● Trump Baby Boom, Robinhood, Micron, AI Stocks Surge

Trump’s Newborn Account Launch, and Why Robinhood, Micron, and AI Infrastructure Stocks Are Moving Together

The real story here is not simply a newborn subsidy.

The U.S. government has officially launched a policy that deposits $1,000 into accounts for newborns, while companies such as Micron, Dell, SpaceX, Nvidia, Intel, and IBM are being linked to the initiative through donations and sponsorships.

More importantly, the capital is not being held as cash. It is being routed into the U.S. equity market through Robinhood accounts and S&P 500 ETFs.

In other words, this policy combines welfare, market liquidity, election strategy, the semiconductor sector, AI infrastructure investment, and financial platform growth in a single framework.

As the second half of the year and the midterm election cycle approach, the Trump administration is likely to promote the program aggressively, and related companies may trade as both policy beneficiaries and political names.

1. What the Trump Newborn Account Is

The newborn account launched by the Trump administration is a long-term asset-building account for U.S. newborns born between 2025 and 2028.

The U.S. Treasury provides an initial $1,000 seed deposit per newborn.

That is roughly equivalent to KRW 1.5 million in Korean currency terms.

The funds are not distributed as cash but are managed in a long-term investment account.

The key feature is tax treatment.

Investment gains within the account may benefit from tax deferral, which can materially enhance long-term compounding.

President Trump has framed the policy as a way to instill ownership in America’s future rather than simply provide direct cash transfers.

2. The Structure in Simple Terms

-

Government seed funding

The Treasury provides $1,000 to newborns born between 2025 and 2028.

This amount is treated as baseline seed capital rather than part of a separate contribution cap.

-

Corporate donations

Companies such as Micron may contribute additional funds to newborn accounts.

In the source material, Micron is described as planning an additional $250 contribution per account.

As a result, newborn accounts may receive both government funding and corporate donations.

-

Parental contributions

Parents may contribute additional annual amounts.

The source material refers to annual contributions of around $5,000.

-

Employer matching

Employers may also provide matching contributions for employees’ children’s accounts.

For example, if a parent contributes $1,000, the company may match up to another $1,000.

This creates a structure in which government, parents, companies, and employers all contribute to the same account.

On the surface, this is a child savings policy. From a market perspective, it expands the long-term investment base of U.S. households.

3. Why the Policy Matters Politically

The Trump administration is likely to make strong use of the newborn account ahead of the midterm elections.

The reason is straightforward.

A message that “real money has been deposited into a child’s account” is highly tangible for voters.

It has a stronger immediate impact than tax cuts or deregulation.

In a high-inflation environment, a policy that creates a visible path to household asset formation has clear political value.

Trump has already emphasized the stock market, 401(k) accounts, stable energy prices, and tax cuts as evidence of economic performance.

Adding newborn accounts allows him to reinforce the frame of being a president who builds future wealth for American families.

This could further align market gains and household wealth creation with the campaign message.

4. Why Robinhood Is Considered the Main Beneficiary

Robinhood is the most directly exposed beneficiary in this initiative.

The reason is that the company is closely connected to the account-opening and custody infrastructure surrounding the newborn account program.

As accounts are created, government deposits are made, corporate donations are added, and assets are held, Robinhood may serve as a core platform.

The source material states that more than 6 million accounts have already been opened.

For Robinhood, this creates a long-duration customer lock-in effect starting from infancy.

Traditional banks and brokerages spend heavily to acquire teenagers and college students because of lifetime customer value.

Robinhood could establish that relationship from birth.

That represents a major expansion in customer lifetime value for a financial platform.

5. The CEO’s 60 Million User Opportunity

Robinhood’s CEO described the program as a 60 million-plus opportunity for new wealth creation.

At first glance, that may sound exaggerated, but the estimate is not limited to newborns in a single year.

The broader addressable market includes newborns, parents, family members, employers, and long-term account users.

The current U.S. stock ownership rate is described as approximately 65%.

Robinhood’s goal is to raise that figure above 90%.

From that perspective, the newborn account is not merely an account-opening event but part of a broader effort to structurally expand equity ownership in the United States.

6. Robinhood’s Other Growth Driver: AI Agent Trading

Robinhood is not relying only on the newborn account initiative.

A second major theme is AI agent trading.

Today, users still trade by opening a mobile app and executing orders manually. In the future, AI agents may execute trades according to user-defined conditions.

Robinhood is already preparing products and services that would allow AI agents to trade on behalf of users.

If this trend develops, the customer base of brokerage firms will expand from humans to AI agents.

Trading activity may also become less constrained by conventional market hours.

As crypto, tokenized assets, and 24-hour markets expand, fee-based revenue opportunities for financial platforms could increase.

In that sense, Robinhood is building a model that captures both newborn customers at the base and AI agent trading at the top.

This expands both the customer lifecycle and the trading participant base.

7. Where the Funds Are Invested

The default investment vehicle referenced for the newborn account is State Street’s S&P 500 ETF.

The source material identifies SPYM as the default option.

SPYM is described as a low-cost product from State Street, the same firm behind the SPY ETF.

The low expense ratio makes it suitable for long-term investing.

Once the government’s $1,000 deposit is made, the money may be automatically allocated to an S&P 500 ETF.

In that scenario, State Street benefits from direct asset inflows and brand visibility.

Because fees are very low, the immediate earnings impact may be limited, but the long-term asset accumulation effect is more important.

8. Potential Follow-On Benefits for BlackRock and Vanguard

BlackRock’s IVV and Vanguard’s VTI may later be added as alternative options.

IVV is an S&P 500 ETF.

VTI is a broad U.S. total market ETF.

If the policy objective is long-term compounding, low-cost ETFs tracking the S&P 500 or the full U.S. market are natural choices.

As a result, not only Robinhood but also State Street, BlackRock, and Vanguard may benefit structurally.

9. Why Micron’s Contribution Matters

Micron is one of the most symbolic corporate participants in the newborn account flow.

The source material states that Micron announced a donation of approximately $250 million.

It also references an additional $250 contribution per newborn account.

President Trump publicly praised Micron’s decision and referenced the company’s stock price gains.

The market sees this as significant because it ties into the administration’s industrial policy.

Micron is an important memory chip company in the U.S. semiconductor revival strategy.

As AI servers and data centers expand, demand for HBM, DRAM, and NAND continues to rise.

Micron therefore connects to semiconductor policy, AI infrastructure spending, and the Trump administration’s manufacturing revival narrative.

10. Why the Market Interprets This as a “Donate and Be Supported” Dynamic

The issue is sensitive because corporate donations may be interpreted as policy signaling rather than simple philanthropy.

Companies donate to a high-priority initiative of the Trump administration.

The president publicly praises those companies.

Those firms may then expect a more favorable environment in regulation, subsidies, government contracts, and industrial policy.

This should not be taken as proof of a direct quid pro quo.

However, investors will inevitably assess which companies are likely to gain from proximity to the Trump administration.

For that reason, participating companies could see higher volatility alongside the midterm election theme.

11. Why SpaceX and Musk Have Re-Entered Focus

Trump said in a CNBC interview that he expects Musk to contribute through SpaceX.

Although the wording suggests expectation rather than demand, the market may interpret it as a form of public pressure.

Trump often uses public statements to force counterparties to move first.

SpaceX is closely tied to space, defense, satellite internet, and government contracts.

For Musk, it is difficult to ignore the relationship with the Trump administration entirely.

Given SpaceX’s IPO expectations, regulatory exposure, and government contract potential, the political relationship matters.

Tesla may also attract renewed attention in the second half of the year, as it has historically traded as a Trump-linked political name.

12. Why Treasury Allowing Publicly Traded Stock Donations Matters

The Trump administration announced that it would allow donations of publicly traded stocks to help fund the newborn account program.

At face value, this opens a channel for wealthy donors to support children’s futures through equity donations.

From a market standpoint, the more important implication is that companies can participate in the policy not only with cash but also with stock.

If expanded, this could channel equity, donations, and corporate ownership into policy platforms.

Politically, it allows the administration to frame the initiative as companies investing in the future of American children.

For companies, it provides another avenue to strengthen their relationship with the government.

13. Companies Linked to the Newborn Account Initiative

The main companies referenced in the source material are as follows.

-

Robinhood

Described as a core beneficiary through account opening, platform infrastructure, custody, and long-term customer acquisition.

-

Micron

Highlighted through its donation and its role in U.S. semiconductor policy.

-

Dell

Referenced as an early corporate donor and linked to AI servers and infrastructure spending.

-

SpaceX and Tesla

Relevant through the possibility of Musk participation and the company’s relationship with the Trump administration.

-

IBM

Connected to quantum computing and government technology strategy.

-

Intel

Central to U.S. semiconductor manufacturing revival and foundry strategy.

-

Nvidia

A core name in AI infrastructure and data center capital spending.

-

JPMorgan and Wells Fargo

Referenced as financial-sector participants.

-

Coinbase, Visa, and Mastercard

Potentially linked to digital finance, payments, and tokenized asset flows.

14. Why OpenAI and Anthropic Equity Donations Matter

Separately from the newborn account program, the possible donation of equity stakes by AI companies has attracted attention.

The source material cites a Financial Times report stating that OpenAI may consider donating 5% equity to the Trump administration.

The significance lies in the fact that this is not a cash sponsorship but an equity transfer.

OpenAI and Anthropic depend heavily on their relationship with the government in areas such as regulation, power infrastructure, data center approvals, and oversight of big tech.

For the Trump administration, receiving equity in AI companies creates an opportunity to frame AI growth as something that benefits the public.

For the companies, it may improve the odds of regulatory flexibility, listing support, infrastructure expansion, and policy protection.

This makes the structure potentially attractive to both sides.

15. Equity Donation Candidates in Prediction Markets

The source material says prediction markets currently assign the highest probability to OpenAI as a potential equity donor.

The probability is described at around 70%.

Other names mentioned include GlobalFoundries, Palantir, Anduril, TSMC, Boeing, and Nvidia.

These companies share a common feature: strong exposure to government policy.

GlobalFoundries is linked to U.S. foundry strategy.

Palantir is strong in government data analytics and defense AI.

Anduril is a next-generation defense and drone company.

TSMC is tied to the U.S. semiconductor supply chain.

Boeing is closely linked to aviation and defense policy.

Nvidia sits at the center of AI infrastructure, export controls, and data center growth.

16. The Most Important Point That Is Often Missed

The core issue is not who donated, but how money and power are being connected through new channels.

Most coverage focuses only on the newborn subsidy, corporate donations, or Robinhood as the beneficiary.

But the larger point is that this policy may become a new model for U.S. industrial policy.

The government does not need to rely solely on tax-funded redistribution.

Companies participate in the policy through cash or equity.

Households see actual money enter accounts.

Politicians gain support.

Companies expect regulatory advantages and policy support.

Financial platforms gain new customers and assets under management.

Asset managers receive ETF inflows.

If this structure expands, future U.S. economic policy may evolve from simple tax cuts or subsidies into a hybrid model that combines government, corporations, and financial platforms.

For investors, the key question is not only which stock may rise on donation headlines, but where policy capital accumulates and who captures recurring revenue.

From that perspective, Robinhood, asset managers, payment networks, and AI infrastructure companies may matter more than the donor list itself.

17. Why the Trump Administration Cares About the Stock Market

Trump frequently treats the stock market as a core measure of economic performance.

He often presents the S&P 500, Nasdaq, and Dow Jones rallies as evidence of economic strength.

He also uses rising 401(k) balances as proof of middle-class wealth creation.

Tax cuts are described as putting more money into Americans’ pockets.

Lower oil and gasoline prices are tied to inflation control and election strategy.

As the midterm elections approach, the administration is unlikely to ignore a sharp decline in equities.

The government cannot guarantee higher stock prices, of course.

But policy messaging, tax cuts, deregulation, energy-price pressure, and corporate investment announcements can still be used to support sentiment.

18. Other Events to Watch in the Second Half of the Year

-

SK hynix U.S. listing-related developments

The source material notes the possibility of a U.S. listing and large capital raising for SK hynix.

As memory semiconductors remain central to the AI server cycle, global investor attention could increase.

However, large capital raising can also absorb market liquidity, so both upside and pressure should be considered.

-

Samsung Electronics preliminary earnings

Samsung’s results are an important indicator of memory market conditions and AI semiconductor demand.

The outcome could affect Micron, SK hynix, and the broader Nvidia supply chain.

-

Space-related stock catalysts

If expectations around SpaceX increase, space-sector listed names may attract short-term interest.

Since SpaceX is private, investors may need to look for indirect exposure through listed peers.

-

Sun Valley Conference

This gathering of major tech CEOs and business leaders may produce announcements on deals or strategic partnerships.

If executives from OpenAI, Anthropic, or Samsung attend, there may be signals related to AI infrastructure, memory, and data center investment.

19. Key Beneficiary Groups for Investors

-

1st priority: Financial platforms

Robinhood appears to have the most direct benefit through account opening, custody, and long-term customer acquisition.

-

2nd priority: Asset managers

State Street, BlackRock, and Vanguard may benefit from ETF inflows linked to S&P 500 and total market products.

-

3rd priority: Policy-linked companies

Micron, Dell, IBM, Intel, Nvidia, SpaceX, and Tesla may gain attention through their policy connections.

-

4th priority: AI infrastructure firms

If OpenAI and Anthropic equity donation discussions advance, data center, power, semiconductor, and server names may benefit from improved sentiment.

-

5th priority: Payments and digital asset companies

Coinbase, Visa, and Mastercard may gain from the expansion of tokenized assets and 24-hour financial trading.

20. Risks Should Also Be Considered

First, much of the policy optimism may already be reflected in valuations.

Stocks such as Robinhood and Micron, which have already rallied, may face short-term profit-taking.

Second, it remains unclear how much corporate donations will contribute to actual earnings.

Donation announcements generate publicity, but they do not automatically translate into revenue or profit growth.

Third, election-themed stocks tend to be volatile.

Stock prices can swing rapidly based on Trump’s approval ratings, congressional expectations, and policy statements.

Fourth, AI infrastructure spending depends on interest-rate expectations, power costs, data center regulation, and the pace of big tech investment.

Fifth, in a market near record highs, even positive news may have limited impact on share prices.

< Summary >

The Trump newborn account is a long-term investment account for U.S. newborns born between 2025 and 2028, funded with an initial $1,000 government contribution.

Corporate donations, parental contributions, and employer matching can turn it into a broader household asset-building policy.

Robinhood is positioned as a core beneficiary through account creation, custody, and long-term customer acquisition.

State Street, BlackRock, and Vanguard may benefit from ETF inflows.

Micron, Dell, IBM, Intel, Nvidia, SpaceX, and Tesla are drawing attention through their policy links to the Trump administration.

The possibility of equity donations from OpenAI and Anthropic adds another dimension tied to AI infrastructure policy and regulatory expectations.

The central issue is not simply the donor list, but how policy capital accumulates and who captures recurring value.

In the second half of the year, U.S. equities may continue to be influenced by the midterm election cycle, semiconductors, AI infrastructure, interest-rate expectations, and inflation trends.

[Related Articles…]

- Trump Policy Beneficiaries and U.S. Equity Market Outlook

- AI Infrastructure Spending Cycle and Semiconductor Leaders

*Source: [ 소수몽키 ]

– 트럼프 계좌에 기부해야 밀어준다? 지금부터 주목해야 할 주식들의 공통점

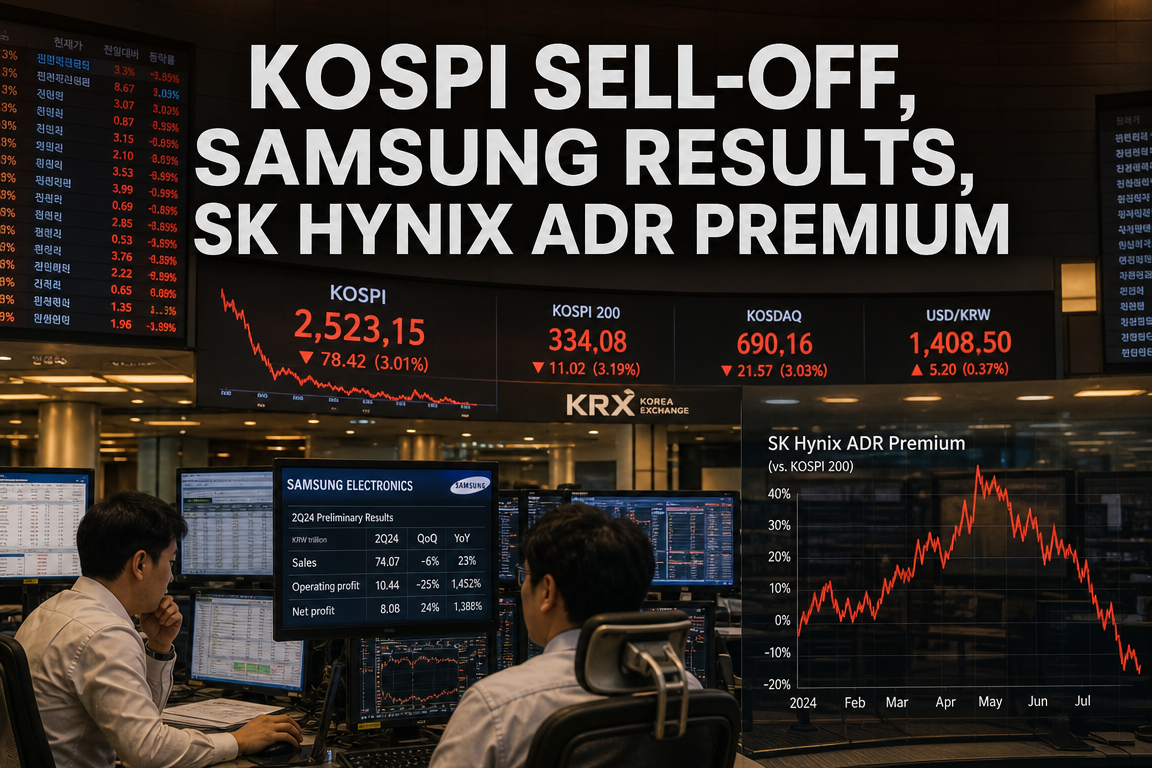

● Samsung Shock, Kospi Slumps, ETF Chaos, Foreign Selloff, Pension Rebalance

Samsung Electronics’ Record Results and the Real Reason the KOSPI Weakened: Leverage ETFs, National Pension Rebalancing, and Foreign Selling

Today’s market issue was not simply why Samsung Electronics fell despite strong earnings.

The key point is that a surprise earnings beat at Samsung Electronics, a correction in semiconductor stocks, a broader KOSPI decline, leverage ETF flows, National Pension rebalancing, and foreign selling pressure converged at the same time, making the market appear to lose normal price-discovery function.

This correction is difficult to explain through corporate fundamentals or the global growth outlook alone.

That Samsung Electronics fell sharply after reporting record-level earnings suggests that the Korean equity market is currently reacting more to flows and policy variables than to earnings.

Based on the original live discussion, the following summarizes why today’s market was viewed as an unusual correction.

1. Today’s market can be summarized in one sentence: a flow shock, not an earnings-driven market

Samsung Electronics reported results that exceeded market expectations.

The earnings release reflected improvement in the semiconductor cycle, AI server demand, HBM expectations, and a rebound in memory prices.

However, the market reaction was the opposite.

Even after the earnings announcement, the KOSPI underwent a sharp correction, and semiconductor stocks faced broader pressure.

Under normal conditions, strong earnings should support share prices.

Today’s market moved differently.

This suggests that the decline should be interpreted less as an earnings disappointment and more as a correction driven by market structure and policy-related factors.

2. Why Samsung Electronics’ results were regarded as “record-level”

The original discussion emphasized the scale of Samsung Electronics’ results.

Although the automated subtitle slightly distorted some figures, the core message was that Samsung Electronics significantly exceeded consensus expectations.

There was also an interpretation that operating profit could have been even higher if performance-based compensation provisions had not been reflected.

In other words, the company’s underlying operating strength may have been stronger than the reported operating profit suggests.

Samsung Electronics matters not only as a single company but also as a benchmark for Korean exports, the semiconductor cycle, and the broader KOSPI outlook.

As one of the largest constituents of the Korean market, alongside SK hynix, Samsung Electronics has substantial influence on index direction.

Therefore, strong earnings would normally be read as evidence that Korea’s export engine and corporate profit cycle remain intact.

The fact that the market still fell sharply implies that non-fundamental factors were dominant.

3. First factor: June and July were already expected to be volatile

The live discussion described 2025 and 2026 as a liquidity-driven market cycle, while emphasizing that June and July would likely be volatile months.

A liquidity-driven market refers to a period in which expectations of lower rates, global capital rotation, and risk appetite support equities.

Even within such a cycle, significant corrections can occur.

June and July are typically sensitive to U.S. rate uncertainty, geopolitical risk, political events, and policy variables.

In such an environment, even strong earnings can fail to stabilize stock prices in the short term.

Still, the scale of today’s move went beyond ordinary volatility.

4. Second factor: expectations of a possible U.S. rate hike pressured the market

The original discussion did not suggest that the Federal Reserve had actually raised rates, but it noted that markets became more concerned about the possibility of another hike.

What matters is not whether a rate hike occurred, but whether investors began to price in that risk.

Financial markets react to expectations before they react to outcomes.

Rising expectations of a U.S. rate hike can strengthen the dollar, trigger foreign outflows, and pressure growth stock valuations.

Semiconductor and AI-related stocks are especially sensitive because their valuations incorporate substantial future growth.

The discussion also suggested that this rate-related anxiety could ease after July.

In that view, the concern was more likely to remain an expectation shock than to become an actual policy shift.

5. Third factor: leverage ETFs amplified market volatility

One of the most important themes in this correction was leverage ETFs.

Leverage ETFs are designed to track two times or more of the underlying index’s movement.

For example, if the KOSPI 200 rises 1%, a leverage ETF may rise by roughly 2%.

Conversely, a 1% decline in the index can translate into a much larger loss.

The issue is that these products amplify buying in rising markets and intensify selling pressure in falling markets.

As a result, greater leverage ETF participation tends to make the market move faster in both directions.

The original discussion used unusually strong language to describe the market as resembling a casino.

That reflects concern that short-term positioning and leveraged speculation have begun to dominate market direction.

6. Fourth factor: National Pension rebalancing added structural supply pressure

Another key variable was National Pension rebalancing.

The National Pension Service adjusts allocations across domestic equities, overseas equities, and bonds according to preset portfolio weights.

If the domestic equity market rises sharply over a short period, domestic equity exposure can exceed the target allocation.

In that case, the fund may mechanically reduce domestic equity holdings.

This creates selling pressure in the market.

When the KOSPI rises quickly and rebalancing follows, large-cap stocks can face notable supply pressure.

Names such as Samsung Electronics, SK hynix, Hyundai Motor, and financial stocks are especially vulnerable because of their large index weights.

The discussion argued that leverage ETFs and National Pension rebalancing together contributed to the abnormal market move.

7. Fifth factor: foreign selling and a lack of market support

Foreign investor flows remain a major variable in the Korean market.

Foreign investors typically hold large-cap stocks and have a strong impact on semiconductor shares.

Even strong earnings from Samsung Electronics cannot prevent short-term weakness if foreign investors are net sellers.

Foreign investors consider not only earnings but also exchange rates, U.S. rates, dollar liquidity, global risk appetite, MSCI weighting, and geopolitical risk.

As a result, they may reduce exposure to Korea even when corporate results remain strong.

Today’s market was driven more by flows than by earnings.

When foreign selling, institutional rebalancing, retail leverage, and ETF activity move in the same direction, the market can fall sharply in a short period.

8. Why the move was described as difficult to explain under normal logic

Under ordinary market logic, strong earnings should support stock prices.

Of course, share prices are never determined by earnings alone.

However, when a market leader such as Samsung Electronics posts record results and the KOSPI still corrects sharply, investors naturally see a disconnect.

The original discussion described this as an unusual correction.

In other words, the move appeared less like a fundamentals-based correction and more like a price distortion caused by policy, flows, and leveraged trading.

In such a market, short-term forecasting becomes difficult.

Even if prices should normalize after an excessive decline, policy variables and mechanical trading can prevent that adjustment from happening smoothly.

9. Outlook for the next session: normalization is possible, but volatility remains

The discussion suggested that a normalizing move could appear in the next session if today’s decline was indeed excessive.

In that sense, a technical rebound after an abnormal correction is possible.

However, this view depends on several conditions.

If policy variables, National Pension rebalancing, leverage ETF flows, and foreign selling remain strong, the market could again move in a distorted manner.

Accordingly, near-term rebound potential exists, but June and July should still be treated as a volatile period.

In particular, semiconductor earnings were strong in the second quarter, but the market may begin to focus on slower growth rates in the second half.

That does not mean earnings are weak; it means the pace of growth may moderate.

Equity markets often respond more to the direction of earnings growth than to absolute earnings levels.

10. The deeper issue: the market is losing its price-discovery function

The most important point is not that Samsung Electronics declined for one day.

The real issue is that the Korean equity market appears to be moving more strongly in response to flow mechanisms and policy events than to corporate value.

Leverage ETFs amplify market direction.

National Pension rebalancing creates mechanical pressure on large-cap stocks.

Foreign selling reacts quickly to rates, currency moves, and global liquidity.

When these forces act together, even a strong fundamental event such as Samsung Electronics’ earnings may be unable to support the market.

This is the central takeaway from today’s correction.

Many reports focus only on the fact that Samsung Electronics fell despite strong earnings.

What matters more is why earnings failed to support prices.

The answer is that the market structure has become highly sensitive to flows, policy, and mechanical trading.

11. An Adam Smith perspective: who should set prices?

The original discussion referenced Adam Smith’s concept of the “invisible hand.”

Prices should be determined naturally through market participants’ transactions, not by artificial direction from the government or a specific institution.

This does not mean government intervention is unnecessary.

Governments should address market failures, prevent unfair trading, and strengthen investor protection.

However, attempts to steer prices in a specific direction can create larger distortions later.

The key question in this market is whether prices were formed naturally based on corporate value.

If the move reflected Samsung Electronics’ earnings, the semiconductor cycle, and the global outlook, it would be understandable.

But if prices were driven sharply by leverage ETFs, National Pension rebalancing, policy variables, and foreign selling, investor confidence in the market weakens.

12. Is a country truly wealthy if its people remain poor?

The discussion also highlighted another Adam Smith quote: a country cannot be called truly wealthy if most of its citizens are poor and living in hardship.

This frames the market move not only as a stock-price event but also as an issue of household wealth.

Korea may report strong exports, a better trade balance, and record earnings from major companies.

However, if individual investors’ portfolios are damaged and household wealth declines, the economy cannot be considered fully healthy.

The stock market is the core of the capital market.

A healthy stock market supports corporate financing, household asset formation, and the transmission of economic growth to families.

If the market becomes dominated by volatility and loses trust, long-term investment culture becomes harder to sustain.

13. Key checkpoints for investors

-

First, monitor foreign flows together with Samsung Electronics’ earnings.

Strong results may still coincide with short-term weakness if foreign investors are selling.

-

Second, identify whether National Pension rebalancing is underway.

During such periods, the KOSPI can become more sensitive to flows than to fundamentals.

-

Third, track leverage ETF trading volume and retail concentration.

Overheated leverage products can exaggerate both gains and losses.

-

Fourth, monitor whether U.S. rate hike expectations are easing.

If those expectations fade, growth stocks and semiconductor shares may stabilize in the short term.

-

Fifth, watch for any slowdown in third-quarter semiconductor earnings growth.

The direction of growth may matter more than the strong second-quarter base.

14. AI and semiconductors: why this correction is not necessarily the end of the trend

The live discussion also previewed additional coverage on AI, HBM, gold, and crypto as part of a subscriber milestone event.

That is not just a programming note; it also points to the next major themes in the market.

AI depends heavily on semiconductors.

HBM, GPUs, data centers, power infrastructure, and cloud investment remain central to the medium- and long-term outlook for Korean semiconductor companies such as Samsung Electronics and SK hynix.

Semiconductor stocks can certainly weaken in the short term.

However, if the AI investment cycle continues, semiconductors should remain a key thematic area.

The issue is not whether AI and semiconductors are over; it is that even strong industries must be evaluated alongside price and flows.

15. Conclusion: strong companies and strong markets are not the same thing

Samsung Electronics posting strong earnings and the KOSPI showing short-term weakness are separate matters.

Even strong companies can see their share prices fall when flows deteriorate.

Even strong industries can face valuation pressure when rate concerns rise.

Even positive macro data can fail to improve household sentiment if asset markets are unstable.

Today’s correction reflected all three points.

Accordingly, what is needed now is neither panic selling nor unconditional optimism.

Investors should separate flows, policy, rates, earnings growth, and foreign selling pressures.

During volatile periods such as June and July, caution is warranted for high-risk products such as leverage ETFs.

The market may normalize in the short term, but structural volatility has not yet disappeared.

< Summary >

Samsung Electronics reported very strong earnings, but the KOSPI corrected sharply.

This decline is best explained by a flow shock driven by leverage ETFs, National Pension rebalancing, foreign selling, and U.S. rate uncertainty rather than by weak fundamentals.

June and July remain volatile even within a broader liquidity-driven cycle.

Today’s move appears more like an abnormal correction shaped by flows and policy than a fundamental repricing.

Near-term normalization is possible, but third-quarter semiconductor growth and foreign flows still need to be monitored.

The main issue is that the Korean equity market is increasingly reacting to leverage and mechanical rebalancing rather than corporate value.

[Related Articles…]

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– [🚨50만 기념 LIVE🚨] 삼성전자 ��대급 실적에도 주식시장 대조정된 ‘진짜이유’ [즉시분석]