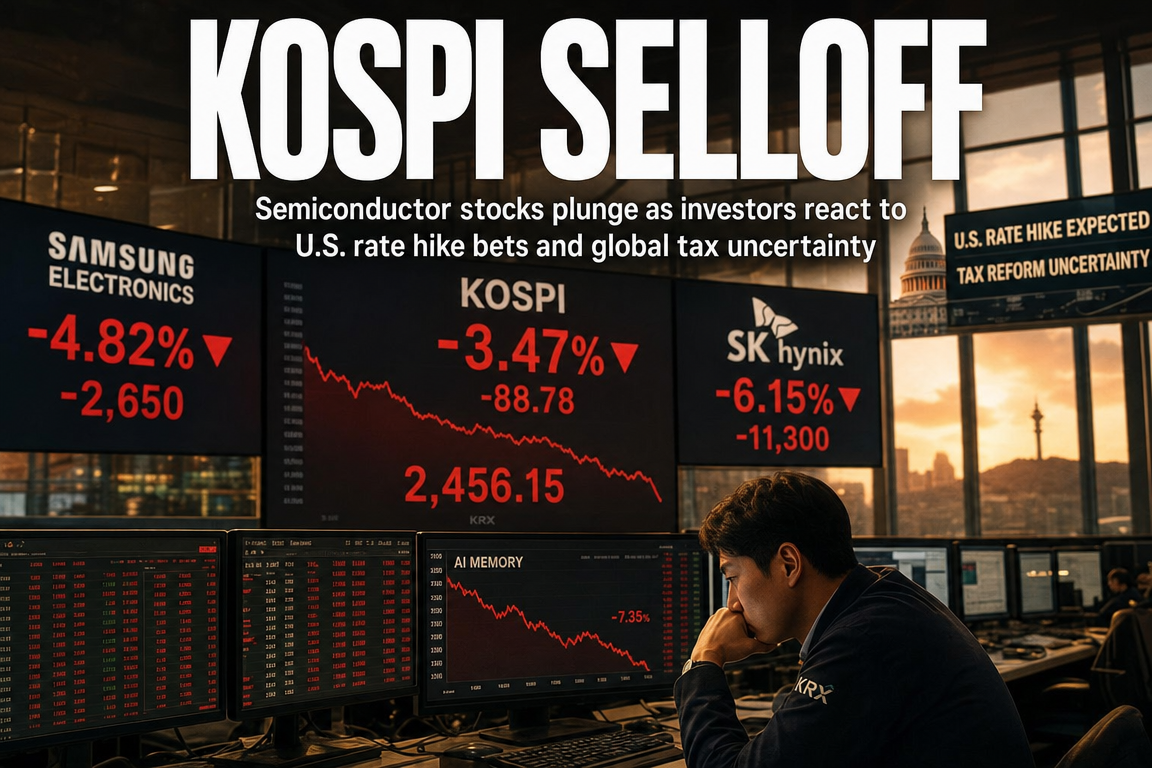

● Market Meltdown, Samsung, SK Hynix Slammed, Three Shock Drivers

KOSPI, Samsung Electronics, and SK Hynix Sell-Off: Three Key Drivers Behind Today’s Market Breakdown and the Variables to Monitor

Today’s market action is not defined solely by the KOSPI decline. The central issue is why bellwether semiconductor large caps—Samsung Electronics and SK Hynix—sold off in tandem, and how US equities, interest-rate expectations, and tax-related policy uncertainty transmitted into Korean assets.

This report consolidates:

- The spillover from the Nasdaq decline into Korean semiconductor equities

- How shifting US rate expectations affected foreign flows and risk appetite

- Why discussions on taxation of unrealized equity gains amplified downside risk

- Core points often omitted in headline coverage

What was the core takeaway from today’s KOSPI sell-off?

The decline reflected a combined shock rather than a single idiosyncratic catalyst: global equity risk-off sentiment, interest-rate risk, and policy uncertainty occurred simultaneously. Given their index weight, weakness in Samsung Electronics and SK Hynix mechanically and psychologically tightened overall KOSPI conditions.

In practical terms:

- US mega-cap weakness reduced confidence in the semiconductor demand narrative

- Renewed rate-hike risk increased valuation pressure on growth-sensitive assets

- Tax-policy uncertainty added a risk premium, reinforcing defensive positioning

1. Why did deteriorating Nasdaq sentiment hit Samsung Electronics and SK Hynix?

US mega-cap risk-off transmits directly into Korean semiconductors

Samsung Electronics and SK Hynix function as global AI and memory-cycle exposures as much as they are domestic blue chips. Their equity performance is closely linked to:

- US mega-cap technology investment sentiment

- Data-center and AI server deployment trends

- Cloud providers’ capital-expenditure plans

US hyperscalers remain key end-demand drivers for advanced memory.

SpaceX issuance headlines and broader funding-risk sentiment

The market sensitivity centered on large-growth-company financing signals. While capital raising can be interpreted as expansionary in strong regimes, in a high-rate environment it can also be read as:

- higher cash-flow pressure,

- delayed payback on investment,

- increased capital costs.

This interpretation compresses growth valuations, with spillovers from the Nasdaq into Korean semiconductor large caps.

Why reports of AI talent outflows at Google were treated as negative

In AI-driven competition, human capital is increasingly treated as a leading indicator of competitiveness. Talent attrition at a major platform is often interpreted not as an HR issue but as a potential weakening of AI leadership. This can:

- undermine mega-cap AI investment confidence,

- raise questions about the pace of AI infrastructure scaling,

- soften expectations for HBM, server DRAM, and NAND demand.

Because SK Hynix and Samsung Electronics have been priced as “AI beneficiaries,” they tend to exhibit higher downside beta when AI expectations moderate.

News-style summary

- Nasdaq weakness directly pressured risk appetite toward Korean semiconductor large caps.

- Mega-cap funding concerns reinforced skepticism toward growth narratives.

- AI talent headlines were interpreted as potential competitiveness risk.

- Samsung Electronics and SK Hynix fell on perceived AI capex and demand uncertainty.

2. Renewed US rate-hike risk: why it was particularly damaging for the KOSPI

Why Bank of America commentary can move markets

Beyond official Federal Reserve communication, changes in guidance from major investment banks can reprice expectations. When a high-profile institution reiterates the possibility of additional hikes, the market may infer that the tightening cycle is not conclusively over.

At this stage, the key risk is less an immediate hike and more the repricing of “imminent easing” assumptions, which tends to compress equity multiples.

Why higher rates hit semiconductors and growth exposures first

Higher rates reduce the present value of future earnings, which disproportionately impacts growth and long-duration assets. While Samsung Electronics and SK Hynix are industrial in classification, they have increasingly traded as growth-sensitive AI and cycle beneficiaries, making them more responsive to rate-driven valuation resets.

Why foreign flows and FX must be monitored

US rate repricing matters in Korea primarily via cross-border allocation:

- Higher-for-longer US yields raise the relative attractiveness of USD assets.

- EM allocations can weaken, pressuring KRW.

- Foreign selling can intensify in KOSPI-heavy names with high foreign ownership, including Samsung Electronics and SK Hynix.

Thus, rate expectations translate into both sentiment and mechanical flow effects.

News-style summary

- Renewed hike risk reduced global risk-asset preference.

- Semiconductor large caps faced amplified valuation compression.

- USD strength and KRW weakness risks raised the probability of weaker foreign inflows.

- The KOSPI decline reflected the interaction of rate repricing and foreign flow sensitivity.

3. Taxation of unrealized equity gains: why markets react strongly

The liquidity concern: taxes on gains not yet monetized

Markets respond negatively to unpredictable tax frameworks. Taxation on unrealized gains creates a liquidity mismatch: paper gains may not correspond to available cash. If tax liabilities arise from mark-to-market gains, investors may be compelled to sell holdings to fund payments, structurally increasing forced selling pressure.

Why the debate itself can matter more than implementation timing

The primary issue is not immediate enactment but the risk premium created by policy uncertainty. Tax-regime shifts can alter:

- portfolio construction,

- holding-period decisions,

- capital allocation strategies.

In fragile sentiment environments, perceived policy risk can suppress incremental demand and weaken rebound dynamics.

News-style summary

- Unrealized-gain taxation discussions increased perceived liquidity and forced-selling risks.

- Policy uncertainty itself became a valuation discount factor.

- In weak tape conditions, tax headlines can accelerate risk aversion.

Key points often omitted in mainstream coverage

Core point 1. The move was driven more by “expectation reset” than by immediate earnings deterioration

The decline appears less about abrupt fundamental impairment and more about a repricing from elevated expectations. Samsung Electronics and SK Hynix had already priced in substantial AI/HBM and memory-cycle recovery narratives. In such conditions, incremental negative signals can trigger profit-taking and multiple compression.

Core point 2. The market’s focus differs between Samsung Electronics and SK Hynix even when both fall

Despite sector co-movement:

- SK Hynix is more directly positioned as a primary HBM/AI memory beneficiary and may be more sensitive to AI capex expectations.

- Samsung Electronics has broader business exposures (devices, foundry, consumer electronics), and often reflects a wider set of macro and flow variables, including foreign ownership dynamics.

This distinction is relevant for identifying where risk is being reduced first.

Core point 3. The underlying driver was a global increase in discount rates rather than a Korea-specific issue

Interpreting the move solely through domestic headlines can be incomplete. The more consistent explanation is a global repricing of discount rates and risk premia applied to future growth, which tends to impact AI-linked leaders most strongly.

What to monitor next

1. US mega-cap earnings and capital expenditure

A stabilizing signal for Korean semiconductors would be confirmation that AI infrastructure and server investment remains intact. Conversely, downside risk increases if capex guidance softens meaningfully versus expectations.

2. Federal Reserve communication and US Treasury yields

Beyond policy-rate decisions, the key variables are:

- the tone of Fed messaging,

- the level and trajectory of the US 10-year yield,

- market reactions to inflation data.

The relevant sensitivity is often whether yields can move higher from current levels, not only their absolute level.

3. Foreign flows and KRW-USD

Sustained KOSPI recovery typically requires renewed foreign buying in Samsung Electronics and SK Hynix. KRW stability is a supporting condition; persistent FX volatility can constrain risk-taking by global investors.

4. Domestic policy signaling

Tax and capital-market policy commentary can affect sentiment even without near-term execution. The key question is whether messaging reduces uncertainty or prolongs it, influencing retail risk appetite and marginal liquidity.

Investor framework for interpreting current conditions

In the current regime, the key variable is not only company quality but the market multiple investors are willing to assign. While the long-term competitiveness of Samsung Electronics and SK Hynix is unlikely to change materially in a single session, assets priced for high expectations can experience deeper and longer adjustments when discount rates rise or narratives are challenged.

The practical distinction is whether the move reflects:

- a fundamental deterioration in the semiconductor cycle, or

- valuation-driven adjustment driven by rates, risk premia, and sentiment.

This differentiation informs whether pullbacks are treated as tactical opportunities or signals to remain conservative.

At-a-glance summary of today’s market

- The KOSPI decline reflected simultaneous pressure from US equity weakness, rate risk, and policy uncertainty.

- Samsung Electronics and SK Hynix were directly affected by weaker US mega-cap AI sentiment.

- Re-emerging rate-hike risk increased valuation pressure on growth-sensitive semiconductors.

- Unrealized-gain taxation discussions amplified risk premia via policy uncertainty.

- The dominant driver was expectation reset and higher global discount rates rather than immediate earnings collapse.

< Summary >

The sharp decline in the KOSPI, Samsung Electronics, and SK Hynix can be attributed to concurrent factors: weaker Nasdaq-driven AI and semiconductor sentiment, renewed concerns about additional US rate hikes, and policy uncertainty related to taxing unrealized equity gains. The primary mechanism appears to be multiple compression via higher discount rates and an expectations reset rather than a sudden breakdown in fundamentals. Key variables to monitor include US mega-cap capex guidance, Federal Reserve messaging and Treasury yields, foreign flows and KRW stability, and domestic policy clarity.

[Related Articles…]

- KOSPI Outlook: Foreign Flows and Key Turning Points

- Semiconductor Cycle: AI Memory and HBM Demand Signals

*Source: [ 내일은 투자왕 – 김단테 ]

– 코스피 삼전 닉스 폭락의 3가지 비밀

● AI-Power-Bottleneck-Supercycle

Even if the Strong Dollar Reverses, the Power Equipment Trade Is Not Over: AI Data Centers, 765 kV Transformers, and the Real Bottleneck in Grid Capacity

The key takeaways in this cycle are threefold.

First, the power infrastructure supercycle is likely to last longer than the market assumes.

Second, even if the U.S. dollar tailwind fades, the core investment thesis for power equipment is not FX-driven; it is anchored in shortages of extra-high-voltage (EHV) transformers and supplier pricing power.

Third, AI’s binding constraint has shifted beyond GPUs and HBM to power grids, transformers, and data center interconnection/permitting.

This note focuses on why Hyosung Heavy Industries, HD Hyundai Electric, and LS Electric can lead at different points in time; why 765 kV-class EHV transformers function as a scarce global asset; why earnings momentum may remain resilient even with FX normalization; and why power infrastructure is increasingly pivotal in the next phase of AI deployment.

1. Core message: power equipment is a bottleneck trade, not an FX trade

The rally in power equipment should not be framed primarily as a strong-dollar beneficiary trade.

The central driver is a global shortage of EHV power infrastructure supply.

Rising demand from AI data center build-outs, replacement of aging grids, renewable interconnection expansion, and higher utility capex is occurring simultaneously, structurally extending the shortage in transformers and related equipment.

Accordingly, the sector should be treated less as a cyclical trade and more as a beneficiary of long-duration structural change.

2. Why power infrastructure has become the binding constraint in the AI era

2-1. Bottlenecks in the AI value chain continue to migrate

The initial AI investment wave concentrated on GPU availability.

The next bottleneck shifted to HBM.

The current constraint is increasingly power infrastructure.

As AI models scale, server counts rise; as servers rise, data center power demand increases sharply. Even with sufficient semiconductors, data centers cannot operate without reliable grid connection. This has become a practical, execution-critical bottleneck.

2-2. Data centers consume materially more power than commonly assumed

Large-scale data centers operate at power levels comparable to, or exceeding, residential demand of a mid-sized city.

The key issue is that securing a site is often easier than securing power. Even with land and construction readiness, projects can be delayed if grid interconnection approval is not granted.

AI infrastructure competition is therefore increasingly determined by speed of power access, not only compute performance.

2-3. Interconnection and permitting delays can extend the cycle

In the U.S., data center delays are increasingly linked to:

- Grid interconnection approval delays

- Environmental regulation

- Local community and NGO opposition

- Insufficient transmission capacity

- Extended transformer lead times

These delays are not demand-driven; they reflect demand outpacing institutional processes and industrial capacity. Such conditions typically extend the upcycle rather than end it.

3. Where the power supercycle stands

Some investors argue the sector is late-cycle given prior price appreciation.

An alternative view is that, once bottlenecks, permitting delays, and long manufacturing lead times are incorporated, the cycle can remain effectively early-to-mid stage for longer than expected.

Korea’s domestic power infrastructure investment cycle may also be less advanced than implied by global headlines, reinforcing the need to evaluate the theme as multi-year infrastructure capex rather than a short-lived equity rotation.

4. Does the thesis end if the strong dollar reverses?

4-1. FX has been supportive, but it is not the core thesis

Higher USD/KRW has benefited exporters with meaningful U.S. exposure, supporting revenue and margins.

This explains recurring concerns that earnings may peak if FX normalizes.

However, FX is a secondary variable; the structural driver is not currency, but equipment scarcity and pricing power.

4-2. The primary driver is supplier pricing power and high-spec capability

Sector margins are more sensitive to who can manufacture scarce, high-spec products than to spot FX.

A key example is the 765 kV-class EHV transformer.

This class is believed to be producible by only ~4–5 companies globally, and effectively by only a small subset in Korea. With strong demand and limited qualified supply, pricing power accrues to suppliers, supporting profitability even if FX tailwinds fade.

4-3. U.S. local production expansion may reduce FX sensitivity over time

Tariff risks and supply-chain reshoring are incentivizing Korean power equipment firms to increase U.S. production footprints.

As localization rises, USD/KRW sensitivity can decline, potentially shifting the market framework from “FX beneficiary” toward “globally localized power infrastructure supplier.”

5. Why stock performance diverges within the sector: Hyosung Heavy Industries, HD Hyundai Electric, LS Electric

5-1. Sector grouping is insufficient; equity leadership rotates

Power equipment names should not be treated as a single beta basket.

Markets typically reward the company with the strongest forward growth profile. A firm may post +100% operating profit growth one year and decelerate to +50–60% the next; another may accelerate from a lower base. Equity performance often tracks the direction of growth rates, not just absolute levels.

5-2. Growth deceleration does not necessarily signal cycle termination

A slowdown from +100% to +60% can still represent sector-leading expansion. If absolute earnings levels remain elevated and competitive advantages persist, leadership can continue.

5-3. Markets discount the next inflection

Selection factors increasingly include:

- Order backlog trajectory

- Capacity expansion timing

- Product mix and high-margin EHV exposure

- North America revenue mix and localization

- Year-on-year operating profit growth direction

- Price durability tied to supplier scarcity

At this stage, security selection is more important than sector exposure alone.

6. Why 765 kV EHV transformers matter

6-1. Extremely scarce, high-barrier capability

EHV transformers are among the most pricing-powerful assets in power infrastructure. The 765 kV class requires advanced engineering, long fabrication cycles, and stringent certification, creating high entry barriers. In this setup, limited supply can matter more than demand strength.

6-2. Long lead times constrain supply response

While some industries can expand output quickly, EHV transformers can require roughly two years from order to delivery.

As demand rises, supply cannot respond immediately, leading to:

- Backlog accumulation

- Sustained pricing power

- Higher earnings visibility

This dynamic tends to prolong the upcycle.

7. Renewables and on-site generation: complementary, not separate

7-1. Nuclear is strategically important but too slow for near-term constraints

Nuclear can be a long-term solution, but it is generally too slow to alleviate near-term data center power shortages. From contracting to commissioning, timelines can exceed 10 years. The immediate need is power that can be connected quickly.

7-2. This increases focus on solar, BESS, and SOFC

Under urgent load growth, faster-deployable options gain relevance:

- Solar

- BESS (battery energy storage systems)

- SOFC (solid oxide fuel cells)

- Gas turbine-based distributed generation

On-site generation, located near data centers, can reduce transmission constraints and accelerate power availability. It may become a core design option rather than an auxiliary measure.

7-3. Alternatives can create secondary shortages

If data center deployment remains rapid, demand concentration can also tighten supply for solar, BESS, and fuel cells, producing new bottlenecks. The constraint can spread beyond T&D into generation equipment and project delivery.

8. U.S. versus Korea: the primary demand center and the key suppliers

The U.S. is central given its scale in AI data center investment, utility capex, and EHV equipment demand.

Korean suppliers are relevant because they are positioned as direct beneficiaries of U.S. structural demand, implying the need to monitor U.S. grid investment and data center expansion alongside domestic indicators. This is a global equity theme, not solely a local market rotation.

9. News-style checklist: what to monitor

9-1. Demand

- AI data center build-out remains rapid.

- Power demand is exceeding prior expectations.

- Interconnection delays are affecting project schedules.

9-2. Supply

- The number of EHV transformer suppliers is limited.

- 765 kV-class equipment is effectively a scarce capability asset.

- Long lead times limit near-term supply expansion.

9-3. Earnings

- Even with reduced FX support, high-margin mix is critical.

- Backlog and price durability are key determinants.

- Differentials in earnings growth rates drive intra-sector dispersion.

9-4. Policy

- The U.S. is moving to accelerate grid interconnection processes.

- Environmental regulation and local opposition remain risks.

- Policy easing reflects excessive demand pressure, not weakening demand.

10. Underappreciated point: bottleneck migration drives capital concentration

Most coverage ends at “AI-driven demand,” “strong-dollar benefit,” or “transformer shortage.”

The more actionable framework is bottleneck migration.

Capital and profit pools tend to concentrate where supply is most constrained:

- Previously: GPUs

- Then: HBM

- Now: grids, transformers, and interconnection/permitting

This helps explain why leadership can rotate and why the sector can remain strategically relevant even as FX tailwinds soften.

The durability of the thesis rests on the combination of:

- Scarce technical capability

- Supplier pricing power

- Long manufacturing lead times

- Essential role in AI infrastructure activation

11. Practical investor framework

Recommended evaluation sequence:

- Capability to produce EHV transformers

- North America exposure and U.S. localization plans

- Backlog growth rate

- High-margin product mix share

- Direction of operating profit growth (next year versus this year)

- Price durability and continuation of supplier scarcity, versus FX effects

At the index level, the decision is whether to treat the sector as “already up significantly” or as an “AI infrastructure bottleneck enabler.” Under the latter framing, the group can retain characteristics of a medium-term structural growth exposure rather than a short rotation.

12. Conclusion: a weaker dollar does not automatically end the power equipment thesis

The strong dollar has been supportive, but it is not the defining driver.

Key structural factors include global grid capex expansion, rapid AI data center power demand growth, scarcity of 765 kV-class EHV transformers, and high entry barriers that concentrate supply among a small number of qualified manufacturers.

Given permitting delays and long production lead times, the power infrastructure cycle can persist longer than market expectations. The more accurate framing is “essential AI-era infrastructure supplier” rather than “late-stage strong-dollar beneficiary.”

< Summary >

The primary driver is not FX, but shortages in EHV transformers and supplier pricing power.

AI data center expansion is shifting AI’s binding constraint toward grids, transformers, and interconnection/permitting.

765 kV-class transformers are a scarce global capability, supporting price-setting power.

Even if FX normalizes, earnings can remain resilient if high-spec pricing and backlog stay firm.

Hyosung Heavy Industries, HD Hyundai Electric, and LS Electric can diverge due to differences in earnings growth rates and forward momentum.

Nuclear is slow to deploy; solar, BESS, SOFC, and on-site generation are faster and therefore increasingly relevant for data center power solutions.

Overall, the power infrastructure supercycle is unlikely to be over and may gain importance as an AI-era bottleneck segment.

[Related Articles…]

- AI Infrastructure Bottlenecks and Data Center Power Demand

- Transformer Supercycle: Grid Capex, Lead Times, and Supplier Pricing Power

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 강달러 끝나도 전력주는 끝난 게 아닙니다 | 경읽남과 토론합시다 | 손현정 연구원 [2편]