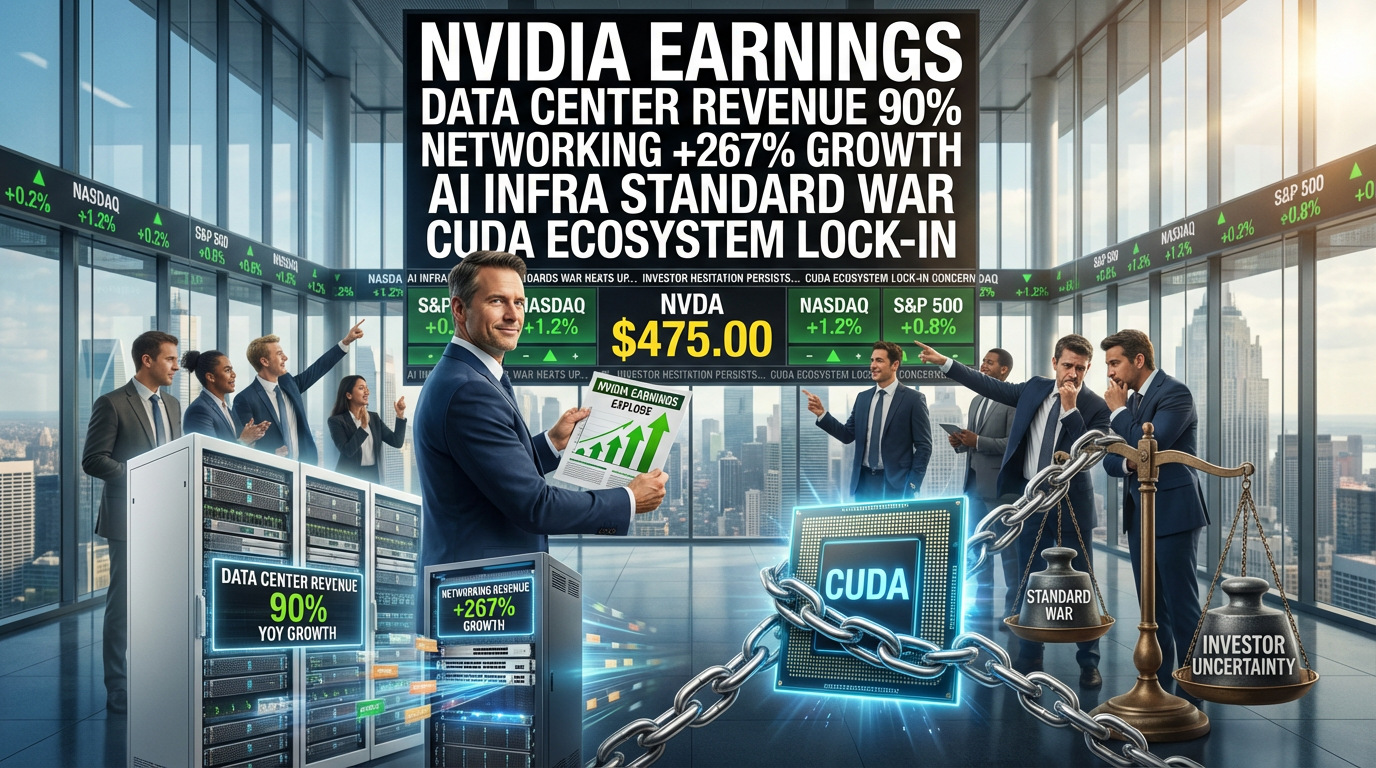

● Nvidia Earnings Blowout, Data Center Takeover, Networking Surge, 75 Percent Margins, Stock Stalls

NVIDIA earnings, the real reason “they’re great but the stock is ambiguous”: the era of 90% data center + 267% networking growth + what a 75% margin means

This post includes all of these core points.

① Why NVIDIA’s earnings should not end with “flawlessly great”

② The structural shift where data center revenue share surpassed 90% (gaming GPUs effectively becoming a side business)

③ Why a 267% surge in networking revenue will reshape the future AI infrastructure landscape

④ Why a gross margin in the 75% range is proof of “cost pass-through + ecosystem lock-in”

⑤ The hidden variables that keep the market from immediately pushing the stock up (positioning, expectations, and timing gaps in supply/CapEx)

1) Today’s headline (news-style summary)

– NVIDIA beat expectations on both EPS and revenue.

– EPS came in at 1.62, above consensus (1.53).

– Revenue was $68.1 billion, beating consensus by about 5–6%.

– Data center revenue was $62.3 billion, effectively confirming “NVIDIA = a data center company.”

– A structure where 90%+ of total revenue comes from the data center segment.

– Next quarter’s guidance is even more formidable: $76.4–$79.5 billion.

– More than 7% above the market estimate (about $72.7 billion).

– Gross margin (Non-GAAP) recorded 75.2%.

– A number that directly overturns concerns about margin deceleration.

– Networking revenue +267% year over year.

– Confirms the trend that the next bottleneck in AI infrastructure is not “chips,” but “networks.”

2) If you look only at the numbers, it’s “perfect”: what was so good, and by how much

2-1. What the EPS/revenue surprise means

– EPS of 1.62 is not just a “blowout quarter,” but can be interpreted as a signal that cost structure and pricing power improved together.

– Revenue of $68.1 billion matters because this is the phase where you evaluate whether growth holds up even after scale has expanded.

2-2. Growth rate: a pace rarely seen in mega-caps

– Year-over-year revenue growth is mentioned in the 70% range (about 73% in the original source).

– Usually, as a company gets larger, the “law of large numbers” kicks in and growth slows, but NVIDIA is pushing through that phase instead.

– This also means it’s not merely an AI boom; it suggests AI infrastructure spending (CapEx) is being “concentrated” into a specific vendor.

3) The core of the structural change: what the era of 90% data center means

3-1. From a “gaming GPU company” to a company “selling an AI infrastructure OS”

– Data center revenue of $62.3 billion is a message in and of itself.

– NVIDIA is now a company whose success is determined more by data center/cloud (hyperscaler) supply than by consumer GPUs like RTX.

3-2. (Original-source interpretation) A nuance that gaming GPU supply could shrink

– The original source contains phrasing along the lines of “we’ll make only the money-making data center products now,” but it’s hard to flatly conclude this as “stopping gaming.”

– Still, the market is already feeling that the short-term priority is the data center.

– As a result, the consumer GPU lineup may see higher “demand/supply volatility,” which could show up as a negative experience (pricing/supply) in the gaming market.

4) Networking up 267%: the “next megatrend” people miss

4-1. In AI data centers, the bottleneck is now the network

– Performance does not increase linearly just by plugging in more GPUs.

– As training/inference scales up, inter-GPU communication (scale-out), storage/memory movement, and latency become bottlenecks.

– That’s why networking (switches, interconnects, optical communications, etc.) becomes the “floor that determines performance.”

4-2. Why 10% of the cost can determine 30% of the performance

– The original source explains that “the network is 10% of total cost, but removing the bottleneck improves performance by 30%.”

– This leads to a very straightforward ROI calculation for companies.

– There comes a moment when improving the network to raise GPU utilization is cheaper than buying more GPUs.

4-3. Why CPO (optical communications/packaging) is heating up

– Large-scale clusters quickly hit the “limits of copper” due to power/heat/distance issues.

– So efforts to bring optical-based connections closer (such as CPO) keep growing, and

– NVIDIA’s surge in networking revenue is a moment that confirms this direction in “earnings.”

5) 75.2% gross margin: evidence that “cost pass-through” is possible

5-1. Margin held up despite concerns about memory/cost increases

– The market has been worried about “HBM and other memory price increases → GPU cost increases → margin declines.”

– But Non-GAAP GM of 75.2% suppresses that concern for now.

5-2. Why pass-through was possible: ecosystem lock-in + lack of substitutes

– NVIDIA doesn’t just sell chips; it has a powerful software ecosystem centered on CUDA.

– Customers (big tech) maintain a premium they are willing to pay for “performance/developer productivity/time-to-market.”

– This is a representative case of margins holding up even during inflationary periods, and it is also why the company receives a premium in global financial markets.

6) Translating Jensen Huang’s remarks into an “investment perspective”

6-1. “Agentic AI survival game” = the nature of compute demand changes

– Agentic AI is not simple Q&A; it repeatedly cycles through goal setting → planning → execution → verification.

– That is, token usage and repeated calls are likely to increase.

– This is not just a fad; it increases the likelihood that inference demand will grow larger over the long term.

6-2. “Lower cost per token” = it becomes a hardware efficiency race

– As models improve, it may feel like software will solve everything, but

– In reality, cost structure becomes critical, and “cost per token” becomes competitiveness itself for companies.

– When NVIDIA emphasizes efficiency, it ultimately means it is directly tied to the profitability of cloud operators.

6-3. The implications of the “A-series sold out” remark

– It can be read as meaning that demand is strong not only for the latest chips (e.g., Blackwell family) but also for the previous generation.

– This can be interpreted in two ways.

1) AI demand is not only seeking “the latest,” but is in a phase of absorbing everything that’s “available right now”

2) While supply is tight, it’s an environment where average selling price (ASP) and margin defense are easier

6-4. “Securing production capacity for several quarters” = a declaration of supply-chain advantage

– The more bottlenecks there are in TSMC/packaging/memory and so on, the more the side that pre-secures capacity wins.

– Jensen’s message is meant to build trust that “we have volume locked in stably.”

7) But why was the stock reaction an “ambiguous rise” rather than a “surge”?

7-1. Expectations were already high

– NVIDIA is a stock where strong earnings have become the “default,” so even when there is a surprise, the market demands an even bigger catalyst.

7-2. Positioning/profit-taking: earnings releases are flow events

– Even if earnings are strong, “sell the news” can appear right after the release.

– This is especially true when large-cap tech has already risen a lot.

7-3. The real checkpoint is the regular session reaction + next-day flows

– More important than the after-hours reaction is what price levels institutional money supports the next day.

8) The most important point I see, but one that other news talks about less

8-1. The essence of this earnings report is not “GPU unit sales” but the “AI infrastructure standards war”

– The market focuses on revenue/stock price, but the bigger picture is “whether data center design becomes fixed around NVIDIA.”

– The fact that networking revenue also surged indicates growing influence not as a simple component supplier but at the architecture level.

8-2. A 75% margin is closer to “deepening lock-in” than “intensifying competition”

– In a phase where competitors are catching up, margins usually get shaken first.

– But if margins hold, it means customers cannot easily switch, and

– It shows that the AI semiconductor market is not a simple spec war but an “ecosystem war.”

8-3. When networks heat up, the “AI investment cycle” gets longer

– If the cycle is just buying GPUs, replacement/expansion can end as a one-off, but

– If networks, optics, packaging, and power all grow together, the entire data center becomes a long-term project.

– This flow can become a basis for AI infrastructure investment to remain relatively resilient even during economic slowdown phases.

9) Checklist going forward (next-quarter watch points)

– Whether data center revenue growth is “maintaining high growth” or transitioning to a “gradual slowdown”

– The quality of networking growth: one-off (a big deal) vs. structural (product mix/standards adoption)

– Whether the 75% gross margin range is maintained (despite rising memory/packaging costs)

– Supply: the stronger the demand, the more “how much more can be made” determines the top end of results

– Whether there are signs that big tech CapEx direction (cloud/data center investment) is wobbling

NVIDIA beat expectations on EPS, revenue, and guidance, and data center revenue has fully settled into a structure exceeding 90% of total revenue.

In particular, 267% growth in networking revenue is a key signal showing that the next bottleneck in AI infrastructure is moving to the network.

Non-GAAP gross margin of 75.2% proves that cost pass-through and ecosystem lock-in are being maintained despite cost pressures.

The stock not reacting immediately is largely due to expectations and flow-event effects, and the regular session/next-day institutional flows are key.

[Related posts…]

- After NVIDIA earnings: the AI infrastructure investment map reshaped by data centers and networking

- The AI data center bottleneck is networking: why optical communications and CPO are rapidly emerging

*Source: [ 월텍남 – 월스트리트 테크남 ]

– “정말 이해가 안가네요…”