● Micron Shock, Memory Supremacy, AI Boom

Micron’s Earnings Surprise Signals a Structural Shift: Memory Semiconductors Are Moving from a “Price Cycle Industry” to an “AI Infrastructure Contract Industry”

The key takeaway from Micron’s latest earnings is not simply that results were strong.

The core message is that memory semiconductor companies are no longer passive price takers. They are increasingly setting supply terms for AI data center customers.

Micron’s implied price floor and long-term contract structure suggest materially stronger profitability than in prior peak cycles, which has also raised the possibility of a revaluation for Samsung Electronics and SK Hynix.

In the near term, this issue may affect the KOSPI outlook as well as Samsung Electronics and SK Hynix share prices. Over the medium to long term, it may influence AI semiconductors, HBM, data center investment, and the broader global economic outlook.

1. The Most Material Change in the Memory Industry Today

The central point is that the market has begun to reassess the memory semiconductor industry after Micron’s earnings release.

Historically, memory semiconductors were a classic cyclical industry.

Prices rose when demand was strong and collapsed when supply expanded.

As a result, companies such as Samsung Electronics, SK Hynix, and Micron struggled to receive high valuation multiples even when earnings were strong.

Investors often assumed that current profitability would not last.

That long-standing framework is now being challenged by Micron’s earnings and contract structure.

Memory prices are increasingly being shaped not only by the market, but also by supply-side pricing floors and customer acceptance of those terms.

2. The Most Important Part of Micron’s Results Is Not the Numbers, but the Contract Terms

The main point of Micron’s report is not the headline earnings figures, but the contract structure behind them.

Customers are competing to secure memory supply, and some appear willing to commit upfront or make strong purchase commitments to obtain allocation.

This is unusual in the memory industry.

In the past, customers pressed for lower prices and memory vendors had to compete aggressively on price.

Today, the dynamic has shifted toward customers seeking guaranteed supply.

AI servers, GPU clusters, and data center expansion have made high-performance memory a core requirement for competitiveness.

The real significance of Micron’s earnings is that bargaining power in memory has shifted from customers to suppliers.

3. Why Have Memory Companies Suddenly Become the Stronger Party?

① AI data centers are driving a sharp increase in memory demand

AI does not run on GPUs alone.

Without sufficient memory bandwidth and speed, even powerful GPUs cannot operate efficiently.

As generative AI, large language models, and inference workloads expand, demand for HBM and high-performance DRAM is rising sharply.

In AI semiconductors, memory has become a critical infrastructure component rather than a simple part.

② HBM supply cannot be expanded quickly

HBM is not as easy to scale as standard DRAM.

It requires advanced stacking, packaging, yield stabilization, and customer qualification.

In other words, supply cannot be increased materially just because customers want more.

This supply constraint is shifting pricing power toward memory suppliers.

③ For customers, supply shortage is a larger risk than higher prices

For major technology companies building AI data centers, the greater risk is not paying a slightly higher memory price.

The bigger risk is failing to secure supply on time and delaying server deployment.

When trillions of won are being invested in AI infrastructure, the cost of launch delays is far greater than paying a few percentage points more for memory.

That is why customers are increasingly willing to accept higher prices in exchange for long-term supply contracts.

4. What It Really Means to Say “Memory Is No Longer a Cyclical Industry”

Taken literally, that statement may sound overstated.

Memory semiconductors are still affected by economic cycles, inventory cycles, and capital expenditure cycles.

However, the important change is that the nature of the cycle is evolving.

In the past, the industry was centered on commodity DRAM and NAND.

When supply increased, prices fell sharply and vendors often suffered losses.

Today, the key demand driver is AI data center memory.

HBM, high-bandwidth DRAM, and high-capacity server memory depend on customer qualification and long-term contracts.

This suggests a move away from daily market price volatility toward a structure with more stable pricing and volume over a given period.

More accurately, the entire memory industry has not fully escaped cyclicality. Rather, the high-performance AI memory segment is being re-rated as a structural growth area.

5. Why Micron’s Price Floor Matters

One of the most important points in the original analysis is Micron’s implied price floor.

A price floor is not merely a pricing policy.

It is a mechanism that improves earnings stability.

In the past, lower memory prices could rapidly erode profitability.

If contracts now include a threshold below which supply will not be sold, revenue and operating margin visibility improves materially.

The original text argues that margins at this price floor could exceed Micron’s previous peak-cycle profitability.

If that interpretation is correct, the market can no longer treat Micron purely as a traditional cyclical stock.

If operating margins can remain above 50% on a more stable basis, valuation frameworks could change significantly.

6. More Important Than Micron Are Samsung Electronics and SK Hynix

Micron is one of the three major global memory companies.

However, from a Korean market perspective, the implications for Samsung Electronics and SK Hynix are more important.

The key question raised in the original text is whether Samsung Electronics or SK Hynix would be negotiating worse terms than Micron if Micron was able to secure such contracts.

That question is highly relevant.

① SK Hynix is a primary beneficiary of the HBM market

SK Hynix is regarded as highly competitive in HBM.

In the AI GPU ecosystem, HBM supply capability is a critical competitive advantage.

If customers continue to accept long-term contracts and price premiums, SK Hynix’s earnings outlook could improve beyond current expectations.

This would support a re-rating of SK Hynix as a core AI infrastructure company rather than merely a cyclical semiconductor name.

② Samsung Electronics is positioned for both recovery and revaluation

Samsung Electronics has a broad memory portfolio.

It covers DRAM, NAND, server memory, and next-generation HBM.

At the same time, the market has had mixed expectations regarding its HBM competitiveness and qualification speed.

However, if pricing power improves across the memory market, Samsung Electronics could also benefit significantly.

In particular, stronger commodity DRAM pricing combined with a rising mix of high-performance memory could accelerate earnings recovery faster than the market currently expects.

③ Micron’s earnings may be a leading indicator for Korean semiconductor stocks

Although Micron is a U.S. company, its earnings serve as a barometer for the global memory cycle.

When Micron reports strong results and favorable contract conditions, investors naturally reassess Samsung Electronics and SK Hynix.

For that reason, Micron’s earnings surprise is not just a U.S. semiconductor story. It is directly relevant to the KOSPI outlook.

7. Impact on the KOSPI: Semiconductor Concentration May Increase Further

Samsung Electronics and SK Hynix have significant weight in the Korean equity market.

When these two names move sharply, the KOSPI index is materially affected.

The original text also points to the possibility of strong opening gains for Samsung Electronics and SK Hynix.

If that trend continues, the main driver of KOSPI upside is likely to be semiconductors once again.

Foreign investors typically view the Korean market through the lens of the semiconductor cycle.

If Micron’s earnings strengthen expectations for a global memory supercycle, foreign inflows into Korean semiconductor large caps could increase.

That said, after a sharp near-term rally, profit-taking remains a risk. Investors should therefore monitor earnings estimate revisions and the durability of long-term contract structures.

8. A Key Point Often Missed by Other Coverage: The Valuation Framework for Memory Companies May Be Changing

Many reports reduce the story to “Micron posted strong results” or “Samsung Electronics and SK Hynix will benefit.”

The more important issue is the change in the valuation framework.

Historically, memory companies received low multiples even when earnings were strong.

The reason was simple.

The market believed those earnings would not be sustainable.

But if long-term contracts, price floors, and customer competition for supply become entrenched, that logic weakens.

If earnings become more stable, the market may assign higher multiples to memory companies.

In other words, the case for upside in Samsung Electronics and SK Hynix is not only stronger earnings, but also higher quality earnings.

That is the most important investment implication of Micron’s latest report.

9. What This Means for the Global Economic Outlook

Rising memory prices are not only an issue for semiconductor companies.

They also affect AI data center investment costs, cloud capex, server pricing, and power infrastructure demand.

As major technology companies continue increasing AI investment, semiconductor demand should remain firm.

At the same time, higher prices for high-performance memory may increase cost pressure on AI service providers.

As a result, the global economic outlook now reflects both productivity gains from AI investment and rising cost pressure.

This trend is likely to affect semiconductors, power networks, cooling systems, data center REITs, and cloud service providers across the ecosystem.

10. Key Indicators Investors Should Monitor Now

① Duration and pricing terms of HBM supply contracts

The first thing to monitor is whether HBM contracts are short-term or long-term.

The longer the contract duration, the higher the earnings visibility.

If contracts include price floors or prepayment terms, cash flow could also improve.

② Operating margin outlook for Samsung Electronics and SK Hynix

The key issue is operating margin.

More important than revenue growth is the pace at which high-margin products increase as a share of sales.

As the mix shifts toward HBM and server DRAM, overall profitability can improve.

③ Continuation of AI data center investment

The main driver of memory demand is AI data center spending.

Investors should track whether capital expenditure plans from Microsoft, Google, Amazon, and Meta remain intact.

If AI investment slows, expectations for memory demand may be revised downward.

④ Recovery in commodity DRAM and NAND prices

HBM alone does not fully explain the memory cycle.

For diversified manufacturers such as Samsung Electronics, the price trend for commodity DRAM and NAND also matters.

The key question is whether AI demand lifts server memory pricing and normalizes inventory levels in conventional memory as well.

⑤ Foreign flows and semiconductor weight in the KOSPI

Foreign investor flows are highly important in the Korean market.

If global investors begin to recognize a memory supercycle, semiconductor large caps could gain more weight in the KOSPI.

In that case, the KOSPI outlook itself may be revised upward.

11. Risks Must Also Be Considered

Strong news should always be evaluated together with risk factors.

The first risk is supply expansion.

When prices rise, companies eventually consider expanding capacity.

Excess supply could again pressure prices.

The second risk is a slowdown in AI investment.

If major technology companies begin questioning the return on AI spending, data center investment could decelerate.

The third risk is technology competition.

In the HBM market, customer qualification, yield, and packaging competition could lead to uneven beneficiaries.

The fourth risk is that much of the good news may already be reflected in share prices.

If Samsung Electronics and SK Hynix have already priced in strong expectations, volatility may remain elevated around earnings announcements.

12. Conclusion: This Micron Result Signals an Industry Structure Shift, Not Just a Better Cycle

This event should not be viewed only as a strong earnings print from Micron.

The more important issue is that pricing power in memory semiconductors is changing.

As AI data center demand rises, HBM supply remains constrained, and customers compete for long-term allocation, the bargaining power of memory suppliers is increasing sharply.

If that trend continues, Samsung Electronics and SK Hynix may be re-rated not as classic cyclical stocks, but as core AI infrastructure companies.

The key question going forward is whether memory companies can turn this upswing into a durable structural shift through long-term contracts and higher-value products.

If they can, Korean semiconductor stocks and the KOSPI may enter a significantly stronger revaluation phase.

< Summary >

Micron’s earnings are significant not only because of stronger numbers, but because they indicate a shift in bargaining power within the memory semiconductor industry.

AI data centers and HBM demand are rising sharply, and customers are increasingly accepting long-term contracts and higher prices to secure supply.

This supports greater earnings stability for memory companies and increases the possibility of a valuation re-rating for Samsung Electronics and SK Hynix.

If price floors and high-margin contract structures are sustained, the memory industry will be harder to classify as a purely cyclical business.

At the same time, investors should monitor supply expansion, a potential slowdown in AI investment, technology competition, and valuation already priced into shares.

[Related Articles…]

*Source: [ 내일은 투자왕 – 김단테 ]

– 메모리는 더 이상 사이클 산업이 아닙니다.

● Dollar Bubble, US Decline, China Alarm

Why Does the United States Keep Printing Money? Fraying Dollar Hegemony and the Recurrent Bubble Cycle Seen by China

The core issue here is not simply that the United States prints a large amount of money.

The key questions are why the U.S. economy repeatedly restores financial markets through dollar liquidity during crises,

why U.S. equities recover to new highs even when the real economy weakens,

and why Chinese think tanks view this structure as central to a “U.S. collapse scenario.”

Three points are especially important.

First, dollar hegemony is a source of U.S. power, but it also amplifies internal imbalances.

Second, the combination of Wall Street, the Federal Reserve, and fiscal policy has created a global financial system that repeatedly cycles through bubbles and busts.

Third, China interprets this gap as a sign of weakening U.S. hegemony, while U.S.-China competition has expanded beyond trade into financial and technological dominance.

1. Why Are Asset Markets So Volatile Now?

Equities have recently shown sharp rallies followed by abrupt declines, reflecting a high-volatility market environment.

At the surface, headlines about conflict in the Middle East, rate hike concerns, inflation risks, and slowing growth appear to drive markets.

At a deeper level, the central dynamic is the repeated cycle of bubbles and busts.

The quantity of assets does not change significantly, while the amount of money continues to expand.

The number of shares, apartments, gold reserves, and Bitcoin issuance is limited.

By contrast, dollars and other currencies are expanded aggressively during crises.

As money supply rises, the value of money declines and asset prices rise in relative terms.

This can be understood as debasement, or currency value dilution.

The problem is that assets rise on liquidity, but correct sharply when fear returns.

Geopolitical risk, inflation reacceleration, higher rates, banking stress, and debt concerns can quickly weaken sentiment.

In effect, capital markets operate on a structure in which liquidity creates bubbles and fear bursts them.

When fear subsides, liquidity again lifts markets.

2. China’s View of the U.S. Collapse Scenario Centers on Wall Street

The referenced book analyzes U.S. economic weaknesses from the perspective of a Chinese think tank.

Its notable feature is that it does not frame U.S.-China tensions solely as trade or military competition.

Instead, it identifies Wall Street-centered finance as one of the important sources of U.S. decline.

In the past, U.S.-China relations were relatively clear.

China supplied production capacity, while the United States supplied consumer demand.

China grew as the world’s factory, and the United States sustained a consumption-led economy by importing low-cost goods.

Both countries benefited from this structure.

However, the Chinese analysis argues that the gains did not accrue evenly across the U.S. population.

In particular, it views Wall Street financial institutions as the primary beneficiaries of globalization, rather than U.S. workers or manufacturers.

The text also notes that, even before the 2007 subprime mortgage crisis, financial firms on Wall Street accounted for a very large share of total U.S. corporate profits.

This symbolized the shift of the U.S. economy from manufacturing toward finance.

3. From “What Is Good for GM Is Good for America” to “What Is Good for Wall Street Is Good for America”

Before the 1970s, the United States was the world’s largest manufacturing power.

At that time, the growth of industrial giants such as General Motors was seen as synonymous with the growth of the U.S. economy.

The phrase “What is good for GM is good for America” reflected this view.

From the 1980s onward, the center of gravity in the U.S. economy shifted rapidly toward finance.

Finance became more influential than manufacturing, and capital markets and financial products began to function as the core engine of the economy.

In this process, Wall Street evolved from a market participant into a structural power center influencing policy and politics.

Chinese analysts view this as a structural vulnerability in the U.S. economy.

That said, any reference to specific ethnic groups as the hidden force behind financial power should be treated with caution.

In modern economic analysis, the critical issue is not ethnicity, but how financial capital is embedded in political and policy structures.

The real question is not who belongs to which group, but how financial power has been institutionalized.

4. How Does Wall Street Influence U.S. Policy?

The text identifies three channels through which Wall Street influences U.S. politics and policy.

First, political funding.

Presidential, Senate, House, and other elections require large sums of money.

The financial sector can influence policy decisions through donations and lobbying.

As this structure strengthens, market stability becomes not just an economic issue, but a political priority.

Second, personnel networks.

Wall Street alumni often move into government, the Treasury, the White House, regulatory agencies, and the Federal Reserve ecosystem.

The revolving door between finance and public office is persistent.

This increases the likelihood that the interests of the financial industry are reflected in policy.

Third, systemic risk.

When large financial institutions fail, the impact is not limited to one company.

Banks, insurers, bonds, derivatives, pension funds, and corporate financing can all be affected in sequence.

For this reason, governments and the Fed are often compelled to support financial institutions during crises.

This is the essence of the “too big to fail” structure.

5. Why Does the Fed Have to Inject Liquidity in Every Crisis?

When U.S. financial markets weaken, the Fed responds with large-scale liquidity injections.

Quantitative easing after the 2008 global financial crisis is the leading example.

A similar response occurred during the COVID-19 crisis.

The Chinese analysis is sharply critical of this pattern.

Its argument is that financial institutions create excessive risk, the government and central bank rescue the system when the bubble bursts, and society ultimately bears the cost.

In this process, Wall Street recovers, asset prices rebound, and equities move toward new highs.

However, workers, the middle class, and lower-income households face inflation and higher living costs more directly.

In other words, money creation is highly effective at stabilizing financial markets, but it can widen wealth inequality.

Those who own equities, property, gold, or Bitcoin benefit from liquidity.

Those dependent on cash and wages bear the burden of currency depreciation.

6. The Gap Between Wall Street and Main Street

A recurring concept in the U.S. economy is the gap between Wall Street and Main Street.

Wall Street refers to financial markets and capital markets.

Main Street refers to the real economy centered on businesses, workers, households, and consumers.

During the COVID-19 crisis, the real economy suffered a severe shock.

Unemployment rose, consumption weakened, and business activity stalled.

Yet U.S. equities rebounded quickly after the initial collapse and later entered a strong advance.

This was not primarily because the real economy improved, but because massive liquidity flowed into financial assets.

Chinese analysts view this as one of the clearest contradictions in the U.S. economy.

If the real economy weakens while financial markets strengthen, confidence in dollar hegemony could gradually erode.

7. The Real Power of Dollar Hegemony Is the Ability to Expand Supply Without Limit

The U.S. dollar is the world’s reserve currency.

It dominates international trade, oil pricing, foreign exchange reserves, and global financial transactions.

This structure gives the United States a major advantage.

When crises emerge, the U.S. can issue dollars to stabilize financial markets.

It can also expand fiscal spending through Treasury issuance.

Global investors still regard U.S. Treasuries as safe assets.

However, this very advantage can create long-term problems.

Continued expansion of dollar supply weakens purchasing power.

This increases global inflationary pressure and exposes emerging markets to currency instability and capital outflows.

When the United States expands liquidity, the effects are not limited to the U.S.

The entire world that uses dollars absorbs the impact.

This is both the strength of dollar hegemony and the reason resistance to it is growing.

8. Why Do Bubbles and Busts Recur?

Asset markets are highly sensitive to liquidity.

When money supply rises, investors prefer assets over cash.

Capital flows into equities, property, gold, commodities, and cryptocurrencies.

When fear returns, investors again prefer cash.

Conflict, recession, rate hikes, bank failures, and inflation shocks can trigger sharp declines in risk assets.

But as crises deepen, governments and central banks inject more money.

Markets then recover.

This repetition creates a long-term upward bias in capital markets.

The key point is not that a market which has risen substantially must inevitably fall.

In a system with continuous dollar liquidity, further upside remains possible.

That said, rising prices do not automatically justify buying.

It is essential to distinguish between gains driven by earnings growth, liquidity, or policy expectations.

9. Fiscal Policy Is Another Channel for Liquidity Creation

Central banks are not the only institutions that inject money into the market.

Fiscal policy is also a powerful liquidity channel.

Defense spending, energy transition investment, infrastructure programs, semiconductor subsidies, and supply chain reshoring budgets all inject capital into the economy.

When the U.S. government issues debt and deploys large-scale fiscal spending, the funds flow into corporate revenue, employment, investment, and financial markets.

As U.S.-China competition intensifies, the United States is allocating substantial fiscal resources to semiconductors, AI, batteries, defense, and energy security.

This is not merely industrial policy; it is also a strategy to defend technological and supply chain dominance.

When monetary and fiscal policy operate together, global financial markets can shift back into a liquidity-driven regime.

This is one reason equities can remain resilient even when the real economy is under pressure.

10. Why Does China See This as a Signal of U.S. Decline?

From China’s perspective, the United States has externalized the costs of its financial and dollar-based dominance onto the global economy.

When the U.S. expands dollar supply, the effects are transmitted through global prices, exchange rates, and capital flows.

China views this as a structural weakness of the U.S.-centered world order.

Within the United States, wealth inequality widens, the middle class weakens, and the manufacturing base erodes.

Externally, de-dollarization efforts gradually emerge as countries seek to reduce dependence on the dollar.

A sudden collapse of dollar hegemony is unlikely in the near term.

There is still no alternative currency with comparable market depth, institutional trust, rule-of-law credibility, military backing, and network effects.

What China focuses on is not an abrupt collapse, but a slow fracture.

Each round of crisis-driven liquidity support raises questions about the dollar system.

As these questions accumulate, they may eventually reshape the international order over the long term.

11. U.S.-China Competition Is Now a Contest in Finance, Technology, and Supply Chains

The U.S.-China rivalry has moved beyond tariffs.

It now includes decoupling, deglobalization, semiconductor export controls, rare earth controls, and competition in advanced AI chips.

The United States seeks to preserve both dollar hegemony and technological leadership.

China is challenging the U.S.-led order through manufacturing capacity, its domestic market, rare earths, batteries, electric vehicles, and AI application ecosystems.

The key point is that finance and technology are inseparable.

AI, semiconductors, data centers, power grids, and robotics require massive capital investment.

Technological leadership therefore depends on the financial system and capital formation capacity.

The United States uses its global capital markets and the dollar as strategic advantages.

China responds through state-led industrial policy and supply chain control.

This competition is likely to remain one of the most important variables in the global economic outlook.

12. The Most Important Point Often Missed by Other Media

Many reports stop at statements such as “the U.S. prints too much money,” “dollar hegemony is weakening,” or “China is catching up with the U.S.”

But the real issue is different.

The key question is not the volume of dollar issuance, but where that liquidity flows.

If dollar liquidity is directed toward productivity-enhancing investment, it can support long-term growth.

If it is allocated to AI infrastructure, semiconductor fabs, energy transition, education, and research and development, it can improve U.S. competitiveness.

By contrast, if liquidity only inflates financial asset prices, it increases bubbles and inequality.

Equity and property prices rise, while wages and productivity fail to keep pace.

In that case, the economy may appear strong on the surface, but internal frictions deepen.

The central question for the U.S. future is not how much money is printed.

It is whether the money goes into productivity or into bubbles.

From this perspective, the AI investment boom should be assessed carefully.

If AI raises enterprise productivity, lowers costs, and generates new revenue, it represents structural growth.

If share prices rise only on expectations and earnings do not follow, it may become another liquidity-driven bubble.

13. Key Checkpoints for Investors

First, separate the real economy from capital markets.

A weak economy does not necessarily mean equities must fall.

With strong liquidity, equities can rise even amid economic slowing.

Second, distinguish between types of fear.

Geopolitical fear, rate fear, inflation fear, and credit stress affect markets differently.

It is important to assess whether the shock is temporary or systemic.

Third, monitor the direction of dollar liquidity.

Fed policy, U.S. fiscal spending, Treasury issuance, and bank lending conditions all affect asset prices.

Fourth, recognize that different asset classes benefit at different stages.

At some times gold is strongest; at others, U.S. equities lead.

Bitcoin or commodities may lead in other phases.

The key is that not all assets move at the same pace.

Fifth, the next front in U.S.-China competition is AI and semiconductors.

Technological leadership is economic leadership, and economic leadership feeds back into financial dominance.

AI chips, data center power, cloud infrastructure, and robotics automation are likely to remain central to future capital flows.

14. China’s Debt Problem Is the Next Key Variable

The latter part of the source text turns to the Chinese economy.

China’s debt problem has been a recurring issue for more than 15 years.

Local government debt, distressed property developers, shadow banking, youth unemployment, and weak domestic demand are among the main risks.

However, China’s internal assessment may differ from Western crisis narratives.

China is likely to argue that state-led financial controls, a high savings rate, a state-owned banking system, and policy intervention capacity allow it to manage debt risks.

The next focus should therefore be the simultaneous evolution of U.S. dollar-system frictions and China’s ability to manage its debt burden.

If the United States fails to resolve its financial imbalances while China contains debt risk, the balance of power could shift.

Conversely, if China’s debt problems intensify while the United States succeeds in AI-driven productivity gains, the U.S.-centered order may remain intact for longer.

15. Conclusion: The United States Can Survive by Printing Money, But That Same Money Can Weaken It

The reason the United States keeps printing money is straightforward.

It must stabilize the financial system during crises, prevent recession, and preserve global leadership.

However, the side effects are increasingly significant.

Asset prices rise, but inequality widens.

Financial markets remain strong, but the gap with the real economy deepens.

The dollar remains dominant, but de-dollarization continues to gain attention.

The Chinese collapse scenario is less a prediction of imminent U.S. failure than an analysis of internal fractures in the U.S. system.

In particular, Wall Street-centered financial capitalism, unlimited dollar creation, asset bubbles, and the widening gap with the real economy are likely to remain central themes in understanding global markets.

For investors and companies, the key issue is not simply the direction of equities.

It is where dollar liquidity is flowing,

whether AI and semiconductor investment translates into productivity gains,

how U.S.-China competition affects supply chains and capital markets,

and where the strengths and weaknesses of the U.S. economy are appearing at the same time.

< Summary >

Volatility in U.S. asset markets reflects a recurring cycle of liquidity-driven bubbles and fear-driven corrections.

Chinese think tanks identify Wall Street-centered finance as one of the key sources of U.S. decline.

The Fed and the U.S. government have repeatedly stabilized financial markets through liquidity and fiscal expansion during crises.

However, this has widened the gap between the real economy and capital markets, increased asset inequality, and intensified inflationary pressure.

Dollar hegemony remains strong, but unlimited dollar creation may create long-term credibility frictions.

The main variables for the global outlook are dollar liquidity, AI productivity, semiconductor leadership, U.S.-China supply chain competition, and China’s debt management capacity.

[Related Articles…]

- Dollar Hegemony and Global Financial Market Outlook

- AI Semiconductor Competition and U.S.-China Technology Rivalry

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– 미국은 왜 계속 돈을 찍을까? 중국이 분석한 달러 패권의 끝 | 김광석의 북리뷰 | 중국이 분석한 미국 침몰 시나리오 [2편]

● Tesla Shock, 16GW Power Play

Beyond the Autopilot lawsuit: Why Tesla quietly introduced a 16GW U.S. virtual power plant

On a day when Tesla shares fluctuated around $375, the market’s headline focus was on the Autopilot fatal-accident lawsuit.

The more significant development was elsewhere.

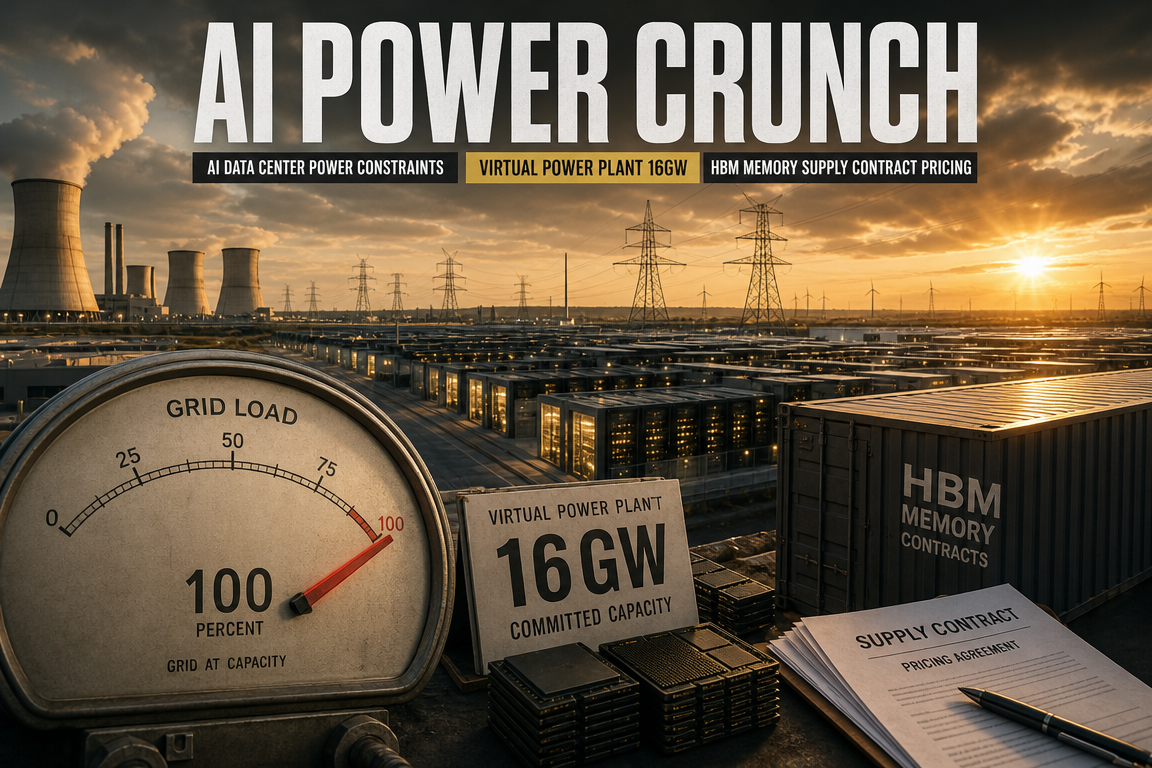

Tesla announced that it will work with Sunrun and Renew Home to build a 16GW distributed virtual power plant, the largest of its kind in U.S. history.

This is not simply an expansion of Tesla’s energy business. It signals a potential re-rating of Tesla as an energy infrastructure company positioned to address power demand from AI data centers.

Today’s key points are threefold.

First, why Tesla Energy announced a 16GW virtual power plant now.

Second, the significance of the Cybertruck receiving the top safety rating in the U.S. pickup segment.

Third, how the Texas Autopilot lawsuit could affect autonomy and robotaxi plans in practice.

1. Market overview: Tesla declined, while technology stocks consolidated

Tesla closed at $375.53, down 1.59%.

The S&P 500 fell 0.09%, and the Nasdaq declined 0.43%, indicating a broader pause in technology shares.

SpaceX-related pricing was cited at 154.54, down 1.01%.

Sentiment shifted somewhat after the close.

Micron Technology reported record quarterly results, and semiconductor-related stocks rebounded sharply in after-hours trading.

This matters because AI memory demand is being confirmed by actual corporate earnings, which in turn implies rapid growth in AI data center power demand.

Accordingly, Tesla’s energy announcement should be viewed together with semiconductor trends, AI data centers, and power grid investment.

2. Tesla Q2 delivery outlook: the first short-term driver

Tesla’s Q2 vehicle delivery report is expected in about 9 days.

Wall Street consensus is cited at approximately 397,500 units.

That would represent an increase from the prior quarter and an improvement year over year.

EV demand in Europe is recovering, and May retail sales in China were reported to have rebounded 22.5%.

In the near term, Tesla shares are likely to remain highly sensitive to whether deliveries exceed or fall short of expectations.

Over the medium to long term, however, the more important shift is in Tesla Energy.

3. Key development: Tesla announces a 16GW virtual power plant in the U.S.

Tesla announced plans to build the largest distributed virtual power plant in U.S. history together with Sunrun and Renew Home.

The target capacity exceeds 16GW.

For context, the Hanul nuclear plant in South Korea is estimated at roughly 6GW of installed capacity.

16GW is therefore about 2.7 times Hanul’s capacity.

In practical terms, this means creating power management capacity comparable to nearly three large Korean nuclear plants by connecting batteries and smart devices already deployed in U.S. homes.

By comparison, a large single battery storage facility in operation in the U.S. is cited at around 0.4GW, making 16GW roughly 40 times larger.

This is not just an ESS project; it is an energy infrastructure strategy that could reshape grid operations.

4. Why VPP matters

A virtual power plant, or VPP, does not mean building one large physical plant.

It uses software to connect distributed resources such as home batteries, solar panels, electric vehicles, and smart thermostats, operating them as a single power asset.

This project does not require new land or a new large-scale power plant.

It links Tesla Powerwall systems, Sunrun’s home battery network, and Renew Home’s roughly 8 million smart thermostats into one network.

Future Tesla EV V2G functionality could also make vehicle batteries part of the grid.

The core advantage is that the project leverages existing assets.

While new power plant construction can take more than 10 years, VPPs can respond much faster by coordinating already-installed equipment through software.

The model can deliver power to AI data centers during peak demand and recharge batteries during periods of lower demand, helping stabilize the grid.

5. Why now: AI data centers are pressuring the grid

The timing of this announcement is important.

As reflected in Micron’s results, AI memory demand remains strong.

More AI chips and servers inevitably require more AI data centers.

The challenge is electricity.

AI data centers consume far more power than conventional commercial facilities.

Regions with concentrated data center development may face grid constraints, transmission bottlenecks, and rising electricity costs at the same time.

Tesla’s 16GW virtual power plant strategy appears aimed directly at this bottleneck.

As the AI sector expands, electricity becomes not just a cost item but a core input.

Against that backdrop, Tesla is positioning itself not simply as an automaker, but as a power platform for the AI era.

6. Tesla Energy profitability: higher margins than automotive

Tesla should not be viewed solely as an automaker.

The company can be broadly divided into automotive, energy, and AI software.

Among these, energy is currently the fastest-growing segment.

Based on the source material, Tesla Energy battery deployments were cited at 46.7GWh, up about 50% year over year.

More important is profitability.

Tesla Energy’s gross margin was cited at around 39.5%.

By contrast, automotive margins were cited at roughly 12% to 13%.

On a simple comparison, the energy business carries about three times the margin of automotive.

This matters because it could alter Tesla’s valuation framework.

If Tesla is treated only as an automaker, its valuation may appear difficult to justify.

If it is viewed as an energy infrastructure, AI software, and grid platform company, the valuation model changes materially.

7. Roles of Sunrun, Renew Home, and Tesla

The partnership assigns different roles to the three companies.

Sunrun will contribute its home battery and solar customer base.

Renew Home will manage smart thermostats and household energy control networks.

Tesla will provide core battery capacity through Powerwall, energy software, and potentially EV V2G functionality.

Tesla’s advantage lies in its battery capacity and software orchestration.

A VPP is not simply an installation business.

It requires real-time control of millions of distributed assets and optimization based on power demand and pricing.

Tesla’s combination of EVs, batteries, energy storage systems, and AI software is a key differentiator here.

8. The Nefpower contract broadens Tesla’s energy opportunity

The source also referenced analysis from Nasdaq.com.

The core message was that bearish views on Tesla may be overstated.

In particular, Tesla’s battery storage contract with Nefpower in Italy and the U.K. was mentioned.

The construction value of that contract was estimated at $4 billion to $5 billion, with long-term revenue potential cited at more than $15 billion.

Combined with the 16GW U.S. virtual power plant partnership, Tesla Energy appears increasingly tied to a global grid investment cycle rather than a one-off project pipeline.

Even if EV growth moderates, energy storage and virtual power plants may continue to expand at a faster pace.

9. The project will not be reflected in this quarter’s earnings immediately

For investors, the key question is whether this news will show up in Tesla’s near-term earnings and share price.

In practical terms, the 16GW VPP announcement is unlikely to contribute materially to this quarter’s revenue.

Partnership structuring, customer integration, power market agreements, data center demand identification, and regulatory approvals will all take time.

Accordingly, it should not be viewed as an immediate catalyst for a sharp share price rally.

However, it is strategically significant over the long term.

Whether the market values Tesla as an automaker or as an infrastructure company that solves AI data center power demand could materially change the company’s valuation.

10. Cybertruck ranks first in U.S. pickup safety evaluations

Tesla also received another positive development.

The Insurance Institute for Highway Safety released its 2026 pickup safety rankings, and the Cybertruck received the Top Safety Pick+ designation.

It was cited as the only pickup model to receive the highest safety rating.

IIHS is a highly regarded safety evaluator that U.S. consumers closely follow when making vehicle purchases.

The Cybertruck reportedly performed well in major tests including small front overlap, moderate front overlap, side impact, headlight performance, and pedestrian crash avoidance.

Notably, it passed pedestrian automatic avoidance testing without a collision.

The report stated that it successfully avoided collisions in scenarios involving children crossing during the day, adults crossing at night, and adults walking at night from the side.

11. Why the Cybertruck safety result matters for robotaxi plans

The Cybertruck’s safety rating is unlikely to move Tesla shares meaningfully on its own.

However, it matters for confidence in autonomy and robotaxi deployment.

The central question in robotaxi adoption is whether passengers are willing to trust the vehicle.

No matter how strong the software, mass adoption is difficult if consumers do not perceive the vehicle as safe.

The Cybertruck faced early criticism over crash safety due to its angular stainless-steel design.

Now that it has received strong official safety results, Tesla has another data point supporting vehicle safety.

This is particularly relevant as Tesla prepares for robotaxi, Cybercab, and broader FSD adoption.

12. Texas Autopilot fatal-accident lawsuit: the market concern

There is also negative news.

A civil lawsuit has been filed in connection with a Model 3 accident in Harris County, Texas.

The accident reportedly occurred on Friday, June 20, U.S. time.

A Tesla Model 3 allegedly drove into a residence in a residential area, resulting in the death of a 76-year-old woman.

The victim’s daughter and son-in-law filed suit against Tesla and the driver on June 24.

The plaintiffs allege product defects and failure to warn.

They are also seeking preservation of Tesla black box data, Autopilot system data, and camera footage from the time of the accident.

13. The key issue: system failure or manual driver override

The central question is how the vehicle was being controlled at the time of the crash.

A Tesla AI executive reportedly argued that the driver manually overrode the system by pressing the accelerator pedal 100%.

The plaintiffs’ counsel has rejected that explanation.

The argument is that if the accelerator remained fully depressed until the vehicle came to a complete stop after impact, it would be difficult to reconcile with the claim that the driver’s foot remained in a normal position.

Harris County authorities said they found no evidence of mechanical failure, but the National Highway Traffic Safety Administration has opened a special investigation.

In the end, black box data, vehicle logs, Autopilot data, and camera footage are likely to be decisive evidence.

14. Impact of the lawsuit on robotaxi plans

It would be excessive to conclude that a lawsuit involving Autopilot will immediately derail Tesla’s FSD-based robotaxi plans.

The incident involved a vehicle with a driver, and the dispute centers on whether the driver intervened manually.

Robotaxi, by contrast, is designed as a fully autonomous model without a human driver.

The technical, legal, and operational frameworks are different.

However, the public may not distinguish between them.

Repeated headlines such as “Tesla autonomy accident” or “Autopilot fatal crash” could affect consumer trust.

Regulators may also become more cautious toward autonomy more broadly.

As a result, the case is important not only for the legal outcome, but also for the social acceptance of Tesla’s robotaxi ambitions.

15. Main takeaway: the headline is the lawsuit, but the structural story is power infrastructure

Most attention today is centered on the Autopilot lawsuit.

However, the more important structural shift is the 16GW virtual power plant announcement.

The lawsuit represents near-term uncertainty.

The VPP, by contrast, could reshape Tesla’s business identity over the long term.

The key issue is whether Tesla is transitioning from an EV company to an energy infrastructure company that helps meet AI data center power demand.

As the AI industry grows, electricity shortages are likely to become more severe.

As semiconductor earnings improve and data center investment expands, grid investment becomes a necessity.

In that environment, Tesla Energy could emerge as a core growth engine rather than a side business.

16. The most overlooked point in this news

The most important point is not the 16GW figure itself, but the fact that Tesla is moving from generating electricity to managing when electricity is used.

In future power markets, the real value will not come only from building more plants.

It will increasingly come from deciding when to charge, when to discharge, which customers receive power, and when demand should be reduced.

In other words, grid optimization becomes a new source of revenue.

Tesla has EVs, Powerwall, Megapack, Superchargers, FSD, and AI software.

This combination is different from that of a pure battery company or a pure utility company.

Once EV batteries are linked to the grid, Tesla could become a platform operator managing millions of mobile batteries.

The key question is whether the market has fully priced this in.

Tesla’s $375 share price may already reflect much of the concern over weaker auto sales.

However, the value of AI data center power demand, virtual power plants, energy storage systems, and grid optimization remains unresolved.

Ultimately, Tesla’s valuation may shift from “how many EVs it sells” to “how much of the AI-era power grid it controls.”

17. Key investment watch points

First, monitor whether Q2 deliveries exceed Wall Street’s estimate of about 397,500 units.

Vehicle deliveries remain the most direct short-term driver of Tesla shares.

Second, track whether energy segment revenue and margins remain intact.

If energy margins hold, Tesla’s overall profitability profile could change.

Third, assess how quickly the 16GW VPP project translates into contracted revenue.

There is a lag between announcement and earnings contribution.

Fourth, monitor how vehicle logs and camera data are interpreted in the Autopilot lawsuit.

The outcome may affect robotaxi regulation and consumer trust.

Fifth, watch the pace of AI data center power demand growth.

The stronger that trend, the greater Tesla Energy’s strategic value.

< Summary >

Tesla closed at $375.53, but the more important story is the 16GW virtual power plant announcement rather than the Autopilot lawsuit.

Tesla will work with Sunrun and Renew Home to build the largest distributed virtual power plant in the United States.

16GW is roughly equivalent to the power management capacity of about three large Korean nuclear plants.

As AI data center power demand rises, Tesla Energy is emerging as a new growth engine.

Energy margins are significantly higher than automotive margins.

The Cybertruck received the top pickup safety rating from IIHS, which is supportive for robotaxi credibility.

The Texas Autopilot lawsuit is a near-term uncertainty, with vehicle data and manual intervention remaining the key issues.

Ultimately, Tesla’s future valuation may depend on whether the market sees it not as an EV company, but as an AI-era power grid and energy infrastructure platform.

[Related Articles…]

- Tesla Energy and the case for re-rating

- AI data center power demand and the global infrastructure shift

*Source: [ 오늘의 테슬라 뉴스 ]

– 오토파일럿 소송이 헤드라인 차지한 날, 테슬라가 조용히 미국 최대 가상발전소 만든 이유 — $375 지금 어떻게?

● AI-Bubble-Myth, Power-Grid-Crunch, SMR-Boost

The Real Variable Beyond the AI Bubble Debate: Semiconductors, Data Centers, Power Constraints, and SMRs Must Be Viewed Together

It is easy to miss the core issue if the AI market is reduced to a simple debate over whether it is a bubble.

The more important point is not how much AI stocks have risen, but that bottlenecks are already emerging across GPUs, HBM, data centers, power grids, and cooling infrastructure before AI has fully entered broad-based adoption.

This report summarizes why the AI bubble argument may be overstated, why AI infrastructure investment is likely to continue, and which sectors are most likely to attract capital going forward.

The key issue often overlooked in other coverage is not whether AI demand will fade, but whether physical infrastructure can keep pace with the speed of AI expansion.

From this perspective, semiconductors, data centers, power constraints, SMRs, offshore data centers, and on-device AI are all part of the same structural trend.

1. Why the AI Bubble Argument Appears Premature

The central question in the AI bubble debate is whether there is real substance behind the market move.

Unlike the dot-com bubble, which involved significant capital flowing into companies with limited revenue models and weak operating businesses, generative AI is already delivering measurable productivity gains in work, content creation, coding, search, and data analysis.

In other words, capital is not flowing into a vacuum; it is concentrating around an ongoing industrial transition.

- AI tools are already changing office productivity.

- Companies are increasing internal experiments and investment for AI transformation, or AX.

- Real demand is emerging in semiconductors, cloud services, data centers, and power infrastructure.

- AI agents, physical AI, and on-device AI remain at an early stage of adoption.

For that reason, it is still too early to conclude that AI is in a bubble.

The current phase is better understood as Stage 1 of AI industrial expansion.

2. Current AI Is in Stage 1: Building Infrastructure to Train Human Knowledge into AI

AI should be viewed not as a fully mature service layer, but as a phase of infrastructure buildout.

For AI to penetrate manufacturing, finance, education, logistics, healthcare, retail, and public services, it must first absorb human knowledge and data.

That process requires AI infrastructure.

- GPUs are required for AI training.

- HBM is required to maximize GPU performance.

- Large-scale data centers are required to process massive workloads.

- Power infrastructure is required to operate data centers reliably.

- Cooling and energy-efficiency technologies are required to manage heat.

Accordingly, AI investment is not limited to software companies.

It is expanding into a broad ecosystem that includes semiconductors, power grids, construction, energy, telecommunications, cloud infrastructure, nuclear power, and cooling systems.

3. Why the “AI Is Still at the City Phone Stage” Analogy Matters

AI should not be viewed as a completed smartphone-era platform.

It is still closer to the early mobile-phone stage, when PCS and city phones signaled the beginning of a mobile transition, rather than its maturity.

Today, people may feel that the AI era has already arrived through chatbots, image generation, document summarization, and coding assistance.

However, the true AI era begins when AI is deeply integrated across manufacturing and service industries.

- Manufacturing AX across industrial sectors has not yet reached full-scale adoption.

- Service-sector AX in finance, education, retail, logistics, and healthcare remains early.

- The share of enterprise work environments using AI agents in a meaningful way is still low.

- Physical AI robots have not yet become dominant in factories or daily environments.

AI should therefore be seen not as a finished theme, but as a long-duration structural growth trend only beginning to spread into industrial operations.

4. Robot Vacuums and Service Robots Are Not Yet True Physical AI

Many observers assume that service robots in restaurants or robot vacuums in homes already represent mainstream physical AI.

In the current context, however, most of these systems are closer to algorithm-based automation than to true AI.

Physical AI goes beyond simple obstacle avoidance. It must integrate language and vision, interpret context, make judgments, and convert them into action.

| Stage | Characteristics | Current Examples |

|---|---|---|

| Level 1-2 | Reactive AI | Obstacle detection, basic avoidance, fixed-path movement |

| Level 3 | Integrated language and vision-based decision-making | Understanding human instructions and adapting actions to object characteristics |

| Level 4 | Human-like sensory interpretation and advanced motion control | Humanoid robots, advanced industrial physical AI |

Physical AI is currently moving toward Level 3.

Once Level 4 humanoids and industrial robots become commercially meaningful, AI demand could expand far beyond current levels.

At that point, AI semiconductors and data centers become not just expectations, but essential industrial infrastructure.

5. The AI Full-Stack Structure: If Infrastructure Is Constrained, Services Are Constrained

The AI industry can be understood in three layers.

- AI infrastructure: GPUs, HBM, data centers, cloud, and power grids

- AI models: generative AI models, multimodal models, inference models

- AI services: chatbots, AI agents, on-device AI, vertical AI solutions

This structure can be described as the AI full stack.

The issue is that even when service demand rises, AI transformation slows if infrastructure cannot keep up.

That is why NVIDIA GPUs, SK Hynix HBM, and Samsung Electronics’ AI semiconductor strategy remain in focus.

As AI services expand, upstream infrastructure demand rises in parallel, creating semiconductor price pressure and supply shortages.

6. The AI Bottleneck Is Shifting from GPUs and HBM to Data Centers

The initial AI bottleneck was GPUs.

Companies needed high-performance GPUs to train AI models.

The next bottleneck shifted to HBM.

High-bandwidth memory became necessary to fully utilize GPU performance.

As GPU and HBM supply improves, the next bottleneck becomes data centers.

- Buying GPUs does not immediately enable large-scale AI operations.

- Physical space is required to install and operate GPUs.

- Servers, networks, cooling, security, and power systems are required.

- Permitting and local power supply constraints must also be resolved.

There are currently more than 11,000 data centers worldwide.

Some forecasts suggest that this number could roughly double by 2030.

That would imply dozens of new data center plans being advanced globally each day.

7. The Next Bottleneck After Data Centers Is Power Shortage

The most underestimated variable in AI is electricity.

Data centers are not ordinary buildings; they are large industrial facilities with extremely high power consumption.

AI training and inference, in particular, require large-scale operation of high-performance chips, driving rapid growth in electricity demand.

The problem is that power supply cannot expand at the same speed as data center deployment.

- Even building a thermal power plant usually takes several years.

- A large nuclear plant typically requires around a decade from design to operation.

- National power grids are not infrastructure that a single company can expand unilaterally.

- AI data center expansion plans are being announced on a one- to two-year cycle.

This gap in pace is the core reason for the emerging power constraint in the AI era.

In some U.S. states, competition to attract data centers is increasingly creating grid pressure.

There is also rising concern that power supply and demand could become misaligned in some regions around 2027.

8. The AI Race Is Ultimately a Data Race and an Energy Race

Although AI competition appears to be a model-performance race, it is in practice an infrastructure race.

Who can secure more data, operate more compute, and access more stable power may determine the competitiveness of companies and countries alike.

For that reason, AI is not just a technology theme. It is linked to capital markets, energy security, industrial policy, and national economic outlooks.

- Competition among AI models leads to competition for GPUs.

- GPU competition expands into competition across HBM and semiconductor supply chains.

- Semiconductor competition extends into data center capacity.

- Data center competition spills into power grids and energy mix strategies.

In the end, the next major AI investment theme may be stable access to electricity.

9. Why SMRs Are Re-Emerging as a Strategic Theme in the AI Era

One of the most discussed responses to the power shortage is the SMR, or small modular reactor.

SMRs are modular nuclear reactors built at a smaller scale than conventional large reactors.

The key advantage is their ability to be delivered in a packaged, repeatable format.

While large nuclear plants face long permitting and construction timelines, SMRs are expected to be deployable over shorter periods.

- They may serve as distributed power sources near AI data centers.

- Their decision-making and construction timelines may be shorter than those of conventional nuclear plants.

- They can help address both carbon-reduction goals and stable power supply needs.

- They may be viewed as strategic assets in the restructuring of the energy mix.

The relevance of SMRs in the AI era is not simply that they are a nuclear theme.

They are emerging as one of the more practical options for meeting data center power demand.

If AI infrastructure expansion continues, investment and policy support for SMRs may remain in place over the long term.

10. Changes in the Energy Mix Can Also Affect Sovereign Yields and Capital Markets

Power infrastructure investment requires large-scale national capital expenditure.

Data centers, power grids, generation assets, transmission systems, renewables, nuclear power, and SMRs all require substantial funding.

If governments increase bond issuance and fiscal investment to restructure energy supply, that can also affect interest rates.

AI is therefore not only a technology-sector issue.

It may become a variable that influences future rate expectations, sovereign bond markets, inflation pressure, and industrial policy.

11. A Second Solution Is as Important as More Power: Reducing Consumption

Solving the data center issue does not depend only on adding more electricity supply.

Reducing electricity consumption is also critical.

A major source of data center power usage is not only server computation, but also cooling.

When GPUs and servers operate at scale, they generate substantial heat, and significant power is required to remove it.

For this reason, cooling efficiency is becoming a core competitive factor in AI infrastructure.

12. Why Offshore and Space-Based Data Centers Are Being Discussed

Offshore data centers are based on installing servers at sea or using marine environments to improve cooling efficiency.

The concept is that placing hot equipment in colder seawater conditions can reduce cooling costs.

Global companies and research institutions are already testing or piloting offshore data center concepts.

In Korea, experimental plans for offshore data centers have also been discussed near Ulsan.

Space-based data centers are also being mentioned as a long-term alternative.

Although many technical challenges remain before commercialization, the broader point is that AI infrastructure is encountering limits in terrestrial grids and cooling systems and is beginning to search for new deployment environments.

13. The Themes Advanced by Jensen Huang: Physical AI, AI PCs, and On-Device AI

The direction emphasized by NVIDIA’s Jensen Huang is also linked to AI’s next phase.

While AI has so far been cloud-centric, on-device AI may become increasingly important as processing shifts into endpoint devices.

As AI PCs, AI smartphones, AI robots, and AI vehicles expand, part of inference processing may move away from data centers and into individual devices.

This trend may reduce some data center load while simultaneously increasing total AI usage.

- AI PCs may reshape individual work environments.

- On-device AI has advantages in privacy and response latency.

- Physical AI may expand into robotics, factories, logistics, and automotive applications.

- AI agents may change how office and service-sector work is performed.

Cloud AI and on-device AI should therefore be viewed as complementary rather than mutually exclusive.

14. Key Sectors to Watch from an Investment Perspective

AI investment flows should follow the location of emerging bottlenecks rather than short-term stock volatility.

Based on current and likely future constraints, the key sectors to monitor are as follows.

- GPUs and AI semiconductors: high-performance compute chips led by NVIDIA

- HBM and memory semiconductors: the high-bandwidth memory supply chain, including SK Hynix and Samsung Electronics

- Data centers: cloud, servers, networks, construction, and operating infrastructure

- Power infrastructure: transmission, transformers, power equipment, and grid upgrades

- SMRs and nuclear power: stable power sources to address AI-era electricity constraints

- Cooling technologies: immersion cooling, liquid cooling, and offshore data center solutions

- On-device AI: AI PCs, AI smartphones, and edge AI chips

- Physical AI: humanoid robots, industrial robots, autonomous driving, and smart factories

The key point is that AI is not simply a short-lived market theme. It is generating a broader capital expenditure cycle across multiple industries.

15. The Most Important Point Often Missed by Other Media

The most important issue is not whether AI is in a bubble, but whether the pace of AI expansion is misaligned with the pace of physical infrastructure buildout.

AI models and services can scale quickly because they are software.

But data centers, power grids, generation assets, and cooling systems are physical infrastructure.

They take time, require permits, and must align with local acceptance, environmental regulation, and national power planning.

This mismatch will become the real bottleneck for the AI industry.

It may also delay any collapse in the AI market, because infrastructure shortages prevent supply from expanding too quickly and instead force demand to be absorbed over time.

In other words, the AI market is less a bubble that expands too fast and bursts than a market that wants to expand quickly but must keep investing because infrastructure cannot keep up.

This is the key framework for understanding semiconductors, data centers, power constraints, SMRs, energy-mix shifts, and capital-market flows in AI.

16. Key Watch Points Ahead

- How quickly AI agents are adopted in enterprise workflows

- When physical AI and humanoid robots begin meaningful deployment in manufacturing and logistics

- When HBM supply constraints ease

- Which regions first encounter permitting and power-supply bottlenecks for data centers

- The pace of power infrastructure investment in the U.S., Korea, Europe, and the Middle East

- The commercialization timeline for SMRs and the strength of policy support

- The pace of adoption of efficiency technologies such as offshore data centers, immersion cooling, and on-device AI

AI is no longer simply a matter of whether people use chatbots.

In the broader economic outlook, AI should be viewed as a central variable that influences semiconductor supply chains, energy security, power infrastructure, and capital-market flows simultaneously.

< Summary >

The AI bubble argument appears premature.

AI is still in Stage 1, centered on training human knowledge into AI rather than full-scale industrial penetration.

The bottleneck is shifting from GPUs and HBM to data centers, and then to power constraints and cooling infrastructure.

As data center expansion accelerates, power grids, SMRs, nuclear power, and energy-mix restructuring become more important.

Physical AI, AI agents, and on-device AI remain early-stage, but their broader adoption could further increase AI infrastructure demand.

The key issue is not weak AI demand; it is that physical infrastructure is not keeping pace with AI expansion.

Accordingly, investors should monitor not only AI semiconductors, but also data centers, power infrastructure, SMRs, and cooling technologies.

[Related Articles…]

- AI Infrastructure Investment and the Global Economic Outlook

- SMRs and the Energy Investment Opportunity Created by Data Center Power Constraints

*Source: [ 경제 읽어주는 남자(김광석TV) ]

– AI 버블? 아직 시작도 안 됐습니다 거품론이 틀린 이유 | 경읽남과 토론합시다 | 김상윤 교수 [2편]