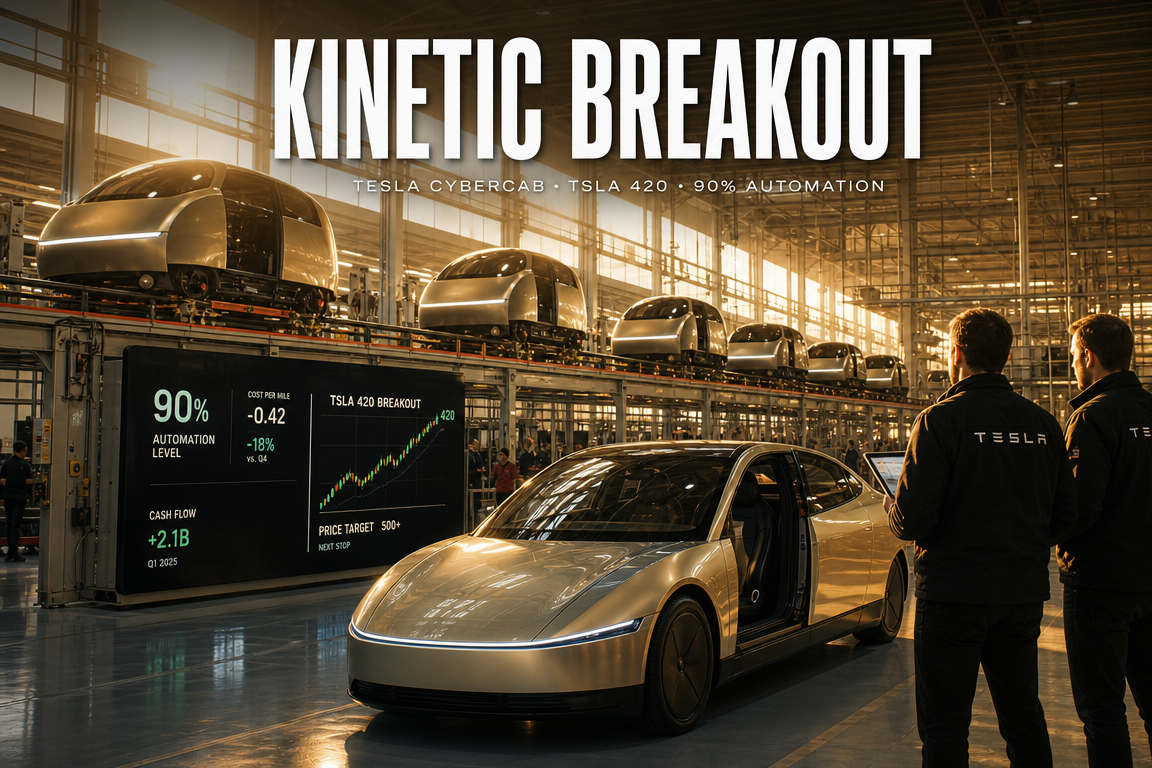

● Tesla Cybercab Shock, 90 Percent Automation, Robotaxi Surge, TSLA Eyes 420 Breakout

Tesla Cybercab Automation Confirmed at 90%: Is This a Signal for Robotaxi Mass Production? | Key Variables to Watch for TSLA in the $420 Range

The core of this Tesla news is not simply that a car without a steering wheel was driven on public roads.

The Tesla official account and Elon Musk simultaneously released Cybercab footage, Tesla vehicle engineering VP Lars Moravy discussed the program in an interview, and the upcoming second-quarter delivery outlook is all part of the same story.

Tesla is signaling a transition from an electric vehicle manufacturer to an autonomous robotaxi platform company.

Cybercab production automation at 90%, process steps reduced from 200 to 20–25, a rebound in European EV demand, and the end of Uber-Waymo collaboration are all affecting how investors view TSLA and U.S. equities.

1. Market overview | Tesla shares above $420, U.S. equities also rise

- Tesla shares were reported at $420.6.

- The daily gain was 2.13%.

- SpaceX-related pricing was cited at $170.86, up 4.06%.

- The Nasdaq rose 1.52%.

- The S&P 500 rose 0.78%.

- The Dow Jones Industrial Average rose 0.26%.

U.S. equities were broadly stronger, and Tesla shares rebounded alongside the market.

This move appears to reflect renewed expectations around Cybercab and the robotaxi business rather than a simple rebound in growth stocks.

For Tesla investors, upcoming delivery figures, autonomous-driving regulation, and Cybercab production announcements are now more important than short-term price action.

2. Tesla official X account and Elon Musk release Cybercab footage

Tesla’s official X account released footage showing Cybercab engineering tests beginning in Austin.

The vehicle in the video had no steering wheel.

It had no pedals.

The cabin featured only a minimal dashboard.

Several hours later, Elon Musk posted the same footage on his own account.

This appears to be a deliberate market signal rather than a routine promotional video.

- Most Cybercabs previously seen in Austin were training vehicles with steering wheels.

- This footage shows a steering-wheel-free Cybercab driving on public roads.

- The market impact of a prototype reveal is different from an actual road-test demonstration.

The key message is that Tesla is publicly signaling that it has reached the stage of testing a steering-wheel-free robotaxi on public roads.

3. Lars Moravy interview | Cybercab production line is already running

Tesla vehicle engineering VP Lars Moravy made several key comments in an interview with Herbert Ong.

- The production line for Cybercab is already running.

- Most vehicles currently seen on the road are for Autopilot and autonomous-driving training.

- Tesla has built a new test track outside Giga Texas.

- Burn-in testing is being conducted there.

Burn-in testing is used to identify defects in early production units.

Moravy’s comments suggest that current Cybercab units are not just test vehicles but early production vehicles used for validation.

This is significant because Tesla is not remaining at the concept stage; it is operating production and testing in parallel.

4. The biggest news | Cybercab automation exceeds 90%

The most important number from Moravy’s interview is the 90%+ automation rate.

In conventional automotive manufacturing, 90% automation is difficult to achieve.

Traditional automakers still rely heavily on human labor for assembly, wiring, inspection, and adjustment.

In many cases, 30–50% automation is already considered high.

Tesla designed Cybercab from the outset to minimize human intervention.

Its wiring and assembly approach appears to differ from Model 3 and Model Y.

- Traditional Tesla vehicles require roughly 200 final assembly steps.

- Cybercab is reportedly reduced to about 20–25 steps.

- This allows significantly higher output from the same factory footprint.

- Fewer process steps can improve speed, cost, and quality control.

This is effectively the core of the story.

Tesla is not merely building a new model; it is designing a product optimized for mass production.

5. How Cybercab differs from Model 3 and Model Y | Designed from the start for robotaxi production

Model 3 and Model Y were developed as electric vehicles for individual consumers.

Cybercab, by contrast, was designed from the start for robotaxi operations.

This difference is substantial.

- Consumer vehicles must account for broad option sets and user experience.

- Robotaxi vehicles prioritize operating efficiency, durability, cleaning, repair costs, and production cost.

- If steering wheel and pedal assemblies are unnecessary, manufacturing can be simplified.

- A simpler process can strengthen pricing competitiveness in the EV market.

Tesla’s real advantage in Cybercab is not design aesthetics but its production model.

If the 90% automation rate is sustained, Tesla could become a company able to deploy robotaxis at scale quickly.

6. Possible July 7 announcement | More likely a production expansion update than a new vehicle reveal

Moravy said that Tesla would have surprising news from Giga Texas about one week later.

He did not specify the exact content, but referred to Tesla’s scaling efforts.

This suggests the announcement is more likely to involve production capacity expansion, process improvements, or Cybercab mass-production preparation than a completely new vehicle launch.

- Giga Texas production line expansion

- Initial Cybercab production scale disclosure

- Unboxed manufacturing process update

- Robotaxi service preparation status

- Automated production system update

This remains unconfirmed until Tesla makes an official announcement.

However, the sequence of releasing footage first and then having an executive reference production developments appears intended to build market expectations.

7. Q2 delivery outlook | The first key number for Tesla’s rebound

Tesla is scheduled to report second-quarter deliveries on July 2, U.S. time.

Current Street consensus is approximately 406,000 units.

This implies year-over-year growth of about 5.7%.

Several major banks are more optimistic than consensus.

- Deutsche Bank: 416,000 units

- Barclays: 418,000 units

- Morgan Stanley: 413,000 units

One reason for the more constructive outlook is recovery in European EV demand.

- Deutsche Bank expects Tesla deliveries in Europe to rise by about 40% year over year.

- China is expected to rise by about 3%.

- North America is expected to decline by about 21%.

Even with weakness in North America, a strong European rebound could lift total deliveries.

8. Why Europe matters | Oil prices, inflation, and changes in consumer behavior

EV demand in Europe is rebounding due to energy prices and consumer sentiment.

The source text links rising oil-price concerns tied to conflict in Iran to renewed EV adoption in Europe.

Europe is highly sensitive to gasoline and diesel prices.

When energy prices rise, consumers reassess the economics of EV ownership.

Inflation pressure also encourages demand for vehicles with lower long-term operating costs.

- EV penetration in Europe was cited at 15.3% last year and around 20% recently.

- A recovery in the EV market would directly affect Tesla’s deliveries.

- Stronger European demand could improve Tesla’s earnings outlook.

Tesla’s share price at the $420 level will likely require more than sentiment alone.

Actual deliveries, margins, and robotaxi execution will need to support the valuation.

9. 2026 consensus remains conservative | A short-term rebound is not enough

Street consensus for Tesla’s 2026 deliveries is approximately 1.65 million units.

This implies only about 1% growth year over year.

The implication is clear.

The market is not yet re-rating Tesla as a rapidly expanding EV manufacturer.

Instead, investors are waiting to see whether robotaxi and autonomous driving can become the next growth drivers.

Even if second-quarter deliveries improve, the key question is whether the recovery extends into the third and fourth quarters.

The issue is whether this is a one-time rebound or the beginning of a broader EV demand recovery.

10. Cybercab’s real advantage | Vertical integration matters more than automation alone

Another important point emphasized by Moravy is vertical integration.

Tesla integrates raw materials, vehicle production, computing, software, charging infrastructure, and autonomous-driving data into one system.

This could create a major advantage in robotaxi operations.

- Tesla manufactures the vehicles directly.

- It develops the autonomous-driving software in-house.

- It is deeply involved in vehicle AI computers and chip design.

- It owns the Supercharger network.

- It can collect operational data directly.

While companies such as Uber, Waymo, Rivian, Zoox, Pony AI, Nuro, and Lucid each have strengths, few combine all these elements in one platform.

Tesla’s objective in robotaxi is not simply to sell vehicles but to control the cost structure of the mobility service itself.

11. What the Uber-Waymo partnership change means for Tesla

The source text also references the end of Uber and Waymo’s collaboration in Phoenix.

Uber is currently partnering with several autonomous-driving companies.

It has agreements with Rivian, Zoox, Pony AI, Nuro, Lucid, and others.

Some view Tesla’s absence from Uber partnerships as a negative.

However, Tesla may be unwilling to share revenue and control with a platform partner.

- Uber needs multiple partners because it lacks its own autonomous-driving technology.

- Tesla aims to control the vehicle, software, and platform itself.

- A partnership with Uber would require sharing platform fees and data control.

- Tesla’s goal is to operate its own robotaxi platform directly.

The outcome in robotaxi is likely to depend less on who launched the app first and more on who can deploy the most vehicles at the lowest cost and operate them reliably.

In that context, Tesla’s vertical integration could be a major advantage.

12. Will a version with a steering wheel exist? | The A-pillar offers a clue

Many investors expected a consumer version of Cybercab with a steering wheel.

However, the publicly shown vehicle architecture does not strongly support that view.

One notable feature is the thick A-pillar.

The A-pillar is the structural support on both sides of the windshield and is important for occupant protection in collisions and rollovers.

However, a thicker A-pillar can create a larger blind spot for the driver.

That would be a disadvantage in a vehicle meant to be driven manually.

For an autonomous vehicle, occupant protection and structural safety matter more than driver visibility.

- A thick A-pillar can be a drawback in a manually driven vehicle.

- In an autonomous vehicle, it can support a stronger safety structure.

- This may indicate that Cybercab was not designed for a steering-wheel-equipped version.

Cybercab appears to be designed as a mobility service vehicle rather than a car intended for manual driving.

13. Tesla is not the first company to build a steering-wheel-free vehicle | Scale is the difference

Steering-wheel-free autonomous vehicles are not unique to Tesla.

Waymo and Zoox have also introduced purpose-built autonomous models.

The difference lies in scale.

- Some autonomous-driving companies focus on limited-area, low-volume operations.

- Tesla appears to be preparing Cybercab for mass production.

- If the 90% automation figure is accurate, Tesla may have a major advantage in deployment speed.

Robotaxi success is not determined by technology alone.

The ability to produce vehicles quickly, cheaply, and in volume is critical.

If Tesla moves Cybercab into mass production, the competitive landscape could change quickly.

14. The key point missing from many reports | The true variable is unit economics, not regulation alone

Many reports focus on the absence of a steering wheel, the video release, and the share-price move.

However, the more important question is whether a robotaxi can be profitable on a unit basis.

The key issue is unit economics.

- How low is the cost of building one vehicle

- How many hours per day can one vehicle operate

- How low are charging and maintenance costs

- How well can insurance and accident risk be controlled

- How quickly can the service expand after regulatory approval

Tesla’s 90% automation rate and process simplification are directly linked to improving unit economics.

Lower vehicle costs and faster production can support lower fares.

Lower fares could make Tesla’s robotaxi more attractive than Uber for some users.

Tesla’s goal may ultimately be not just a better autonomous vehicle, but a mobility network with lower costs, wider deployment, and higher margins than Uber.

15. The biggest risk | Steering-wheel-free vehicles are not yet broadly permitted in the U.S.

If Tesla is preparing for mass Cybercab production, regulation is the biggest risk.

Steering-wheel-free vehicles are not yet free to operate nationwide in the United States.

They may be possible in Austin and certain test environments, but national expansion requires legal and safety approval.

- Federal and state autonomous-driving regulation

- Safety standards for vehicles without steering wheels or pedals

- Liability in the event of an accident

- Insurance pricing mechanisms

- City-by-city operating permits for robotaxi service

As a result, Tesla’s approach can be viewed either as bold preemptive investment or as a large bet that production will move ahead of regulation.

However, Tesla’s historical pattern has been consistent.

It pushes technology and production first, then pressures the market and regulators to catch up.

16. What investors should monitor at TSLA in the $420 range

At around $420, Tesla should not be viewed simply as a buy-or-sell decision.

This valuation may reflect both an automaker multiple and an AI/autonomous-platform multiple.

Investors should focus on the following key variables.

- Q2 deliveries: Whether Tesla exceeds the 406,000-unit consensus estimate.

- European EV demand: Whether the rebound is structural or temporary.

- Cybercab production announcement: Whether Tesla provides concrete scaling numbers around July 7.

- FSD performance and regulatory approval: Whether autonomous driving can move into robotaxi operations.

- Margins: Whether profitability can hold under EV price competition.

- Rate-cut expectations: Interest-rate conditions remain important for growth-stock valuation.

Tesla is no longer explained solely by vehicle sales.

It is now a composite growth story tied to EV demand, autonomy, robotaxi, AI computing, and energy infrastructure.

17. Conclusion | Tesla is signaling a production system, not just showing a Cybercab

This Cybercab video release should not be viewed as a simple promotional event.

Tesla’s official account and Elon Musk simultaneously released footage of a steering-wheel-free Cybercab driving on public roads.

Moravy then referred directly to the production line, burn-in testing, a 90%+ automation rate, and a reduction in process steps.

Taken together, the message appears to be:

Cybercab has moved beyond concept status and into production preparation.

Important challenges remain.

Regulatory approval, safety validation, city-by-city operating permits, robotaxi pricing, and actual consumer demand are all unresolved.

But Tesla’s effort to design Cybercab for mass production is highly significant.

In the robotaxi market, the eventual winner may not be the company with the most advanced technology, but the one that can deploy the most vehicles at the lowest cost with the highest reliability.

< Summary >

- Tesla and Elon Musk released footage of a steering-wheel-free, pedal-free Cybercab driving on public roads.

- VP Lars Moravy said the Cybercab production line is already running and automation exceeds 90%.

- The Cybercab process was described as being reduced from roughly 200 steps to 20–25 steps.

- Second-quarter deliveries are expected to come in above the Street consensus of 406,000 units.

- European EV demand recovery is a key factor supporting Tesla’s delivery rebound.

- Tesla’s main advantage is its vertical integration across vehicles, software, AI, and charging infrastructure.

- Changes in Uber-Waymo cooperation further highlight Tesla’s independent robotaxi strategy.

- The largest risks remain regulation for steering-wheel-free vehicles and robotaxi unit economics.

- At the TSLA $420 level, investors should monitor deliveries, Cybercab production updates, and autonomous-driving approvals.

[Related Articles…]

*Source: [ 오늘의 테슬라 뉴스 ]

– 테슬라 부사장이 직접 확인했다 — 사이버캡 자동화 90%, 이제 대량생산만 남았다? $420 지금 어떻게?

● Mid-Rate Shock

The End of the Low-Rate Era: The “Mid-Rate Era” Created by the End of Globalization and the New Order of Wealth

The most important point in this article is not simply that interest rates have risen.

The key issue is that the global economic structure that prevailed from 1980 to 2020 has ended, and the price of money is being reset at a higher level than in the past.

Accordingly, the central question for the economic outlook is not when policy rates will be cut, but whether rates can return to near-zero levels after easing.

De-globalization, supply-chain reorganization, rising U.S. Treasury yields, expanding government debt, persistent inflation, and AI-driven productivity competition are all interacting at once, and the survival strategies for corporations and households are changing accordingly.

The conclusion is clear: investment approaches designed for the low-rate era are losing relevance, while cash-flow-focused strategies suited to a mid-rate era are becoming more important.

1. From 1980 to 2020, the world operated in a low-rate globalization era

From 1980 to 2020, global economic activity was shaped by the strongest phase of globalization.

Major economies, including Korea, Japan, China, the United States, and Europe, opened markets and expanded trade.

Companies could source raw materials, components, and labor from the lowest-cost locations.

Korean firms no longer needed to produce every component domestically; if China could supply more cheaply, they sourced from China.

This structure exerted strong downward pressure on global prices.

When inflation is stable, central banks have less need to raise policy rates aggressively.

As a result, long-term interest-rate levels declined steadily.

In the 1970s and 1980s, deposit and lending rates above 10% were common.

But after the 2000s, low inflation and low growth drove rates down persistently.

Following the global financial crisis, the Federal Reserve and other major central banks maintained ultra-low rates and quantitative easing, supplying ample liquidity to markets.

This is the low-rate environment that became the baseline for investors.

2. Why the low-rate era ended: from globalization to de-globalization

The low-rate era ended not merely because inflation rose, but because the operating model of the global economy changed.

After the global financial crisis, globalization had already begun to slow.

This is often described as slowbalization.

The shift accelerated sharply after the Russia-Ukraine war in 2022.

The global economy is moving away from a pure lowest-cost sourcing model.

In strategic sectors such as security, energy, food, semiconductors, critical minerals, batteries, and defense, stability of supply has become more important than lowest price.

This is geoeconomic fragmentation.

As economics becomes intertwined with security, supply-chain restructuring is advancing.

For example, even if urea water could be imported most cheaply from China, excessive dependence on China creates national-security risk.

Accordingly, some production must be brought home or diversified across allied countries, even at higher cost.

From an economic perspective, this is a higher-cost structure.

De-globalization therefore acts as an inflationary force rather than a disinflationary one.

3. The core of the mid-rate era: rates are not just temporarily higher; the structural level is higher

A common question in markets is when the Federal Reserve will begin cutting rates.

Policy rate decisions at FOMC meetings are important for short-term financial markets.

However, the more important question is whether rate cuts can bring policy rates back to the ultra-low levels of the past.

The key issue in the mid-rate era is not the direction of rates, but their average level.

In the past, when growth weakened, central banks could cut rates toward zero and provide liquidity.

Going forward, inflationary pressure may not disappear easily.

Supply-chain realignment, energy security, defense spending, U.S.-China competition, Middle East conflict risk, and rising government debt all add cost pressure.

In such an environment, the neutral rate itself may rise above historical levels.

The neutral rate is the theoretical policy rate that neither stimulates nor restrains the economy.

If the neutral rate rises, it becomes difficult for central banks to return to the ultra-low rates of the past.

Accordingly, the key issue in rate forecasting is not whether cuts will occur, but where the new equilibrium rate will be.

4. Government debt and U.S. Treasury yields reinforce the mid-rate era

Government debt is a critical variable in explaining the mid-rate era.

The United States and other major economies expanded fiscal spending substantially after the pandemic.

Population aging, welfare spending, defense outlays, industrial policy, green investment, and semiconductor subsidies continue to increase fiscal needs.

Governments must either raise taxes or issue more debt.

However, tax increases are politically difficult.

As a result, debt issuance rises.

When Treasury supply increases, investors may demand higher yields.

This structurally pushes up U.S. Treasury rates.

When U.S. Treasury yields rise, the discount rate for global financial markets also rises.

Equities, real estate, bonds, emerging-market currencies, and corporate funding costs are all affected.

As long as the dollar’s reserve-currency status remains intact, U.S. yields will continue to serve as the reference point for global money pricing.

Therefore, Korean mortgage rates, corporate bond yields, real estate markets, and the won exchange rate remain linked to U.S. Treasury trends.

5. The impact on corporations: “growth” becomes less important than “interest expense”

In the low-rate era, borrowing to invest was relatively easy for corporations.

New businesses, capex, R&D, M&A, and overseas expansion could be funded at low borrowing costs.

In the mid-rate era, the burden of the same investment rises materially.

For example, if borrowing costs are 2%, an investment yielding 5% can still appear attractive.

But if borrowing costs are 6%, a 5% return is insufficient.

At that point, companies can no longer focus only on top-line growth.

Operating margin, cash flow, leverage, and interest coverage become more important.

Highly leveraged firms are especially vulnerable in a mid-rate environment.

By contrast, companies with strong cash positions, pricing power, and the ability to pass on higher costs are relatively better positioned.

Investors must assess not only whether a company is growing, but whether it can withstand a higher-rate environment.

6. The impact on households: debt becomes heavier, and spending becomes more cautious

The mid-rate era also imposes direct pressure on households.

Interest expenses on mortgages, consumer loans, jeonse-related loans, and student loans are heavier than in the past.

Decisions to borrow for housing, vehicles, education, or entrepreneurship become more difficult.

As interest burdens rise, households reduce consumption.

Lower consumption weakens corporate revenue.

When corporate revenue slows, employment and wages also come under pressure.

In this sense, the mid-rate era acts as a broad drag on economic momentum.

Not all households are affected equally.

Households with high debt are more exposed, while those with large cash holdings or stable interest income may be relatively better off.

Whereas debt-led asset accumulation was favorable in the low-rate era, debt management and cash-flow management are more important in the mid-rate era.

7. What many reports miss: the mid-rate era is an era of security costs

Many reports explain interest rates solely through inflation and central bank policy.

But the deeper issue is that the mid-rate era is an era of security costs.

In the globalization era, the cheapest supply chain was the optimal choice.

In the de-globalization era, the safest supply chain becomes the more important choice.

The problem is that safer supply chains are usually more expensive.

Diverting production concentrated in China to Korea, the United States, Japan, India, Vietnam, or Mexico raises costs.

Expanding LNG, nuclear, renewable, and strategic reserve capacity to reduce dependence on a single energy supplier also raises costs.

Subsidies to produce semiconductors and batteries domestically or within allied countries increase fiscal burdens.

Higher defense and cybersecurity spending follows the same pattern.

In other words, future inflation is likely to reflect not only demand overheating, but also the cost of securing strategic resilience.

This is a central feature of the mid-rate era.

8. Is AI the solution to the mid-rate era, or another cost burden?

AI is one of the most important variables in the mid-rate era.

If AI significantly lifts productivity, it can ease inflationary pressure and improve corporate profitability.

For example, if AI enhances software development, customer service, logistics optimization, manufacturing processes, financial analysis, and medical diagnostics, more output can be generated with the same labor and capital.

In that case, AI-driven productivity gains could help offset a high-cost environment.

However, AI is also a cost in the short term.

Data centers, semiconductors, power grids, cooling systems, cloud infrastructure, and cybersecurity require substantial capital.

When rates are high, financing such investment becomes more burdensome.

As a result, not all companies benefit equally from the AI trend.

Large technology firms and infrastructure companies with strong balance sheets may be advantaged, while AI startups with weak business models may face survival pressure in a high-rate setting.

AI therefore has a dual role: it may reduce the cost burden of the mid-rate era, but it also requires substantial upfront investment.

9. Investment strategy changes: the low-rate formula no longer works

In the low-rate era, assets with strong future growth were rewarded with high valuations.

Even if earnings were not yet visible, investors accepted high valuations if significant future growth was expected.

In the mid-rate era, however, the present value of future earnings declines.

The discount rate is higher.

As a result, growth stocks, unprofitable technology names, and long-duration project assets face a tougher valuation environment.

By contrast, companies that generate stable cash flow, pay dividends, and possess pricing power may attract more attention.

Bond investing also changes.

In the past, very low rates reduced the attractiveness of bonds, but in a mid-rate environment, high-quality and short-duration bonds may become more attractive.

Real estate must also rely less on leverage.

If rental yield is below borrowing cost, the investment case weakens.

Accordingly, investors should evaluate actual cash flow and interest expense before relying on asset-price appreciation.

10. Key indicators to watch

- U.S. policy rates and FOMC guidance

The key issue is not how quickly the Fed cuts rates, but what level it regards as the long-run appropriate rate. - 10-year U.S. Treasury yield

This serves as the benchmark discount rate for global asset prices and directly affects equities, real estate, and exchange rates. - Neutral rate estimates

If the neutral rate rises, the likelihood of a return to ultra-low rates declines, and the mid-rate era may persist. - Government debt and Treasury issuance

As fiscal expansion increases bond supply, upward pressure on yields may intensify. - Supply-chain reconfiguration speed

Faster de-risking, reshoring, and friend-shoring can increase cost pressures. - Inflation composition

It is necessary to distinguish demand-driven inflation from cost inflation linked to energy and supply chains. - AI productivity indicators

The extent to which AI improves corporate margins and labor productivity will shape medium- to long-term rates and growth.

11. Practical responses for individuals and companies

First, review debt structure.

High variable-rate exposure or short-maturity debt increases sensitivity to rate changes.

In the mid-rate era, the question is less whether borrowing is available and more whether it can be sustained.

Second, focus on cash flow.

Strategies based solely on asset-price appreciation are riskier.

Monthly interest expense, fixed costs, and net cash flow should come first.

Third, companies should reprioritize capital allocation.

Rather than pursuing all new businesses at once, capital should be concentrated in areas with clear profitability and productivity gains.

Fourth, AI adoption should be treated as a cost-reduction strategy.

If AI is viewed only as a trend, it becomes a cost; if it is tied to automation and productivity improvement, it becomes a defense mechanism in the mid-rate era.

Fifth, investors must calculate rate sensitivity.

Growth stocks, real estate, long-duration bonds, and highly leveraged companies are especially sensitive to rate changes.

By contrast, companies with strong cash flow and high-quality bonds may present opportunities in the mid-rate era.

12. Core conclusion: future wealth will come from the ability to withstand expensive money, not from cheap money

In the low-rate era, borrowing cheaply to buy assets was an effective strategy.

In the mid-rate era, borrowing costs are higher.

As financing costs rise, corporate investment decisions, household consumption decisions, and portfolio allocation must all change.

The key issue for the economic outlook is not being driven by short-term rate-cut headlines.

It is the structural shift toward de-globalization, supply-chain reorganization, rising government debt, and growing security costs.

In this environment, interest rates are likely to remain at a higher average level than in the past.

Accordingly, the appropriate strategy is no longer aggressive leverage suited to the low-rate era.

In the mid-rate era, cash flow, productivity, cost control, debt management, and AI adoption become the new competitive advantages.

< Summary >

From 1980 to 2020, globalization helped drive lower inflation and lower rates, creating a low-rate era.

But the Russia-Ukraine war, U.S.-China competition, de-globalization, and supply-chain restructuring are shifting the world economy toward a higher-cost structure.

Even if rates decline temporarily, returning to the ultra-low levels of the past may be difficult.

In the mid-rate era, borrowing costs will weigh more heavily on both corporations and households, and investment decisions will shift from growth expectations to cash flow and debt-servicing capacity.

AI may ease the burden of a high-cost environment by improving productivity, but it also requires substantial upfront investment.

The key strategy going forward is to reduce debt, strengthen cash flow, and improve productivity through AI in order to withstand the era of expensive money.

[Related Articles…]

- Mid-Rate Era Investment Strategy and Interest Rate Outlook

- AI Productivity Revolution and the Changing Global Economic Outlook

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 저금리 시대는 끝났다…이제 ‘중금리 시대’가 온다 #경읽남 #경제읽어주는남자 #경제전망 #북리뷰 #머니쇼크