● AI Shock, Big Tech Pullback, Capex Slowdown

Has the AI investment pace started to moderate? Changes in Big Tech AI infrastructure spending and key July U.S. market variables

The core issue in this market is not simply whether Nvidia rises or semiconductors fall.

The more important question is whether Big Tech will continue accelerating AI infrastructure investment or begin slowing the pace due to cost pressure.

Recent U.S. market action has seen sharp daily swings in semiconductor, memory, data center, neocloud, and power infrastructure stocks.

On the surface, these appear to be company-specific moves, but in practice they reflect a reassessment of the AI infrastructure investment cycle ahead of Big Tech earnings releases.

In particular, if late-July earnings confirm AI capex, cloud profitability, data center leasing strategy, and AI cost control, the direction of semiconductor and AI infrastructure stocks could diverge significantly again.

Today’s key points are fourfold.

First, why Meta and SoftBank are moving into AI computing sales.

Second, why the internal culture of unlimited AI spending at Big Tech is changing.

Third, why the token index, a leading indicator for AI investment on Wall Street, has weakened.

Fourth, why late-July Big Tech earnings are the most important inflection point for this AI investment cycle.

1. Market backdrop: AI infrastructure stocks and semiconductors are moving as one group

The most notable feature of the recent market is that AI infrastructure names are reacting more to sector-wide flows than to individual earnings or headlines.

Memory semiconductors, CPU semiconductors, semiconductor equipment, data centers, power infrastructure, and neocloud companies are moving in the same direction.

One day AI infrastructure stocks surge, and the next day they fall as Big Tech rebounds, creating a persistent rotation-driven market.

This is a difficult environment for investors.

Stock prices are swinging sharply based less on fundamentals and more on the possibility that AI investment growth may slow.

Even when the broader U.S. market is strong, AI infrastructure stocks have shown uneven performance.

This indicates that the market is shifting from the view that AI is universally positive to the question of whether AI investment can continue at the current pace.

2. The key variable is the change in Big Tech behavior

Big Tech is the primary driver of the current AI infrastructure investment cycle.

Amazon, Microsoft, Google, and Meta must build data centers, purchase GPUs, sign power contracts, and expand cloud infrastructure for semiconductor and AI infrastructure companies to maintain revenue expectations.

For that reason, the market is highly sensitive to how much these companies spend.

The more important issue is not the absolute level of investment, but the rate of change.

Investment levels may still rise, but if the pace of increase is slower than expected, heavily owned AI infrastructure stocks could face near-term pressure.

That is why the market is awaiting Big Tech earnings.

If late-July results show that Big Tech intends to increase AI infrastructure spending further, AI semiconductors and data center-related stocks could react strongly.

By contrast, if companies emphasize efficiency, cost optimization, reprioritization, or profitability management, the market is likely to interpret that as a signal of slower investment momentum.

3. Meta and SoftBank’s cloud expansion: positive or negative?

One of the recent market-moving developments is that Meta and SoftBank have shown interest in AI computing sales.

The existing cloud market has effectively been dominated by Amazon AWS, Microsoft Azure, and Google Cloud.

Now Meta and SoftBank are also considering leasing or selling data center resources to external customers, which has led to mixed market interpretation.

In simple terms, this means entering the AI cloud business as well.

Meta is reportedly evaluating a plan to sell AI compute resources to external customers through its AI compute projects.

One rationale is that some of Meta’s data center capacity is not fully utilized, and monetizing excess compute could create new revenue.

One estimate suggests that about 65% of Meta’s data center resources are in use, while roughly 35% may be available.

The market has interpreted this in two ways.

The negative view is that AI compute may not actually be as scarce as claimed.

The positive view is that Meta would not enter this business unless it saw an opportunity to monetize spare capacity.

In the near term, this is more likely to be viewed as a positive development.

However, medium- to long-term supply overhang risk must also be considered.

If SpaceX, Meta, SoftBank, and existing Big Tech firms all enter AI data center services, compute supply could expand rapidly in a few years.

At present, AI semiconductors and power supply remain constrained, but by 2028 and beyond, data center oversupply concerns could emerge in some segments.

4. SoftBank’s SB Neo and neocloud competition

SoftBank is also moving toward AI computing sales in the U.S. through SB Neo.

Plans to secure 10 GW of data center capacity by 2030 indicate intensifying competition in the neocloud segment.

Neoclouds are GPU-focused cloud providers dedicated to AI workloads, unlike the broader platforms operated by AWS, Azure, and Google Cloud.

As demand for model training and inference has surged, a market for renting GPUs has expanded, allowing new entrants to emerge quickly.

SoftBank’s push to secure large-scale AI computing infrastructure in the U.S. reflects this trend.

Even without building AI models itself, providing the infrastructure to run them can generate stable rental income.

This is supportive for the data center industry.

But investors must still assess both demand expansion and potential supply excess.

In the early stage, more supply can support AI semiconductor demand.

Over time, however, excessive data center buildout could pressure lease rates and profitability.

5. The SpaceX case and the market’s mixed reaction

An interesting point is that when SpaceX announced a similar AI computing leasing strategy, the market treated it as a positive catalyst.

When reports suggested SpaceX would provide data center compute to Google or Anthropic, the reaction focused on stronger AI semiconductor demand.

By contrast, Meta’s similar move has prompted some investors to ask whether compute capacity is already becoming excessive.

The reason for the different reaction is that market sentiment has changed.

Earlier this year, the market viewed AI infrastructure investment expansion as uniformly positive.

Recently, however, concerns about Big Tech profitability, shareholder pressure, and AI cost control have led investors to interpret the same news more cautiously.

That is the key feature of the current market.

The interpretation framework has changed more than the news flow itself.

6. The most important change: from token maxing to token mining

A major point often missed in other coverage is that AI spending behavior is changing.

In April and May, many companies were focused on maximizing AI usage.

Some firms even displayed employee AI usage on dashboards and offered incentives for higher usage.

The market described this as token maxing.

In other words, “the more AI use, the better.”

But by June, the tone had changed.

Big Tech and other large companies began controlling AI usage, evaluating cheaper models, and focusing more on cost versus productivity.

This can be viewed as token mining, or AI spending minimization and cost optimization.

This is a more important development than a short-term headline.

The AI infrastructure cycle is ultimately determined by usage and cost structure.

If AI users begin to feel cost pressure, demand growth for premium models and high-performance GPU infrastructure could slow.

7. Tesla and SpaceX have also moved to limit AI spending

Reports indicate that companies led by Elon Musk, including Tesla and SpaceX, have begun limiting employee AI spending.

Previously, employees may have used AI tools costing thousands of dollars per week without much scrutiny.

More recently, spending caps of around $200 per week have been discussed, with approval required for additional usage.

If accurate, this is a meaningful signal.

It suggests that even the most aggressive AI users are beginning to control costs.

Musk still emphasizes the importance of AI compute.

He has argued that sufficient AI compute resources could quickly alter the ranking of current AI models.

In other words, the strategic importance of AI infrastructure remains intact, while internal operating expenses are being managed separately.

These are not contradictory positions.

The message is that AI compute remains important over the long term, but indiscriminate near-term AI usage costs are being reduced.

8. Amazon and Anthropic: AI model cost pressure is becoming real

Amazon has also been reported to be reviewing lower-cost alternatives in response to Anthropic-related spending pressure.

The key issue is the billing structure.

If the model shifts from a time-based pricing structure to a usage-based structure, it may effectively amount to a price increase for heavy AI users.

For Amazon, which deploys high-performance AI models at scale, cost pressure could rise materially.

This is why companies are increasingly evaluating in-house models, lighter models, competing models, or lower-cost AI alternatives.

This is an important shift for both the cloud industry and the AI model industry.

Once model performance competition matures, the next phase is inevitably cost-efficiency competition.

Even when AI improves productivity, if costs rise too quickly, CFOs and shareholders will push back.

9. Why Microsoft is also considering Chinese AI models

Microsoft has also been linked to discussions about lower-cost AI models as part of its cost reduction efforts.

Some reports have even mentioned the possibility of using Chinese AI models or open-source models.

This is not merely a technical choice.

It can be viewed as part of Microsoft’s effort to strengthen its bargaining power against AI model providers.

If frontier model companies such as OpenAI or Anthropic keep prices elevated, cloud providers can counter by signaling that alternative models are available.

This is similar to how Apple may reference alternative suppliers in memory negotiations to pressure Samsung Electronics or SK hynix.

Companies ultimately have to protect profitability.

Even if AI is strategically important, they will seek alternatives if the cost structure becomes unsustainable.

10. The significance of Palantir’s CEO criticizing pricing

Palantir’s CEO recently criticized the pricing models of OpenAI and Anthropic.

While the remarks may have seemed aggressive on the surface, the market interpreted them as a reflection of broader corporate frustration with AI costs.

He argued that frontier AI model companies are too expensive and can waste both time and money for enterprise users.

Palantir also had its own commercial incentives for making such comments.

But the key point is that the message appears to resonate with the market.

If enterprise customers are becoming more sensitive to model usage fees, that could also affect the pace of AI infrastructure demand growth.

Cost optimization is now a central issue for both AI software firms and AI infrastructure providers.

11. Meta’s internal concern: pressure from being behind in model competition

Reports based on internal Meta meeting recordings suggest that Zuckerberg acknowledged AI agent development had not progressed as expected this year.

Meta has continued hiring AI talent, reorganizing teams, and expanding infrastructure spending, but there is growing concern about the pace of OpenAI and Anthropic.

This is relevant to Meta’s strategy.

If it is difficult to secure a clear lead in model competition, Meta may shift part of its focus toward monetizing data center and AI compute infrastructure.

In other words, this does not mean Meta will stop investing in AI.

Rather, it suggests a possible move from a strategy of indiscriminately pouring capital into model development toward one that seeks returns through infrastructure monetization.

The market may interpret this as a sign of slower AI investment growth.

12. Wall Street’s leading indicator for AI investment: the token index has weakened

Wall Street is paying close attention to the token index as a leading indicator for AI investment.

In simple terms, this metric reflects whether companies remain willing to invest in AI despite high costs.

When the token index rises, it suggests strong willingness to spend on AI regardless of cost.

When it falls, it indicates that AI costs are becoming burdensome and that companies may evaluate cheaper or alternative models.

Recent commentary suggests the index has declined about 20% from its peak, increasing market caution.

The recent rise in AI infrastructure stock volatility since June is likely not unrelated to this trend.

One indicator does not determine the entire market.

But when valuations are already elevated, even a slowdown in a leading indicator can provide a reason for profit-taking.

13. Shareholder pressure on Big Tech is also rising

Big Tech now faces the challenge of sustaining AI investment while also protecting stock performance and profitability.

Some Big Tech names have underperformed from their highs this year, and shareholders are demanding evidence of AI returns.

In the past, buybacks or dividends were tools to support valuations.

Now, AI spending has grown so large that investors are asking when it will translate into earnings.

As a result, Big Tech management must deliver two messages in late-July earnings.

One is that the company will not fall behind in AI competition.

The other is that it will manage profitability and costs.

The risk is that if the market emphasizes the second message too strongly, AI infrastructure stocks could face near-term pressure.

14. A Bill Ackman-style view: cloud Big Tech could be re-rated

Some hedge fund investors argue that this may be the right time to revisit Big Tech cloud companies.

The logic is straightforward.

It remains unclear which AI model company will emerge as the final winner.

It will take more time to determine whether OpenAI, Anthropic, Google, Meta, or xAI prevails.

However, regardless of the model winner, cloud infrastructure and data centers will still be required.

For that reason, Amazon, Microsoft, and Google may be viewed as collecting tolls across the AI ecosystem.

If AI model cost optimization continues, companies may move away from relying only on the most expensive models and instead combine models based on use case.

In that environment, the value of cloud platforms offering multiple models and infrastructure options could rise.

In other words, slower AI infrastructure spending does not have to be negative for Big Tech as a whole.

It could instead lead to a re-rating of cloud profitability.

15. Michael Burry’s warning: a bubble signal or excessive pessimism?

Michael Burry recently expressed a negative view on the AI investment cycle and pointed to possible peak-cycle signals.

He has taken a cautious stance on semiconductors, AI infrastructure, and equipment suppliers, and has reportedly viewed Korea’s semiconductor megaprojects as late-cycle developments.

Burry is known for making highly contrarian warnings.

For that reason, his views should not be followed mechanically.

Still, in a market that has already risen significantly, such bearish commentary can increase short-term volatility.

This is especially relevant for investors using leveraged ETFs or other short-term trading vehicles.

Even if one believes in the long-term AI infrastructure story, short-term volatility can still materially affect portfolio performance.

16. Late-July Big Tech earnings are the real inflection point

The answer is likely to come from late-July Big Tech earnings.

The market is currently trading on assumptions.

Investors need confirmation in earnings releases and conference calls on whether Meta is slowing investment, whether Microsoft is tightening cost controls, whether Amazon is feeling model cost pressure, and whether Google is increasing data center spending further.

The most important items to watch are the following.

First, capex guidance.

Second, any increase in AI infrastructure spending.

Third, plans for data center capacity expansion.

Fourth, pressure from inference costs.

Fifth, margin pressure.

If Big Tech says it will increase AI investment further, semiconductors and data center-related stocks could regain momentum.

If the emphasis shifts to cost optimization and investment efficiency, AI infrastructure stocks may need to reset expectations in the near term.

17. Positive catalysts still remain

This environment should not be viewed in an overly negative way.

Long-term AI infrastructure demand remains strong.

Power shortages, data center bottlenecks, supply constraints in advanced semiconductors, and rising AI inference demand remain structural issues.

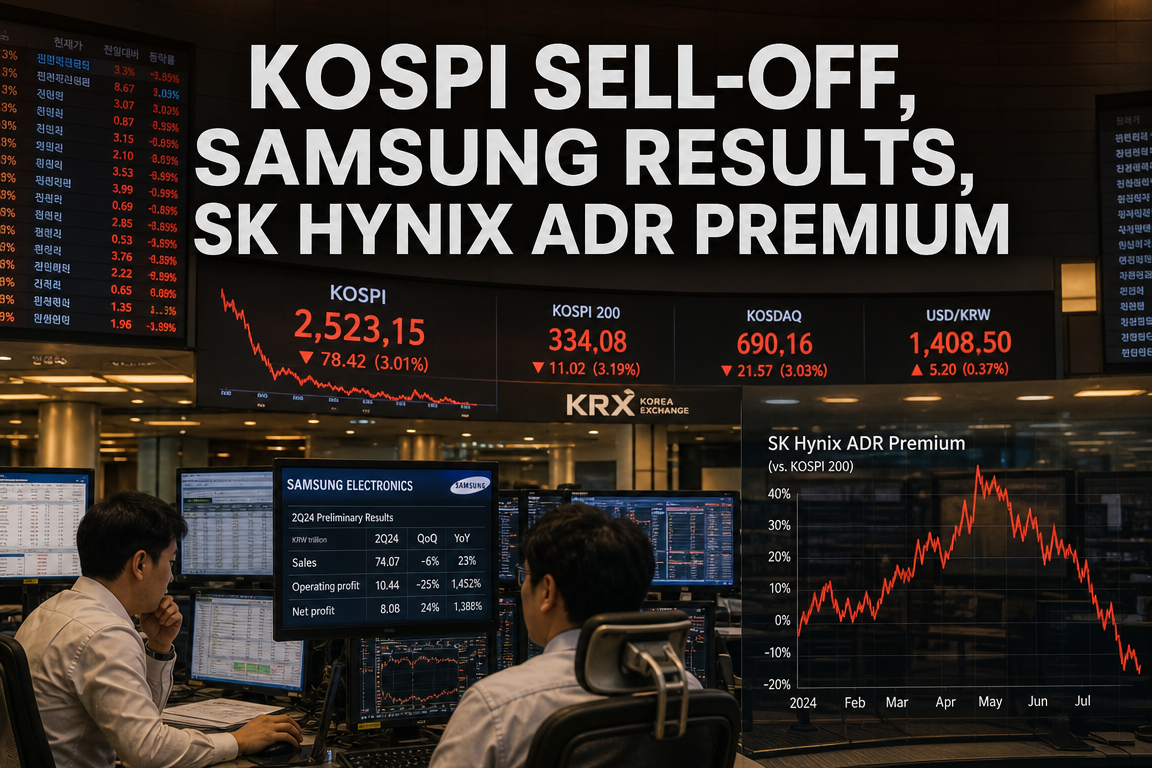

In addition, SK hynix’s U.S. ADR-related financing issue is drawing significant market attention.

If the indicated scale materializes, it could become a major event in the global semiconductor market.

Momentum in Samsung Electronics and SK hynix memory semiconductors is now influencing not only the Korean market but also global AI sentiment.

This is due to continued demand for HBM, high-bandwidth memory, and AI servers.

Separately, index inclusion issues related to SpaceX, as well as defense themes tied to space, drones, and NATO-related contracts, could also provide short-term support.

Macro factors such as post-July tariff issues, China-related restrictions, and negotiations with Canada and Mexico may also come into focus.

In short, July is a month with both positive and negative catalysts.

As a result, volatility is likely to rise before direction becomes clearer.

18. The most important point that is often overlooked

The key issue in this AI investment debate is not whether AI investment is declining.

The real question is whether the nature of AI investment is changing.

The market tends to frame the discussion as either expansion or contraction.

In reality, the change is more nuanced.

Big Tech is unlikely to stop investing in AI altogether.

That is because falling behind in AI competition would jeopardize long-term growth.

However, the industry is moving away from a stage in which companies simply call for the most expensive models, the largest number of GPUs, and the biggest data centers.

Going forward, the same AI investment may be pursued more cheaply, more efficiently, and with greater focus on profitability.

This could be a near-term headwind for AI semiconductor companies.

But it may create opportunities for cloud platforms, AI cost optimization software, lightweight models, and companies with their own proprietary models.

In other words, this may not be the end of the AI cycle, but rather a phase in which the set of winners changes within the cycle.

Investors should focus not on whether AI is over, but on where AI capital is moving next.

19. Key investment checkpoints

First, check whether Big Tech capex guidance is being revised higher in late-July earnings.

Second, watch how strongly AI cost optimization language appears.

Third, track whether the token index continues to fall or begins to recover.

Fourth, confirm whether Meta and SoftBank’s AI computing sales business is translated into actual revenue.

Fifth, observe whether semiconductor stocks are being driven more by sentiment than by earnings.

Sixth, determine whether data center supply expansion is a near-term demand tailwind or a medium-term oversupply signal.

Seventh, exercise caution with leveraged products, as both gains and losses can compound rapidly in a volatile market.

20. Conclusion: the AI infrastructure cycle is not over; it has entered a pace debate

To summarize in one sentence, the AI infrastructure investment cycle is not over; it has entered a debate over pace and efficiency.

Big Tech still has to invest in AI.

However, shareholder pressure and cost constraints are making it difficult to keep spending without limits.

That is why late-July Big Tech earnings are likely to be the most important event for the U.S. market in this period.

If increased AI infrastructure spending is reaffirmed, semiconductors and data center-related stocks could resume their advance.

By contrast, if cost control and investment efficiency become the dominant messages, the sector may face short-term corrections and continued rotation.

At this stage, portfolio management matters more than trying to call a top.

Even if the long-term AI story remains intact, short-term volatility should not be underestimated.

Ultimately, the next leg higher is likely to depend not on how much AI is used, but on how efficiently it is monetized.

< Summary >

AI infrastructure stocks have shown significant volatility as the market questions whether Big Tech is slowing the pace of spending.

Meta and SoftBank’s move into AI computing sales is supportive in the near term, but it may also raise medium-term oversupply concerns.

Corporate AI spending behavior is shifting from token maxing to token mining, meaning cost optimization is becoming a priority.

Amazon, Microsoft, Tesla, and Meta have all shown signs of AI cost control and a review of lower-cost models.

If late-July Big Tech earnings confirm higher capex, AI semiconductors and data center-related stocks could strengthen again.

If the emphasis shifts to profitability protection and cost reduction, AI infrastructure stocks may correct in the near term.

The current phase is not the end of the AI cycle, but a change in how AI investment is being deployed.

[Related Articles…]

AI Infrastructure Spending and Semiconductor Market Outlook

Cloud Profitability and Data Center Capacity Trends

*Source: [ 소수몽키 ]

– AI투자 속도 느려지기 시작? 빅테크의 변심, 불길한 신호일까

● Bitcoin-SpaceX-Burry Shock, Selloff Warning

MSTR Sells Bitcoin to Fund Dividends, SpaceX Nasdaq-100 Coverage, and Michael Burry’s Micron Short: Three U.S. Market Issues to Watch This Week

This is not a simple single-stock headline.

Reports that MSTR sold 3,588 BTC to fund dividend payments, coverage regarding SpaceX and the Nasdaq-100, and Michael Burry’s disclosed short position in Micron have all emerged at the same time.

At first glance, these appear to be separate developments. In practice, they connect U.S. equities, AI semiconductors, Bitcoin, Nasdaq-100 rebalancing, and shifts in investor sentiment.

The key point is that even in a rising market, scrutiny of cash flow and valuation has resumed.

Below is a concise investor-focused summary of the main issues.

1. MSTR Sells 3,588 BTC to Fund Dividends: A Shift in Bitcoin Strategy?

The first development drawing market attention is MSTR’s reported Bitcoin sale.

According to reports, MSTR sold 3,588 BTC to fund dividend payments.

MSTR has been viewed as an aggressive Bitcoin accumulator and, in effect, as a leveraged Bitcoin proxy.

As a result, this sale carries symbolic significance beyond simple cash management.

- A company that has continued to accumulate Bitcoin has sold part of its holdings

- The proceeds were used for dividend payments rather than new investment

- Even during a Bitcoin rally, corporate balance sheet pressures remain relevant

- MSTR’s valuation is increasingly difficult to explain solely through Bitcoin price movements

MSTR’s investment case has been straightforward: hold Bitcoin long term, raise capital through equity and debt issuance, and benefit from a re-rating as Bitcoin prices rise.

However, if BTC was sold to fund dividends, the market may increasingly view MSTR not only as a Bitcoin holder but also as a company with financing and cash flow constraints.

That means investors will need to monitor debt structure, preferred dividend obligations, funding costs, and interest rate expectations alongside Bitcoin prices.

2. What MSTR’s Sale Means for the Bitcoin Market

The reported 3,588 BTC sale is not large relative to the total Bitcoin market capitalization.

However, the key issue is not size but identity.

MSTR carries significant symbolic weight in the Bitcoin market.

Its actions have often served as a reference point for institutional sentiment toward Bitcoin.

This sale raises several questions for investors:

- Is MSTR’s Bitcoin accumulation cycle slowing?

- Could additional sales occur due to balance sheet pressure?

- Can the stock’s premium persist even if Bitcoin continues to rise?

- Does this signal a weakening in leveraged risk appetite across crypto-linked assets?

Bitcoin-related equities in the U.S. market do not move only with coin prices.

They also reflect interest rates, dollar liquidity, ETF inflows, and institutional risk appetite.

Accordingly, MSTR’s BTC sale is relevant not only to crypto but also to broader sentiment across Nasdaq growth stocks and risk assets.

3. SpaceX and the Nasdaq-100: A Critical Point Investors Must Verify

The second issue is coverage of SpaceX and the Nasdaq-100.

One report stated that SpaceX would be included in the Nasdaq-100 on the 7th.

However, there is an important factual issue to note.

SpaceX is a private company.

The Nasdaq-100 is generally composed of large non-financial companies listed on Nasdaq, so direct inclusion of a private company would not normally be feasible.

Investors should therefore distinguish between several possibilities:

- Whether the report refers to direct inclusion of SpaceX

- Whether it refers to a related listed company or partner

- Whether it concerns an ETF or listed vehicle with SpaceX exposure

- Whether it reflects a derivative or thematic product issue

- Whether it is simply a market rumor tied to future IPO expectations

This distinction matters because headlines involving private company names can quickly influence sentiment and cause short-term moves in thematic stocks.

At the same time, Nasdaq-100 inclusion is directly linked to passive fund flows, so investors must identify the actual inclusion target before drawing conclusions.

4. Why the SpaceX Issue Matters: AI, Space, and Defense Themes Are Linked

When SpaceX appears in market headlines, the story extends beyond the space sector.

SpaceX is connected to satellite communications, rocket launches, space logistics, defense contracts, internet infrastructure, and AI network infrastructure.

Starlink, in particular, can be linked to global connectivity and AI infrastructure expansion.

As AI models grow, demand rises for data centers, semiconductors, power, networking, and satellite communications.

As a result, SpaceX-related headlines can influence the following areas:

- Aerospace and launch service companies

- Satellite communications and low-Earth-orbit network companies

- Defense and national security technology stocks

- AI data infrastructure and cloud networking companies

- Nasdaq-100 large-cap technology and growth stock sentiment

Still, it must be emphasized again that SpaceX remains a private company.

Investors should assess actual contract exposure, revenue linkage, ownership relationships, and ETF structure rather than relying on theme-driven headlines.

5. Michael Burry’s Micron Short Position: A Warning Signal for the AI Semiconductor Rally?

The third key development is Michael Burry’s disclosed short position in Micron.

Burry is widely known for anticipating the 2008 financial crisis.

For that reason, any disclosed short position by him is closely watched by the market.

This time, the target is Micron, a leading memory semiconductor company.

Micron is not a direct GPU leader like Nvidia, but it has been viewed as a beneficiary of rising HBM and high-performance memory demand in the AI cycle.

As AI server deployment increases, demand rises not only for GPUs but also for HBM, DRAM, and NAND.

If Burry has taken a short position in Micron, the market will consider several possibilities:

- AI expectations may already be priced in too aggressively

- The memory cycle may be approaching a peak

- Micron’s valuation may be running ahead of earnings improvement

- The broader semiconductor rally may be extending too far beyond Nvidia

- Supply growth could reintroduce cyclical pressure

That said, Burry’s position does not necessarily imply a correct market call.

Public filings are delayed, and the disclosure date may not match the actual position timing.

In addition, a short position can reflect hedging rather than a directional bearish view.

Accordingly, “Burry is short Micron” should not be interpreted as a guaranteed forecast of decline.

6. What the Micron Short Means for the AI Semiconductor Market

The AI semiconductor sector has been one of the main drivers of U.S. equity performance in recent years.

Nvidia, AMD, Broadcom, and Micron have all benefited from strong investor enthusiasm.

Micron, in particular, has been positioned as an AI memory beneficiary due to HBM demand expansion.

However, semiconductors remain a cyclical industry.

When demand is strong, companies increase capital spending, and over time supply growth can create pricing pressure.

Burry’s short position may be aimed at this risk.

- AI demand remains strong, but valuations may have moved too far ahead

- HBM competition may pressure margins

- The memory price upcycle may prove shorter than expected

- China demand and U.S. regulatory risk may weigh on earnings

- Interest rate shifts may pressure growth stock valuations

The issue is not a rejection of AI semiconductors as a sector. It is a reminder that even strong industries can become risky when valuations rise too quickly.

7. Why These Three Headlines Are Connected

MSTR’s Bitcoin sale, SpaceX coverage in relation to the Nasdaq-100, and Michael Burry’s Micron short appear unrelated on the surface.

However, from an investment perspective, they share a common theme.

They all reflect growing scrutiny of high-growth, high-expectation assets.

- MSTR represents the market’s Bitcoin upside narrative

- SpaceX represents the future of private space and growth investing

- Micron represents a key beneficiary of the AI semiconductor cycle

These are all areas that have historically received elevated market premiums.

However, investors are once again focusing on cash flow, earnings, valuation, actual index inclusion benefits, and interest rate sensitivity.

This does not imply the end of the bull market.

It more likely signals a shift toward selective leadership, which is common in the later or middle stages of a strong market.

8. The Most Important Point Often Missed in Market Coverage

The most important takeaway is that the market is shifting from story-driven investing to structure-driven investing.

In recent years, strong narratives received high valuations: Bitcoin holdings, AI semiconductors, space industry growth, and Nasdaq-100 inclusion expectations.

Now investors are asking different questions:

- Is the company generating actual cash flow?

- Can it manage debt and dividend obligations?

- Is AI demand translating into earnings and margins?

- Does index inclusion create real capital inflows?

- Has valuation already discounted too much future growth?

MSTR’s BTC sale shows that even a Bitcoin-heavy strategy must account for cash flow.

The SpaceX Nasdaq-100 issue shows the importance of distinguishing between headlines and investable assets.

Burry’s Micron short suggests that even an AI rally can face valuation risk.

In short, the market is placing more weight on structure than on narrative.

9. Key Indicators Investors Should Watch

For this week’s U.S. market outlook, investors should monitor more than just price action.

- Further BTC sales by MSTR: Determine whether the sale was one-time or part of a recurring funding strategy.

- Bitcoin price reaction: Assess whether MSTR’s sale affects broader crypto sentiment.

- Accuracy of SpaceX coverage: Verify whether the report refers to direct inclusion, a related stock, or an ETF issue.

- Nasdaq-100 rebalancing flows: Identify which assets receive actual passive inflows.

- Micron price and earnings outlook: Track HBM demand, memory pricing, and inventory trends.

- Nvidia and AI semiconductor correlation: Determine whether the Micron headline spreads across the sector.

- Interest rate outlook: Growth stocks, Bitcoin, and AI-related names remain highly sensitive to rate expectations.

10. How to Interpret the Main Stocks

MSTR should now be evaluated not only on Bitcoin prices but also on financial structure.

Bitcoin holdings, average purchase price, debt maturities, preferred dividend obligations, and potential share issuance all matter.

Micron remains positioned as an AI memory beneficiary, but investors should assess whether the stock has already priced in strong earnings improvement.

Competition among HBM suppliers, including Samsung Electronics and SK Hynix, is also important.

SpaceX-related themes require careful analysis because direct investment is not possible. Investors should verify actual contract and revenue exposure.

Nvidia and AI semiconductors remain central to the market, but adjacent names may not advance at the same pace.

Within the AI infrastructure theme, differentiation among winners and laggards is likely to increase.

11. Outlook for the Market Ahead

The U.S. market continues to be supported by AI, Bitcoin, and large-cap technology names.

At the same time, these headlines suggest that investors are again examining risk more carefully.

Even if the Nasdaq-100 rally continues, stock-specific dispersion may widen beneath the surface.

AI semiconductors retain strong long-term growth potential, but short-term volatility will remain tied to earnings and guidance.

Bitcoin still benefits from institutional inflows and scarcity logic, but leveraged corporate structures require separate review.

The space industry remains a compelling long-term theme, but private-company headlines should not be confused with investable listed assets.

Overall, the market is not necessarily turning bearish. It is becoming more selective and more valuation-sensitive.

< Summary >

MSTR reportedly sold 3,588 BTC to fund dividend payments.

This indicates that cash flow and balance sheet pressure now matter even for Bitcoin-heavy strategies.

Coverage of SpaceX and the Nasdaq-100 must be verified carefully because SpaceX is a private company.

Michael Burry’s short position in Micron highlights valuation risk in the AI semiconductor rally.

The common theme across these headlines is that the market is placing greater emphasis on cash flow, earnings, valuation, and interest rates.

U.S. equities may continue to trend higher, but the next phase is likely to be more selective.

[Related Articles…]

- Bitcoin Investment Strategy and U.S. Equity Market Trends

- AI Semiconductor Outlook and Nasdaq Technology Stock Themes

*Source: [ Maeil Business Newspaper ]

– MSTR, 배당금 마련 위해 3588 BTC 매각ㅣ스페이스X, 7일에 나스닥100 편입ㅣ마이클버리, 마이크론 숏 포지션 공개ㅣ홍키자의 매일뉴욕