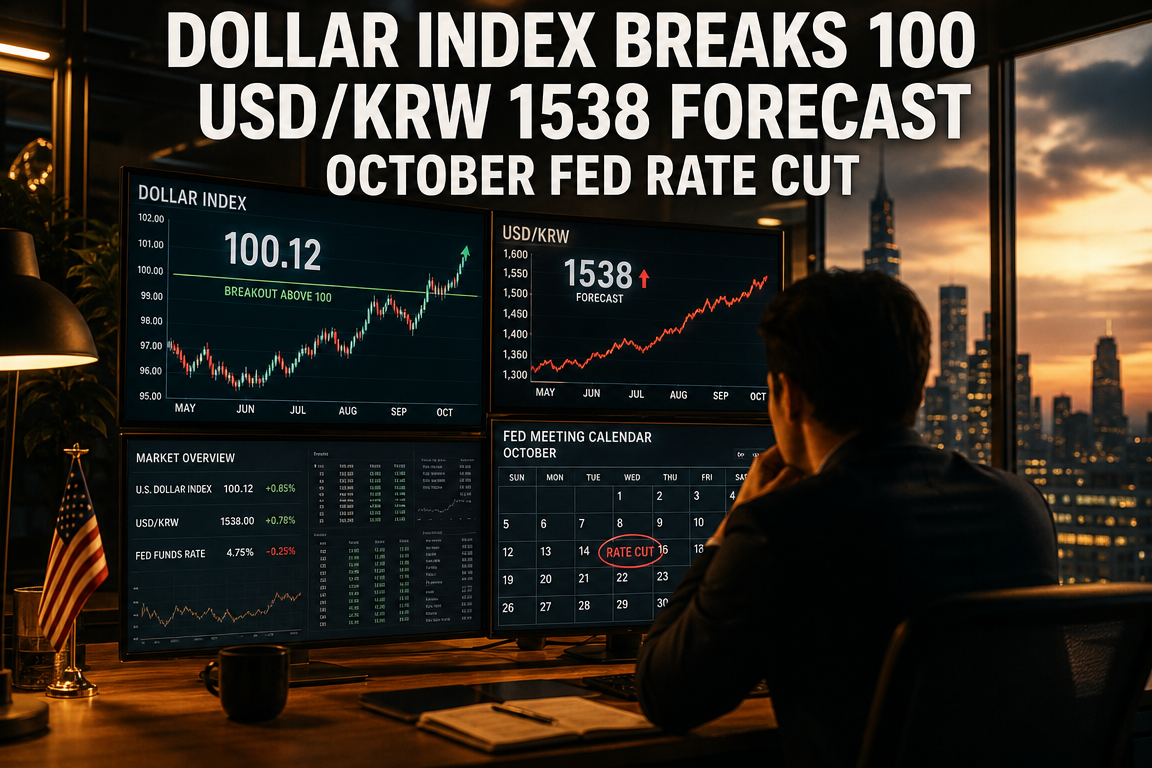

2. Dollar Index Above 100 and USD/KRW at 1,538: Why the Move Is So Strong

For Korea-based investors, FX is as critical as U.S. equity direction. The Dollar Index has moved above 100 and USD/KRW reached 1,538, consistent with a persistent strong-dollar regime rather than a single-news spike.

2-1. Drivers of the Strong Dollar

- Residual risk of further Fed tightening

- Relative U.S. growth outperformance

- Broad weakness across Asian currencies

- Reaffirmed safe-haven demand following geopolitical stress

- Renewed focus on structural vulnerabilities in KRW

A key point is that KRW did not recover meaningfully even after risk-off pressure eased and oil declined, implying the FX market is still positioned defensively even as equities reprice toward risk-on.

2-2. Implications for Korea-Based Investors

USD/KRW in the 1,500s is a headwind for Korean assets.

- FX translation can support returns on overseas equity exposure

- Domestic equities face additional foreign flow sensitivity

- Import cost pressure may limit the pace of disinflation

- The Bank of Korea’s policy trade-offs become more complex

A prolonged strong-dollar environment tends to raise volatility in emerging-market assets, affecting overall asset allocation into 2H 2026.

3. Oil Selloff and the Iran Variable: Why Markets De-Risked

WTI and Brent declined sharply, signaling easing stress in energy markets. Markets began to price reduced U.S.–Iran tension, lower perceived risk around the Strait of Hormuz, and improved supply continuity.

3-1. Why Lower Oil Matters

- Reduced energy-driven inflation pressure

- Weaker justification for additional Fed tightening

- Lower valuation pressure on growth equities via rates expectations

- Relief on household and corporate cost structures

In a period where AI investment remains active, a decline in oil is particularly supportive for tech and semiconductors.

3-2. Why This Should Not Be Treated as a Final Settlement

The current framework appears closer to an MOU than a definitive end state. Over the next ~60 days, negotiations on nuclear material handling, sanctions scope, and implementation sequencing may generate renewed volatility. Oil could reprice accordingly.

4. Is the Fed Moving Toward More Hikes? Why Interpretation Is Split

Post-FOMC market action has reflected renewed sensitivity to additional hikes, driven by dot-plot signaling and an emphasis on inflation control. The more investable signal, however, is the Chair’s emphasis and policy function rather than the dot plot alone.

4-1. Key Points Under a Kevin Warsh Framework

Based on the overall message, Chair Kevin Warsh appears less reliant on dot-plot forward guidance and more focused on productivity, technology investment, and structural reform.

- Dot plots may not function as binding guidance

- Productivity gains from AI could absorb inflation pressure

- Prolonged restrictive rates could impair AI investment and corporate innovation

- Policy decisions may not be driven solely by traditional CPI interpretation

This raises the possibility that policy could evolve more dovishly than headline “hawkishness” suggests, depending on growth and productivity dynamics.

4-2. Why Citigroup Still Sees an October Cut

Citigroup continues to allow for rate cuts in October and December, and again in January of the following year. This implies a delayed, not abandoned, easing path. Supporting factors include election-cycle constraints, growth moderation risk, oil-driven disinflation, and the desire to sustain technology investment momentum.

The market appears to be in a transition regime where “hike risk” and “cut potential” are being priced simultaneously.

5. Why Semiconductors Remain Strong: Not a Simple Theme Trade

The current semiconductor strength reflects three concurrent forces.

5-1. First, the AI Capex Cycle Has Not Clearly Turned Down

Big Tech capex trends do not show clear contraction. Spend is expanding into AI agents, data center upgrades, memory, and power infrastructure.

- Sustained GPU demand

- Expanding HBM and memory demand

- Rising power and cooling infrastructure needs

- Agentic AI adoption supporting renewed CPU relevance

5-2. Second, Lower Oil Supports Growth Valuations

Energy price stability reduces inflation pressure and can ease long-end rate pressure, supporting growth and semiconductor valuations. Where earnings delivery remains strong, premium multiples can persist.

5-3. Third, Policy Is Driving Supply-Chain Reconfiguration

Intel’s rally is tied less to near-term earnings expectations and more to policy. Repeated political emphasis on Intel suggests framing the company as an industrial security asset within a domestic semiconductor agenda.

6. Renewed Focus on Intel: Why the Market Reacted

Political commentary reiterated the possibility of Apple using Intel’s foundry capacity, alongside references involving NVIDIA and Elon Musk. This functions as an extension of U.S. semiconductor reshoring and supply-chain localization.

6-1. Why Intel Is Back in Focus

- Symbolic importance of U.S.-based manufacturing expansion

- Strategic need to reduce reliance on TSMC

- CPU relevance in the AI era

- Expectations around the 18A node

- Potential for policy support and subsidies

Market framing is shifting from purely technology-driven assessment to one incorporating policy and supply-chain strategy, allowing for a “strategic asset” re-rating if rhetoric converts into tangible orders.

7. AI Semiconductor Rally: How Far the Chain Extends

Market leadership is broadening beyond GPUs into memory, CPUs, storage, power equipment, and cooling. This expansion materially changes how the AI value chain should be evaluated.

7-1. Current Strong Areas

- Micron: memory cycle aligned with AI-driven demand

- Broadcom: AI networking and custom silicon exposure

- AMD: dual exposure to CPUs and AI accelerators

- Intel: policy tailwinds and CPU re-rating

- Lam Research, SanDisk, Vertiv: equipment, storage, and power infrastructure exposure

7-2. Areas Requiring Caution

Not all AI-linked equities are equally resilient. Names with valuation far ahead of earnings can exhibit sharp drawdowns.

- Earnings-backed semiconductor exposure remains comparatively resilient

- Loss-making or low-visibility revenue profiles carry higher downside risk

- Leveraged single-name ETFs and options positioning can amplify volatility

The AI rally may persist, but security selection has become more complex.

8. “Meme-Stock” Debate: How to Treat It

Some commentary argues the semiconductor and select tech moves resemble meme-like excess. While pockets of overheating may exist, broad-brush classification is not analytically precise.

8-1. Why Overheating Concerns Appear

- Increased call buying

- Potential gamma-squeeze dynamics

- Flow distortions from single-stock leveraged ETFs

- Multiple names with rapid, short-window price appreciation

8-2. Why This Differs From Classic Meme Episodes

In classic meme cases, price action detached from fundamentals. In the current semiconductor move, a significant portion is supported by earnings and observable demand. The key is separating fundamental beneficiaries from names driven primarily by expectations.

9. Under-Discussed Catalyst: Middle East Reconstruction and Potential Wall Street Upside

Beyond near-term oil relief, a critical angle is who benefits during reconstruction. If a USD 300 billion reconstruction fund becomes actionable, beneficiaries could include large investment banks and U.S. capital via bond issuance, project finance, advisory mandates, and energy infrastructure rebuilding. This reframes geopolitical de-escalation as a potential transition from military risk to financial deal flow.

10. Key Investor Checklist

10-1. Macro Checklist

- Whether the Dollar Index holds above 100

- Whether USD/KRW remains anchored in the 1,500s

- Whether oil stabilizes in the 70s

- Whether expectations for an October Fed cut remain intact

10-2. Equity Market Checklist

- Whether semiconductors retain leadership in U.S. equities

- Whether Intel policy narrative converts into orders/contracts

- Whether leadership expands across memory, CPUs, and power infrastructure

- Whether signals emerge of AI capex deceleration

10-3. Korea-Based Investor Checklist

- Rebalance domestic vs. overseas equity exposure under FX stress

- Emphasize valuation discipline within semiconductors

- Avoid chasing high-multiple thematic names without earnings support

- Understand leverage mechanics before using leveraged ETFs

11. One-Sentence Summary

The market is balancing strong-dollar and rate uncertainty against stronger tailwinds from lower oil, AI-driven productivity expectations, and policy-led semiconductor supply-chain reconfiguration. The core approach for 2H 2026 is to accept the FX regime, keep rate-cut optionality, and focus on AI semiconductor exposures with both earnings support and policy tailwinds, while avoiding indiscriminate thematic chasing.

Most Material Points Often Under-Weighted in Standard Coverage

- The primary beneficiaries of Iran-related de-escalation may include Wall Street capital via reconstruction finance, not only near-term oil-sensitive equities.

- Despite hawkish optics, the Fed could pivot faster if AI-driven productivity becomes a policy justification for easing.

- Political emphasis on Intel should be interpreted as a semiconductor supply-chain and industrial security signal, not a simple single-stock promotion.

- USD/KRW at 1,538 is a structural signal of dollar dominance, with direct implications for Korean asset pricing and flows.

< Summary >

A Dollar Index move above 100 and USD/KRW at 1,538 indicate that the strong-dollar structure remains intact. Lower oil and easing Iran risk reduce inflation pressure and are supportive for U.S. equities and semiconductors. Citigroup continues to expect an October rate cut, and the Fed may retain more easing optionality than headline messaging implies. Political attention on Intel should be read as a policy signal tied to U.S. foundry and AI semiconductor supply-chain restructuring. The central question is whether AI semiconductors and U.S. equity leadership persist under a strong-dollar regime; security selection should prioritize companies where earnings and policy support align.

[Related Articles…]

- Dollar Dynamics and Global Asset Allocation

- Semiconductor Supply-Chain Reshoring and U.S. Foundry Strategy

*Source: [ Maeil Business Newspaper ]

– 달러 인덱스 100 돌파, 환율 1538원까지 올라ㅣ시티, 여전히 금리인하(올해 10월) 베팅ㅣ트럼프 “애플, 인텔 파운드리 쓸 것”ㅣ홍키자의 매일뉴욕