● Korea Market Shock, Pension Selloff, AI Shockwave, Rate Hike Fears

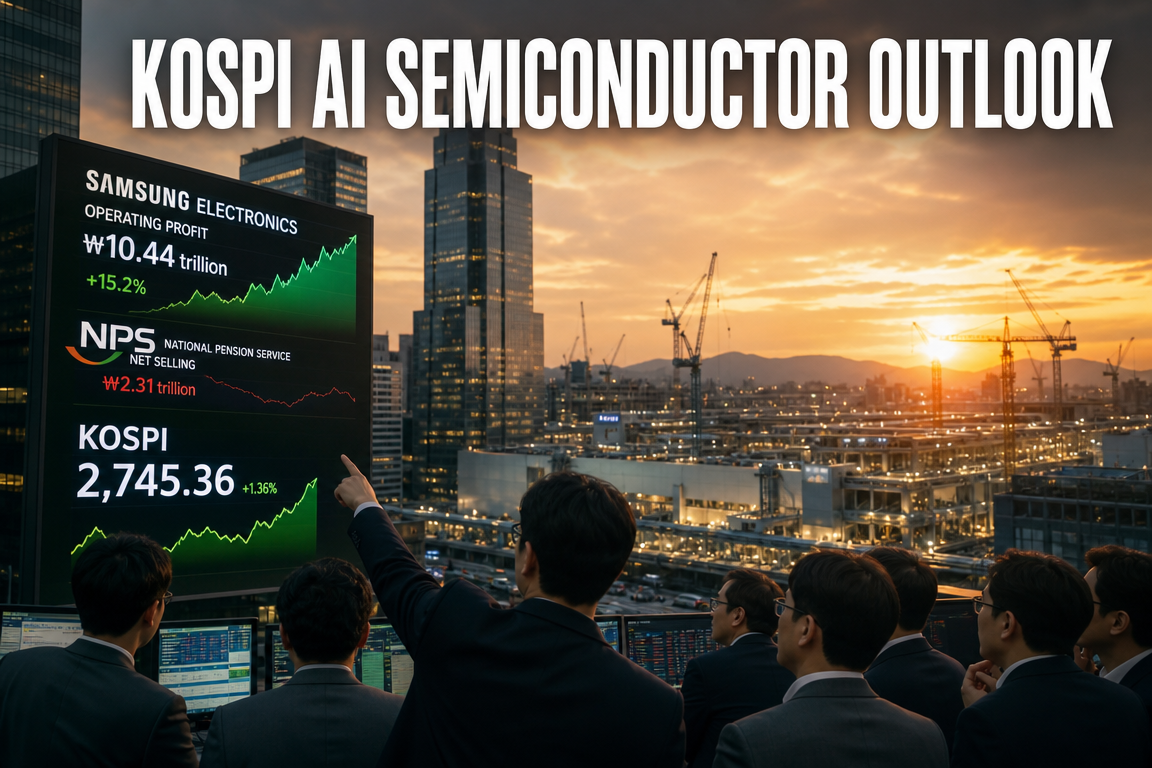

Samsung Electronics and SK Hynix earnings versus the alleged KRW 55 trillion National Pension Service selling pressure: the key variable for the KOSPI in July

July will not be determined by a single headline such as “the National Pension Service will sell KRW 55 trillion.”

The key issue is the simultaneous interaction of National Pension Service rebalancing, earnings from Samsung Electronics and SK Hynix, rising overseas investment by retail investors, the possibility of a Bank of Korea rate hike, and large IPOs in China and the United States.

While much of the media and online commentary focuses only on “selling pressure,” the decisive factor for the KOSPI in July may be who absorbs that supply.

This report assesses whether the alleged KRW 55 trillion National Pension Service selling pressure can materially weigh on the KOSPI, or whether the market is pricing in excessive concern.

1. Why the KRW 55 trillion National Pension Service selling story suddenly became a market factor

Recent reporting that Barclays suggested the National Pension Service’s asset allocation could increase volatility in the Korean equity and foreign exchange markets has intensified debate.

The core issue is that the National Pension Service must manage its domestic equity weighting within a defined range, and the recent rally in the KOSPI may have pushed that weighting above the upper limit.

The National Pension Service stated that the analysis was based on overly aggressive assumptions, but the market has nonetheless become concerned that large-scale selling could begin in July.

- The National Pension Service portfolio includes domestic equities, overseas equities, domestic bonds, overseas bonds, and alternative assets.

- The previous target weighting for domestic equities was around 14.9% by end-2026.

- However, the domestic equity weighting was cited at around 21% as of March 2026, reflecting the market rally.

- This increase was driven primarily by rising equity valuations rather than additional purchases of domestic stocks.

In other words, the National Pension Service did not necessarily buy more Samsung Electronics or SK Hynix shares; the value of existing holdings rose, which increased the portfolio share of domestic equities.

2. A 20.8% domestic equity target: the issue is the effective range

In late May, the National Pension Service’s fund management committee revised the domestic equity target weighting from 14.9% to 20.8%.

This decision can be seen as an effort to reduce market disruption.

Had the target remained at 14.9%, the National Pension Service would likely have needed to sell significantly more domestic equities after the rally in the KOSPI.

- Domestic equity target weighting: 20.8%

- Tactical asset allocation band: ±2 percentage points

- Strategic asset allocation band: ±6 percentage points

- Effective upper bound: 20.8% + 2% + 6% = 28.8%

- Effective lower bound: 20.8% – 2% – 6% = 12.8%

The concern is that domestic equity weighting may already be near 30% or higher, depending on estimates.

If so, once the temporary rebalancing deferral ended on June 30, the National Pension Service may have had to begin reducing domestic equity exposure from July.

3. Is the “KRW 55 trillion selling wave” realistic or exaggerated?

The market has circulated concerns that the National Pension Service could sell up to KRW 55 trillion of domestic equities.

However, interpreting this as a single selling wave in July is overstated.

As a public pension fund, the National Pension Service must also consider market stability, making gradual and phased selling more likely than a one-time disposal.

- The National Pension Service deferred mechanical selling related to excess domestic equity weighting through the end of June.

- This was intended to avoid unnecessary volatility in the Korean market.

- Some preemptive rebalancing appears to have occurred in May and June.

- According to the source text, net selling by pension funds reached about KRW 120 billion in one week in mid-May.

- This translates to an average of about KRW 24 billion per day.

In other words, the scenario of a single KRW 55 trillion sell-off in July appears unlikely.

That said, National Pension Service rebalancing would still create downward pressure on the KOSPI.

The more important issue is not the size of the selling alone, but the pace of the selling and who absorbs it.

4. First variable for the July KOSPI outlook: whether foreign capital returns

In the first half of 2026, retail investors are said to have absorbed a substantial amount of the selling from institutions and foreigners.

According to the source text, foreigners recorded net selling of about KRW 116 trillion in the first half, much of which was absorbed by retail investors.

Despite that, the KOSPI maintained an upward trend, indicating strong retail demand.

The key question now is July and beyond.

If foreigners return and buy Korean equities while the National Pension Service gradually sells, the market impact may remain limited.

However, if foreigners stay on the sidelines and retail investors continue shifting capital abroad, domestic market liquidity could weaken.

- National Pension Service selling + foreign buying = limited KOSPI impact

- National Pension Service selling + foreign neutrality + rising overseas retail investment = greater downside risk

- National Pension Service selling + weak semiconductor earnings + rate hike concerns = combined downward pressure

Accordingly, the July KOSPI outlook is not determined by the National Pension Service alone.

Foreign capital flows, retail allocation to overseas assets, and the won-dollar exchange rate must be monitored together.

5. Second variable: rising overseas investment by retail investors

Recent foreign securities custody trends indicate renewed strength in overseas investment by retail investors.

In particular, net buying of foreign securities accelerated from May 2026.

This suggests that retail capital is rotating from domestic equities to U.S. equities, AI-related stocks, and expectations around large IPOs.

For the Korean market, rising overseas investment by retail investors is a short-term headwind.

If the National Pension Service reduces domestic equity exposure while retail investors move further into U.S. markets, a domestic liquidity gap may emerge.

- Expectations for a SpaceX listing or related investment themes

- IPO expectations for AI companies such as OpenAI and Anthropic

- Preference for U.S. mega-cap technology and AI exposure

- Profit-taking sentiment in the Korean market after the rally

- Higher exchange rate expectations and demand for dollar assets

As enthusiasm for the AI sector rises, capital may continue shifting from Korean large caps to overseas growth names.

This could reduce the upside momentum of the KOSPI.

6. Third variable: Samsung Electronics and SK Hynix earnings releases

One of the most important July events for the Korean market is the second-quarter earnings release from Samsung Electronics and SK Hynix.

Given their large weight in the market capitalization of the KOSPI, these companies are effectively central to index direction.

The source text notes that, when combined with Samsung Electronics preferred shares, SK Hynix, and related names, their market influence is substantial.

The market has already priced in a meaningful degree of recovery in semiconductor earnings.

As a result, the key issue is not whether earnings are strong, but whether they exceed expectations.

- Samsung Electronics preliminary second-quarter results are expected around mid-July.

- SK Hynix earnings release is also a major July event.

- The market expects strong operating profit growth.

- The source text references second-quarter operating profit expectations of about KRW 9.2 trillion.

- Results above expectations could support the market through an earnings surprise.

- Results below expectations could trigger corrections in semiconductor-heavy indices.

Samsung Electronics and SK Hynix are the primary beneficiaries of AI semiconductors, HBM, and the memory upcycle.

For investors, however, the immediate question is whether second-quarter results can meet the elevated market bar.

7. Fourth variable: the possibility of a Bank of Korea rate hike

In the second half of 2026, global financial markets are again focused on the possibility of higher interest rates.

As some economies raise policy rates, the Bank of Korea may also face pressure to tighten policy.

For Korea, the main reasons are twofold.

First is inflation pressure.

Second is exchange-rate pressure.

- A weaker won increases import-price pressure.

- If inflation rises again, the Bank of Korea may need to consider tightening.

- Higher policy rates are generally negative for equities.

- Growth stocks and highly valued large caps are especially sensitive to higher discount rates.

If rate-hike expectations become more credible in July, short-term downside pressure on the KOSPI could increase.

If National Pension Service rebalancing and a rate-hike risk occur simultaneously, investor sentiment may weaken further.

8. Fifth variable: China’s large IPO pipeline and the CXMT listing issue

China also has large IPOs under consideration, and these are drawing market attention.

The source text refers to a major IPO by a Chinese renewable energy company and the possible listing of CXMT, or ChangXin Memory Technologies.

CXMT is viewed as a key company in China’s memory semiconductor localization strategy.

If its IPO proceeds, some global semiconductor capital could shift toward China.

- Possible large IPOs in China’s renewable energy sector

- Potential listing plans for CXMT

- Support from China’s semiconductor self-sufficiency policy

- Relative valuation comparisons with Korean semiconductor firms

- Possible reallocation of global liquidity toward Chinese assets

For the Korean market, large Chinese IPOs could become a source of capital dispersion.

In particular, if competition between Korean and Chinese semiconductor firms becomes more pronounced, investor sentiment toward Samsung Electronics and SK Hynix could be affected.

9. Sixth variable: U.S. mega-IPOs and the pull of AI capital

In the United States, expectations for AI-related IPOs remain strong.

The source text cites SpaceX, OpenAI, and Anthropic as possible listing candidates.

Although the timing is uncertain, the market increasingly views these potential IPOs as major liquidity events.

OpenAI and Anthropic are central to global AI competition.

Movement of key talent from major technology companies into AI startups has also reinforced investor interest.

- AI IPO expectations could draw capital toward the U.S. market.

- Talent migration in the AI sector may support revaluation of related companies.

- OpenAI and Anthropic are symbols of infrastructure-level AI competition, not just software businesses.

- U.S. mega-IPOs could intensify overseas investment by Korean retail investors.

- This would likely weigh on domestic liquidity conditions.

In the medium term, the AI theme is constructive for Korean semiconductors, but in the short term it may divert capital toward U.S. markets.

That is an important consideration for the July KOSPI outlook.

10. The key point often missed: simultaneity matters more than National Pension Service selling alone

Many reports focus only on National Pension Service selling.

However, the real issue is whether other variables move in the same direction at the same time.

If the National Pension Service sells but foreign investors buy, Samsung Electronics and SK Hynix beat expectations, and the exchange rate stabilizes, the KOSPI may remain resilient.

By contrast, if the National Pension Service sells, retail investors continue moving overseas, foreigners stay cautious, semiconductor earnings miss expectations, and rate-hike concerns increase, the correction could deepen.

- National Pension Service selling is a supply overhang, not a standalone shock

- Semiconductor earnings are the key earnings variable for the index

- Retail overseas investment is a liquidity outflow factor

- Rate-hike risk is a valuation compression factor

- U.S. and Chinese IPOs are global liquidity rotation events

If these five factors all turn negative at once, the KOSPI could weaken in July.

However, if some of them move in a constructive direction, it is difficult to argue that National Pension Service rebalancing alone will trigger a major downturn.

11. Why the National Pension Service cannot simply execute a large-scale sell-off

The National Pension Service is not a conventional investor focused solely on returns.

As a public pension fund managing retirement assets, it must consider profitability, stability, public responsibility, liquidity, and long-term sustainability.

- Profitability: long-term returns must be maintained

- Stability: excessive losses and volatility must be avoided

- Public responsibility: unnecessary market shocks should be avoided

- Liquidity: pension payments and allocation management must remain stable

- Sustainability: the long-term funding outlook must be preserved

Even if rebalancing is required to align with policy targets, the National Pension Service is unlikely to sell in a way that would destabilize the market.

A phased and diversified approach is more likely than abrupt liquidation.

12. Three scenarios for the July KOSPI and implications for investors

The July KOSPI outlook can be divided into three broad scenarios.

- Positive scenario

Samsung Electronics and SK Hynix beat expectations, foreign buying returns, and rate-hike concerns ease.

In this case, the KOSPI could continue its upward trend despite National Pension Service rebalancing pressure. - Neutral scenario

National Pension Service selling remains gradual, semiconductor earnings are in line with expectations, and foreign and retail flows offset each other.

The KOSPI may experience short-term consolidation rather than a sharp decline. - Negative scenario

National Pension Service selling, rising overseas retail investment, weaker-than-expected semiconductor earnings, rate-hike concerns, and capital diversion into U.S. and Chinese IPOs all occur together.

In this case, the KOSPI could face a meaningful correction in July.

Investors should focus not on the headline that the National Pension Service is selling, but on which conditions emerge simultaneously.

In particular, foreign flows, the won-dollar exchange rate, and the semiconductor earnings releases are critical indicators around the Samsung Electronics and SK Hynix reporting dates.

13. Key indicators to monitor in July

- Daily net selling by the National Pension Service and pension funds

- Whether foreigners return to net buying in the KOSPI

- Whether retail overseas stock purchases continue to rise

- The outcome of Samsung Electronics’ second-quarter preliminary results

- SK Hynix earnings and commentary on HBM demand

- Movements in the won-dollar exchange rate

- Bank of Korea rate-hike expectations

- News flow on CXMT and other Chinese IPOs

- U.S. AI IPO expectations and capital flows into mega-cap technology

If these indicators align in one direction, volatility in the KOSPI may increase.

If they offset one another, the market may remain more stable than currently feared.

14. Conclusion: the market is too complex to be defined by the KRW 55 trillion selling story alone

The National Pension Service’s reduction in domestic equity exposure is clearly a headwind for the KOSPI.

However, it is not sufficient to conclude that the index will necessarily decline in July.

Some preemptive rebalancing likely occurred in May and June, and the National Pension Service must also consider market stability.

Ultimately, the key issue for the July Korean market is not selling by the National Pension Service alone, but the combination of semiconductor earnings, foreign flows, retail overseas investment, interest rates, and global IPO events.

If Samsung Electronics and SK Hynix exceed expectations, much of the rebalancing pressure could be absorbed.

If weaker earnings are combined with capital outflows, downside risk would rise materially.

Investors should avoid reacting to fear headlines and instead monitor liquidity, earnings, rates, and the exchange rate together.

July may prove to be a turning point for determining whether the Korean market can extend its semiconductor-led rally.

< Summary >

The alleged KRW 55 trillion National Pension Service selling pressure is a headwind for the KOSPI, but it is unlikely to appear as a sudden one-time liquidation.

The National Pension Service has raised its domestic equity target to 20.8%, and the effective upper bound is around 28.8%.

Domestic equity weighting may already be near 30%, increasing the need for rebalancing.

Some preemptive adjustment may already have occurred in May and June.

The key July variables are earnings from Samsung Electronics and SK Hynix, foreign capital inflows, overseas retail investment, Bank of Korea rate-hike risk, and large IPOs in China and the United States.

The market direction will not be decided by National Pension Service selling alone; downside risk rises when multiple negative factors occur at the same time.

Investors should prioritize monitoring pension fund flows, foreign flows, the exchange rate, and semiconductor earnings releases.

[Related Articles…]

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 삼성전자-SK하이닉스 실적 발표 Vs 국민연금 55조 매도. 7월 코스피 꺾일까? [경읽남 251화]

● AI-Shift, KOSDAQ-Surge, Foreign-Selloff

Money Flow Is Shifting: Why Kosdaq and Undervalued Sectors Moved as Samsung Electronics and SK Hynix Paused

The key point today is not simply that Samsung Electronics and SK Hynix declined.

The more important development is that, amid unstable foreign investor flows, capital moved rapidly into Kosdaq, secondary batteries, biopharma, robotics, shipbuilding, power equipment, and undervalued growth stocks.

This shift coincided with Samsung and SK’s large-scale investment plans, the BIS warning on an AI bubble, expectations for a Kosdaq tiering system, and pressure on low-PBR companies to improve capital efficiency.

In other words, the market is moving from an “own only AI semiconductors” phase to one in which AI must be viewed alongside exchange rates, rates, earnings, and policy beneficiaries.

1. Today’s market in one line: as Samsung and SK paused, previously lagging sectors came alive

Samsung Electronics and SK Hynix weakened today, while other sectors rebounded strongly.

As large-cap semiconductor stocks that had led the KOSPI paused, funds rotated into sectors and names that had underperformed.

- Samsung Electronics and SK Hynix: weaker on short-term profit taking and AI semiconductor concerns

- LG Energy Solution: strong rebound

- Power equipment, shipbuilding, and autos: buying concentrated in previously lagging sectors

- EcoPro: sharp gain

- Alteogen and Rainbow Robotics: inflows into leading Kosdaq growth names

This may prove to be only a one-day rebound, but a clear change in positioning was visible.

Capital that had concentrated in Samsung Electronics, SK Hynix, semiconductor equipment, and AI data center-related names is now rotating toward less extended sectors.

2. First driver: Samsung and SK announced massive investment plans

The first market-moving issue was the large-scale investment plans announced by Samsung and SK.

Based on the source text, Samsung referenced approximately KRW 2,655 trillion, while SK referenced approximately KRW 2,100 trillion.

Combined, the two groups’ investment plans approach KRW 4,700 trillion.

The investment areas are broadly divided into three categories.

- Expansion of semiconductor production bases

- AI data center construction

- Regional industrial infrastructure investment, including Yongin, Pyeongtaek, Cheongju, and the Honam region

Samsung continues semiconductor investment centered on Yongin and Pyeongtaek, while AI data center investment in Haenam was also mentioned in the Honam region.

SK placed stronger emphasis on AI data centers.

In particular, a 15 GW AI data center plan was mentioned, with an initial 5 GW phase and expansion to 15 GW by 2035.

The related investment scale was cited at around KRW 1,000 trillion.

SK also indicated plans to bring forward completion of the Yongin semiconductor cluster by roughly 20 years to 2033.

Additional regional investment plans were also cited, including KRW 600 trillion in Yongin, KRW 100 trillion in Cheongju, and KRW 400 trillion in semiconductor investments in the Yeongnam or Seonnam region.

3. Why did Samsung Electronics and SK Hynix not rise materially?

At first glance, large-scale investment announcements should have been positive for Samsung Electronics and SK Hynix.

However, the market reaction was limited.

The reason is straightforward.

Equity markets tend to be most sensitive to capital that can be converted into earnings within one to two years.

Building fabs, data centers, and semiconductor clusters takes time.

If the investments are unlikely to translate into revenue and earnings quickly, the share price response is typically muted.

As a result, this mega-project announcement had more impact on related beneficiaries than on Samsung Electronics and SK Hynix themselves.

The move in power equipment, construction, infrastructure, equipment, materials, and data center-related stocks reflects this dynamic.

In short, the announcement is positive over the long term.

In the short term, however, the main drivers remain memory prices, AI demand, earnings outlooks, and foreign investor flows.

4. Second driver: BIS warning on an AI bubble, not new, but not ignorable

The Bank for International Settlements warned that AI investment may be forming a bubble.

The message was strong.

AI data center investment is expanding too quickly, and if higher rates, higher power costs, and higher chip prices coincide, returns could fall below expectations.

The BIS outlined the following risk scenario.

- Interest rates remain elevated.

- Power costs rise.

- GPU and AI semiconductor prices increase.

- AI data center construction costs surge.

- Returns on investment decline.

- Large-scale investment by Big Tech and startups slows.

- Recursive financing structures weaken.

- Risk may spread to banks and investment banks.

Some observers note that, if such a structure worsens, it could evolve into a financial shock similar to the Lehman Brothers crisis.

That said, this is not a new concern.

Fears about an AI bubble, data center profitability, power shortages, and GPU collateral risk have been discussed throughout the year.

Accordingly, the BIS report alone does not justify categorizing all AI-related stocks as risky.

What matters is that the market is increasingly evaluating AI companies on actual returns and cash flow, not only on revenue growth.

5. The key issue rarely highlighted elsewhere: the AI circular financing structure is the real risk

The most important point in today’s market is not simply whether AI is a bubble.

The real issue is that money within the AI ecosystem is circulating through investment capital rather than through end-customer demand.

For example:

An AI startup with minimal revenue is valued by a Big Tech company at KRW 10 trillion.

Big Tech then invests KRW 1 trillion for a 10% stake.

The startup is immediately treated as a KRW 10 trillion company.

In practice, it has only received KRW 1 trillion in cash.

Yet its paper valuation becomes KRW 10 trillion.

The startup uses that KRW 1 trillion to pay cloud usage fees or purchase GPUs.

That capital then reappears as revenue for Big Tech or AI infrastructure companies.

In this structure, money invested by Big Tech returns as revenue to Big Tech.

On the surface, AI cloud revenue appears to rise and GPU demand appears to surge.

However, if the final customer is not paying in a durable way, the structure resembles circular financing.

Risk increases further if GPUs are pledged as collateral for loans, or if the same collateral is used multiple times across institutions.

This issue is often reduced in the media to a simple “AI bubble” narrative, but in reality it is a potentially material financial-system risk.

That said, it is not yet an imminent breakdown scenario.

The signals to monitor are clear.

- Lower AI data center utilization

- Slower cloud revenue growth

- Declining GPU lease rates

- Reduced capex from Big Tech

- Lower AI startup valuations

- Weakness in GPU-backed lending

Until these signals appear, AI should not be dismissed wholesale as a bubble.

However, investors in AI-related stocks should now assess investment payback periods and cash flow as closely as growth rates.

6. Third driver: foreign investor selling has increased materially

Another important variable today was foreign selling.

Based on the source text, foreign investors sold approximately KRW 7.7 trillion in a single day.

Over the past five trading days, cumulative selling in the KRW 4 trillion to KRW 8 trillion range was cited, with total selling near KRW 21 trillion.

If this scale of foreign selling continues, the issue extends beyond equities.

It can affect the exchange rate as well.

When foreign investors sell Korean stocks and convert won into dollars, pressure on the won increases.

If capital outflows continue at an annualized pace equivalent to roughly KRW 80 trillion per month, FX volatility could become a new burden for the market.

Today, the market held up as institutions stepped in to buy selectively.

Retail investors remain net buyers, and the direction of the index is increasingly shaped by whether institutions absorb the selling.

If foreign investors and institutions sell together, the market can weaken quickly.

Conversely, if institutions provide support, the KOSPI and Kosdaq can remain resilient despite foreign selling.

7. Why the Kosdaq was strong: it had barely risen year to date

The Kosdaq was strong today for a simple reason.

It had underperformed materially.

The KOSPI rose strongly on large-cap IT and semiconductor leadership such as Samsung Electronics, SK Hynix, and Samsung Electro-Mechanics.

By contrast, the Kosdaq remained weak on a year-to-date basis.

Even after today’s rebound, the Kosdaq was still described as being around -1% year to date in the source text.

In other words, it was not the entire market that rose, but primarily large semiconductor names that lifted the KOSPI.

This created room for capital to rotate into previously neglected Kosdaq growth names, biopharma, secondary batteries, robotics, beauty, and mid-cap earnings stocks.

As concerns emerged around AI and memory semiconductors, investors took profits in part and began searching for undervalued names with less prior appreciation.

That is the core of today’s Kosdaq rotation.

8. Kosdaq tiering system expectations: premium names versus monitored names

Another key issue in the Kosdaq is the expected tiering system.

Market expectations rose that related direction could be announced at the July 1 ceremony marking the Kosdaq’s 30th anniversary.

The Kosdaq tiering system would effectively classify companies by quality.

- Premium group: top companies with stronger earnings, scale, and governance

- Standard group: typical Kosdaq listings

- Monitored group: companies at risk of delisting or requiring investor caution

The premium group may become a more concentrated version of the Kosdaq 150.

Market participants also speculate that a Kosdaq 70 or Kosdaq 80 quality cohort could emerge.

Likely selection criteria include profitability, market capitalization, and governance.

Accordingly, top-cap biopharma, semiconductor equipment, secondary battery, and robotics names could be considered potential premium candidates.

If implemented, this system could further differentiate capital flows within the Kosdaq.

Institutional and foreign capital may concentrate more heavily in premium names, while investor sentiment toward monitored names could weaken sharply.

9. Penny stocks and low-PBR companies should be treated more cautiously

Starting July 1, revised rules related to delisting for sub-KRW 1,000 stocks are scheduled to take effect.

Accordingly, buying low-priced stocks simply because they appear cheap may become more risky.

In addition, a list of low-PBR companies is scheduled to be disclosed from October.

The lower 20% of listed companies will be named publicly.

In practical terms, this is a structure that publicly pressures companies with low capital efficiency.

It is similar to posting a report card on the wall, forcing low-PBR firms to improve returns on capital.

This policy is also linked to the broader value-up program.

Companies that do not expand dividends, cancel treasury shares, improve governance, or lift ROE may face stronger market pressure.

Conversely, low-PBR companies with strong cash balances, dividend capacity, and potential for treasury share cancellation may re-rate positively.

10. Portfolio strategy now: AI-only exposure is becoming less comfortable

At this stage, diversification is the key portfolio strategy.

AI and semiconductors remain core growth themes.

However, portfolios concentrated only in AI, memory, or semiconductor equipment now carry higher risk.

The source text argues for combining AI-related names with non-AI holdings.

In particular, undervalued beauty names, earnings growth stocks, dividend stocks, and defensive sectors were highlighted.

Three portfolio buckets may be considered.

- AI data center-related defensive dividend names: power infrastructure, telecom infrastructure, data center infrastructure, and grid-related companies

- Growth names not directly tied to AI but with rapid earnings growth: beauty, healthcare, consumer staples, and export growth stocks

- AI-linked growth names: semiconductors, power equipment, robotics, AI software, and cloud infrastructure

Allocation depends on risk tolerance.

Aggressive investors may prefer a higher AI weighting.

Investors focused on stability may prefer a roughly equal split among AI-related names, non-AI growth names, and defensive dividend names.

The source text also suggests a conservative approach of allocating around 20% to leading themes and 80% to assets less directly tied to AI.

This may reduce short-term upside but improve resilience in a sharp market correction.

11. Sector-by-sector signals to monitor today

Today’s market showed clear sector-level differentiation.

- Semiconductors: Samsung Electronics and SK Hynix were weaker, but the sector did not break down materially intraday.

- Secondary batteries: LG Energy Solution, EcoPro, and other previously lagging names rebounded strongly.

- Biopharma: capital flowed into large Kosdaq biopharma names such as Alteogen.

- Robotics: interest returned to growth themes such as Rainbow Robotics.

- Power equipment: expectations for AI data centers and power infrastructure remained supportive.

- Shipbuilding: leading names such as Hanwha Ocean strengthened again.

- Autos: large-cap names such as Kia rebounded on valuation support.

- Nuclear and energy: policy and order-related names such as Doosan Enerbility also gained.

This pattern does not indicate the end of AI leadership.

It suggests that some capital is rotating away from AI into other sectors.

In other words, the move is more consistent with sector rotation than with a regime change.

12. Key indicators to watch going forward

From here, investors should look beyond the index level.

The following indicators matter.

- Foreign investor flows: whether selling pressure eases

- Exchange rate: whether capital outflows weaken the won further

- Interest rates: direct impact on AI data center economics and growth valuations

- Memory prices: critical for Samsung Electronics and SK Hynix earnings

- AI data center investment pace: whether Big Tech capex slows

- Kosdaq tiering announcement: potential capital concentration in premium names

- Low-PBR disclosure: potential re-rating of value-up beneficiaries

13. Most important investment conclusion

The market is not necessarily becoming more dangerous, but it is becoming more difficult to navigate.

Given the strength of the AI semiconductor-led rally, some profit taking is natural.

However, if foreign selling continues, the exchange rate weakens, and rate pressure persists, volatility could increase further.

In this environment, a strategy focused only on chasing recent winners is less attractive than one centered on earnings support and lagging but fundamentally sound names.

In particular, the Kosdaq requires selective positioning in premium-tier candidates, earnings growth names, biopharma, secondary batteries, robotics, and semiconductor equipment companies with strong balance sheets.

By contrast, penny stocks, persistent loss makers, companies with weak governance, and low-PBR names without a clear improvement path should be treated more cautiously.

The key message is this.

When Samsung Electronics and SK Hynix pause, the next sector rotation becomes visible through where capital moves.

Most important point rarely emphasized in other media

First, the investment payback period matters more than the scale of the announcement.

Even if Samsung and SK announce investments worth several thousand trillion won, the market is more sensitive to the portion that can translate into earnings within one to two years.

Accordingly, mega-projects are long-term positives, but not necessarily immediate share-price catalysts.

Second, the core of the AI bubble debate is financial structure, not technology.

The issue is not AI technology itself, but the circular structure in which Big Tech investment capital flows through startups and returns as Big Tech revenue.

If this structure breaks down, AI valuations could be repriced quickly.

Third, the Kosdaq tiering system is not merely a procedural change; it can alter capital flows.

Companies likely to enter the premium group may attract institutional and passive capital.

Conversely, capital may leave monitored names quickly.

Fourth, foreign selling may matter more through FX than through equities alone.

If selling translates into a weaker won and higher FX volatility, market sentiment across Korean equities could deteriorate.

Fifth, this is not a market to abandon leadership names, but to rebalance the portfolio.

Rather than eliminating AI and semiconductors entirely, a more practical approach is to combine them with non-AI growth names and defensive dividend stocks to reduce risk.

< Summary >

Today’s market was characterized by capital rotating into the Kosdaq and undervalued sectors while Samsung Electronics and SK Hynix paused.

Samsung and SK’s large-scale semiconductor and AI data center investment plans are positive in the long term, but only limitedly reflected in near-term share prices.

The BIS warning on an AI bubble is not new, but AI circular financing and data center profitability remain important to monitor.

Rising foreign selling could feed into FX pressure, making fund flow monitoring essential.

The Kosdaq tiering system and low-PBR disclosure may reshape capital allocation toward premium Kosdaq names and value-up beneficiaries.

At present, a diversified allocation across AI-related names, non-AI growth names, and defensive dividend stocks appears more appropriate than concentrated AI exposure alone.

[Related Articles…]

- Kosdaq Rotation and Small-Cap Investment Strategy

- Exchange Rate Volatility and Its Impact on Foreign Flows in Korea

*Source: [ Jun’s economy lab ]

– 돈의 흐름이 바뀌고 있습니다(ft. 코스닥)